花旗看多AI光互联:2028年市场剑指920亿,新易盛目标价翻倍

- 核心观点:花旗研报预计,受AI数据中心对高速互联需求的驱动,全球光互联市场规模到2028年将达920亿美元。这一增长主要来自800G向1.6T、3.2T及CPO/NPO技术迁移,推高了高速光模块、硅光子和激光芯片需求,中国供应链最直接受益,但供应瓶颈与高估值构成制约。

- 关键要素:

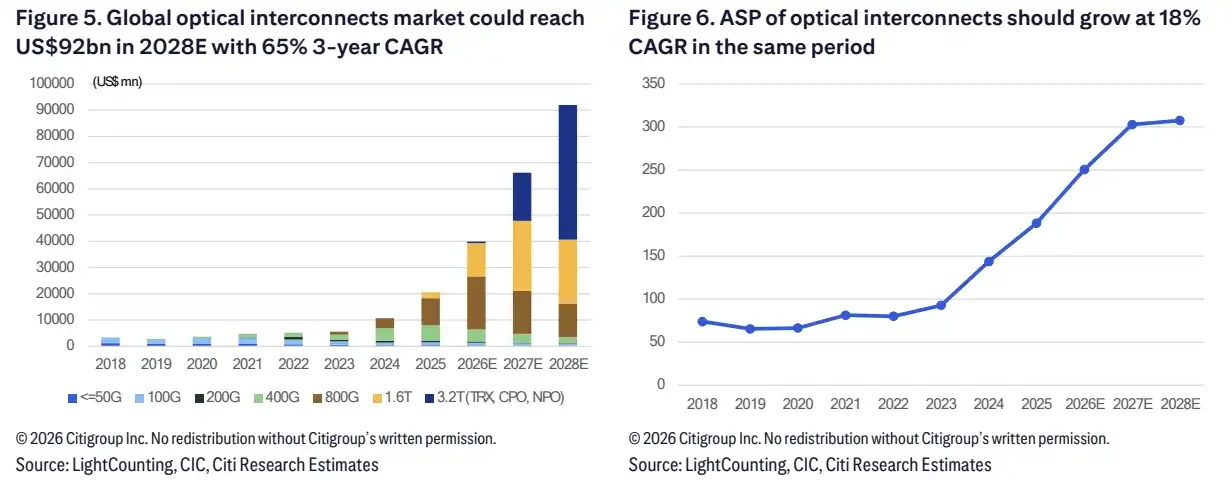

- 花旗预计2028年全球光互联市场达920亿美元,2025-2028年复合增速约65%,主要由数据中心互联需求驱动。

- 技术迭代加速,800G以上高速产品在数据中心占比预计从2025年的37%升至2028年的89%,1.6T收发器出货复合增速达215%。

- 硅光子方案在高速光模块中的渗透率将从2025年的29%升至2028年的60%,带动CW激光芯片需求复合增速达114%。

- 花旗大幅上调新易盛、东山精密和天孚通信目标价,认为AI光学业务是主要增量来源。

- 太辰光评级被下调至卖出,主要风险来自与核心客户脱钩、竞争加剧及59倍的高估值。

- 增长面临三重约束:EML/CW激光芯片供应紧张、CPO/NPO技术落地节奏不确定、部分公司估值已提前反映乐观预期。

TL;DR

- Citi predicts the global optical interconnect market will reach $92 billion by 2028, raising price targets for Eoptolink Technology, DSBJ, and TFC Communication.

- The migration from 800G to 1.6T, 3.2T, and CPO/NPO is driving demand for high-speed optical modules, silicon photonics, and laser chips.

- China's optical communication supply chain is the most direct beneficiary, but laser chip supply, yield rates, and high valuations may limit the pace of realizing gains.

Behind the $92 Billion: Data Centers Take Over Optical Interconnect Demand

In a research report on June 24, Citi raised its forecast for the AI optical interconnect market, predicting the global market size will reach $92 billion by 2028, with a compound annual growth rate (CAGR) of approximately 65% from 2025 to 2028. In the same adjustment, price targets for Chinese optical communication companies such as Eoptolink Technology, DSBJ, and TFC Communication were significantly raised.

The basis for this judgment is not complicated. As AI data centers grow larger, the amount of data that needs to be transferred between GPUs and ASICs increases, and the demand for connections between cabinets, switches, and servers will rise accordingly. High-speed optical modules, silicon photonics, and laser chips are no longer just supporting equipment for data center expansion, but key components determining whether computing power can be connected efficiently.

Citi's model shows that the average selling price (ASP) for optical interconnects is expected to have a CAGR of about 18% from 2025 to 2028, primarily driven by the increasing share of high-speed products like 800G, 1.6T, and 3.2T.

Global optical interconnect market size is projected to reach $92 billion in 2028E, with ASP maintaining an 18% CAGR from 2025-2028 before stabilizing.

After 800G: 1.6T, 3.2T, and CPO/NPO Take the Baton

General investors first need to understand a key shift: this upward revision is primarily driven by data center interconnects, not traditional telecom networks or enterprise networks.

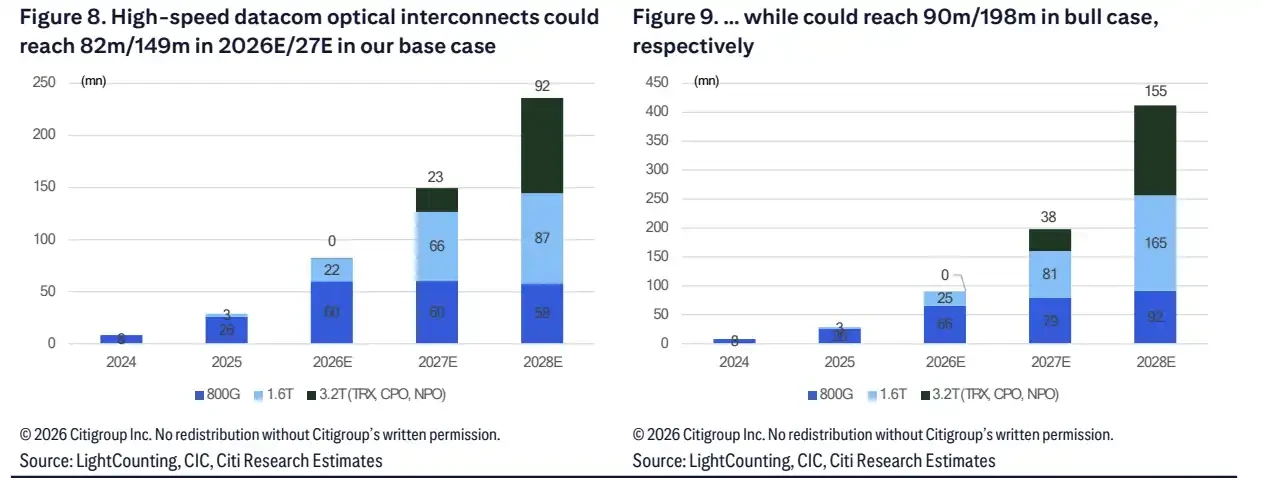

In Citi's model, global optical interconnect shipments are expected to increase from 110 million units in 2025 to 300 million units in 2028, a three-year CAGR of about 40%. The share of data center business in total shipments will rise from 71% in 2025 to 89% in 2028.

Product specifications are also moving up. The share of high-speed products above 800G in data center optical interconnects is expected to increase from 37% in 2025 to 89% in 2028. This indicates the growth is not just about "buying more optical modules," but a faster substitution of lower-speed products by higher-specification ones.

800G remains one of the mainstays in recent years, but 1.6T, 3.2T, and newer packaging solutions are growing faster. Under the base case scenario, shipments of 1.6T transceivers are expected to have a CAGR of 215% from 2025 to 2028. 3.2T will begin to ramp up from 2027, with shipments reaching 4 million units in 2027 and rising to 35 million units in 2028.

CPO and NPO represent later-stage technology migrations. Under the base case, CPO/NPO shipments are expected to reach 18 million and 56 million units respectively by 2028. Under the bull case, they could rise to 33 million and 116 million units by 2028. The significant difference between the two scenarios depends mainly on cloud provider demand, yield improvements, and the deployment pace of platform architectures from companies like Nvidia and Google.

Demand for high-speed optical interconnects diverges significantly post-2027; 1.6T and 3.2T/CPO/NPO are the main sources of elasticity between base and bull case scenarios.

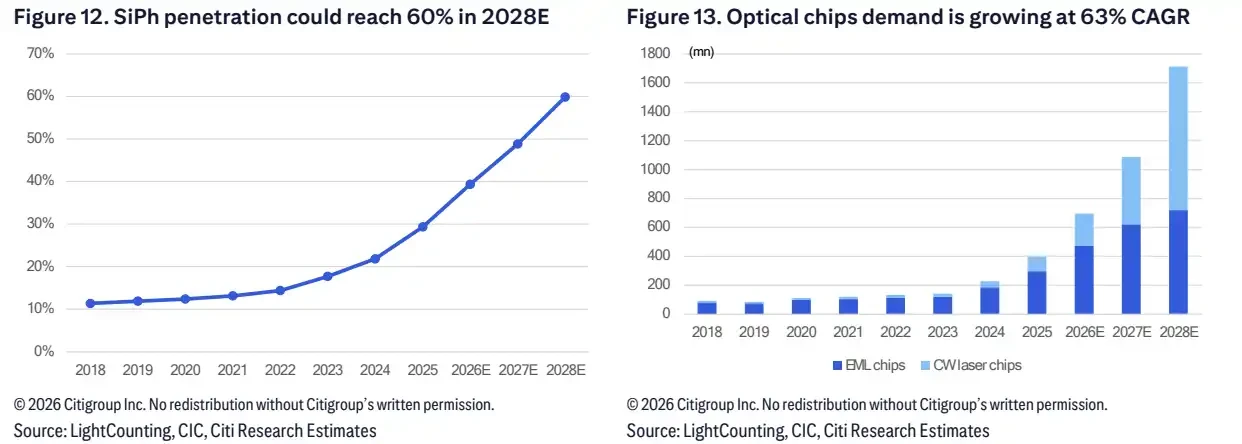

Silicon Photonics Reaches 60%: Value Shifts to Laser Chips and Optical Engines

If the $92 billion figure represents the market space, then "silicon photonics" and "laser chips" determine how this growth is distributed across the supply chain.

Citi expects the penetration rate of silicon photonics solutions in high-speed optical modules to rise from 29% in 2025 to 60% in 2028. Under this assumption, total demand for optical chips in 2028 will be approximately 1.714 billion units, with a CAGR of about 62% from 2025 to 2028.

Among these, demand for EML chips is expected to reach 718 million units, with a three-year CAGR of about 34%. CW laser chips are growing faster, with demand expected to reach 987 million units in 2028, a three-year CAGR of about 114%.

This is also the reason why supply tightness is frequently mentioned. As high-speed optical modules ramp up, bottlenecks may not necessarily occur in the module assembly stage but could appear in laser chip supply, packaging yields, and upstream capacity reservation. Pure module manufacturers securing upstream supply through long-term agreements and strategic investments are essentially positioning themselves ahead of the subsequent ramp-up of 1.6T, 3.2T, and CPO/NPO.

Silicon photonics penetration rate is expected to reach 60% in 2028E, with optical chip demand reaching ~1.714 billion units in 2028E. CW laser chip CAGR reaches 114%.

DSBJ, Eoptolink Technology, TFC Communication Upgraded; T&S Communications Downgraded

At the stock level, the most direct changes are for Eoptolink Technology, DSBJ, and TFC Communication.

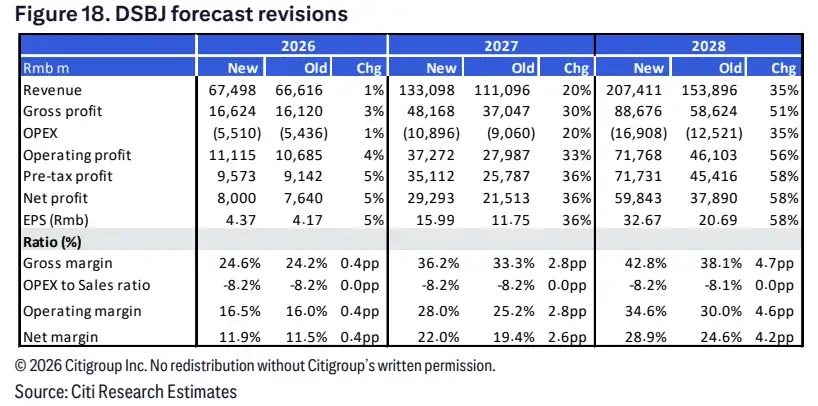

DSBJ is one of the most prominent companies in this round of upgrades. Citi raised its price target from RMB 225 to RMB 350, and increased its net profit forecasts for 2026-2028. The report indicates that the AI optical business is seen as a major incremental driver, expected to contribute significantly to profit in the coming years.

In terms of valuation, DSBJ was broken down into parts: traditional business, optical modules, optical chips, and AI PCB. This decomposition suggests that when the market looks at DSBJ, it is no longer just looking at its traditional PCB or electronics manufacturing business, but assessing whether it can convert its AI optical business into profit.

Eoptolink Technology's target price was raised from RMB 353.57 to RMB 701, with the main increment coming from 3.2T transceivers and NPO. TFC Communication's target price was raised from RMB 318.57 to RMB 419, benefiting from CPO ramp-up and 3.2T optical engines.

Upward revision of DSBJ's earnings forecast.

Divergence is also emerging. T&S Communications (300570.SZ) was downgraded from Buy to Sell, with a target price reduced from RMB 156 to RMB 152. Citi lowered its EPS forecasts for 2026 and 2027, primarily considering the risk of decoupling from Corning, increased competition in the Asian supply chain, and high valuations. According to the report, T&S Communications is currently trading at ~59x 2027 P/E, while the target price corresponds to 31.8x 2027 P/E.

These rating changes indicate that the upward revision in AI optical interconnect demand does not mean all supply chain companies benefit equally. The market places more value on high-speed product capabilities, silicon photonics and laser chip layouts, customer structure, supply chain stability, and whether the current stock price has already priced in the growth.

It is worth noting that these target prices remain assumptions in the broker's model, not company commitments. For investors, upward target price revisions reflect institutions simultaneously raising expectations for AI optical interconnect demand, product upgrades, and China's supply chain share. However, the subsequent realization still depends on whether orders, delivery, and profit margins can keep pace.

Growth Story Hinges on Laser Chips, Yields, and Valuations

This upward revision does not mean AI optical interconnects have entered a risk-free growth phase.

The first constraint is supply. EML and CW laser chips could both face tightness, especially under the scenario of rapidly increasing silicon photonics penetration and accelerated ramp-up of 1.6T and 3.2T. Upstream capacity and yields will directly impact final shipments. If key chip supply falls short, orders and expectations may rise first, but revenue recognition will have to wait for the delivery schedule.

The second constraint is technology deployment. CPO/NPO are seen as significant growth drivers post-2027, but whether the new architecture can ramp up according to the bull case depends on cloud provider capex, network architecture choices, equipment yields, and the progress of platform solutions from companies like Nvidia and Google. The significant gap between the base and bull cases indicates that shipments over the next two years are not yet locked in.

The third constraint is valuation. T&S Communications was downgraded by Citi from Buy to Sell, citing decoupling risks from Corning and excessive valuation. Accelink Technologies was also maintained with a Sell rating, primarily due to valuation pressure.

The $92 billion market forecast brings AI optical interconnects into the spotlight, but stock prices have already priced in much of the optimistic expectations. What will truly differentiate companies is not just how many AI orders they secure, but who can break into higher-end product generations, lock up upstream laser chip supply, and convert the ramp-up of 1.6T, 3.2T, and CPO/NPO into sustainable profits.