SK海力士登顶次日即熔断,存储超级周期走到哪了?

- 核心观点:全球存储芯片市场(DRAM/NAND)在 AI 需求驱动下正经历严重供需失衡,利润率创新高,但产能集中释放预计在 2027 年下半年后,届时价格急跌风险将显著上升。

- 关键要素:

- SK海力士2026年一季度营业利润率72%超英伟达,全球DRAM供需缺口达15年来最严重4.9%。

- 全球存储市场规模预计2027年上半年突破1.5万亿美元,服务器用存储占比升至57%。

- HBM4单颗AI加速器DRAM消耗量增加33%,新产能(美光、三星、SK海力士)集中投产于2027年中期至2028年。

- 美光2026年资本支出上调至200亿美元,三星平泽P5厂2028年运营,SK海力士M15X设施2027年中启用。

- 韩国股市因杠杆产品过度集中触发熔断,短期波动与基本面(短缺持续到2027年)形成矛盾。

Original author: Curie

Introduction: On June 22, SK Hynix's market cap surpassed Samsung for the first time in 26 years. The very next day, the Korean stock market triggered a circuit breaker, as the semiconductor sector faced a panic sell-off.

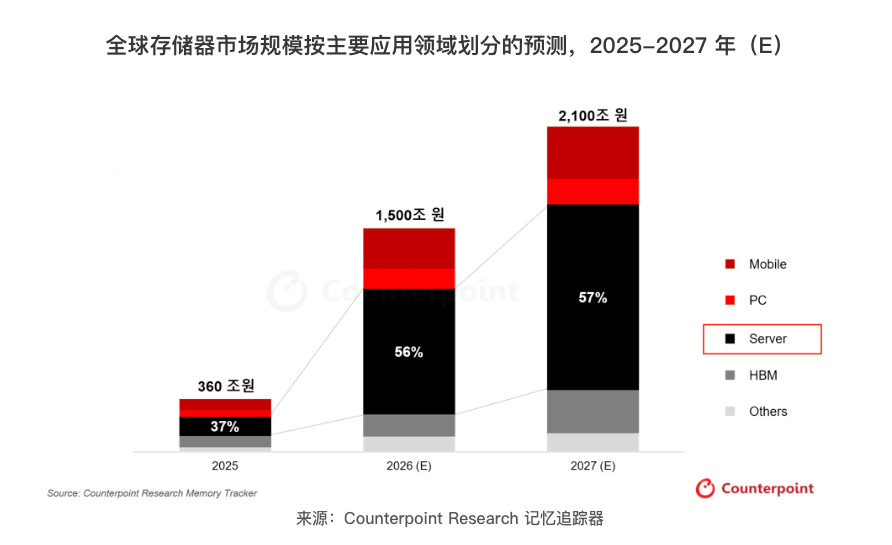

Yet on the same day, a research agency forecast that the global memory market would exceed $1.5 trillion by 2027, with server memory's share expanding to 57%, and the shortage likely persisting at least until the second half of next year.

Where exactly is the super cycle? When will the price inflection point arrive? The capacity expansion plans of Samsung, SK Hynix, and Micron offer timeline clues, pointing towards after the second half of 2027.

On June 23, the South Korean stock market experienced a textbook case of "from euphoria to panic."

Just the day before, SK Hynix's intraday market cap touched approximately $1.35 trillion, surpassing Samsung Electronics for the first time in 26 years to become the most valuable company in South Korea, closing up 5.6%. But a single trading day later, KOSPI 200 futures plunged 5%, triggering a circuit breaker, with both Samsung and SK Hynix hit by panic selling. According to TradingKey, direct triggers included AI competitiveness concerns stemming from a senior executive shakeup at Google, and forced liquidations due to a regulatory crackdown in South Korea on excessive concentration in semiconductor leveraged financial products.

This violent volatility coincided with an optimistic industry forecast.

Data from Counterpoint Research's Memory Tracker, released on June 23, shows that the global memory market (DRAM + NAND) will continue to expand through the first half of 2027, surpassing 2,100 trillion Korean Won (approximately $1.5 trillion). The share of server memory is projected to rise from under 50% in 2025 to 57%.

On one hand, the market is experiencing sharp fluctuations at high levels. On the other, industry data points to a persistent shortage. For investors focused on the memory sector, the moment of divergence has arrived.

Memory Chip Profit Margins Trump NVIDIA, But the Supply-Demand Gap is the True Pricing Anchor

To understand current memory stock valuations, one must first look at the strength of the fundamentals.

SK Hynix's Q1 2026 revenue reached $52.58 billion (converted at the then-current exchange rate), a year-over-year increase of 198%. Operating profit was $37.61 billion, up 405% YoY, with an operating margin of 72%, surpassing NVIDIA's 65% in the same period, setting a historical record for the semiconductor manufacturing industry.

According to CNBC, Counterpoint Research analyst MS Hwang commented that the Q1 earnings showed demand for memory from AI inference far exceeded expectations, with companies scrambling for supply.

The root of this extraordinary profitability is a structural supply deficit.

An April report from Goldman Sachs estimated the global DRAM supply-demand gap would widen from 3.3% to 4.9%, the most severe in 15 years. Samsung, SK Hynix, and Micron control over 95% of global DRAM production capacity, but almost all incremental output is being consumed by AI.

According to TrendForce data, DRAM contract prices in Q1 2026 surged 90% to 95% quarter-over-quarter. Although Q2 price increases narrowed to 58% to 63%, NAND flash contract prices actually accelerated to a 70% to 75% sequential increase.

HBM (High Bandwidth Memory) is at the core of this price surge. This technology, which vertically stacks multiple layers of DRAM chips, is designed specifically for AI accelerators. Producing 1GB of HBM consumes roughly three times the wafer area of standard DDR5, but a single stacked unit sells for $300 to $500, with profit margins three to five times that of regular DRAM. SK Hynix currently holds approximately 57% to 62% of the global HBM market share and is NVIDIA's primary supplier for AI accelerators.

Goldman Sachs estimates SK Hynix has secured roughly two-thirds of the HBM4 orders for NVIDIA's next-generation Rubin platform. SK Group Chairman Chey Tae-won stated publicly in March that the global chip wafer shortage could last until 2030, with capacity expansion taking at least four to five years, and he estimates a gap of over 20%.

Therefore, fundamentally, the shortage is expected to continue for another one to two years. With the two companies collectively controlling about 70% of global DRAM capacity, the supply-demand gap is unlikely to change in the short term.

Inflection Point Timeline: New Capacity Concentrated After H2 2027

Counterpoint explicitly warns in its report: once new capacity commissioning becomes visible, the risk of a sharp price decline cannot be ruled out. The specific timeline is as follows:

Micron has raised its FY2026 capital expenditure to $20 billion. Its new fab in Idaho will begin production in mid-2027, and its Singapore HBM packaging facility will contribute capacity in the same year. Samsung's Pyeongtaek P5 plant is expected to be operational by 2028. SK Hynix's M15X facility will be commissioned in mid-2027, and it has also announced an investment of 19 trillion Korean Won to build a new plant.

However, the pace of expansion still lags far behind demand growth.

Goldman Sachs calculates that the incremental memory demand from U.S. data centers between 2027 and 2028 will be approximately 9% to 12%, while local capacity expansion is only about 2% to 4%. Simultaneously, the arrival of HBM4 will exacerbate the supply-demand imbalance – HBM4 requires 16 DRAM dies per stack, up from 12, increasing DRAM consumption per AI accelerator chip by 33%.

TrendForce's assessment is consistent: HBM3E remains the primary shipping product, while HBM4 begins to contribute revenue. However, delays in AI chip upgrades and inventory accumulation are causing growth momentum to slow. The true window for a price adjustment may appear between the second half of 2027 and 2028.

Before that, the absolute level of the supply-demand gap will continue to support high prices and high margins. Afterward, the concentrated release of new capacity, potentially combined with a slowdown in AI investment pace, will cause the risk of sharp price declines to accumulate.

Counterpoint emphasizes that the volume locked in Long-Term Agreements (LTAs), customized HBM strategies, and the speed of next-generation process node conversion will determine the competition for market share among suppliers. In other words, even if overall growth slows, the competitive landscape among the three giants is undergoing a dramatic restructuring.

What Does This Mean for Holders and Spectators?

The market cap peak on June 22 and the circuit breaker on June 23 encapsulate the core contradiction of the current memory sector:

The fundamentals of the memory sector are still accelerating – for example, SK Hynix's Q1 profit margin of 72% and the largest supply-demand gap in 15 years. However, valuations have already priced in extremely optimistic expectations (SK Hynix shares have surged over 340% year-to-date), while the high concentration in leveraged products has amplified volatility in either direction.

Both Samsung and SK Hynix have warned in their earnings reports that the memory shortage is expected to last at least until 2027.

Kim Jaejune, head of Samsung's memory business, stated that the demand satisfaction rate has fallen to historic lows, and customers are racing to secure future supply. But the market has already begun pricing in risks on the other side: the Bank of Korea is leaning towards raising interest rates due to the semiconductor super cycle, and South Korean government bonds are performing at the bottom globally.

According to available public data, 38 analysts have a consensus rating of "Strong Buy" on SK Hynix, with an average 12-month target price of approximately 2.71 million Korean Won. Korean brokerage Hanwha Investment & Securities recently raised its target price directly from 1.63 million to 4.3 million Korean Won.

Therefore, synthesizing public analyst views, the general assessment is:

- For holders: Both Counterpoint and TrendForce point to the second half of 2027 as the earliest inflection point for supply and demand. Before then, fundamental support remains. However, the liquidation risk triggered by leveraged ETFs is an exogenous shock unrelated to fundamentals; position management is more critical than directional judgment.

- For spectators: The transmission of the memory shortage to consumer electronics has just begun. Margin pressure on smartphone and PC brand manufacturers, and contraction of low-end product lines, are certainties over the next two to three quarters. Shorting logic along this transmission chain may be a safer bet than chasing high-priced memory stocks.