Gate Research: Combined Market Cap of the Three Major Storage Giants Exceeds $1 Trillion

- Core View: Micron Technology's market cap surpassing the trillion-dollar mark signals that the storage industry is transitioning from a traditional cyclical hardware sector to a key strategic resource for AI computing power. This growth is driven by a structural revaluation led by high-end products like HBM and long-term agreements (LTAs), rather than a simple cyclical rebound.

- Key Factors:

- Micron's market cap is approximately $1.17 trillion, with its stock price surging over 800% in the past year, primarily fueled by sustained demand from AI servers and data centers for high-end storage products like HBM and DDR5.

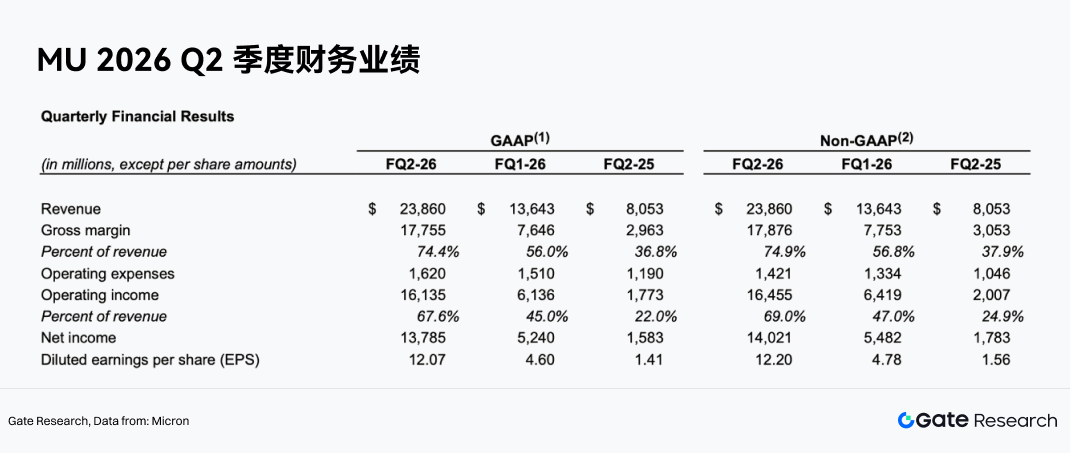

- Record FY2026 Q2 earnings: Revenue reached $23.86 billion, with Non-GAAP gross margin jumping to 74.9%. The core driver was the AI data center business, generating combined revenue exceeding $13.4 billion.

- Product mix upgrade is key: High-end products like HBM command stronger pricing power. Their ASP is expected to increase by approximately 50% year-over-year, driving profitability and earnings stability significantly above traditional DRAM cycles.

- Long-Term Agreements (LTAs) are transforming the business model: New LTAs not only lock in purchase volumes but also partially lock in prices (for terms of 3-5 years), enhancing revenue visibility and earnings resilience across cycles.

- Industry supply remains tight: DRAM and NAND are expected to face supply shortages until Q2 2028 and Q4 2027, respectively. HBM capacity is constrained by process technology and yield rates, leading to slow supply release and supporting price elasticity.

- Gate platform has launched related trading services: Users can trade US stocks like Micron, perpetual contracts, and leveraged ETFs using USDT, enabling unified management of digital asset and equity allocations.

Summary

- The total market capitalization of the global storage sector has experienced explosive growth, with the three giants Samsung Electronics, SK Hynix, and Micron Technology all surpassing the trillion-dollar mark.

- The continuous growth in demand for AI model training and inference is significantly increasing data centers' demand intensity and value for storage products such as High Bandwidth Memory (HBM), DDR5, and enterprise-grade SSDs.

- Micron Technology recently officially joined the trillion-dollar market cap club, becoming one of the most closely watched revaluation targets in the AI storage industry chain. According to StockAnalysis data, as of June 3, 2026, Micron's market cap was approximately $1.17 trillion.

- The core driver of this storage sector rally is not a traditional DRAM cyclical rebound, but rather the market's repricing of the structural value within AI servers, High Bandwidth Memory (HBM), Long-Term Agreements (LTAs), and the tight supply-demand dynamics of the storage industry.

- Gate has officially launched stock trading, allowing users to directly trade stocks and ETFs from major securities markets within the platform using USDT. The stock contract zone has introduced perpetual contracts, supporting USDT settlement and 1-20x leveraged two-way trading. Gate has also launched leveraged ETF tokens, providing investors with long exposure to stocks.

- Micron's trillion-dollar market cap is not the result of a single earnings cycle, but a manifestation of the combined effects of AI storage value reassessment, HBM product upgrades, long-term agreement mechanisms, and improved industry supply-demand dynamics.

The AI-Driven Storage Sector

In the past, the storage industry was often viewed as a typical cyclical sector, with corporate profitability highly dependent on supply-demand fluctuations and price elasticity. However, in the AI era, storage is transitioning from a supporting component in general-purpose hardware to a critical resource within the computing infrastructure.

Large model training and inference require not only more powerful GPUs and interconnect capabilities, but also storage systems with higher bandwidth, larger capacity, and lower latency. Whether it's HBM on the GPU side or DDR5 and enterprise SSDs on the server side, their importance is clearly rising. For cloud providers and data center clients, storage is no longer just a cost item but a key variable affecting model training efficiency, inference throughput, and overall deployment cost.

The changes brought by the expansion of AI applications are not just an increase in storage chip shipments; more importantly, it's the rising proportion of high-end products. Compared to regular DRAM, HBM offers higher bandwidth, higher integration, and higher added value; enterprise SSDs also benefit from increased data center workloads. As product portfolios shift towards high-performance directions, the revenue structure, profit margin structure, and valuation frameworks of leading manufacturers may all change.

Unlike the traditional historical logic of "raising prices then expanding production," the supply of high-end storage products like HBM is relatively constrained due to limitations in manufacturing processes, yield rates, advanced packaging, and customer qualification cycles. At the same time, core customers are more inclined to lock in capacity and some pricing through long-term supply agreements. This gives leading manufacturers greater revenue visibility and bargaining power than in the past, endowing this cycle with more distinct structural characteristics.

Micron Technology, Inc. (NASDAQ: MU), founded in 1978 and headquartered in Boise, Idaho, USA, is a leading global supplier of semiconductor memory and storage solutions. The company designs, manufactures, and sells DRAM, NAND Flash, NOR Flash, High Bandwidth Memory (HBM), SSDs, and storage products for data centers, mobile devices, automotive, industrial, and consumer electronics. Using Micron as a case study is not intended to focus this article on a single stock, but rather because Micron's product portfolio, customer base, earnings elasticity, and market pricing relatively well reflect the evolutionary direction of the AI storage track.

Micron Technology

In the global storage chip industry, Micron, alongside Samsung Electronics and SK Hynix, is a major DRAM supplier and a significant player in the global NAND market. As demand for large model training and inference continues to grow, the need for high-bandwidth memory HBM, high-capacity DDR5, and enterprise SSDs in AI servers is rapidly increasing. Storage chips are no longer just supporting components in general-purpose computing devices; they are gradually becoming one of the key bottlenecks in AI computing infrastructure. Especially in GPU clusters, the bandwidth, capacity, and power consumption of HBM directly impact the performance release of AI chips, leading to Micron being re-evaluated as a core supplier within the AI semiconductor industry chain. This report views Micron Technology as a key representative enterprise in the AI storage industry chain, analyzing its trillion-dollar market cap milestone, long-term agreements, HBM growth, valuation restructuring, and related Gate stock trading support.

Fundamental Analysis and Investment Thesis

According to Gate market data, as of June 3, 2026, Micron Technology's stock was quoted at $1,056. Based on approximately 1.1 billion diluted shares outstanding, the company's total market capitalization is approximately $1.17 trillion. Over the past year, Micron Technology (MU) has shown a clear trend of volatile upward movement culminating in an accelerated breakout. The stock price started around $110, initially strengthened alongside expectations for AI storage demand, steadily rising above $400. After a period of correction, it entered a major rally driven by the explosion in HBM and AI data center demand, with significant surges from May to June, reaching a high of $1,076, representing an accumulated increase of over 8x from its low of the previous year. In the past year, Micron's stock price has risen from approximately $110 to around $1,056, an accumulated gain of over 800%, while the company's market capitalization simultaneously broke through $1 trillion, reflecting the market's continuous reassessment of AI storage demand and the prospects for the HBM business.

From a business structure perspective, Micron currently primarily serves four major application areas: Data Center and Cloud Computing (including AI servers, enterprise servers, and networking equipment); Mobile Terminals (including smartphones and tablets); Storage Business (including enterprise and client SSDs); and Embedded Business (including automotive, industrial, and consumer electronics applications). With AI data center capital expenditures continuing to expand, data center-related storage demand is becoming Micron's fastest-growing and highest profit-elasticity business direction.

Micron's recent trillion-dollar market cap milestone is not simply derived from a rebound in the traditional storage cycle, but stems from the market's repricing of its strategic value within the AI infrastructure industry chain. FY2026 Q2 results showed record revenues, gross margins, EPS, and free cash flow, validating the profit inflection point driven by AI demand, tight industry supply, and high-end storage product upgrades.

AI Era: Storage Upgrades from a Supporting Component to a Strategic Asset

In traditional computing architectures, memory chips were often seen as supporting components alongside CPUs and GPUs, with industry pricing primarily influenced by cyclical supply and demand. However, in the AI era, especially as large model training and inference scales continue to expand, memory bandwidth, capacity, and energy efficiency have become key bottlenecks for AI system performance.

In its FY2026 Q2 earnings release, Micron explicitly stated that the record Q2 performance reflects the "strategic value of memory in the AI era." CEO Sanjay Mehrotra stated that in the AI era, memory has become a strategic asset for customers. This indicates that Micron's management has repositioned the company from a traditional memory supplier to a core participant in the AI computing infrastructure.

The rapid growth in demand for HBM, high-capacity DRAM, DDR5, and enterprise SSDs in AI servers is significantly increasing the value of storage products within the server BOM. As GPU cluster sizes grow, customers are not only concerned about chip computing power but also increasingly focused on the stability of storage supply, performance matching, and controllable deployment costs. This shift provides Micron with stronger bargaining power and higher earnings elasticity.

FY2026 Q2 Results Validate Demand Strength

Micron's FY2026 Q2 revenue reached $23.86 billion, a significant increase from $13.64 billion in the previous quarter and substantially higher than $8.05 billion in the same period last year. The company's Non-GAAP net profit reached $14.02 billion, Non-GAAP EPS was $12.20, operating cash flow was $11.90 billion, and adjusted free cash flow was $6.90 billion.

More critically, earnings quality improved concurrently. FY2026 Q2 Non-GAAP gross margin reached 74.9%, a significant increase from 56.8% in the previous quarter and 37.9% in the same period last year; Non-GAAP operating margin reached 69.0%, a substantial expansion from 47.0% in the previous quarter and 24.9% in the same period last year.

This indicates that Micron's profit improvement is not solely driven by revenue growth, but also represents a leap in profit margins resulting from the combined improvement in product pricing, product mix, and cost efficiency. For a memory company, a gross margin increase from the 30%-40% range to over 70% signifies a fundamental shift in the industry's supply-demand dynamics and the company's product portfolio.

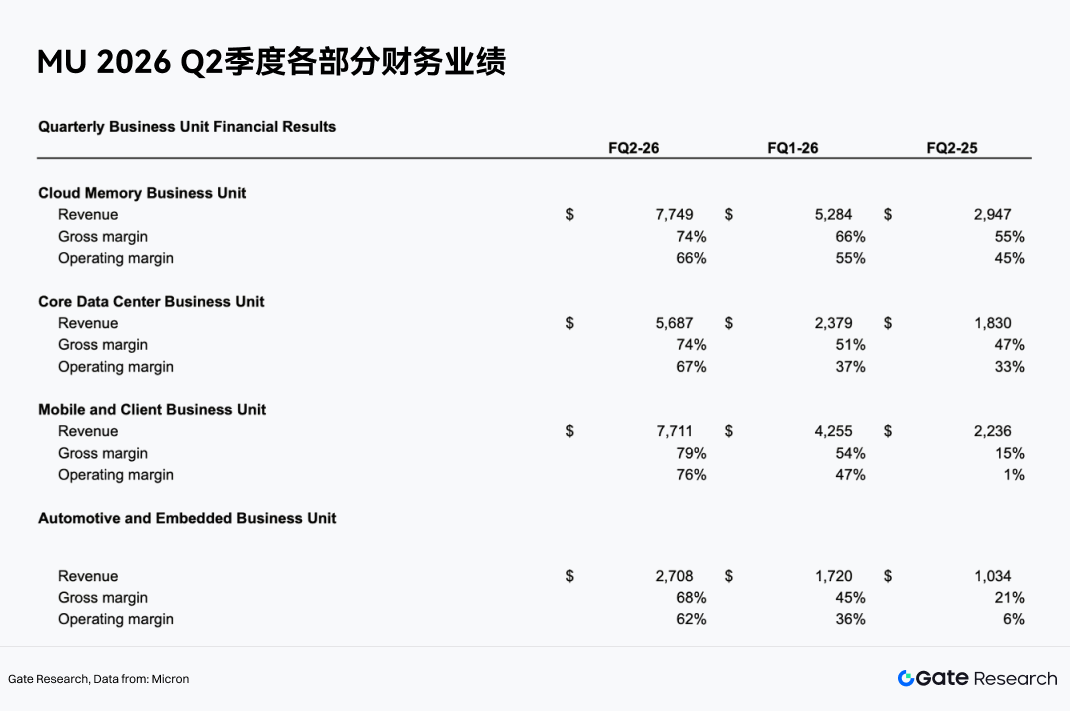

Data Center and Cloud Business Becomes the Core Growth Driver

From a business segment perspective, Micron's FY2026 Q2 growth was highly concentrated in AI and data center-related areas.

The Cloud Memory Business Unit generated revenue of $7.749 billion, with a gross margin of 74% and an operating margin of 66%. The Core Data Center Business Unit generated revenue of $5.687 billion, with a gross margin of 74% and an operating margin of 67%. Combined, these two segments generated over $13.4 billion in revenue, establishing them as the company's most important growth engine.

This demonstrates that Micron's business focus is shifting from traditional consumer electronics cycles like PCs and mobile phones towards cloud computing, AI servers, and data centers. Compared to consumer electronics, AI data center customers are characterized by large capital expenditure scale, high product performance requirements, and strong continuity of supply needs, making them more conducive to forming premium pricing for high-end products and long-term supply relationships.

HBM and High-End DRAM Drive Product Mix Upgrade

The product area where Micron benefits most visibly is HBM and high-end DRAM. HBM is a critical memory product for AI GPUs and accelerators, characterized by high bandwidth, high capacity, and high energy efficiency, with higher price per GB and gross margins compared to regular DRAM.

UBS expects Micron's HBM ASP to grow by approximately 50% year-over-year in 2027, driving continued HBM revenue expansion. With the iteration of AI chip platforms increasing HBM capacity and bandwidth requirements, Micron is well-positioned to achieve a higher revenue share through its HBM3E, subsequent HBM products, and advanced packaging capabilities.

The significance of the product mix upgrade is that Micron is no longer just following industry DRAM average price fluctuations but is gaining stronger pricing power through high-end products. As the proportion of HBM increases, the company's overall gross margin and earnings stability are expected to improve.

Tight Industry Supply Strengthens Price Elasticity

Micron's strong FY2026 Q2 performance was also driven by tight industry supply. The results were driven by a strong demand environment, tight industry supply, and company execution. Some institutions predict that the DRAM market will remain undersupplied at least until Q2 2028, and NAND undersupply will persist until Q4 2027. In a supply-constrained environment, DRAM and NAND prices have sustained support, allowing Micron's revenue and profit margins to remain at high levels.

More importantly, this cycle differs from the past. Historically, memory manufacturers would rapidly expand production after price increases, ultimately leading to oversupply and price declines. However, the demand growth for high-end memory from AI servers is relatively fast, and HBM capacity expansion is constrained by technology, yield rates, advanced packaging, and customer qualification cycles. Therefore, supply release cannot easily catch up with demand quickly.

Long-Term Agreements (LTAs) Enhance Earnings Visibility

An LTA, or Long-Term Agreement, in the semiconductor memory industry typically refers to a pre-arranged supply arrangement between a supplier and its core customers for a future period, covering purchase volumes, delivery timelines, product specifications, and, in some cases, a pricing framework. In the past, procurement agreements in the memory industry were more often "volume-locked, price-not-locked." Customers would pre-commit to a certain purchase volume, giving suppliers some demand visibility, but prices would still fluctuate rapidly with DRAM and NAND market supply and demand. Consequently, during industry downturns, significant price drops would directly impact the revenue and profits of memory manufacturers like Micron, Samsung, and SK Hynix.

LTAs represent another key logic behind Micron's valuation reassessment. Newer LTAs not only lock in purchase volumes but also partially lock in prices, with terms potentially spanning 3-5 years. This differs from past procurement agreements that only locked in volumes. For Micron, the value of LTAs lies in enhancing revenue visibility, reducing price volatility, and improving cross-cycle profitability. For cloud providers and AI customers, LTAs can secure future memory supply and partially lock in costs, avoiding passive acceptance of higher prices during supply tightness. If LTAs become widely adopted, Micron's business model could gradually transform from a traditional cyclical commodity company to a semiconductor supplier characterized by long-term orders, stable cash flows, and higher customer stickiness.

Earnings and Cash Flow Support Valuation Restructuring

Micron's FY2026 Q2 adjusted free cash flow reached $6.9 billion, and the company's Board of Directors approved a 30% increase in the quarterly dividend. This indicates not only a significant improvement in profitability but also a clear enhancement in cash flow quality. In capital markets, stable and substantial free cash flow typically supports higher valuations. Micron's valuation was relatively low in the past, mainly due to market concerns about earnings sustainability. Now, if AI demand, LTAs, and the HBM product mix upgrade collectively reduce cyclical volatility, Micron has the potential to shift its valuation from a traditional memory cyclical stock towards that of a core AI semiconductor asset.

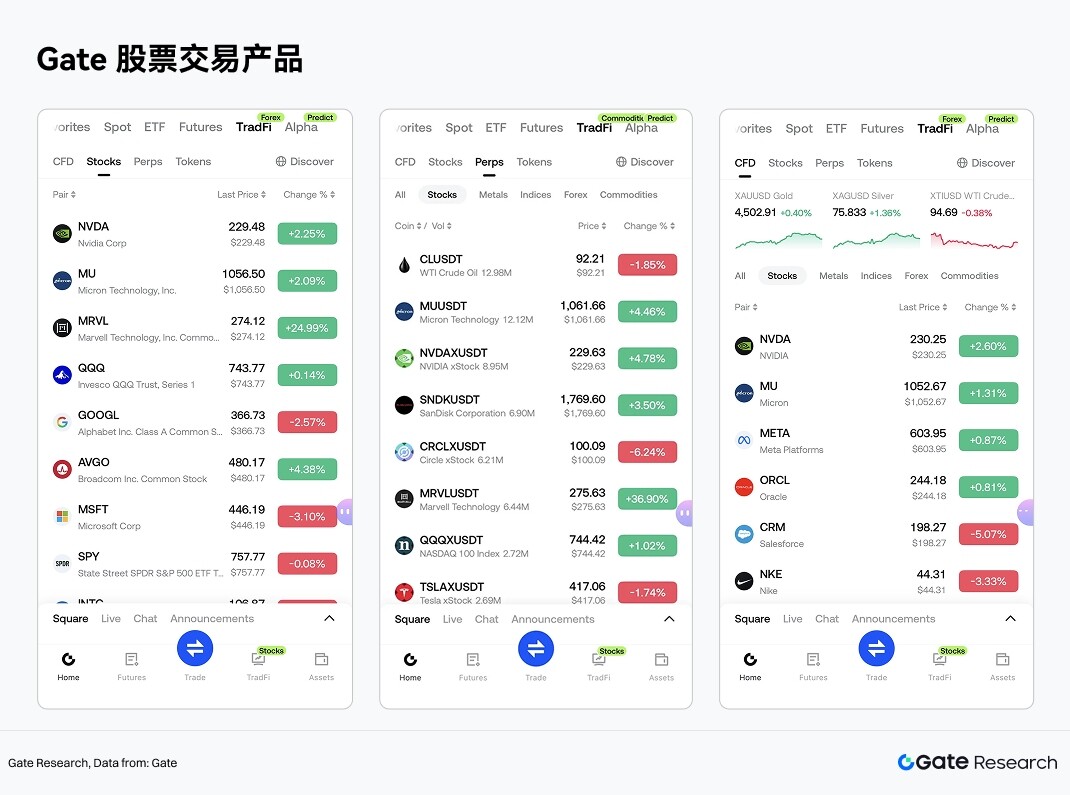

Gate Stock Investment Products

The storage track features some of the most closely watched US stock targets. Gate has also introduced related US stock trading services within its TradFi segment, allowing users to participate in trading stocks and ETFs from major securities markets using USDT through a unified account system.

Unlike common market models involving stock tokenization or RWA mapping, Gate Stock service emphasizes market access capabilities and compliant trading infrastructure. Gate Stock provides stock and ETF trading services by connecting to compliant brokerages. These are not on-chain mapped assets or tokenized stock derivatives. Users can buy, hold, and sell stock assets through their Gate account, with relevant holdings, P&L, fund flows, and corporate action information viewable and manageable within a single account.

In terms of asset coverage, Gate Stock currently supports over 10,000 stocks and ETF assets, covering major securities trading markets and liquidity networks such as NYSE, Nasdaq, NYSE Arca, NYSE American, and BATS. Currently, Gate Stock supports intraday trading, with plans to gradually expand to 24/7 round-the-clock trading, providing global users with a more flexible entry point for US stock asset allocation.

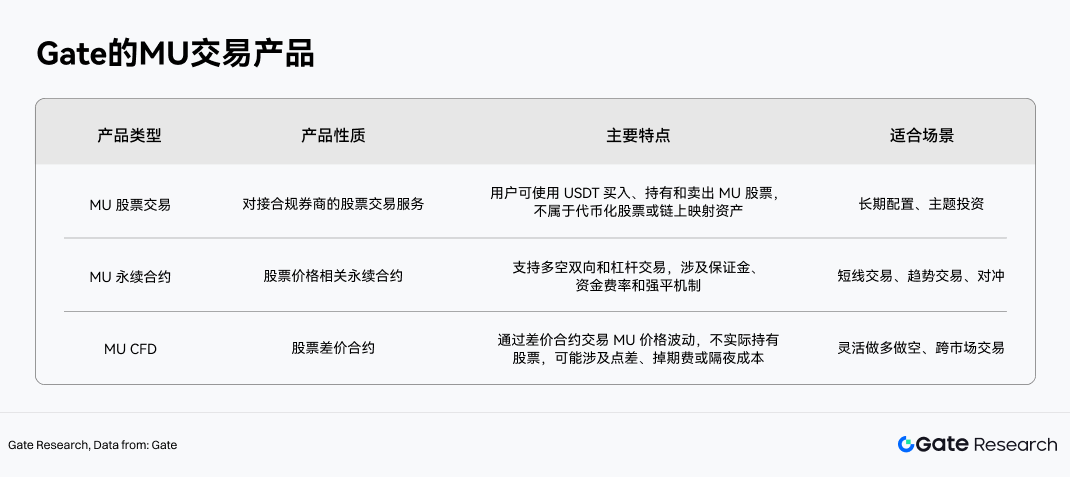

In terms of product structure, the stock-related trading tools in Gate TradFi can be categorized into three types, using the MU trading product as an example:

Among these, Gate Stock spot trading operates independently from the traditional CFD system. Stock trading does not involve funding rates found in perpetual contracts, nor holding costs like swap fees or overnight fees associated with CFD products. Therefore, it is more suitable for users looking for long-term allocation in US stocks. In contrast, perpetual contracts and CFDs are more oriented towards trading tools, suitable for directional trading or risk management based on short-to-medium-term price fluctuations of Micron stock.

Leveraging the unified crypto asset account system, Gate further integrates digital asset trading with stock investment scenarios. After completing KYC and meeting regional access requirements, users can enter the stock section via the TradFi segment in the Gate App to view quotes, and after transferring stablecoins through the trading or asset pages, participate in trading. This signifies that the application scenario for USDT is extending from crypto asset trading to global stock asset allocation.

From an industry trend perspective, Gate's launch of stock trading services provides users with a unified trading entry point for both digital assets and traditional financial assets. For users focused on the AI semiconductor theme, the availability of real stocks, perpetual contracts, and CFDs enables them to engage in more flexible asset allocation and trading management within a single platform, centered around storage, AI, HBM, and the semiconductor cycle.

Risk Warning

From a sector research perspective, assessing the future health of the storage industry and the quality of individual companies can focus on four key dimensions: First, whether capital expenditures by AI servers and cloud providers continue to expand; Second, the penetration rate and ASP changes for high-end segments like HBM, DDR5, and enterprise SSDs; Third, the supply discipline and expansion pace of leading manufacturers like Samsung, SK Hynix, and Micron; Fourth, whether long-term supply agreements, customer qualifications, and advanced packaging capabilities continue to strengthen industry barriers.

This means the storage sector can no longer be fully understood using the old, singular "price cycle stock