เขียนหลังจาก SpaceX เปิดตัวครั้งแรก: มูลค่าตลาด 2.1 ล้านล้านดอลลาร์ ยังน่าลงทุนตามหรือไม่?

- ประเด็นหลัก: SpaceX เข้าจดทะเบียนในวันที่ 12 มิถุนายนด้วยราคา IPO 135 ดอลลาร์ ปิดวันแรกที่ 160.95 ดอลลาร์ มูลค่าตลาด 2.1 ล้านล้านดอลลาร์ แม้ผลงานจะประสบความสำเร็จ แต่ต่ำกว่าความคาดหวังของตลาดส่วนหนึ่ง สะท้อนให้เห็นถึงการประเมินอย่างมีเหตุผลของตลาดต่อมูลค่าที่สูงและธุรกิจที่ขาดทุนของบริษัท

- ปัจจัยสำคัญ:

- SpaceX กำหนดราคา IPO ที่ 135 ดอลลาร์ เปิดตลาดวันแรกที่ 150 ดอลลาร์ ปิดที่ 160.95 ดอลลาร์; การถือหุ้นกระจุกตัวสูง กรรมการผู้บริหารมีระยะเวลาล็อคอัปนานสุด 366 วัน มูลค่าตลาดหมุนเวียน初期อยู่ที่ประมาณ 750 พันล้านดอลลาร์

- SpaceX ขาดทุนสุทธิทั้งปี 2025 จำนวน 4.9 พันล้านดอลลาร์ และไตรมาส 1 ปี 2026 ขาดทุน 4.28 พันล้านดอลลาร์; ธุรกิจที่ทำกำไรได้เพียงแห่งเดียวคือ Starlink ซึ่งมีกำไรจากการดำเนินงานปี 2025 อยู่ที่ 4.423 พันล้านดอลลาร์ แต่ธุรกิจปล่อยจรวดขาดทุน 657 ล้านดอลลาร์

- Elon Musk ระบุในหนังสือชี้ชวนถึงแผนธุรกิจขุมพลังคอมพิวเตอร์ในอวกาศ (กำลังการผลิต 100GW ต่อปี) และอ้างว่าตลาดศักยภาพสูงถึง 28.5 ล้านล้านดอลลาร์ ซึ่งมากกว่าความสามารถในการทำกำไรที่แท้จริงอย่างมาก ถูกวิจารณ์ว่าเป็น “นิยายไซไฟ”

- สัดส่วนการจัดสรรหุ้น IPO ให้กับนักลงทุนรายย่อยสูงถึงประมาณ 20% ซึ่งสูงกว่าระดับปกติอย่างมีนัยสำคัญ แต่ผลการดำเนินงานของตลาดแสดงให้เห็นว่านักลงทุนรายย่อยให้ความสนใจกับราคามากกว่า พฤติกรรมของพวกเขาเพิ่มความผันผวนมากกว่าที่จะผลักดันให้ราคาปรับตัวขึ้นในที่สุด

- ช่วงเวลาสำคัญคือ: เดือนกรกฎาคมมีแนวโน้มสูงมากที่จะถูกบรรจุเข้าดัชนี Nasdaq 100 อย่างรวดเร็ว ซึ่งจะนำเงินทุนแบบพาสซีฟนับหมื่นล้านดอลลาร์เข้ามา; เดือนสิงหาคมมีรายงานผลประกอบการ Q2 และการปลดล็อคหุ้นภายในส่วนหนึ่ง ทำให้เกิดความไม่แน่นอนในตลาดเพิ่มขึ้น

Author | Golem (@web3_golem)

On June 12, U.S. local time, Musk did not go to New York. Before SpaceX stock (Nasdaq: SPCX) officially debuted on Nasdaq, he chose to stay at the company's Texas headquarters, standing among employees to complete a remote bell-ringing ceremony.

During the ceremony, Musk once again told the story of SpaceX to a wider audience. He stated that the company's goal is to send humanity to the Moon, Mars, and even more distant stars. After the bell-ringing, Nasdaq's live channel played Elton John's "Rocketman," adding a romantic footnote to the most anticipated IPO in the history of space commercialization.

But the emotional part ended there, and the games of the capital market began immediately. SpaceX's IPO was priced at $135, opened at $150 on its first trading day, briefly rose above $176 intraday, and eventually closed at $160.95, giving it a temporary market cap of $2.1 trillion.

Opened at $150, Market Cap Settled at $2.1 Trillion on Debut Day

SpaceX's IPO has been a global focus since it filed its registration statement with the U.S. SEC. The company finally decided to issue approximately 555.6 million Class A common shares at a fixed price of $135, corresponding to a company valuation of $1.77 trillion.

Regarding equity distribution, Musk personally holds about 42%, Valor Equity holds about 7.3%, Google holds about 5%, other early venture capital firms collectively hold 10-12%, employees and former employees hold 10-15%, and the IPO offering accounts for only 4.2%. Although Musk and his surrounding interest groups hold the majority of SpaceX shares, none of their shares can be sold on the listing day. The lock-up period for core investors like Musk and Valor Equity is 366 days, while regular IPO shareholders (institutions and employees) must undergo a basic lock-up of 180 days, meaning they cannot sell until at least the end of 2026.

Therefore, on the listing day of June 12, the initial circulating shares were only the approximately 555.6 million Class A common shares from the IPO offering. SpaceX is a typical "low float, high FDV" project. According to its valuation model, the first-day circulating market cap was about $75 billion, which aligns closely with SpaceX's originally planned fundraising amount.

Investors familiar with crypto projects may not be strangers to high-control models. Therefore, during the subscription phase, market sentiment quickly fell into FOMO. Reports indicate that SpaceX received over four times oversubscription, with total subscription demand from institutions and retail investors exceeding $250 billion. Retail investors alone subscribed for over $100 billion, far exceeding the $75 billion offering size. Crypto players also participated in this feast, but unfortunately, most ended up empty-handed. (Related reading: SpaceX On-Chain IPO Dreams Dashed: In a Trillion-Dollar IPO Feast, I Only Got 4 Shares)

Notably, SpaceX unusually planned to allocate up to 30% of its IPO shares to retail investors, significantly lowering the barrier to participation in this tech feast. Typically, large IPO projects allocate only 5% to 10% to retail investors. Although SpaceX ultimately allocated about 20%, it is still double the conventional IPO ratio.

The reason for this is that SpaceX management believes retail investors will hold their shares long-term, similar to how Tesla's core investor base currently consists of many retail investors. Essentially, they trust that retail investors will pay for the dream Musk describes, but this time retail investors were much more rational than they imagined (detailed below).

Before SPCX officially started trading on Nasdaq, the pre-IPO quotes on Hyperliquid fluctuated between $170 and $175, corresponding to a company valuation exceeding $2.2 trillion. In the Nasdaq call auction before the official open, SPCX's indicative opening price initially stood at $172, up about 29% from the IPO price, basically in line with pre-market expectations. However, after an hour, the indicative opening price quickly slipped, eventually opening at $150, only about 11% above the IPO price.

According to Gate's US stock market data, SPCX eventually rose to around $176 intraday, closing at $160.95, up about 19% from the IPO price but only about 7.3% from the opening price. The first-day market cap settled at $2.1 trillion. From the results, SpaceX's debut performance was definitely a success, making Musk the world's first trillionaire. However, the result was not stunning and even fell short of some market expectations.

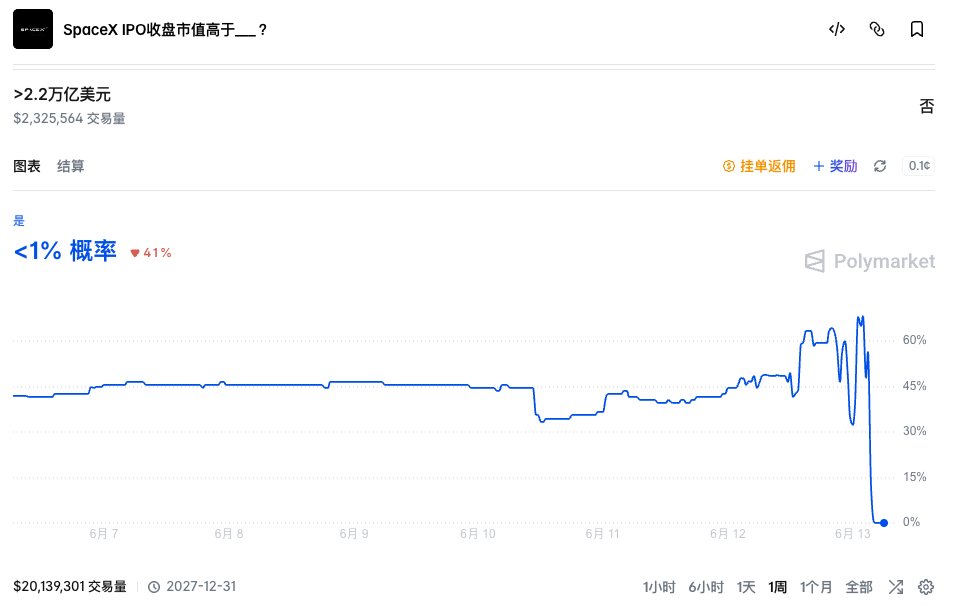

In the pre-pricing of SpaceX, not only did pre-IPO platforms frequently fail, but prediction market results also deviated significantly.

Just hours before the SpaceX IPO, the market generally expected its market cap to break above $2.2 trillion. On Polymarket, the probability of "SpaceX IPO closing market cap above $2.2 trillion" was still above 65%, once surging to 70%.

However, as SPCX's price "opened relatively low," the probability of this event also began to fluctuate wildly. Ultimately, SpaceX's IPO closing market cap settled around $2.1 trillion, and the event was resolved as "No."

Retail Investors Affect Volatility, Not Price Appreciation

There is only one reason for this phenomenon: although the market is still willing to believe in SpaceX's narrative and the "Musk premium," SpaceX is simply too expensive. Given a good price, even the strongest conviction can be sold.

SpaceX is the first mega-cap in human history to directly descend onto the capital market with a "trillion-dollar valuation." On its debut day, its market cap surpassed tech giants like Meta and Samsung, becoming the world's ninth largest company. But even the craziest retail investors know that SpaceX's current revenue cannot support its massive valuation. SpaceX has not yet achieved profitability, with a net loss of $4.9 billion for the full year 2025 and a net loss of approximately $4.28 billion in Q1 2026.

Starlink is currently SpaceX's only profitable business. According to the prospectus data, Starlink generated revenue of $11.387 billion in 2025, accounting for 61% of SpaceX's total revenue, with an operating profit of $4.423 billion. It has over 10.3 million global users and more than 9,600 satellites in orbit. In Q1 2026, it achieved revenue of $3.257 billion and an operating profit of $1.188 billion. But this "cash cow" business is just SpaceX's side hustle.

Space launch is SpaceX's main calling card. As of the prospectus disclosure, the Falcon rocket family has completed over 650 launches with a success rate of 99%. Its rocket booster recovery technology provides a significant cost advantage and technological leadership within the industry. However, SpaceX's largest external customer for launch services is the U.S. government, and this business is still in the red. In 2025, SpaceX's launch business recorded an operating loss of $657 million with a loss rate of 16.1%. In Q1 2026, the operating loss surged to $662 million, with a loss rate of 107%.

The reason for the massive losses is SpaceX's increased spending related to Starship. However, given the current technological and usage scenario bottlenecks, Starship is still some distance away from true commercial mass production.

Beyond these two businesses, SpaceX's yet-to-be-realized space computing business is also factored into its valuation. Compared to the mature Starlink and space launch businesses, Musk's boasts about the space computing business seem a bit exaggerated.

Simply put, SpaceX's plan is to send GPUs into low Earth orbit, using solar power to provide cloud computing power for global AI computing clusters. In the SpaceX prospectus, Musk stated that SpaceX's goal is to deploy 100GW of AI computing capacity into orbit annually. Currently, the global AI industry requires about 15-25GW of electricity per year. This means SpaceX's planned orbital computing system could theoretically support a fivefold expansion of today's global AI industry scale.

In case readers don't know what 100GW represents: the installed capacity of the Three Gorges Dam is about 22.5GW. So, one space computing center in Musk's plan would be equivalent to 4.4 fully operational Three Gorges Dams.

Not only that, but SpaceX also explicitly stated in its prospectus that it expects to unlock a potential market of $28.5 trillion in the future (mainly related to AI businesses). For context, China, currently the world's second-largest economy, had a nominal GDP of approximately $19.4 trillion in 2025. The figure proposed by SpaceX is equivalent to 1.47 times China's 2025 nominal GDP.

Reading this, you might wonder whether this is an IPO prospectus or a piece of science fiction. Even the most FOMO-driven investors need to cool down when they see these numbers. Research firm CFRA issued a "Sell" rating on SpaceX after its listing, with a target price of $115.

Beyond the mismatch between actual business and valuation, the high proportion of retail IPO allocation might also be a reason suppressing SPCX's stock price. Musk allocated 20-30% of SpaceX's IPO shares to retail investors. The larger the retail shareholding, the greater the inherent volatility. Retail investors can buy at any cost driven by FOMO, but they can also sell emotionally at the slightest fluctuation without thinking. Therefore, retail investors truly affect volatility, not the final price appreciation.

Key Upcoming Milestones

Of course, whether you are sitting on the sidelines or have already cashed out, the following two time points are particularly important for investors focused on SpaceX.

Approximately 15 Trading Days Post-IPO (Estimated around July 6-7)

This is the most important milestone, as SpaceX is expected to be directly included in the Nasdaq 100 Index after 15 trading days. In March, Nasdaq specifically revised its rules. Newly listed companies previously had to wait three months to be eligible for index inclusion, but now they can be quickly included after just 15 trading days if conditions are met. The rule also removed the requirement of at least about 10% float. These new rules seem tailor-made for SpaceX and the subsequent wave of AI tech giants.

If SpaceX is successfully included in the index, it means tens of billions of dollars in global funds will passively buy SpaceX shares, providing significant support for its stock price. So, knowing that SpaceX has a very high probability of being included in the Nasdaq in July, and that top-tier funds will then buy this stock, would you as an investor choose to buy now and sell to them at a higher price later?

However, on the other end, some U.S. pension funds and long-term insurance funds have expressed protest. In May 2026, three of the largest U.S. public pension fund managers (with over $1 trillion in assets under management) jointly wrote to Musk, expressing concerns about the potential passive fund risks from rapid index inclusion post-IPO. In the same month, Randi Weingarten, President of the American Federation of Teachers (representing about 1.8 million teachers, healthcare workers, and public employees), directly wrote to the SEC requesting a special review of the SpaceX IPO.

SpaceX Q2 Earnings Report (Mid-to-Early August)

The second important date is the release of SpaceX's Q2 2026 earnings report in August. This will be SpaceX's first report card since listing. If there is no progress in the business compared to the current state (and major progress is unrealistic), its stock price may face further pressure. Additionally, the SpaceX prospectus stipulates that two days after the company releases its Q2 2026 earnings report, eligible internal shareholders (employees, former employees, some early investors) can sell a portion of their locked-up shares. They can sell up to 20% of their locked shares. If the stock price at that time is 30% above the IPO price and meets this standard for 5 out of 10 trading days, an additional 10% can be unlocked.

This means that in August, the market must not only absorb the earnings report volatility but also face the first major unlock of shares since the listing, presenting a huge challenge.

Whether we will be "suffocated" by Musk's dream, at least based on the performance on the first trading day, the market chose to believe the story but did not completely lose its rationality. What will determine SpaceX's fate next is its own real performance.

Recommended Reading:

SpaceX On-Chain IPO Dreams Dashed: In a Trillion-Dollar IPO Feast, I Only Got 4 Shares