1 trillion market cap "Yi-Zhong-Tian" trio: Who offers the best value for money?

- Core Viewpoint: This article provides an in-depth analysis of the value-for-money differences among A-share optical module trio "Yi-Zhong-Tian" (Eoptolink, Zhongji Innolight, and TFC Communication) amid the AI-driven rally. It points out that their valuation logics differ, and reveals the underlying risk that China’s optical module industry's profit pool is constrained by the upstream chip sector.

- Key Elements:

- Eoptolink, with a PEG ratio of approximately 0.30, appears to be the best value on paper. However, due to concentrated customer base, 78% overseas revenue, and a lackluster technology narrative, its low valuation incorporates a discount for "sustainability."

- Zhongji Innolight, as the industry leader, holds the highest earnings certainty thanks to its dominant share in NVIDIA’s 800G and 1.6T modules. Yet its trailing P/E ratio is as high as 73-74x, and it faces geopolitical risks from being included on the U.S. "1260H List."

- TFC Communication, as the upstream "picks-and-shovels" supplier, enjoys a gross margin exceeding 50% and benefits from CPO architecture upgrades. However, its earnings flexibility is limited, its valuation is the highest among the trio, and consensus estimates from institutions are prone to errors due to the misapplication of module-level logic.

- Optical modules are essentially system integration products, while the true profit pool lies in upstream laser chips. Overseas players like Lumentum and Coherent have posted strong earnings. Moreover, CPO requires their CW light sources, meaning that as the "Yi-Zhong-Tian" trio expands, it only enlarges the playing field for upstream suppliers.

- Breakthroughs by domestic chipmakers, such as Yuanjie Technology in areas like 100G EML chips, serve as hidden variables that will determine whether the "Yi-Zhong-Tian" trio can transition from an assembly-based moat to the chip level, thereby capturing better profits.

Douyin influencer "Li Yien" has found his recipe for viral traffic. Before commenting on the stock market daily, he always starts with his catchphrase, "As I always say, time will prove the value of optical modules and computing power." After shouting this for over a year, his single-video likes have surged from two or three thousand to forty or fifty thousand. Netizens flooding the comment section only ask one thing: isn't it too late to finally "step into the spotlight"?

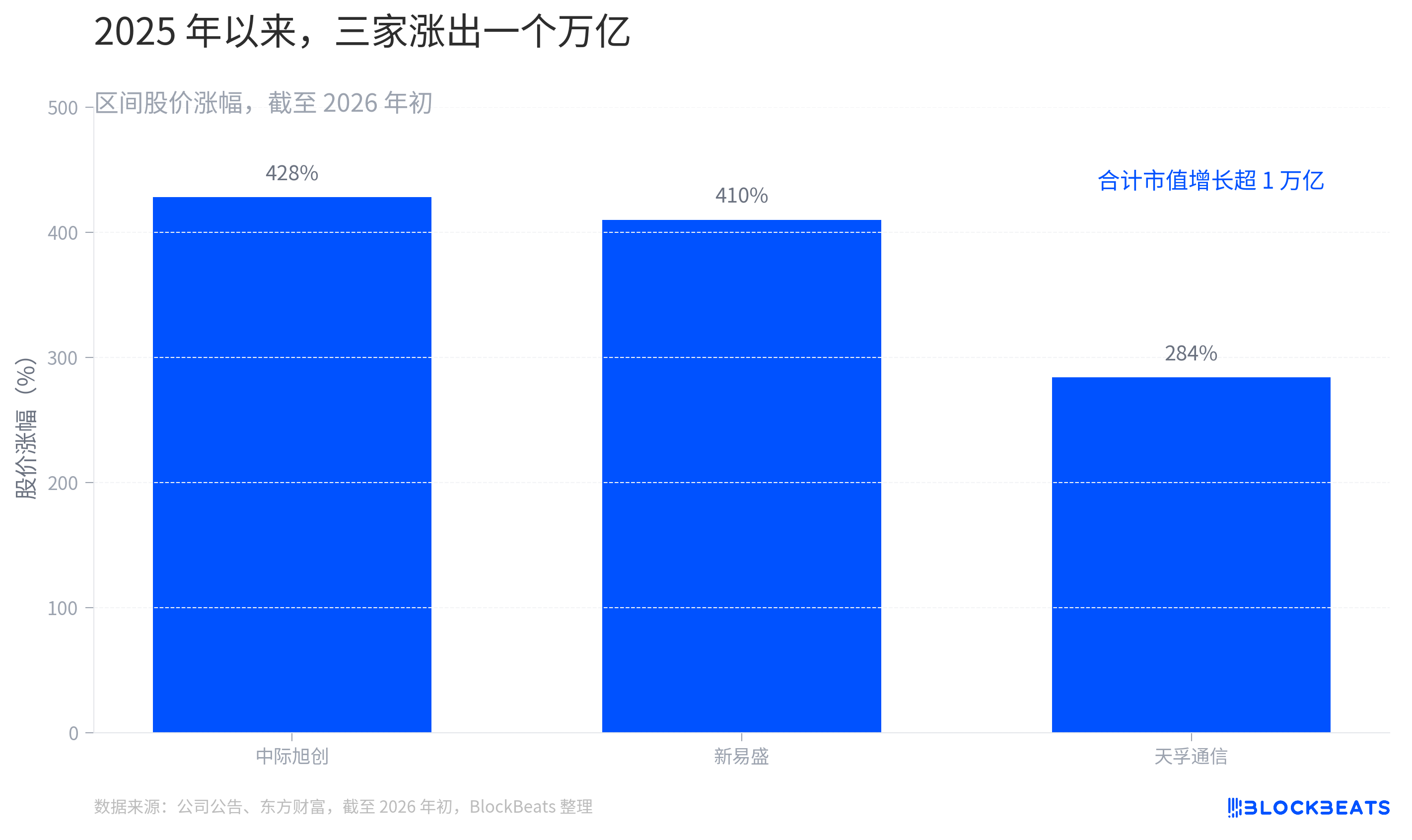

The three words stringing together netizens' anxiety are "Yi-Zhong-Tian". It's not the scholar from the "Lecture Room" program, but a nickname for A-shares' three optical module giants: 新易盛 (Eoptolink), 中际旭创 (Zhongji Innolight), and 天孚通信 (TFC Communication), taking one character from each name. From the low point in April 2025, Eoptolink has risen 16 times, Zhongji Innolight 17 times, and TFC Communication 10 times. Early buyers have made a killing.

But come June 2026, the story takes a twist. On June 5th, "Yi-Zhong-Tian" collectively plunged, with Zhongji Innolight falling nearly 8% in a single day. On June 11th, Eoptolink approached the daily limit down during trading, and the CPO concept began to correct. Those fleeing and those rushing to buy the dip completed their handover amid massive trading volume.

The wealth-creating story has been told to death. The question no one seriously answers is another: if you could only choose one of the three, which is the most valuable? In this article, we won't discuss "whether you can still get on board," but only break down one question: among Yi-Zhong-Tian, who offers the best value for money?

For this round of optical module rally, no one is looking at the current P/E ratio anymore.

The reason is simple: when a company's profit is still growing at a triple-digit rate, calculating the P/E ratio using the past twelve months' profit yields meaningless numbers. The anchor for market pricing has shifted from "how much they earn this year" to "how much they can earn in 2026 and 2027." As of early 2026, the stock price increases of the three companies since 2025 are: Zhongji Innolight 428%, Eoptolink 410%, and TFC Communication 284%, with a combined market cap increase of over one trillion yuan. This trillion yuan buys not the present, but expectations for the next two to three years.

So "value for money" here isn't "which stock price is lower," but needs to be broken down into three yardsticks for measurement. The first is PEG, the price/earnings to growth ratio, measuring "how much you pay for the same growth." The second is earnings quality, measuring how clean the money earned is and how high the gross margin is. The third is the certainty premium/discount, measuring how much the market pays extra for "stability" and deducts for "uncertainty."

Measured by these three yardsticks, the three companies present three completely different answers. One is the value-for-money king on paper, one is expensive but stable certainty, and one is the most expensive certainty.

Eoptolink: The Value-for-Money King on Paper, but Cheap for a Reason

Let's first look at the cheapest one on paper.

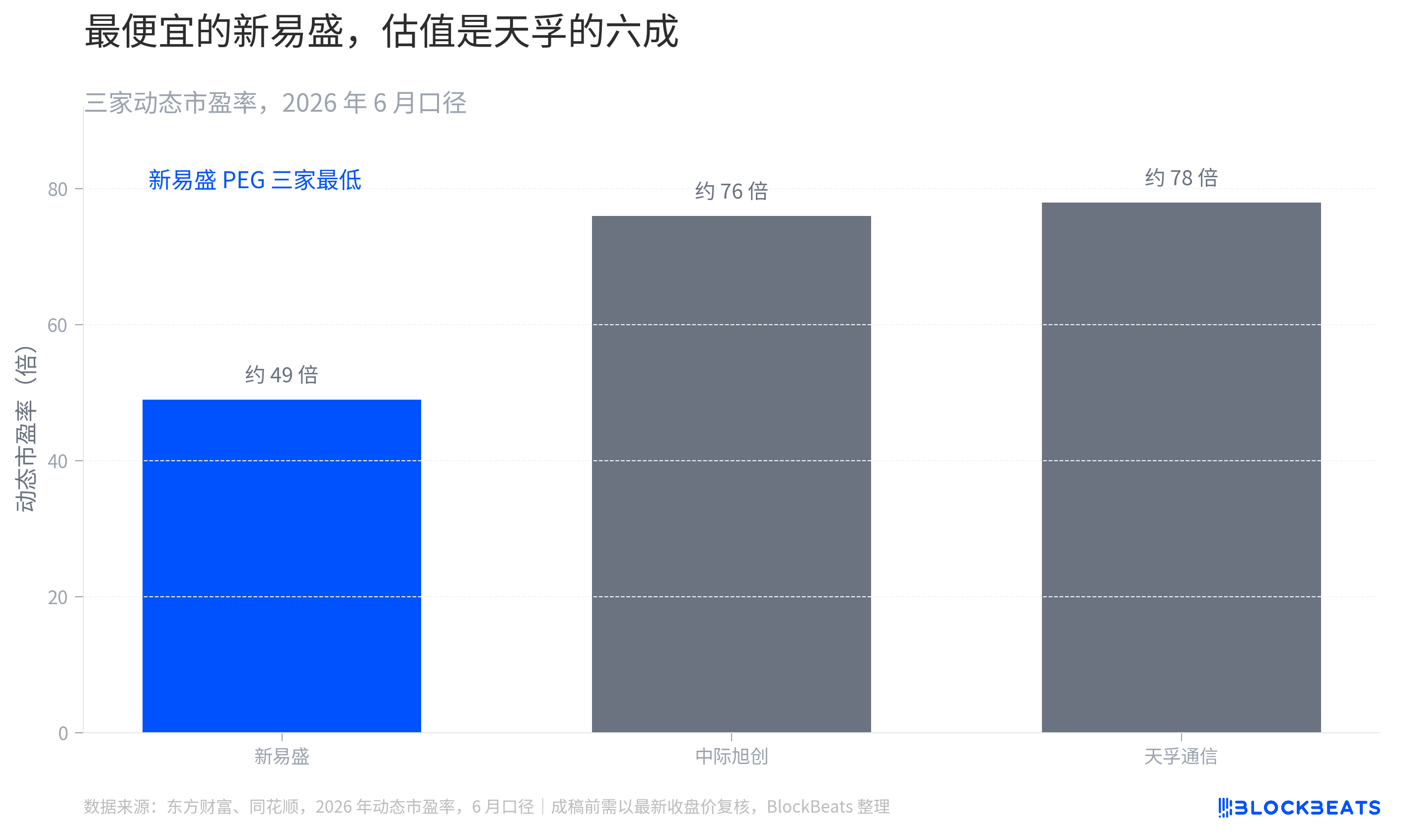

Calculated by PEG, Eoptolink is the most cost-effective among the three. Its net profit attributable to the parent company in 2025 grew nearly 2.5 times year-on-year, significantly higher than Zhongji Innolight's 89.5% to 128% during the same period. Net profit in the fourth quarter was still up +39% month-on-month, with 1.6T products ramping up ahead of schedule. With such strong growth, its valuation is the lowest. Based on the 2026 institutional consensus expected net profit, its forward P/E ratio is only about 22.8 times, corresponding to a PEG of about 0.30, the lowest among the three. For the same unit of growth, you pay the least for Eoptolink.

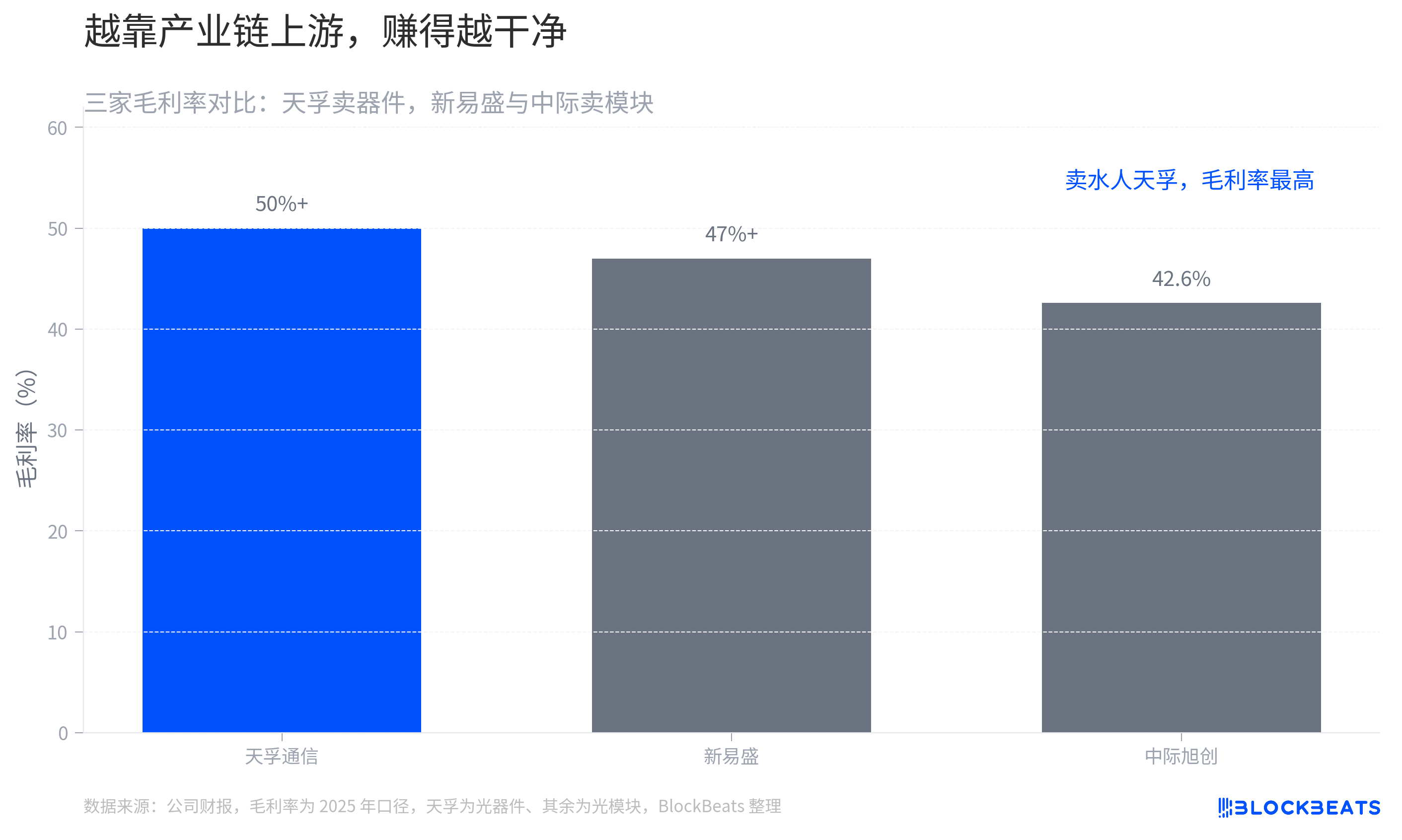

Not only is it cheap, but the money it earns is also the "cleanest." In its 2025 performance, Eoptolink's non-recurring gains and losses were only 33 million yuan, with gross margins maintained above 47%, relying on cost advantages from vertical integration. In terms of earnings quality, it even surpasses the larger Zhongji Innolight.

So far, Eoptolink looks like a dark horse undervalued by the market. But this is precisely where one mustn't stop at the surface. Its cheapness is a discount, not a windfall.

The market doesn't discount a high-growth company for no reason. Eoptolink's suppressed valuation reflects several real risk points. Customer concentration is relatively high, with performance heavily dependent on a few major clients. Overseas revenue accounts for 78%, directly exposing it to tail risks from tariffs and trade restrictions. Most crucially, can the "dark horse's" explosive power be sustained? In terms of long-term technological narrative and forward-looking布局, its story isn't as compelling as Zhongji Innolight's. The low P/E ratio the market gives it is essentially a discount on "sustainability."

This discount is being partially repaired. In 2026, Eoptolink's stock price has already risen over 79%, and it is planning a Hong Kong listing. Capital is voting with its feet, pulling it from "an untrusted dark horse" towards "a re-priced leader." It's cheap, but the cheapness is converging.

So, what about the expensive one? Where is its stability?

Zhongji Innolight: Expensive Certainty

Zhongji Innolight's value isn't in cheapness; it's in certainty.

A comparison makes this clear. In the first quarter of 2026, Zhongji Innolight's single-quarter revenue was 19.496 billion yuan and net profit was 5.735 billion yuan. The net profit from just one quarter exceeded its total for the entire year of 2024. During the same period, its gross margin for optical communication transceiver modules rose from 34.65% in 2024 to 42.61%, an increase of nearly 8 percentage points. Scale is growing, and profit efficiency is improving – this is the hallmark of a leader.

What underpins this certainty is market share and technological advantage. Zhongji Innolight secured over half of Nvidia's 800G optical module procurement. For the 1.6T generation, leveraging its first-mover advantage of being first to complete Nvidia's verification, the market expects it to capture 50% to 60% market share. At last year's Q3 performance briefing, company executives laid out the pace clearly: "In the third quarter of this year, key customers will begin deploying 1.6T and continuously increase orders... It is expected that other key customers will also deploy 1.6T on a large scale from 2026 to 2027." To handle these orders, the company is preparing chips and expanding capacity, domestically and internationally.

The price is that it's the most expensive. Zhongji Innolight's trailing P/E ratio once reached 73 to 74 times, over 40% higher than Eoptolink. What you pay for is a premium for "industry leadership + technological edge." This premium suits those who value certainty more and can afford the high price.

But certainty doesn't mean no risk, and its risks lean more towards "black swan" events. On June 8, 2026 (US time), Zhongji Innolight was added to the U.S. Department of Defense's "1260H List." The company responded urgently, stating the designation does not align with objective facts, that it is neither a military enterprise nor a civil-military integration enterprise, and that it has had no material impact on operations, with orders, production, and supply chain all normal. Despite the response, for a company with overseas revenue accounting for as high as 86.8%, geopolitics is the real sword hanging overhead. It may not affect fundamentals, but it can slash valuation on any trading day.

After analyzing the two module manufacturers, we are left with TFC, which isn't even at the same table.

TFC Communication: The Most Expensive Certainty, Betting on the Next-Generation Architecture

What makes TFC Communication special? It doesn't sell modules; it sells "water."

An industry chain analogy is most intuitive. If Zhongji Innolight and Eoptolink are restaurants directly serving diners, TFC Communication is the supplier to those restaurants. It sells core components like optical engines and optical devices to downstream optical module manufacturers, who then assemble them into complete modules for shipment. It doesn't directly take orders from cloud vendors, but every high-end optical module contains its components.

Being upstream gives it the highest gross margin among the three, consistently above 50%, with the clearest competitive landscape. More importantly, it has bet on a highly certain long-term track: CPO/NPO architecture. Some institutions estimate that in the value chain of a high-end 51.2T switch, the combined potential value of TFC's FAU, precision lenses, and optical engine packaging could reach around $7,000 to $10,000.

Compared to the tens of dollars of component value in the traditional pluggable era, this is a complete volume and price increase. No matter which module solution downstream cloud vendors ultimately choose, as long as data centers continue evolving towards more efficient and energy-saving architectures, the position of the "water seller" remains solid.

Sounds great. But TFC's problem lies precisely in that "water seller" label. It has the least upside potential, the most expensive valuation, and is most prone to expectation gaps.

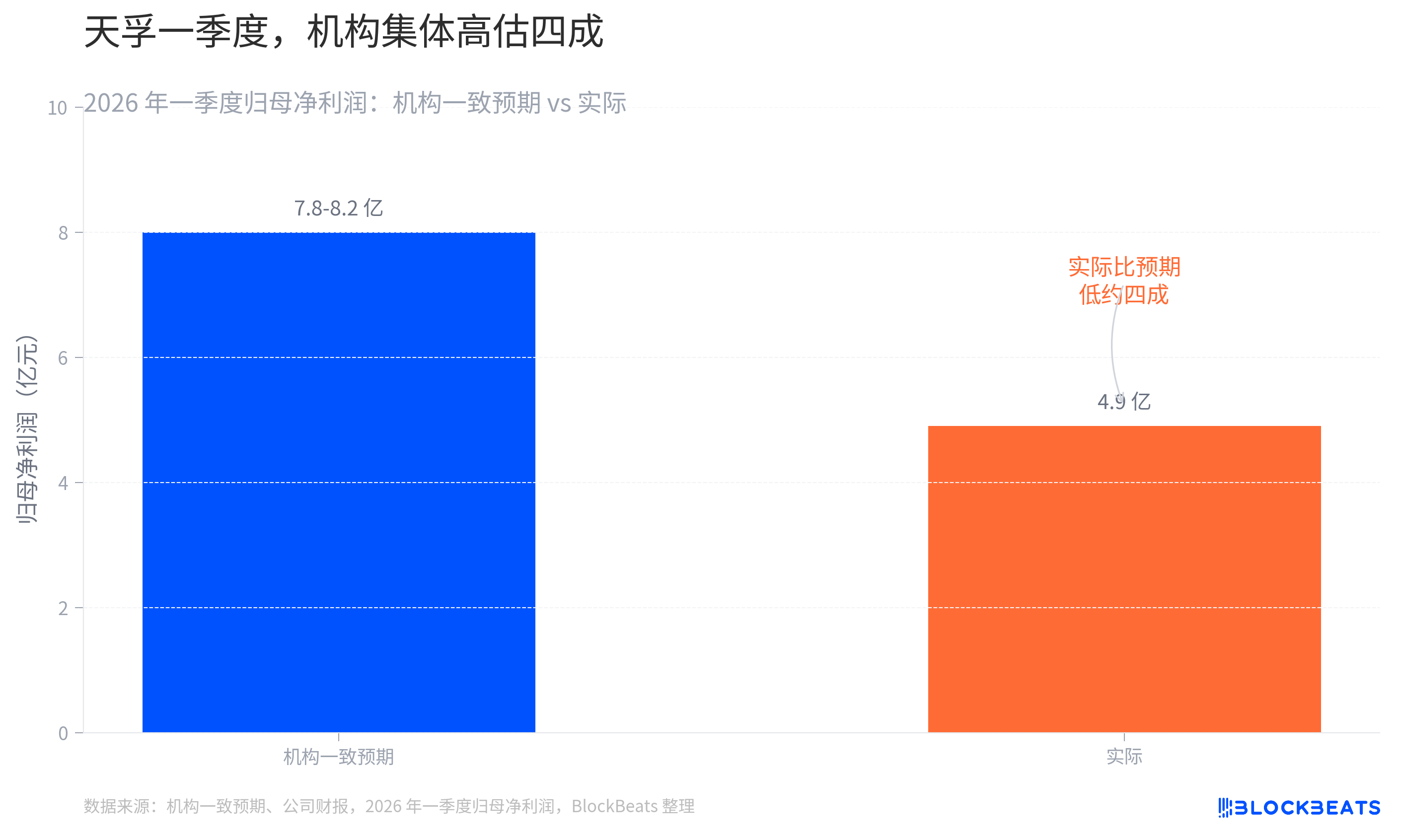

Upside potential is small because its growth is a steady stream, not a pulse. Zhongji Innolight and Eoptolink directly benefit from the pulsed explosion of AI capital expenditure, with huge earnings elasticity. TFC's growth is stable but gradual. The valuation is expensive because the market has priced this certainty ahead of time. As of February 10, 2026, its trailing P/E ratio was about 122 times, far higher than the other two. And regarding expectation gaps, the first quarter of 2026 just provided a bloody lesson. The institutional consensus expected its quarterly net profit to be between 780 million and 820 million yuan, but the actual figure was only 490 million yuan. This huge gap resulted from institutions applying the pulse logic of module manufacturers to an optical device company.

This precisely reminds everyone trying to rank "Yi-Zhong-Tian": TFC and the other two are not the same dish. Pricing a company selling engines using the logic of a company selling complete machines is itself a misinterpretation.

So, the analysis of the three is done. But the "value for money" equation has one hidden variable no one has accounted for.

They Don't Hold the Profit Pool

Let's return to that poker table and ask a tougher question: Is the money "Yi-Zhong-Tian" earns actually "good money"?

The essence of an optical module is system integration. It procures optical chips, electrical chips, and optical devices, then assembles them into a complete module using packaging technology. The barrier isn't the assembly itself. The real profit pools and moats are concentrated at the two ends of the industry chain: upstream laser chips and switching chips. What Chinese manufacturers dominate is the middle assembly process.

Therefore, many people's claims about "Zhongji crushing Lumentum and Coherent" need to be viewed on two levels. In terms of module market share, it's true. Zhongji Innolight has indeed surpassed these two established US manufacturers. But in terms of profit quality, it's a different story.

Lumentum and Coherent guard precisely the upstream end. They use vertically integrated laser chip supply to hedge against shortage risks. The advantages of III-V platforms like Indium Phosphide and Gallium Arsenide in high-power applications remain real. Moreover, these two are not defeated losers; they are upstream players rapidly recovering. Lumentum's revenue in the first fiscal quarter of 2026 grew 58% year-over-year, with gross margins rising from 28% to 34%.

Coherent achieved single-quarter revenue of $1.81 billion in the same period, up 21% YoY. Its data center and communications business now accounts for three-quarters of total revenue, growing over 40% YoY, with non-GAAP gross margins reaching 39.6%.

The sharper point is this. The trillion-yuan valuation of Yi-Zhong-Tian in this round bets on the transition to the CPO architecture. CPO relies on CW light sources and Indium Phosphide substrates, precisely the stronghold of US manufacturers. Coherent is doubling its Indium Phosphide capacity. Its factory in Sherman, Texas, USA, is the world's most advanced Indium Phosphide production line, specifically ramping up CW lasers for solutions including Nvidia's CPO.

The more Yi-Zhong-Tian bets on architecture upgrades, the more they expand territory for upstream US chip companies. So, Yi-Zhong-Tian earns money from assembly and devices, while Coherent and Lumentum earn money from chips. The latter is thinner and slower, but more sustainable.

This is also why people often mention "Yuanjie High-Power Lasers" alongside "Yi-Zhong-Tian." Yuanjie Technology represents the effort of domestic laser chips to climb the upstream industry chain. Its 100G EML passed customer verification in 2025 and entered mass production in 2026. Its CW 100mW high-power light source has also achieved batch delivery, with Q1 revenue growing over three times YoY. If this layer can truly break through at the most profitable bottlenecks of EML and high-power laser chips, then "Yi-Zhong-Tian's" moat will extend from assembly to chips, making the binding truly solid. If they cannot climb up, no matter how good the value-for-money is, they will just be earning a tough living.

This is the real hidden variable for measuring the long-term value-for-money of the three companies. It's not whose PEG is lower, but whether China's optical module industry can snatch the profit pool from upstream.

Will time prove the value of optical modules and computing power? No one knows. But at least, those standing in the spotlight should first figure out which beam they are standing in.