OpenAI's Hyperliquid Pre-Market Pricing Business: Why Did It Only Last Six Months?

- Core Insight: In Hyperliquid's Pre-IPO pre-market contract arena, the anonymous team Trade.xyz found success by targeting assets with confirmed listing dates and public pricing (e.g., SpaceX). In contrast, Ventuals, backed by Paradigm, bet on OpenAI and Anthropic, which lack public markets. This led to the failure of its

self-referential

oracle pricing mechanism, culminating in its acquisition and shutdown. This exposes the fatal flaw of this sector: the lack of a fair anchor price. - Key Elements:

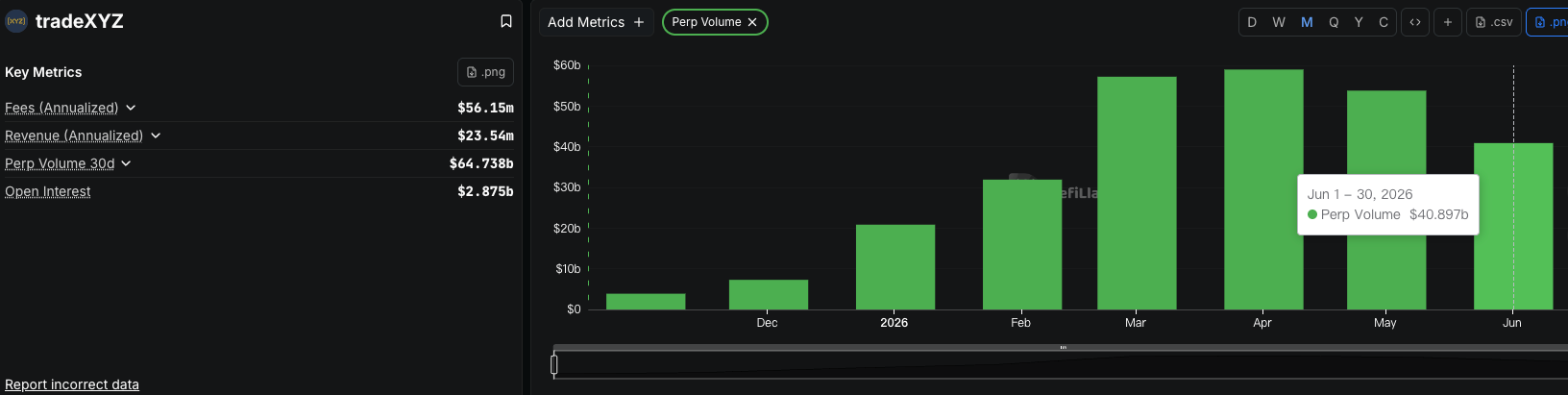

- Trade.xyz holds over 90% of the open interest in Hyperliquid's pre-market contracts. By selecting assets like SpaceX with clear Nasdaq listing plans, it uses public market pricing as a correction anchor, achieving a cumulative trading volume of over $130 billion.

- Paradigm-backed Ventuals chose OpenAI and Anthropic. As neither has a listing date, half of its oracle price came from external secondary share transactions, and the other half from the average price of its own contracts. This caused the price to become self-referential, consistently trading near an upper limit, and lacking validation from real supply and demand.

- When Ventuals shut down, it settled contracts based on a 24-hour average price. The final prices for OpenAI and Anthropic ($1,341.80 and $1,618.90 respectively), reliant on this self-referential mechanism, were questioned for being precise but not real. Ironically, external employees and VCs still use this valuation as a reference.

- Institutions like Coinbase, Polymarket, and Citigroup are entering the pre-market pricing space. This indicates the demand is real and becoming increasingly formalized, but the core challenge (the lack of a public market for price discovery) isn't automatically solved by the involvement of bigger brands.

Original Author: Curry, TechFlow by Shenchao

During the days leading up to the SpaceX IPO, the pre-market price of SPCX on Hyperliquid was all over the feeds, but few people bothered to look into who deployed that market.

It was actually a team called Trade.xyz. Anonymous, only emerged this year. Now, this single team accounts for over 90% of the open interest in pre-market contracts on Hyperliquid. The hype around the SpaceX on-chain Pre-IPO was largely driven by them alone.

And just three days after SpaceX's bell-ringing, on June 15th, another team doing the same business announced its closure.

That team was Ventuals, backed by Paradigm. They also offered pre-market contracts for SpaceX, as well as OpenAI and Anthropic. Launched early this year, it only took nine months from opening to shutting down.

Same chain, same HIP-3 mechanism, same track. One team made SpaceX the largest market of them all, while the other held OpenAI and Anthropic in its hands yet still failed.

The way Ventuals exited is worth pondering. According to its official social media post, it wasn't a case of being unable to sustain losses and running away. The announcement said it was acquired, with the entire team merging into another project within the Hyperliquid ecosystem. User principal was returned 1:1, which counts as a dignified exit.

But therein lies the problem. Holding the two most scarce and sought-after names in the entire market, OpenAI and Anthropic, Ventuals should have been the last one to lose out. So where did it fall short?

Trade XYZ vs. Ventuals

The successful one, Trade.xyz, remains an anonymous team to this day.

The project founder only revealed a bit of background in an interview with Hyperliquid founder Jeff Yan, saying he bought his first Bitcoin for $66 back in 2013. He had been an investor ever since, never actually building a project. He claimed he would have left the crypto space long ago if he hadn't met Jeff.

This relative latecomer built the largest pre-market market on Hyperliquid. According to a report by Colossus, Trade.xyz grew 38% weekly since last October, with cumulative trading volume exceeding $130 billion.

It started with silver, then crude oil, then the S&P 500, and finally got around to SpaceX.

Its choice of SpaceX was very clever.

SpaceX was set to ring the bell on Nasdaq on June 12th, with a confirmed offering price and listing date. By listing a pre-market contract for SpaceX, Trade.xyz was essentially betting on an event with a guaranteed answer. On listing day, Nasdaq would provide the true price. This true price acts like an anchor, preventing the pre-market price from drifting too far. Even if the price was off in the interim, it would be pulled back at the moment of the bell-ring.

And that's exactly what happened. In the days before the SPCX listing, the price was quoted between $154 and $172, betting on a premium above the $135 offering price. It indeed surged after the opening, proving the bet right.

Ventuals chose a different type of asset.

Backed by Paradigm, one of the top-tier VCs in crypto, its pedigree was far more prestigious than the anonymous Trade.xyz. The names it chose were also bigger: OpenAI and Anthropic, the two most coveted assets in the entire market.

But these two companies have no imminent bell-ringing date in the near term.

It's not that there are no anchor prices for them externally. According to Bloomberg, Anthropic allowed employees to sell secondary shares at a $350 billion valuation this year, and OpenAI does this regularly too. However, these are private prices set behind closed doors. In a secondary transaction, buyers and sellers are often the same existing large shareholders who are already heavily invested. The assets haven't truly changed hands in an open market.

Such pricing might be accurate in certain instances, but it lacks an open order book where everyone can take the opposite side to correct errors.

By putting these prices on-chain as contracts, Ventuals essentially suspended the entire market on one or two off-chain price feeds. More troublesome was the mechanism it added, one that effectively competed with itself.

An on-chain analyst dissected Ventuals' pricing logic:

Its oracle price was half derived from external secondary share transactions and financing valuations, and the other half from the moving average of the contract's own price. In other words, half the price was referencing itself. When buying pressure pushed the price up, the moving average rose, causing the oracle to follow, which in turn raised the ceiling further, inviting more buying.

The result was that prices for contracts like OpenAI and Anthropic were perpetually stuck near the ceiling, making sell orders and liquidations very difficult. The charts looked like a steady uptrend, but in reality, it was structurally stuck, having little to do with real supply and demand.

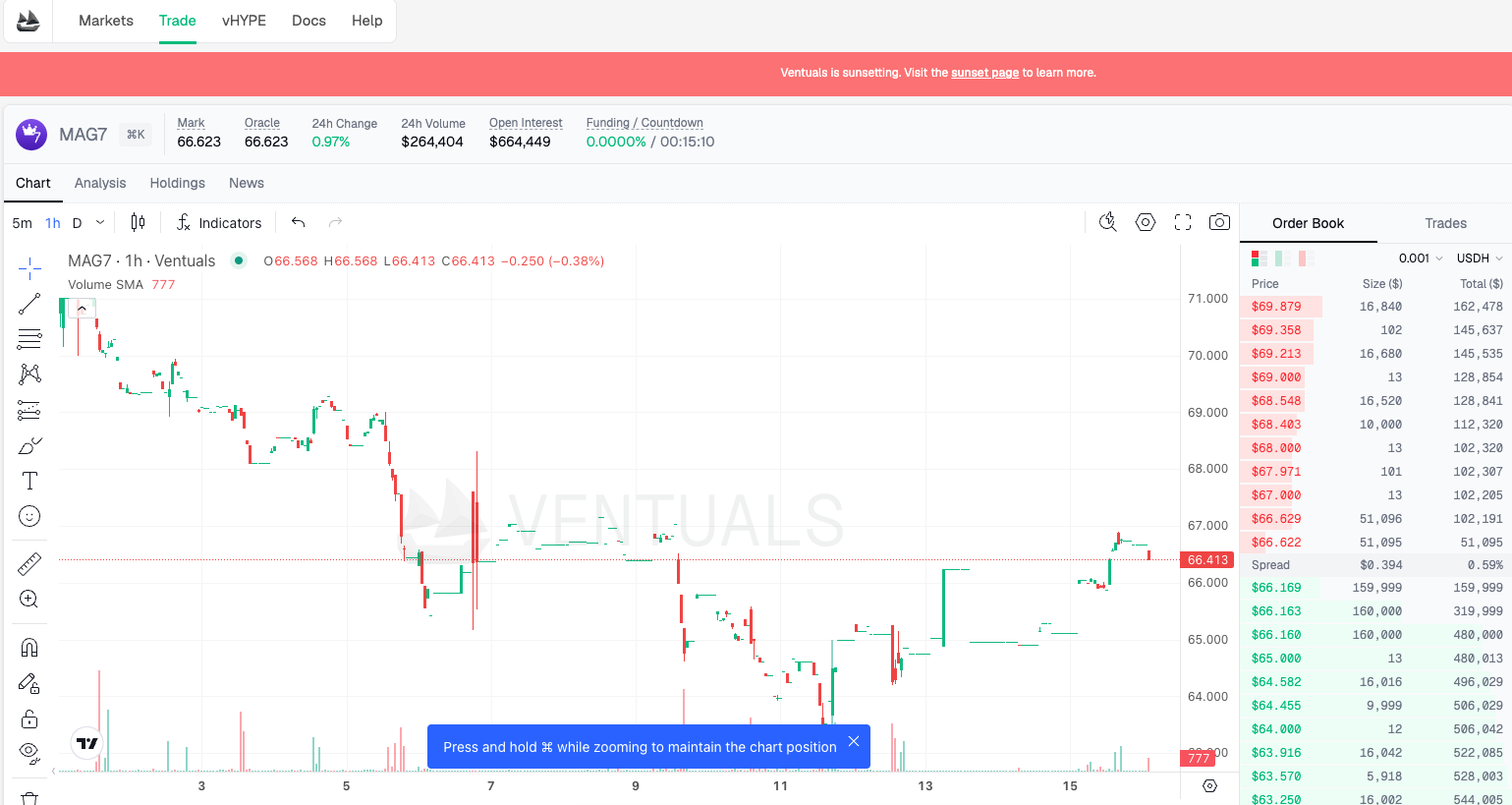

Source: MAG7 asset on Ventuals. Note the intermittent candlestick chart with no trades during some periods.

So, this type of Pre-IPO didn't feel like the market telling you what OpenAI is worth. It felt more like a machine pushing prices up, and then using that self-generated price to push them even higher.

Trade.xyz bet on an asset that would inevitably be "settled" by Nasdaq. If wrong, the true price would act as a safety net. Ventuals bet on assets that only existed in internal quotes for the time being. By wrapping them in a self-referential pricing loop, the price hung in the air without any floor beneath it.

Closing Price Reference: OpenAI at $1300, Anthropic at $1600

When it came time to close shop, did that final quoted price count?

When Ventuals shut down, it needed a final price for its contracts to settle everyone's positions. Its method was to freeze the average price over the past 24 hours. OpenAI was finally priced at $1341.80 per share, and Anthropic at $1618.90 per share.

These two numbers are now etched into the settlement records, becoming the last quoted prices for these two companies on-chain.

As mentioned earlier, this price was half-referenced to external secondary share prices and half to its own moving average, perpetually climbing towards the ceiling. In other words, a significant portion of the $1341.80 figure was the result of the machine pushing up the price it had already created.

It's precise to two decimal places, but it may not be true.

The most ironic part is that people outside actually took this price seriously.

According to Bloomberg, employees of SpaceX, OpenAI, and Anthropic, along with some late-stage VCs, approached Ventuals, saying they were using the platform to value their own equity holdings.

I think this needs closer examination.

These people hold real secondary shares with real money. Logically, they should know best what their stock is worth. But pricing in the primary market is like squeezing toothpaste – it comes out once a year. Between two funding rounds is a blank space, and no one knows how the stock price moves in that gap.

Platforms like Ventuals, however unreliable, at least provide a number 24/7, and you can even see its ups and downs.

Thus, a paradoxical situation emerged. Insiders who should have the highest pricing power were instead looking at numbers on a retail investor's table, seeking some psychological comfort.

This is the most awkward aspect of the pre-market pricing business.

The most scarce assets most lack a fair price. The greater the price gap, the more people cling to anything that looks like a price, even if it was created by a machine competing with itself.

Ventuals has closed up shop, and those two terminal prices are frozen in time. But the demand for referencing such numbers certainly hasn't diminished one bit.

The Pre-Market Pricing Business: Players Rush In

Demand hasn't decreased; instead, supply is increasing, and becoming more regulated.

In the same week Ventuals shut down, Coinbase launched its own pre-market perpetual contracts, with the first asset being SpaceX, targeting users outside the US.

It wasn't just Coinbase. Polymarket used Nasdaq data to create prediction markets for private company valuations. Citi launched tokenized private company shares for its wealth and institutional clients. The crypto space is doing it, and traditional investment banks are doing it too.

This is no longer a small game played by a few anonymous teams on Hyperliquid. Giving unlisted companies a price that can be traded anytime is becoming a legitimate business everyone wants a piece of.

For domestic readers, this demand isn't unfamiliar. Subscribing to new listings requires queuing up. Primary market shares are only distributed among institutions and high-net-worth individuals, leaving ordinary people no way in. Now, when someone lists the prices of companies like OpenAI and SpaceX, allowing 24/7 trading, it's the first time many can touch such assets. The demand is real.

But Ventuals' closure over these past six months has clearly exposed the Achilles' heel of this business.

For price, people willing to trade isn't enough. You need an open market where everyone can take the opposite side to continuously correct errors. Even if Coinbase takes over, this Achilles' heel won't automatically disappear. It just moves from the banner of an anonymous team to a bigger brand name. The underlying company still isn't listed, and that fair price still doesn't exist.

Will the next person to price it be more accurate than Ventuals? The answer probably won't be known until the day OpenAI truly stands at the bell-ringing podium.