沃什首秀前夜:比降息更重要的,是美联储如何重塑预期?

- 核心观点:本周FOMC会议的核心不在于6月是否加息(大概率按兵不动),而在于新任主席凯文·沃什如何重新定义美联储的反应函数,尤其是点阵图是否上移、通胀定性以及缩表策略,这决定了市场对下半年利率路径的预期调整方向。

- 关键要素:

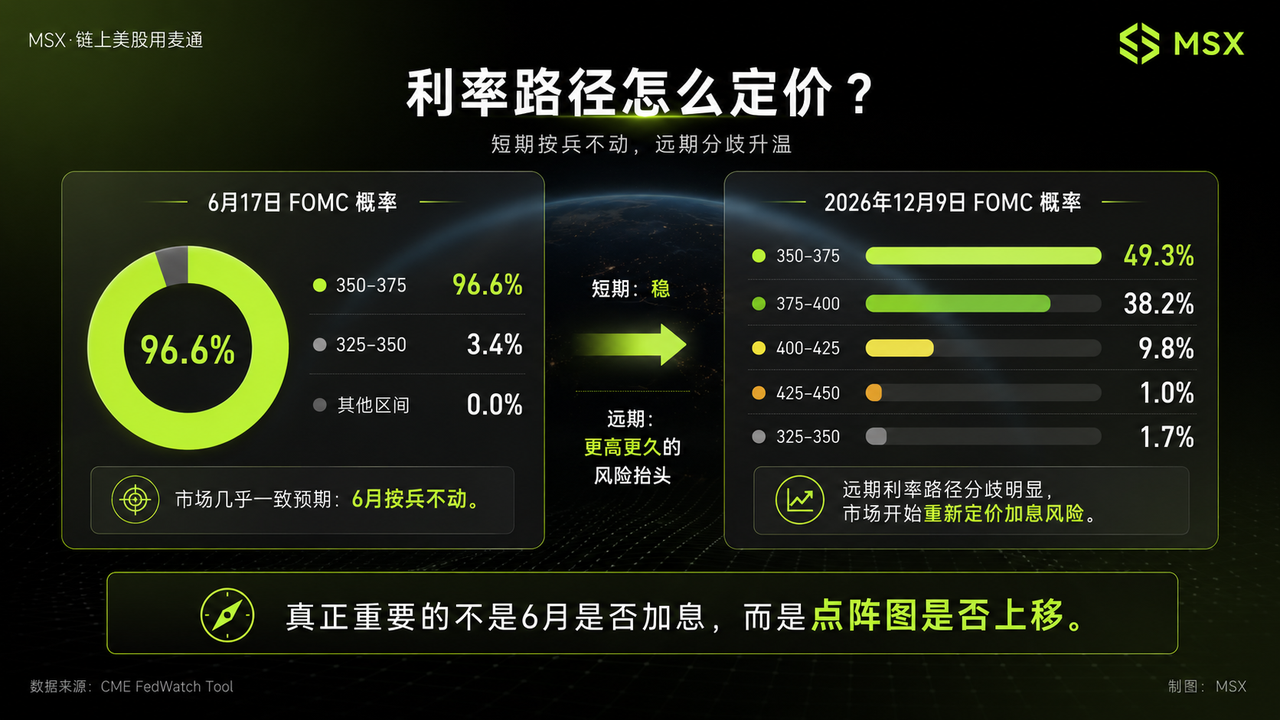

- 市场预期6月维持利率在3.50%-3.75%概率达96.6%,焦点已转向下半年点阵图是否上调,以反映不再默认降息的路径变化。

- 5月CPI同比升至4.2%(能源+23.5%),核心CPI同比2.9%仍高于2%目标,通胀压力复杂化,沃什需定性其为短期冲击还是二次通胀扩散风险。

- 沃什倾向减少前瞻指引和点阵图依赖,强调数据驱动,这削弱了高估值资产(如AI、科技股)依赖的降息预期估值锚。

- 缩表可能是沃什的“中间路线”工具,在利率不变时通过资产负债表正常化释放偏紧信号,重新评估高估值资产的流动性折现。

- 最差风险不是6月不降息,而是美联储降息叙事正式终结,导致市场被迫重新定价利率不确定性。

Original Author: Jim, Frank, MSX Maitong

The most important macro event for the U.S. stock market this week is undoubtedly the June FOMC meeting.

But this time, the market's real concern is no longer a simple question of "hike" or "cut."

According to current market expectations, the Fed is highly likely to hold steady at this meeting, keeping the federal funds rate in the 3.50%-3.75% range. In other words, the lack of a rate move in June is not surprising itself and has already been priced in by the market.

What truly matters is that this is the first time Kevin Warsh will fully preside over a rate-setting meeting as the Fed Chair.

More critically, this meeting will also include the Summary of Economic Projections (SEP), meaning the market will simultaneously see the rate decision, policy statement, dot plot, and economic forecasts. For investors, this is not an ordinary meeting; it is the first complete unveiling of the Warsh-led Fed.

Therefore, the core question for this week's FOMC is not whether Warsh is a hawk or a dove, but what should we really be watching?

1. June Likely to Hold Steady, But the Market is Trading the "Next Step"

Let's start with the conclusion: the Fed is highly likely to hold steady this week.

Based on interest rate futures pricing and mainstream institutional expectations, there is little suspense that the Fed will maintain rates at the June meeting. For instance, the market generally expects the Fed to keep the benchmark rate in the 3.50%-3.75% range. The CME FedWatch Tool also shows a 96.6% probability of rates staying in this range after the June 17 meeting.

Therefore, the real divergence in market opinion is not about June, but about the several meetings in the second half of this year. This is where this FOMC meeting is most likely to be misread.

If one only looks at the June rate decision, it's easy to jump to a simple conclusion: if there's no rate hike, isn't that bullish for U.S. stocks?

Not necessarily.

Because what U.S. stocks truly fear is not the lack of a rate cut this time, but the possibility that the "rate cut path" the market has been trading on gets overturned.

Recently, risk assets, especially AI, semiconductors, software, and small-cap growth stocks, have been enjoying a dual-layer expectation: one, that the economy isn't clearly heading into recession, and two, that the Fed still has room to cut rates in the future. As long as both expectations hold, high-valuation assets can still justify maintaining a higher risk appetite.

But the situation has become more complex now. The U.S. CPI in May rose again to 4.2% year-over-year, with energy prices up 23.5% and gasoline prices up 40.5%. This means that geopolitical tensions in the Middle East, oil price volatility, and supply chain disruptions are now feeding into inflation data. Meanwhile, core CPI rose 0.2% month-over-month and 2.9% year-over-year. While not completely out of control, it remains above the Fed's 2% target.

This data puts the Fed in an awkward position.

If Warsh continues to emphasize room for rate cuts, the market might question whether the Fed is underestimating the rebound in inflation. But if he directly signals a rate hike, high-valuation assets could immediately face valuation compression.

Therefore, the most likely scenario for this meeting is not a clear dovish stance, nor a direct shift to hawkishness, but rather a shift from "the next move is more likely a cut" to "keeping options open."

But this is the key point: while this sounds moderate, its impact on market pricing is anything but moderate.

Because once rate cuts are no longer the default path, the valuation anchor for U.S. stocks needs to be recalculated. Particularly for growth stocks that have already seen significant gains and are trading on stretched valuations, their biggest fear isn't whether rates changed today, but the market suddenly realizing: the second half of the year isn't about waiting for a cut, but about reassessing the risk of a hike.

So, what truly matters this week is not whether the June rate has changed, but whether the Fed officials' projections for the rate path over the next 12 months have shifted upwards.

The dot plot is the first key card of this meeting.

2. Warsh Can't Easily Turn Dovish; Watch His Explanation of Inflation

Warsh is in a very delicate position.

On one hand, his past policy inclinations were closer to the Trump administration, leading the market to believe he might be more supportive of lower interest rates than Powell. On the other hand, he must establish his policy credibility in his debut, especially against the backdrop of re-emerging inflation.

This makes it very difficult for him to start with a strongly dovish stance.

The complexity of the current inflation cycle lies in the fact that it involves both the short-term disruption of an energy shock and the potential risk of spreading to other prices.

If you only look at core CPI, the market could argue that underlying inflation hasn't spiraled out of control. However, looking at headline CPI and energy prices makes it hard for the Fed to completely ignore inflationary pressures. More troublesome is that the Fed's Beige Book also shows that several districts recently reported rising cost and selling price pressures, with energy-related costs spilling over into transportation, packaging, food, and fertilizer sectors. Non-labor input costs are rising faster than selling prices.

This means Warsh cannot simply focus on the 0.2% month-over-month increase in core CPI. The real question he needs to answer is: Is the current inflation merely an energy disruption, or is it evolving into a broader, second-wave inflationary pressure?

If Warsh views the oil price shock and tariff disruptions as largely one-off events and that core inflation remains under control, the market will interpret this as the Fed being in no rush to hike, giving risk assets some breathing room.

But if he emphasizes that energy prices are transmitting to transportation, food, wages, and service prices, or clearly mentions the risk of inflation diffusion, the market will read this press conference as a hawkish shift.

Therefore, the importance of the press conference is no less than the rate decision itself.

The market doesn't just need to hear Warsh say whether inflation is "high or low," but how he characterizes this inflation cycle.

If he defines it as a "short-term shock," that's a relatively friendly signal. If he defines it as a "potentially spreading pressure," it means the Fed still needs to maintain a tighter policy stance. If he further emphasizes the need for the Fed to re-anchor inflation expectations, the market will start to worry about the dot plot, balance sheet reduction, and the rate path all turning hawkish together.

For U.S. stocks, this difference is enormous.

The former implies valuations can still be supported by liquidity and risk appetite, while the latter suggests U.S. bond yields could rise again, leading to a repricing of high-valuation tech stocks first.

For this reason, the real focal point of this FOMC meeting isn't whether Warsh personally is a "hawk" or a "dove," but whether he will lower the Fed's tolerance for inflation.

That is the signal the market cares about most.

3. More Important Than Rates: Balance Sheet Reduction, Communication Style, and Liquidity Expectations

The biggest difference between Warsh and Powell might not be about interest rates, but about the balance sheet and communication style.

In recent years, the market has grown accustomed to the high transparency of the Powell era: press conferences after every meeting, frequent official speeches, and the dot plot providing a path reference. The market could repeatedly trade "rate cut expectations" and "tightening expectations" based on these communications.

But Warsh has always been cautious about such excessive forward guidance. He prefers to reduce the Fed's explicit commitments regarding the future rate path and doesn't want the market to overly rely on central bank statements to bet on asset prices.

This could lead to a significant change: going forward, trading the Fed might not just involve focusing on one phrase about "whether rates will be cut," but returning to the data itself.

In the short term, Warsh is unlikely to immediately scrap the dot plot entirely or plunge the Fed into a "communication black box." However, he could very well diminish the impact of the dot plot and forward guidance by making fewer commitments, providing fewer path hints, and emphasizing data dependency more.

This is not necessarily friendly for risk assets. In the past few years, the valuation support for many high-valuation assets came from the market's forward-looking imagination of the liquidity environment. As long as the market believed the Fed would eventually cut rates, long-duration growth stocks would react in advance. But if Warsh makes the Fed less committed, the market must bear greater interest rate uncertainty.

Another key line is the balance sheet. As of June 10, the Fed's total assets were approximately $6.725 trillion. For Warsh, balance sheet reduction might offer a "middle path" – holding rates steady for now but signaling a tighter stance through balance sheet normalization.

This impact on the market is subtle.

If Warsh merely says the balance sheet will continue its gradual normalization, the market will likely accept it. But if he hints that balance sheet reduction can play a larger role in curbing inflation and reducing liquidity dependency in the future, U.S. stocks will need to reassess their liquidity discount.

Especially for AI, semiconductors, software, and high-quality growth stocks, the core trade recently hasn't just been about earnings growth, but also about the cooperation of interest rates and the liquidity environment. Once the market starts to interpret this as "the Warsh-led Fed is in no hurry to cut rates and doesn't want the market to keep relying on the central bank's safety net," high-valuation sectors will likely face valuation pressure first.

So, for U.S. stocks, the three most important signals this week are very clear:

- First, has the dot plot shifted upward? Specifically, has the outlook for this year shifted from "still room for cuts" to "no cuts, or even risk of hikes"?

- Second, how does Warsh explain inflation? Does he treat the energy shock as a short-term disruption, or does he emphasize the risk of second-wave inflation and cost pass-through?

- Third, will balance sheet reduction and communication style be elevated to a more important position, serving as the starting point for Warsh to reshape the Fed's policy framework?

If the final outcome is holding steady, the dot plot only modestly revised upward, and Warsh emphasizing data dependency without rushing to hike, the market may see short-term volatility but the primary trend for AI and tech stocks might not be broken. As long as oil prices continue to fall and the 10-year Treasury yield doesn't keep rising, high-quality tech stocks could still have room for recovery.

But if the dot plot shifts significantly upward, Warsh emphasizes the risk of inflation diffusion, or frames balance sheet reduction as a more important tightening tool, then U.S. stocks should be wary of short-term valuation compression -- and the hardest hit will still be high-valuation tech stocks, small-cap growth stocks, and the most rate-sensitive long-duration assets.

In other words, the best outcome for this FOMC is not Warsh being overly dovish, but him acknowledging inflation risks without rushing to tighten. The worst outcome isn't the lack of a June rate cut, but the market discovering that the Fed's rate cut narrative has officially ended.

Therefore, from a strategy perspective this week, it is not advisable to blindly bet on a direction before the FOMC.

Conclusion: Don't Bet on an Answer Early, Wait for the Market to Provide Direction

So, in terms of strategy this week, it's not recommended to blindly bet on a direction before the FOMC.

Around the meeting, the market could easily experience a "pump and dump" or a "flush and rally." A safer approach is to wait for the three signals – the dot plot, the press conference, and the U.S. Treasury yield – to materialize before deciding whether to increase positions.

In a nutshell, this FOMC is not about whether Warsh's single statement is hawkish or dovish, but whether he will redefine the Fed's reaction function.

If the answer is "no," the risk-on trade has room to continue. If the answer is "yes," the market must learn how to price a Federal Reserve that offers fewer commitments, places more weight on inflation, and emphasizes liquidity discipline.

Let's wait and see.