ยอดส่งออกและราคาต่อหน่วยพุ่งขึ้นพร้อมกัน ตลาดเริ่มวางเดิมพันกับ "ส่วนชดเชยคอขวด" ของหุ้นกลุ่มหน่วยความจำ

- มุมมองหลัก: ข้อมูลการส่งออกหน่วยความจำของเกาหลีใต้ในช่วง 20 วันแรกของเดือนมิถุนายน (มูลค่าและราคาต่อกิโลกรัม) เพิ่มขึ้นอย่างมากเมื่อเทียบกับปีก่อน ตอกย้ำการประเมินว่าความต้องการหน่วยความจำ AI กำลังกระจายออกจาก HBM แต่ข้อมูลดังกล่าวยังคงเป็นการสรุปเบื้องต้นเท่านั้น ไม่สามารถเทียบได้โดยตรงกับการที่ราคาชิปเพิ่มขึ้นหลายเท่าหรือมูลค่าการส่งออก HBM การเปลี่ยนเกณฑ์การประเมินมูลค่าจำเป็นต้องรอการตรวจสอบจากงบการเงินของบริษัท

- ปัจจัยสำคัญ:

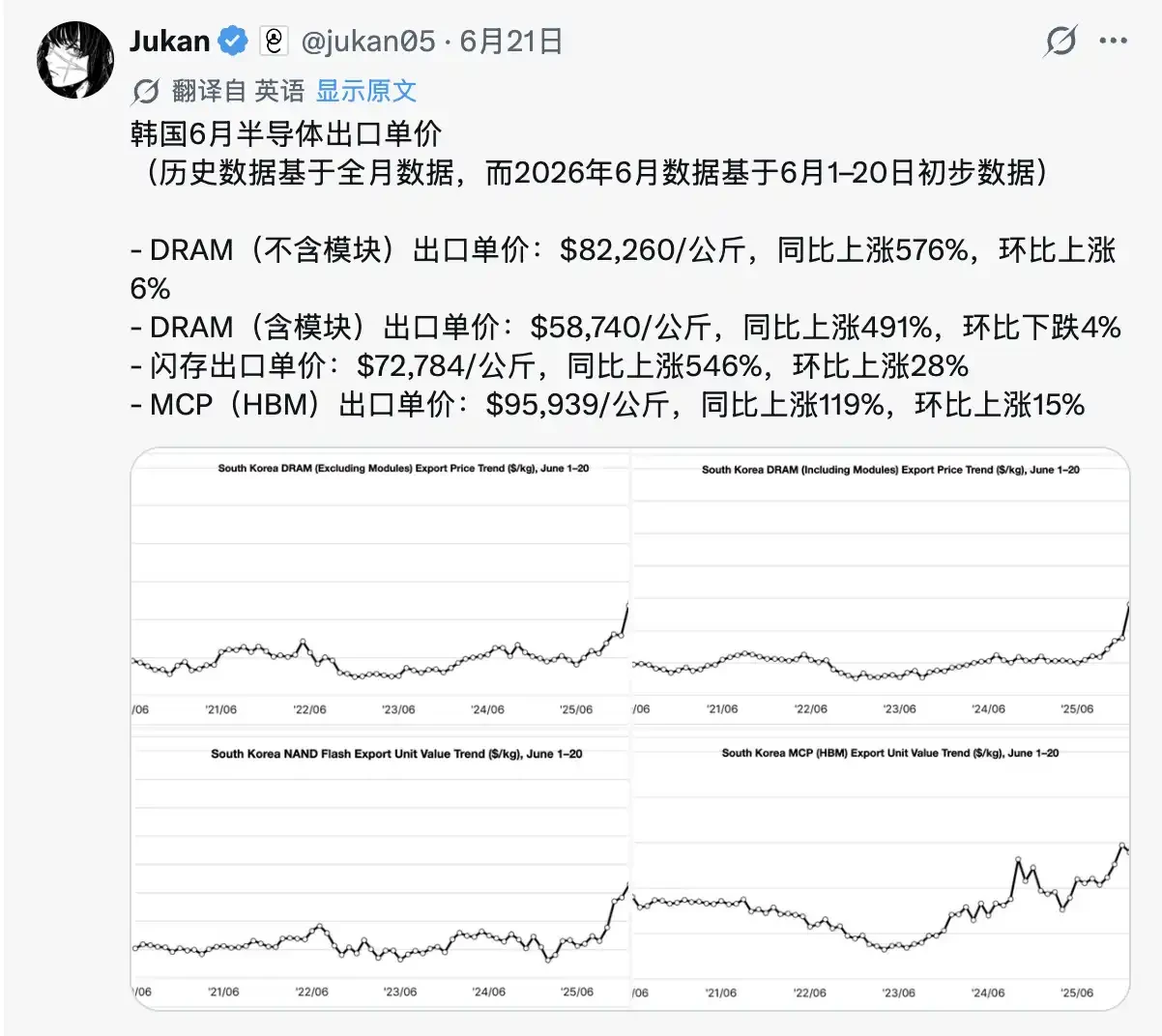

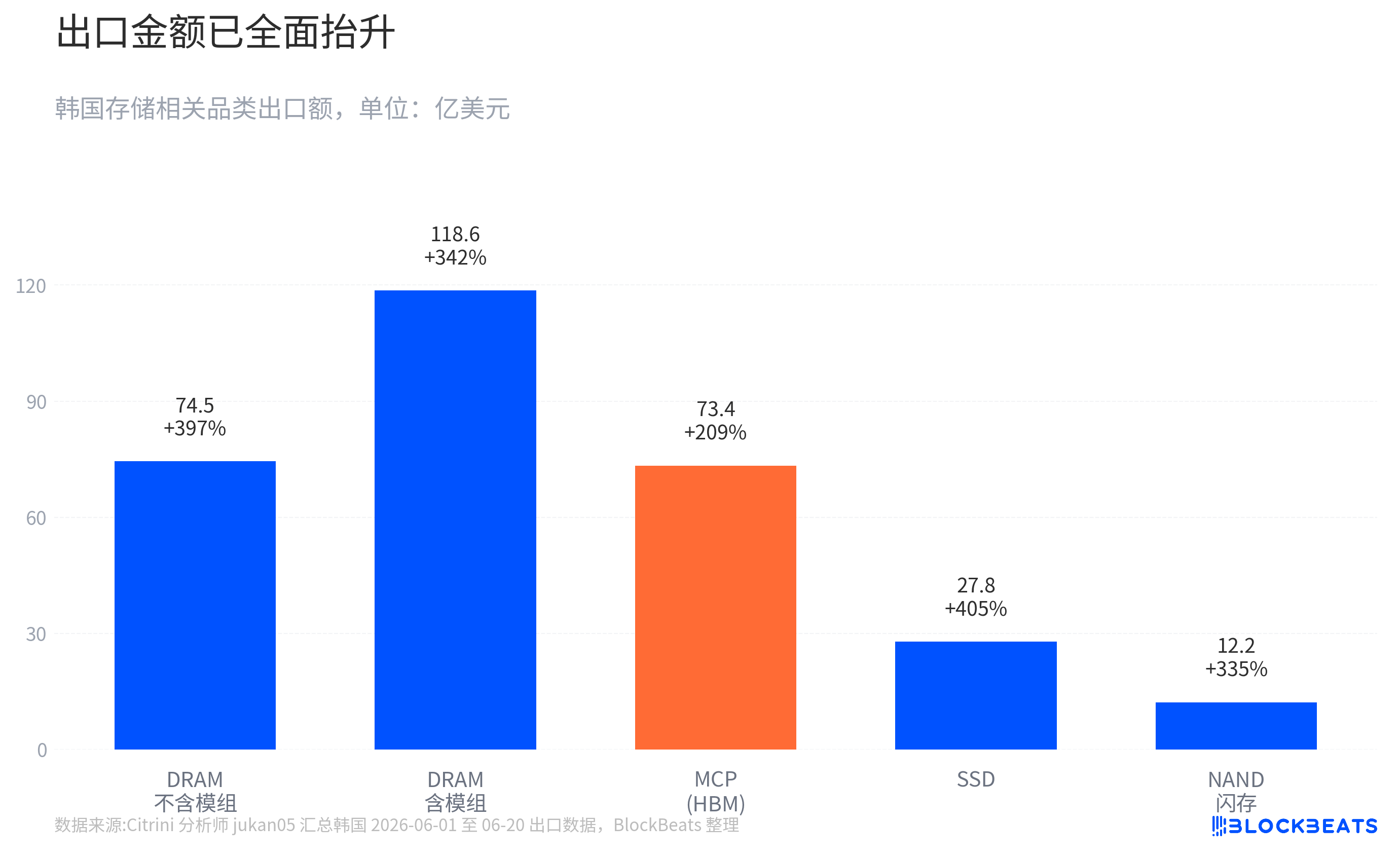

- การส่งออกเซมิคอนดักเตอร์ของเกาหลีใต้ในเดือนพฤษภาคมอยู่ที่ 3.716 หมื่นล้านดอลลาร์สหรัฐ (เพิ่มขึ้น 169% เมื่อเทียบกับปีก่อน) ทำสถิติสูงสุดเป็นรายเดือน คิดเป็น 42.3% ของการส่งออกทั้งหมด ในข้อมูลเบื้องต้นของ 20 วันแรกของเดือนมิถุนายน มูลค่าการส่งออกและราคาต่อกิโลกรัมของหมวดหมู่ DRAM และ NAND เป็นต้น (บางรายการเพิ่มขึ้นกว่า 500% เมื่อเทียบกับปีก่อน) ต่างก็เติบโตสูง

- การพุ่งขึ้นของราคาต่อกิโลกรัมส่วนใหญ่สะท้อนถึงการเพิ่มขึ้นของราคา การเปลี่ยนแปลงโครงสร้างผลิตภัณฑ์ไปสู่ผลิตภัณฑ์ที่มีมูลค่าสูงอย่าง HBM และความแตกต่างของเกณฑ์การวัด ไม่ใช่การปรับขึ้นราคาแบบเดียวกันหลายเท่าของชิปทั้งหมด การส่งออก MCP ที่แข็งแกร่งสามารถใช้เป็นตัวแทนความต้องการบรรจุภัณฑ์ระดับสูงได้ แต่ไม่สามารถเทียบได้โดยตรงกับการส่งออก HBM

- อำนาจการกำหนดราคาในการขาดแคลน HBM กำลังแพร่กระจายไปยัง DRAM, NAND และ SSD ผ่านการจัดสรรกำลังการผลิตและการเปลี่ยนแปลงโครงสร้างผลิตภัณฑ์ SK Hynix มีส่วนแบ่ง HBM ที่นำหน้า ลูกค้าล็อคคำสั่งซื้อจนถึงปี 2026 จึงได้รับประโยชน์โดยตรง ขณะที่ Samsung และ Micron ก็ได้รับประโยชน์จากการขยายตัวของความต้องการหน่วยความจำระดับสูงและความยืดหยุ่นของอัตรากำไรขั้นต้นที่เพิ่มขึ้น

- คอขวดของโครงสร้างพื้นฐาน AI กำลังขยายจาก GPU ไปยังหน่วยความจำ CPU บรรจุภัณฑ์ขั้นสูง และส่วนอื่นๆ ข้อมูลส่งออกของเกาหลีใต้ทำให้การประเมินมหภาคนี้กลายเป็นการเปลี่ยนแปลงเชิงปริมาณที่วัดได้ของมูลค่าการส่งออกหน่วยความจำและราคาต่อหน่วย

- ความเสี่ยงหลักอยู่ที่หน่วยความจำยังคงเป็นอุตสาหกรรมที่มีวัฏจักรสูง ข้อมูลเบื้องต้น 20 วันไม่สามารถพิสูจน์ความแน่นอนตลอดทั้งปีได้ การเพิ่มขึ้นของราคาต่อกิโลกรัมไม่สามารถแยกการขึ้นราคาและการเปลี่ยนแปลงโครงสร้างได้อย่างสมบูรณ์ หากการใช้จ่ายด้านทุน AI ชะลอตัว ความต้องการหน่วยความจำก็จะได้รับผลกระทบเช่นกัน

- เกณฑ์การประเมินมูลค่าจะเปลี่ยนจาก "วัฏจักรสินค้าคงคลัง" ไปเป็น "คอขวดของโครงสร้างพื้นฐาน AI" ได้หรือไม่ ขึ้นอยู่กับว่างบการเงินของไตรมาส 2/3 จะแสดงให้เห็นถึงการส่งมอบ HBM ราคาขายเฉลี่ย อัตรากำไรขั้นต้น และความต้องการ SSD สำหรับศูนย์ข้อมูล ที่บรรลุผลพร้อมกันหรือไม่ ไม่ใช่จากข้อมูลการค้าเพียงชิ้นเดียว

TL;DR

- According to a summary by Citrini analyst Jukan, South Korea's export value and unit price per kilogram for multiple memory products in the first 20 days of June saw significant year-on-year growth, although this data is still preliminary and aggregated from social media sources.

- This data reinforces the judgment that AI memory demand is spilling over. However, MCP is not directly equal to HBM, and a rise in unit price per kilogram does not mean individual chip prices have increased several-fold.

- Related stocks: SK Hynix, Samsung, Micron, Nvidia.

According to a summary by Citrini analyst Jukan, South Korea's export value and unit price per kilogram for multiple memory products in the first 20 days of June saw significant year-on-year growth, sparking renewed market discussion on whether memory manufacturers are gaining a bottleneck premium from AI infrastructure.

This matters not just because it's another set of semiconductor export figures, but because it touches upon two variables most concerning for investors: rising shipment value and rising export value per unit weight. The former points to demand intensity, the latter to price increases and a product mix shift towards higher-value products. For memory stocks, this is more valuable than simply "selling more," as it impacts revenue, gross margins, and EPS upside potential.

Over the past year, the market has accepted that HBM (High Bandwidth Memory) is a scarce resource in AI servers. The debate lies in whether this scarcity is limited to a few high-end products experiencing price hikes, or if it has begun to spill over into the broader memory supply chain of DRAM, NAND, and SSDs. If it's the former, memory stocks still resemble cyclical recovery trades. If it's the latter, the valuation anchors for SK Hynix, Samsung, and Micron could partially shift from an "inventory cycle" to an "AI infrastructure bottleneck."

While the South Korean data provides a strong signal, it is not a final conclusion. Specifically, the sub-category and unit price per kilogram data for the first 20 days of June is more suitable as a preliminary observation from aggregated social media sources and cannot be directly treated as official confirmation. Its value lies in advancing a narrative-driven question into a stage that can be cross-validated using trade value, price indicators, and company guidance.

South Korean Exports Send a Price Signal to the Market

The most direct implication of this data is that the memory market recovery might not just be about volume recovery; prices and product mix are also improving.

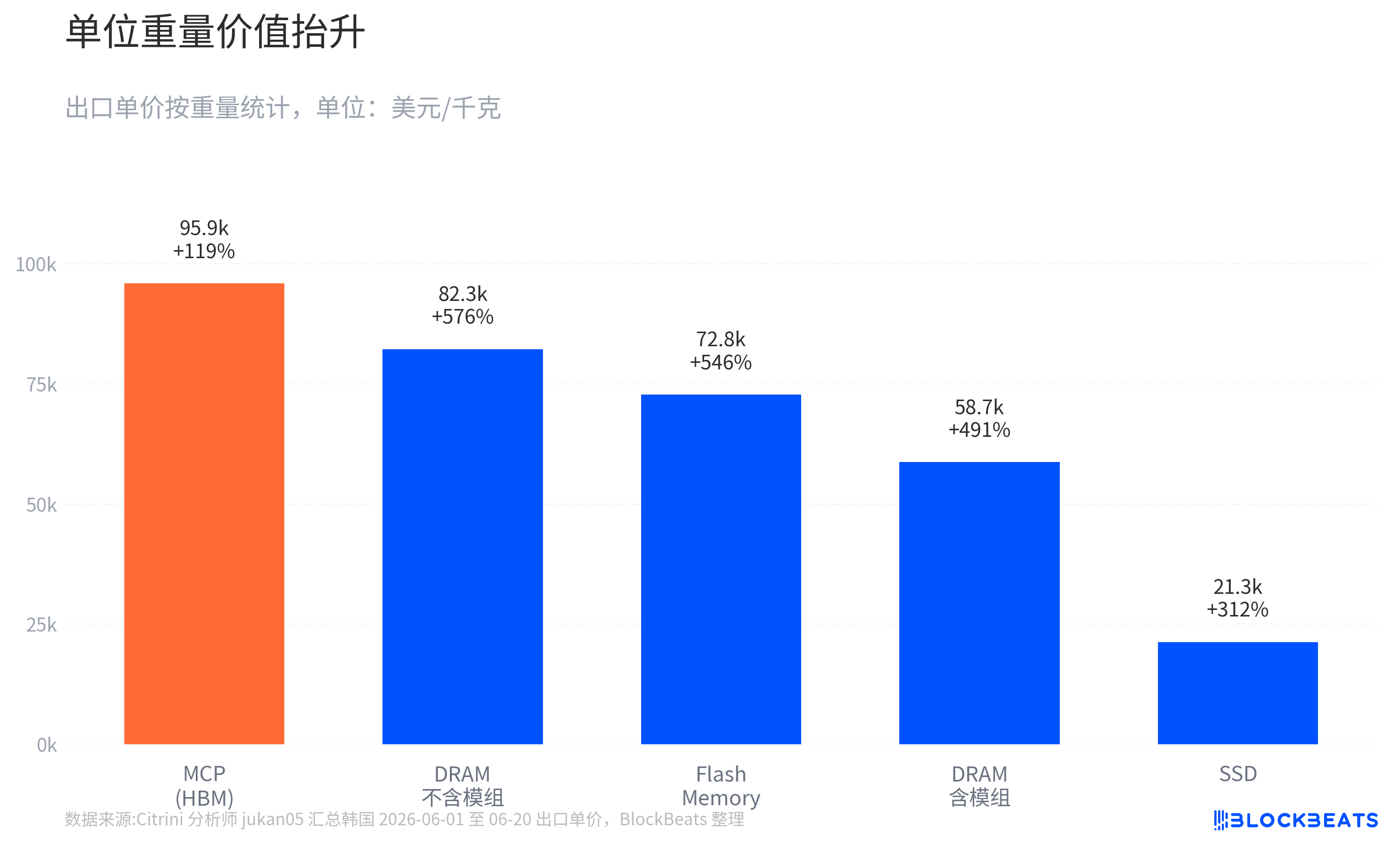

In South Korea's preliminary export data for June 1-20, the export value across multiple categories including DRAM, NAND/Flash, MCP, and SSD showed high year-on-year growth. Among them, DRAM exports excluding modules nearly quadrupled year-on-year, while exports including modules more than tripled. NAND/Flash and SSD export values also saw substantial increases. More notably for the market, the unit price per kilogram for certain DRAM and NAND-related categories surged over 500% year-on-year.

These numbers need to be viewed in context. The first 20-day data is more like a mid-month snapshot of South Korean trade data, providing directional hints and slope indications, but not the final monthly figures. The classification of sub-categories may also differ from the product definitions investors are accustomed to, making it unsuitable for directly extrapolating full-year earnings models.

A more stable reference comes from the already published May data. According to South Korean media citing official data, the country's total exports in May were $87.75 billion, up 53.2% year-on-year; semiconductor exports were $37.16 billion, up approximately 169% year-on-year, hitting a monthly record and accounting for 42.3% of total exports. Exports of computers and related equipment also surged, which media linked to AI server SSD demand. The preliminary export data for June 1-10 was also strong, with total exports of $28.6 billion, up 86% year-on-year, and semiconductor exports of approximately $11 billion, more than tripling year-on-year.

This means the June 1-20 social media aggregated data is no longer an isolated signal. It aligns with previous official export trends, forming continuity. For investors, continuity is more important than a single month's spike, as it determines whether earnings upgrades can transition from a one-time surprise to a multi-quarter model adjustment.

A Surge in Unit Price Per Kilogram Doesn't Mean Chip Prices Have Risen Fivefold

The most common misinterpretation of this data is directly translating a surge in unit price per kilogram into "every chip's price has increased several times." A more accurate description is that the unit price per kilogram reflects the combined effects of price increases, product mix improvement towards higher-end products, and statistical methodology.

In South Korean export data, some categories use weight to calculate average unit prices. This metric is straightforward for commodities. However, for semiconductors, the value of a kilogram of cargo can vary greatly. The value density of a kilogram of low-end memory chips is on a completely different level compared to a kilogram of HBM, high-capacity DRAM, or complex packaged products. An increase in unit price per kilogram could stem from either price increases for similar products or a shift in the export mix towards higher-value products.

This is precisely the core of the AI trade. AI servers require memory systems with higher bandwidth, greater capacity, and lower latency. The value density of HBM and high-end DRAM is significantly higher than that of standard memory products. As the proportion of these products in the export mix increases, the average export value per kilogram rises. What the market is observing is not a uniform fivefold price increase for all memory chips, but rather an increase in the share of high-end products combined with price increases, which is changing the revenue quality of the memory chain.

Caution is also needed regarding MCP data. The market often uses MCP as a proxy indicator for HBM, as HBM involves multi-chip stacking and packaging. However, MCP (Multi-Chip Package) is not equivalent to HBM in a narrow sense; it can also include other multi-chip package products. Strong MCP export value and unit price support the directional judgment of "strong demand for high-end packaged memory," but cannot be directly written off as HBM export figures.

These limitations do not diminish the data's value; rather, they make it more suitable for investment decisions. The truly useful conclusion is not the exact price increase of a specific product category, but that multiple memory categories simultaneously show increases in both value and unit value. This indicates that AI demand may no longer be confined to the isolated segment of HBM. It is influencing the broader memory pricing system through capacity allocation, product mix, and customer procurement.

HBM Shortage Changes the Pricing Power of Memory Manufacturers

If one only looks at HBM itself, the market has long known it is in short supply. The new question is why the HBM shortage affects DRAM, NAND, and SSDs.

The mechanism is not overly complex. Memory manufacturers have limited advanced capacity, R&D resources, and customer qualification capabilities. When Nvidia and cloud providers continuously lock in high-value products like HBM and high-capacity DRAM, manufacturers prioritize allocating resources towards areas with higher returns and better order visibility. This keeps the supply of high-end products persistently tight and can indirectly constrain the supply elasticity of general DRAM, NAND, and SSDs.

SK Hynix is the most direct beneficiary of this logic. The market generally believes its HBM market share is leading. According to industry reports and brokerage analyses, SK Hynix has high visibility for its 2026 HBM capacity, with customer demand exceeding supply capability and growing sales of high-value-added products. For a memory manufacturer, customers securing capacity in advance and growth in high-end product sales change not just the next quarter's revenue, but also the market's assessment of its pricing power. The core issue for traditional cyclical stocks is how long prices can rise; the core issue for a bottleneck asset is what premium customers are willing to pay for guaranteed supply.

The logic for Samsung and Micron differs slightly. Samsung has greater scale in NAND and overall memory capacity while still catching up in high-end HBM customer qualifications. Micron benefits from high-end memory demand expansion and supply chain diversification. For these two companies, the market is not trading on the belief they have fully replicated SK Hynix's HBM pricing power. Instead, it's trading on the possibility that if the HBM shortage spills over into high-end DRAM, enterprise SSDs, and NAND prices, their gross margin flexibility could be stronger than in the previous cycle.

Intel CEO Lip-Bu Tan mentioned in a No Priors interview that the AI infrastructure bottleneck is spreading from GPUs to memory, CPUs, optical interconnects, power conversion, advanced packaging, and materials. The key here isn't to rewrite this as an Intel strategy, but to illustrate a broader context: the constraints on AI data centers are no longer just about a single GPU. Any link that limits cluster expansion or efficiency could gain new pricing power.

Memory is one of the earlier links observable through trade data. No matter how powerful a GPU is, it needs sufficient memory bandwidth and capacity to feed data. With the increase in inference and agentic AI tasks, system requirements for memory, storage, and scheduling resources will become more complex. The value of the South Korean export data is that it grounds the somewhat macro judgment of "AI infrastructure bottleneck diffusion" into observable changes in memory export value and unit value.

Memory Stocks Still Subject to Cyclical Constraints

For investors, the current rally in memory stocks feels more like a combination of "accelerating real-cycle strength plus reassessment of future earnings" rather than pure storytelling. Export data shows demand and prices have real support; the market is essentially buying into whether 2026 revenue, gross margins, and EPS will be revised upwards.

If subsequent earnings reports validate this trend, SK Hynix's valuation premium is most easily explained: leading HBM market share, customer lock-in orders, and the ramp-up of high-value products provide high visibility. The key for Samsung is whether its HBM catch-up translates into actual orders, and whether NAND and SSD prices form a broader support base. Micron needs to prove that price increases in high-end DRAM and data center storage can flow through to gross margins and guidance.

However, risks exist here too. Memory remains a strongly cyclical industry, where supply expansion, inventory changes, and customer procurement cycles all affect prices. Preliminary 20-day export data can indicate a steeper slope but cannot confirm full-year certainty. An increase in unit price per kilogram indicates higher value density but cannot perfectly separate the contribution of average selling price increases from product mix changes. Strength in MCP can serve as a proxy signal for HBM but cannot be directly equated to HBM exports.

Another risk stems from AI capital expenditure itself. If investment pace slows in areas like power, cooling, packaging, or overall computing capacity, memory demand would also be impacted. The bottleneck diffusion is both the reason for memory's premium and a potential constraint. If other links in the system become constrained first, the pace of memory demand release could be delayed.

Earnings Reports Will Determine if the Valuation Anchor Can Shift

This revaluation ultimately needs to land in company financial statements, not just trade data. The official full-month export data for June will first provide a more complete confirmation to the market: whether the strong growth in the first 20 days continued, whether price indicators remain elevated, and whether the strength in NAND and SSDs was merely driven by short-term large orders.

More critical validation will come from the Q2 and Q3 earnings reports of SK Hynix, Samsung, and Micron. The market needs to see HBM shipments and prices continue to materialize, a concurrent improvement in average selling prices for DRAM and NAND, and data center SSD demand driving gross margin expansion, not just top-line revenue growth. If gross margins and guidance fail to keep pace with the slope indicated by the export data, the revaluation will quickly revert to a cyclical trade.

The safer conclusion for now is that South Korea's first 20-day memory export data is robust enough to support upward revisions to memory makers' earnings flexibility and re-open the discussion on the AI infrastructure bottleneck premium. However, it is not yet sufficient to prove the memory industry has decoupled from cycles. What determines if the valuation anchor can shift is not how high a year-on-year figure is, but whether prices, product mix, and profit margins can hold simultaneously over the coming quarters.