美日加息来袭,股债币谁最危险?

- Core View: Global risk assets face dual macro pressure this week: the Bank of Japan (BOJ) is almost certain to raise interest rates by 25 basis points to 1%, back-to-back with the Federal Reserve FOMC meeting. Markets are worried about rising interest rates, reversal of carry trades, and tightening liquidity, potentially triggering market volatility, especially putting pressure on high-valuation growth stocks and crypto assets.

- Key Elements:

- The US May CPI rose 4.2% year-over-year, with non-farm payrolls adding 172,000. Rebounding inflation and resilient employment weaken the case for rate cuts, and the probability of rate hikes is accumulating; Polymarket data shows a ~70.35% probability of no rate cut in 2026.

- The BOJ's policy meeting is on June 15-16. Polymarket indicates a 98.3% probability of a 25bp rate hike. If implemented, the policy rate would rise to its highest level since 1995 (1%), posing a risk of carry trade unwinding.

- Historical experience shows that the BOJ's rate hikes in 2000, 2006-2007, and July 2024 all triggered global market turmoil. For example, in August 2024, the Nikkei 225 plunged 12.4% in a single day, and the Nasdaq fell 3.4%.

- This time, BOJ Governor Kazuo Ueda is absent from the meeting and press conference due to illness, with Deputy Governor Shinichi Uchida chairing the meeting. Uncertainty in communication style could amplify market volatility.

- If the Fed sounds hawkish this week (acknowledging inflation risks, raising the dot plot, or removing dovish language), short-end US Treasury yields would rise, the dollar would strengthen. This, combined with the BOJ rate hike, would reinforce a global tightening effect.

- Pressure on the crypto market is evident: BTC is unstable around $65,000, having fallen to $61,500 after the CPI release. On-chain long liquidations exceeded $1.5 billion, and Bitcoin spot ETFs saw net outflows of $2.7 billion for the week. High-beta assets (like altcoins, meme coins) remain highly vulnerable.

This week, the main narrative in global markets revolves around the Bank of Japan's rate hike and the Federal Reserve meeting. For risk assets, this week is destined to be anything but calm.

Three months ago, Wall Street was still debating when rate cuts would begin. Wash had just taken office, and the market was willing to give the new chairperson the benefit of the doubt. Inflation was trending down, the job market was loosening, and a rate cut was just a matter of time. But the financial world is fickle, and none of the scripts everyone had envisioned played out.

The May CPI rose 4.2% year-over-year and 0.5% month-over-month, with energy prices up 3.9% month-over-month. Core CPI remained around 2.9% year-over-year. Furthermore, employment data didn't give the Fed an immediate reason to pivot dovish. May's non-farm payrolls added 172,000 jobs, and the unemployment rate held steady at 4.3%. This means the Fed is now facing an awkward combination: inflation is picking up again, the job market hasn't shown significant cracks, AI-related investments continue to support economic resilience, the case for rate cuts is weakening, while the conditions for rate hikes are slowly accumulating.

Meanwhile, the Bank of Japan (BOJ) holds its policy meeting on June 15-16. The market has almost priced in a 25 basis point rate hike as the base case. On Polymarket, the "Bank of Japan Decision in June" market shows the probability of a 25bp hike at approximately 98.3%, with rates unchanged at only about 1.45%, and a probability of a 50bp+ hike at around 0.55%.

Many might still remember the significant impact Japan's previous rate hikes had on the overall financial markets. This time, facing the BOJ rate decision on Tuesday and the Fed's FOMC meeting on Thursday, will the market decline?

Wash's "Debut" and Rising Odds of a Fed Rate Hike

Let's first look at the Fed.

The possibility of a rate cut seems to have largely faded. On Polymarket, the probability of "No rate cut in 2026" is about 70.35%, a "Rate cut before July" sits around 2.35%, and a "Rate cut before December" is only about 23%. Seventy percent of bets are placed on no rate cuts at all this year. Regarding the year-end interest rate range, the probability of maintaining a 3.75% upper limit is about 37%, 4.00% is about 32.5%, 4.25% is about 11.25%, and 4.50% or higher is about 3.35%. Collectively, probabilities for 4.00% and above total about 47%.

The market's consensus on Wash is that he will likely hold off on a rate hike during his first appearance, this week's FOMC meeting. The risk of a hike is primarily concentrated after the third quarter. Several markets on Polymarket clearly illustrate this consensus:

"Fed rate hike in 2026?" shows the probability of a hike at any time in 2026 is around 34.5%. "Fed rate hike by...?" indicates probabilities of about 0.65% before June, 6.15% before July, 24.5% before September, and 32% before October. In the "Fed Decision in July" market, a 25bp hike in July is at about 3.15%, a 50bp+ hike around 0.3%, and no change at 93.5%. In "What will the Fed rate be at the end of 2026?", the probability of the year-end upper limit falling at 3.75% is about 37%, 4.00% is 32.5%, 4.25% is 11.25%, and 4.50% or higher is 3.35%.

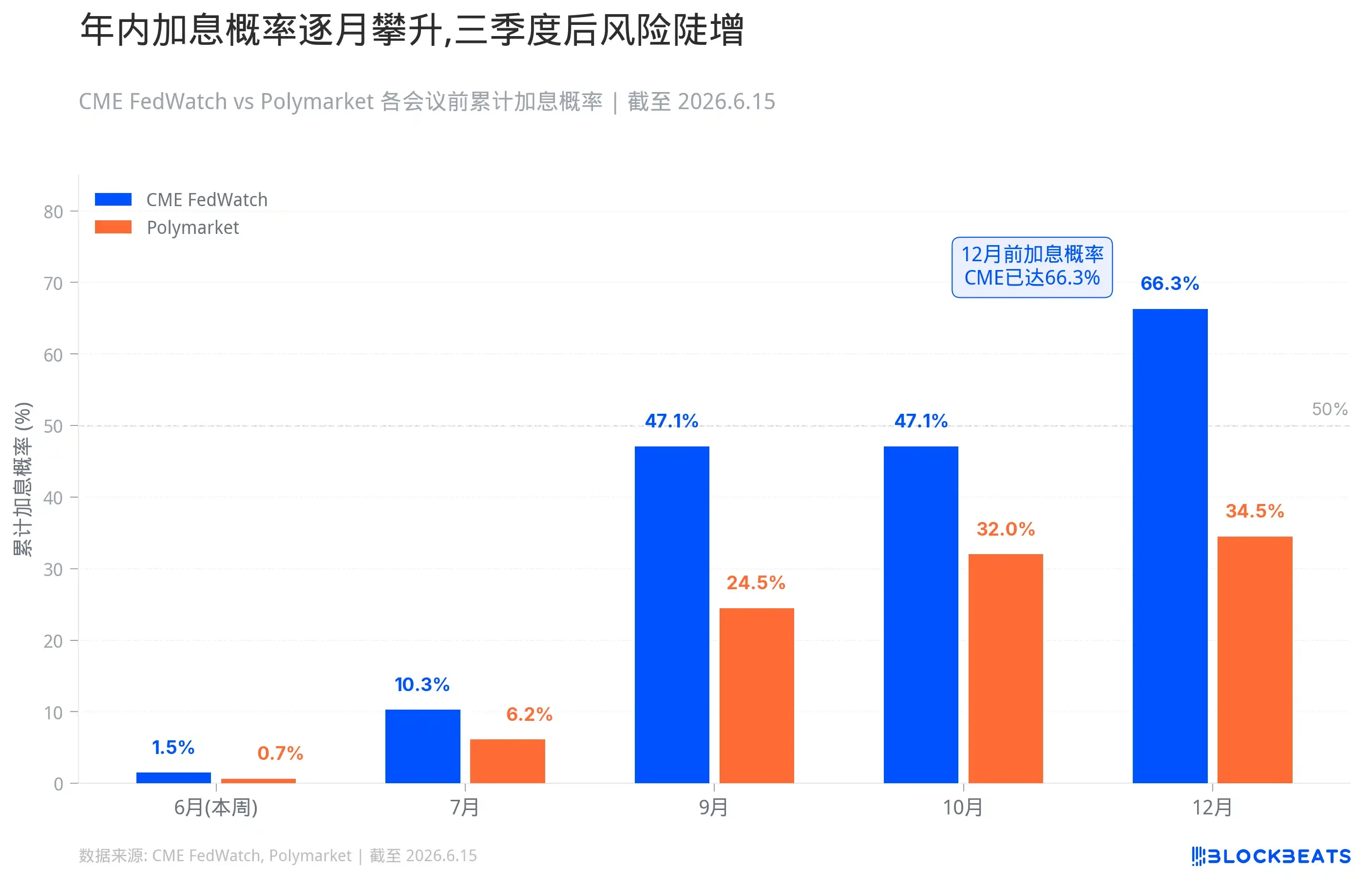

Looking at more specific probabilities and data: the probability of a rate hike before July 29 is about 10.3%, before October 28 is about 47.1%, and before December 9 is about 66.3%. Polymarket is more conservative, giving a 34.5% probability for a hike in 2026, 24.5% before September, and 32% before October. For this month, CME FedWatch gives a 98.5% probability of no change, while Polymarket gives 99.55%.

The US is likely to stay put this week, but "doing nothing" and "not tightening" are two different things.

If Wash acknowledges in his press conference that inflation risks have resurfaced, outweighing growth concerns; if the dot plot shifts the 2026 median rate from a dovish trajectory to flat or even higher; if the "easing bias" language is removed from the statement – then the market will effectively tighten financial conditions on behalf of the Fed.

The first to react will be the short end of the US Treasury curve. Yields on the 2-year and 1-year notes will directly follow the Fed's path. Once the market pivots from expecting a "cut later" to potentially a "hike later," short-end yields will rise. The US dollar will also find support, and a strong dollar itself is a form of global tightening.

Within US equities, high-valuation growth stocks and AI-associated long-duration assets are most sensitive. Higher interest rates make future cash flows less valuable, make financing more expensive, and make the market less willing to pay a premium for unproven narratives. The logic behind small-caps, micro-caps, and unprofitable tech stocks is even more fragile. These companies thrive on cheap money; once money isn't cheap, their valuations collapse first.

Should a true tail-risk scenario occur – a direct rate hike by the Fed despite the 98.5% probability of no change – the impact would be severe. Short-end rates would surge, the dollar would spike, and leveraged positions would be forced to de-risk. This isn't a prediction, but it illustrates the kind of event that, should it happen, would catch everyone off guard.

The significance of Wash's "debut" is amplified by the market. An important factor is that he could potentially change the Fed's communication strategy. Long-time Fed watchers like Timiraos have articulated the issue clearly: for Wash, symbolic adjustments like the dot plot, statement wording, and press conference cadence can be made quickly. However, truly changing the Fed's communication framework requires long-term persuasion and internal collaboration. This week's meeting could be the first step.

Across the Pacific: The "Curse" of Japan's Rate Hikes

Looking at Japan, the BOJ's policy meeting is on June 15-16. Polymarket gives a 98.3% probability of a 25bp hike. If realized, the policy rate would rise from 0.75% to 1.0%, its highest level since 1995.

The logic behind Japan being pushed to this point is straightforward. Middle Eastern conflicts are pushing up oil prices. Japan is a typical energy-importing nation, and the weak yen amplifies these import costs. Wages are rising, service prices are rising, and inflation expectations are beginning to stir. If it continues with ultra-low rates, the market will question whether the BOJ is serious about controlling inflation.

The rate hike itself is not a surprise, but a major concern remains: over the past few years, massive amounts of global capital have borrowed cheap yen to convert into dollars or other high-yield assets, buying US Treasuries, stocks, and credit, with some funds indirectly flowing into high-volatility risk assets. This entire structure was built on the premise that Japanese rates would remain low, yen financing would stay cheap, and the central bank would be slow to act. If the market believes that Japan's rate normalization is a continuous process, carry trades will become fragile, yen shorts will be squeezed, and global leveraged capital will start to contract.

The market's fear of a BOJ rate hike is not unfounded. Over the past two-plus decades, almost every time the BOJ attempted to push rates up from near zero, global markets encountered turmoil.

First, in August 2000. The BOJ raised rates from zero to 0.25%, coinciding with the peak of the US internet bubble. Within three months of the hike, the Nasdaq fell 35%. The Japanese economy itself couldn't withstand it and quickly slid back into recession, forcing the BOJ to cut rates back to zero in 2001.

Second, between 2006 and 2007. The BOJ raised rates to 0.50% in two steps – first in July 2006, then in February 2007. The timeline almost perfectly aligns with the gestation period of the US subprime mortgage crisis. In the summer of 2007, US subprime troubles began to surface, culminating in Lehman Brothers' collapse in 2008 and the global financial crisis. The BOJ was once again forced to cut rates back to zero.

Third, on July 31, 2024. The BOJ raised rates from 0% to 0.25%. The magnitude was small, but the market reaction was extreme. On August 5, the Nikkei 225 plummeted 12.4% in a single day, its worst drop since the 1987 Black Monday crash. South Korea's KOSPI triggered a circuit breaker, while the Nasdaq and S&P 500 fell 3.4% and 3% respectively. The VIX fear index surged above 65. The transmission mechanism of that crash was clear: the BOJ rate hike triggered a sharp yen appreciation, forcing a liquidation of carry trades that had borrowed yen to buy overseas assets. Selling stocks to repay yen led to a collective sell-off and a stampede. To meet margin calls, fund managers even sold "safe-haven assets" like gold and BTC. During the liquidity crisis, correlations across all assets approached 1. The editor still vividly remembers the market carnage of that day.

Therefore, even more important will be the signals from the Japanese government at tomorrow's press conference: what is the indication regarding the ultimate level of rates?

US Stocks, Treasuries, and Bitcoin: Who is Most at Risk This Week?

As mentioned earlier, global markets have generally declined during the BOJ's past three rate hike cycles.

However, the BOJ rate hike itself doesn't necessarily cause a crash; crashes typically occur when other fragile leverage points exist. For instance, 2000 and 2007 coincided with larger bubbles elsewhere. August 2024 caught the market by surprise with heavily overweighted positions. Conversely, subsequent moves where the market was prepared didn't cause major incidents.

This time, a 25bp hike is already priced in at 98.3%, leaving almost no room for surprise. Based on experiences from December 2024 and January 2025, the hike itself will likely be absorbed smoothly. However, there are two additional variables this time.

First, BOJ Governor Kazuo Ueda was hospitalized for an infected liver cyst and is expected to miss this meeting and the subsequent press conference. According to public reports, Deputy Governor Ryozo Himino will act as chair for the meeting, while Deputy Governor Shinichi Uchida will host the post-meeting press conference. This arrangement is unlikely to change the direction of the rate hike. However, the market is less familiar with Uchida's communication style compared to Ueda's, potentially amplifying volatility in interpreting his language. A statement like "future decisions will depend on data" versus "there is still room for rate normalization" may seem similar but sends entirely different signals to traders.

Second, the US is holding its meeting the same week. The BOJ decision and the FOMC meeting are only one day apart. If the BOJ hike is followed by a calm market reaction, but Wash sounds hawkish at his press conference the next day, two layers of pressure will combine. Conversely, if the market is already tense after the BOJ decision and Wash pours fuel on the fire, short-term sentiment could overreact. Two major central banks announcing back-to-back decisions inherently amplifies volatility.

Let's analyze asset by asset:

US Treasuries will likely be the first to react this week. Short-end yields will directly follow the Fed's path, with the 2-year and 1-year notes being most sensitive. A hawkish press conference from Wash and an upwardly revised dot plot would send short-end yields higher, reflecting a market repricing towards "later cuts" or even "a hike this year." The long end is more complex; the 10-year yield may not surge in tandem. If the market begins to worry that high rates will damage the economy, the yield curve could flatten further or even invert more deeply. In Japan, if Uchida hints at further rate hikes, JGB yields would also rise. If Japan, holding $1.13 trillion in UST, shows marginal signs of adjusting its holdings, it could also impact UST supply-demand dynamics.

The US Dollar is likely to find support. A hawkish Fed tone boosts expectations for USD-denominated asset yields, strengthening the DXY. A BOJ hike is theoretically positive for the yen and negative for the dollar, but the actual outcome depends on language: if the BOJ hikes but immediately signals dovishness, the yen could fall and the dollar index could rise. With two central banks meeting the same week, the relative movement of the dollar and yen will be highly sensitive, likely increasing FX market volatility. Asian and emerging market currencies will face pressure. A strong dollar itself represents global tightening, draining offshore USD liquidity.

US Equities will see significant divergence. High-valuation growth stocks, long-duration AI assets, small-caps, micro-caps, and unprofitable tech stocks are most vulnerable. Higher rates make distant cash flows less valuable, make financing more expensive, and make the market less willing to pay for unproven stories. The Russell 2000 and companies reliant on cheap money are first in line. Bank stocks have a complex reaction: short-term spreads might benefit, but if the curve continues to invert and credit risks rise, it's not necessarily positive. Defensive stocks are relatively resilient, but "bond-like assets" such as utilities and REITs will also face valuation compression from higher rates. The S&P 500 closed near 7,382 on Friday, with the Nikkei 225 at 66,078. If both central banks lean hawkish this week, US and Japanese equities will face pressure, especially indices with heavy tech weightings.

Japanese Equities are in a unique position. A BOJ rate hike is bad news for Japanese exporters as a stronger yen erodes overseas profits. However, if the pace and magnitude are in line with expectations, Japanese stocks won't necessarily crash, as evidenced by the experiences of December 2024 and January 2025. The real risk lies in post-meeting communication. If Uchida hints at continued normalization, the Nikkei might fall first and assess later.

Gold will be pulled between two forces. Rising real rates and a stronger dollar are typically bearish for gold. However, if the reason behind the rate hike is an energy shock, geopolitical risks, and runaway inflation, safe-haven demand will support the price. Gold will likely trade in a high range this week, direction depending on what the market fears more: rising rates or inflation spinning out of control.

Crude Oil is more dependent on supply-demand dynamics and geopolitics. Conflicts in Iran are still brewing. If rate hikes are driven by oil-induced inflation, oil prices might not fall immediately. However, if the market begins pricing in expectations of slowing demand, industrial metals and crude oil will face pressure later.

Credit and Real Estate are slower-moving variables, but the direction is clear. High-yield credit spreads will widen, financing costs will rise, and assets sensitive to commercial real estate, REITs, and mortgages will be under pressure. Emerging markets with high USD-denominated debt will also suffer, facing increased capital outflows.

The Crypto Market will also be under pressure in this macro environment. BTC is currently around $65,000, having fallen from ~$72,000 in early June to ~$61,500 after the CPI data release before recovering slightly in recent days. This level is inherently unstable. When BTC broke below $62,000 on June 5, on-chain long liquidations exceeded $1.5 billion, and Bitcoin spot ETFs saw net outflows of $2.7 billion in a single week. Although the price has recovered somewhat, the positioning structure is unhealthy. BTC retains some macro asset characteristics; it may not crash alongside rising rates, but it will struggle to rally independently. ETH, SOL, altcoins, memecoins, and small-cap tokens are more fragile. These assets thrive on liquidity overflow and risk appetite. Once the market starts comparing the relative attractiveness of cash, short-term bonds, and money market fund yields, these high-beta assets are the first to be cut. Contract market funding rates have fallen, on-chain risk appetite has cooled – signs already seen in early June.