IOSG: SpaceX’s IPO Day Marks the First Real-World Test of Three Perpetual Mechanisms

- Core Thesis: Pre-IPO perpetual contracts, through on-chain price discovery mechanisms, offer retail investors directional investment exposure to private companies like SpaceX prior to their public listing, while also filling the gap in traditional after-hours trading. However, they carry significant unresolved risks in handling corporate actions such as stock splits.

- Key Elements:

- Pre-IPO perpetuals solve the pricing challenge of no spot price reference. By utilizing internal oracles and price ranges, they allow the market to discover prices autonomously in the absence of external benchmarks, and kept the prediction error for Cerebras’ opening price within 1.3%.

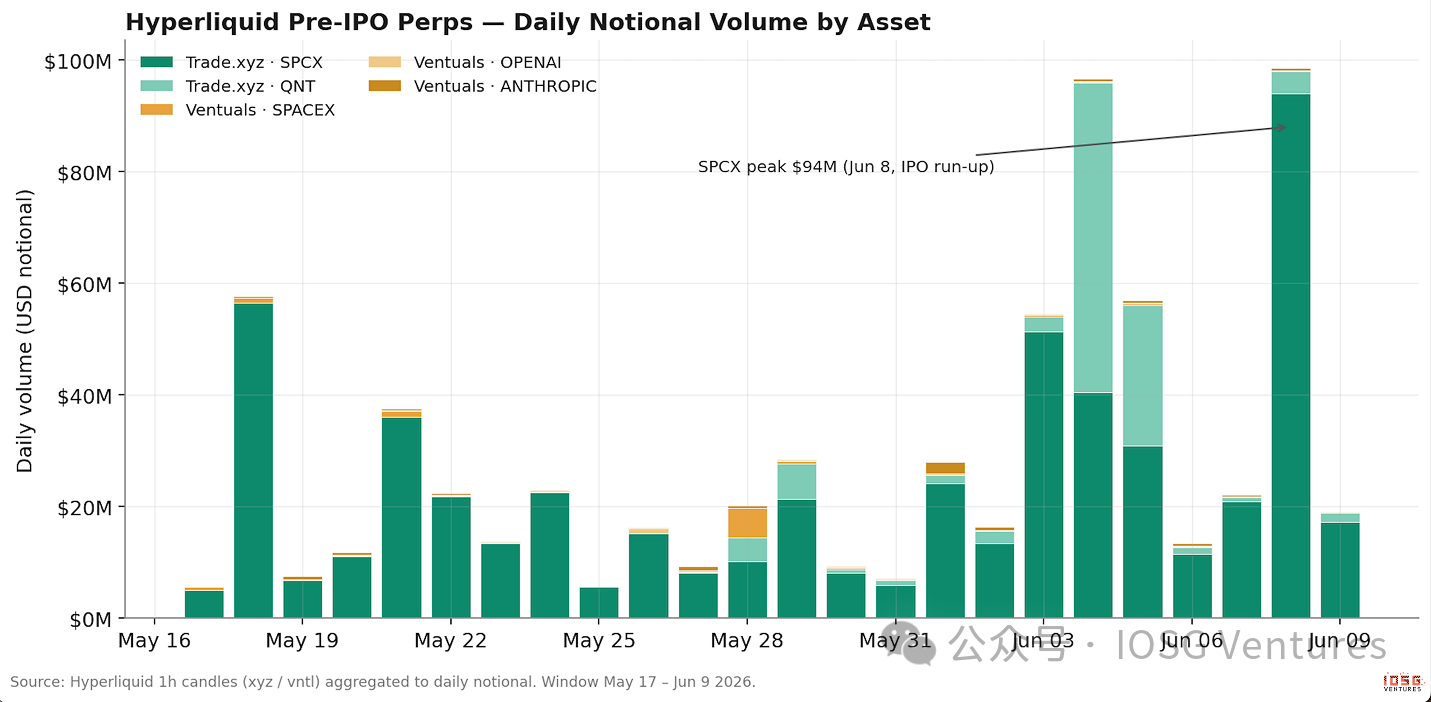

- This market currently accounts for only about 1% of traditional finance perpetual contract volume, indicating vast potential. The leading project, Trade.xyz, commands approximately 96.5% of on-chain volume, driven by its near-zero funding rates and the timing of IPOs.

- The key differentiator in volume distribution is the cost of holding positions. Trade.xyz's near-zero fees enable long-term market holding, whereas competitor Ventuals' high fees (45% annualized) result in a cumulative cost roughly 350 times higher.

- Handling corporate actions is the biggest vulnerability. Trade.xyz lacks a rebase mechanism for splits, while Ventuals, using a single data source, once saw its market flash-crash by 45% due to outdated split data, highlighting the risk concentrated in the lack of a standardized on-chain corporate event processing layer.

Original Author: Mario Chow

Original Source: IOSG Ventures

TL;DR

- Why do Pre-IPO perpetuals matter? They pry open two doors that were previously locked to almost everyone: first, taking a directional bet on a private company like SpaceX or OpenAI *before* its IPO; second, getting a real-time price during nights, weekends, and pre-market hours when stock markets are closed but news is still moving prices. Now, anyone with a wallet can place this bet – continuously, permissionlessly, and just in time for the biggest wave of IPOs in history.

- Without a public spot price, how do you price an asset? This is the core challenge for the entire category. With no external price to copy (which can be stale for months), exchanges are forced to create a price using their own order book alone, and move it only when real money is willing to trade at a different price: slowly, and expensively enough to make manipulation prohibitive. trade.xyz uses an internal oracle with a price collar, while Ventuals relies partly on primary market data. Surprisingly, this works: the perpetual predicted Cerebras' opening price within 1.3%, and even priced crude oil during a weekend when all traditional venues went dark.

- What worked in the SpaceX case? trade.xyz captured the on-chain market (~96.5% of volume), not because of a smarter oracle, but because near-zero funding fees made holding the position nearly costless. It launched *riding* the IPO catalyst, denominated in per-share terms, and was plugged into cross-exchange arbitrage. On listing day (June 12), the transition from synthetic perpetual to spot tracking was clean: no oracle gap, no liquidation cascade. During the IPO day, the perpetual tracked Nasdaq's real-time price within 1% (approx. $152 vs. a matching price of $150); its pre-market mark price also sat right on Nasdaq's own indicative opening price (~$175), before eventually settling at the lower matching price of $150.

- What unresolved risks remain? This category excels at handling prices, but is still primitive at handling events. Corporate actions, especially post-conversion stock splits, have no pipeline on-chain: trade.xyz hasn't published any rebase mechanism, while Ventuals outsources this to a single data vendor, which already failed once (an outdated split data point caused its market to flash crash 45%). The bottleneck isn't price discovery; it's the boring "corporate action" processing layer. Traditional markets took a century to standardize it; no one has rebuilt it on-chain yet. Whoever can reliably deliver it will close the last gap between these markets and the ones they aim to replace.

Background: Crypto Just Pried Open Two Locked Doors

Pre-IPO perpetuals sit at the intersection of two things that, until recently, were almost universally locked. Crypto's rail system has now pried both doors open.

The First Door: Pre-IPO Exposure, Finally Open to Retail

Shares of SpaceX or OpenAI before their IPOs were only accessible to qualified investors, VCs, and a few secondary desks, with opaque valuations, repriced only at each funding round. Pre-IPO perpetuals simply tear down this wall. With a wallet, you can bet on the direction of a private company's valuation, anytime, permissionlessly, without touching any shares, quotas, or voting rights. The timing is exceptionally fortuitous, coinciding with the biggest wave of IPOs in history. SpaceX listed on Nasdaq on June 12 at an estimated ~$1.77T valuation, with OpenAI and Anthropic expected to follow. For the first time, retail can position themselves before the opening bell, rather than chasing the stock post-IPO.

The Second Door: After-Hours Trading, Now Captured by Crypto

Traditional exchanges still operate on "banker's hours." Stocks and futures shut down at night, on weekends, and during holidays. When news breaks after hours, there's nowhere to hedge the real risk. Crypto never closes. This time gap cedes the entire after-hours window to them, and most price discovery happens on Hyperliquid.

The key premise of this report is: the after-hours quote isn't a guess; it often lands right where the real market reopens. One Saturday, Middle East conflict pushed oil prices higher. Only Hyperliquid was trading. When CME crude oil futures reopened Sunday evening, the opening price was exactly what the Hyperliquid perpetual had already found. TD Securities estimates this platform absorbed ~80% of that recent oil price swing before traditional exchanges even opened. The same holds for stocks: trade.xyz's Cerebras perpetual tracked Nasdaq's final opening price within ~1.3%. During after-hours, the perpetual contract *is* the market.

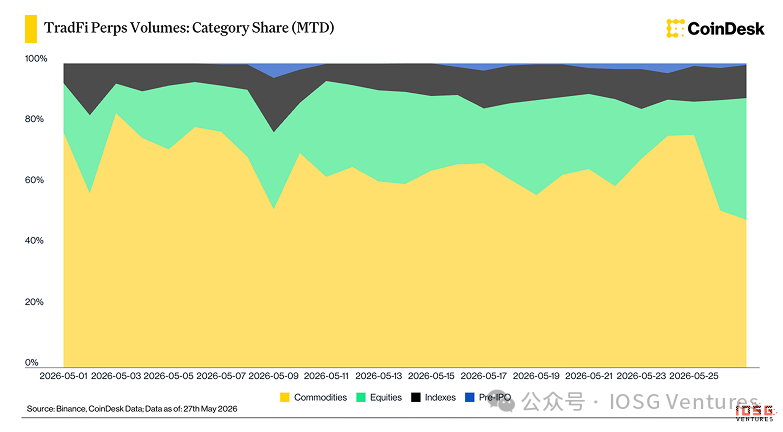

How Early Are We? About ~1% of TradFi Perpetual Volume

CoinDesk data shows how nascent this market is. On Binance and similar platforms, TradFi perpetuals are dominated by commodities and stock indices. Pre-IPO is just the thinnest sliver at the top of the stack chart, representing a little over 1% of total TradFi perpetual volume since its launch around May 21.

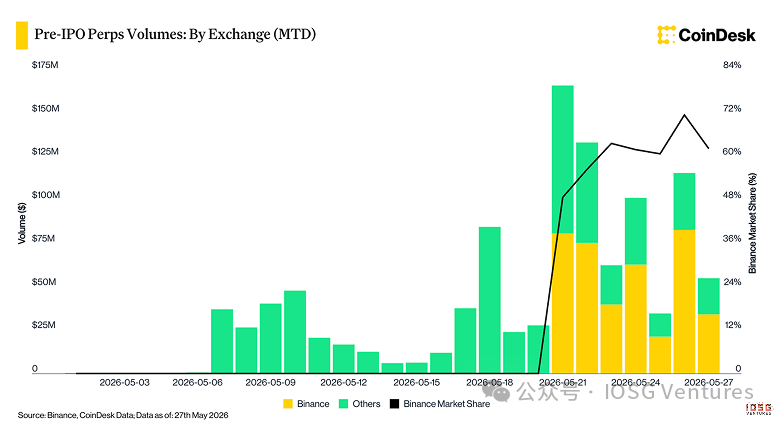

On Binance, Pre-IPO volume is also highly concentrated in a few names: SpaceX accounts for ~79%, OpenAI 11%, and Anthropic 9%. This category launched around May 20, and Binance quickly captured over 60% of the share. Pre-IPO on CEXs is embryonic, with SpaceX as the protagonist. The really interesting activity is on-chain.

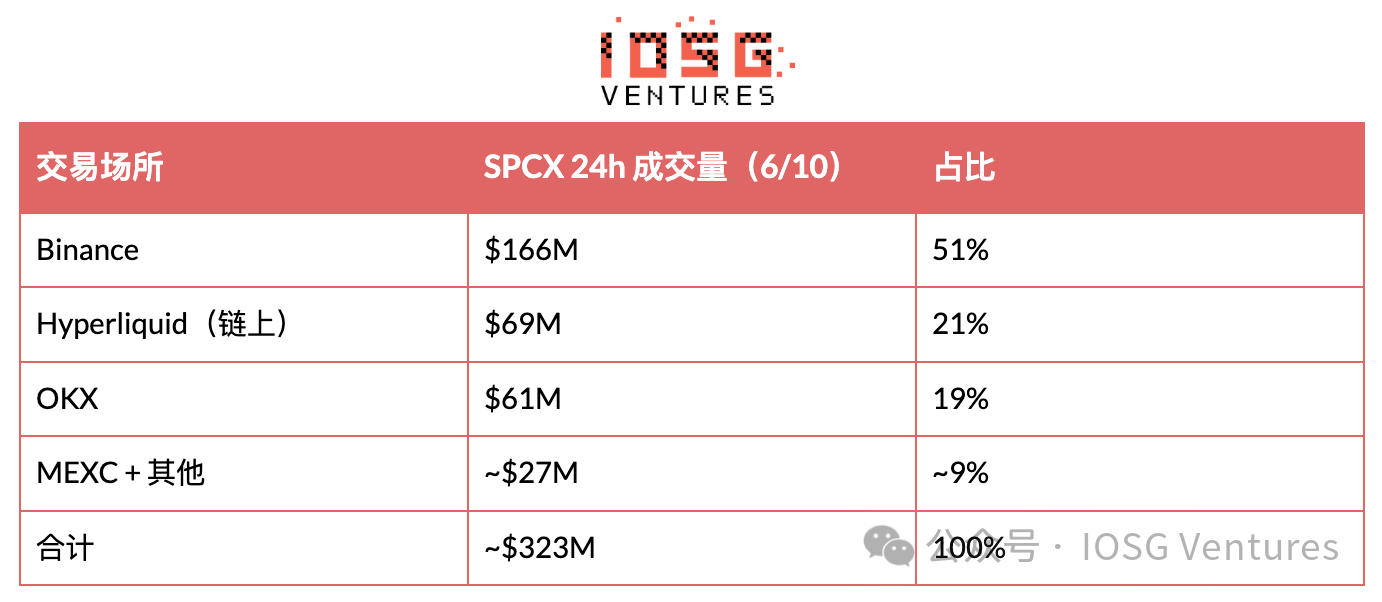

The SPCX Landscape Across Venues: Binance Leads, Hyperliquid Holds On-Chain Home Turf

Market Snapshot: June 10

Focus on SpaceX itself. It *is* the Pre-IPO market right now. In this June 10 snapshot, total 24-hour volume for the SPCX perpetual across all venues was ~$323M. Binance led with $166M (51%), followed by Hyperliquid with $69M (21%), OKX with $61M (19%), and then MEXC and a handful of smaller venues.

On-Chain Landscape: A Market with Only One Builder

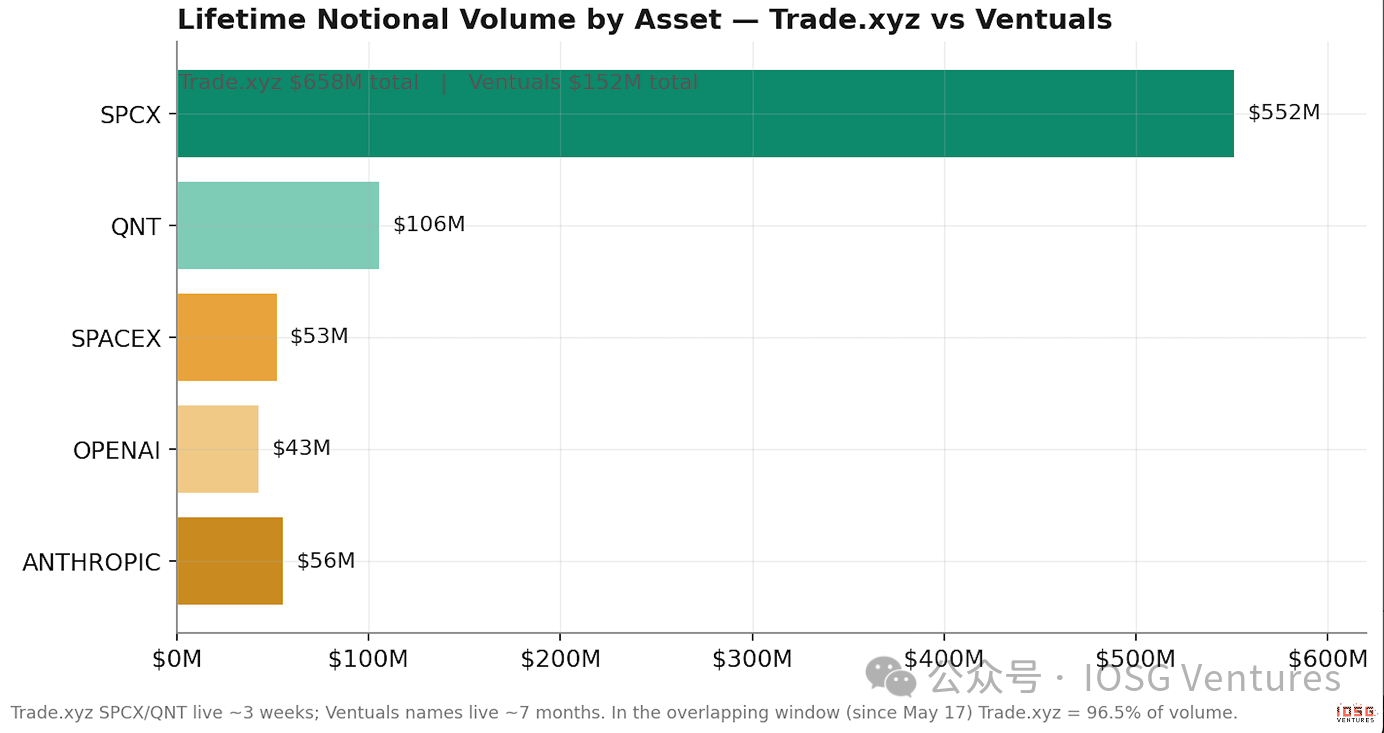

Data Comparison: Trade.xyz vs. Ventuals: 96.5% vs. 3.5%

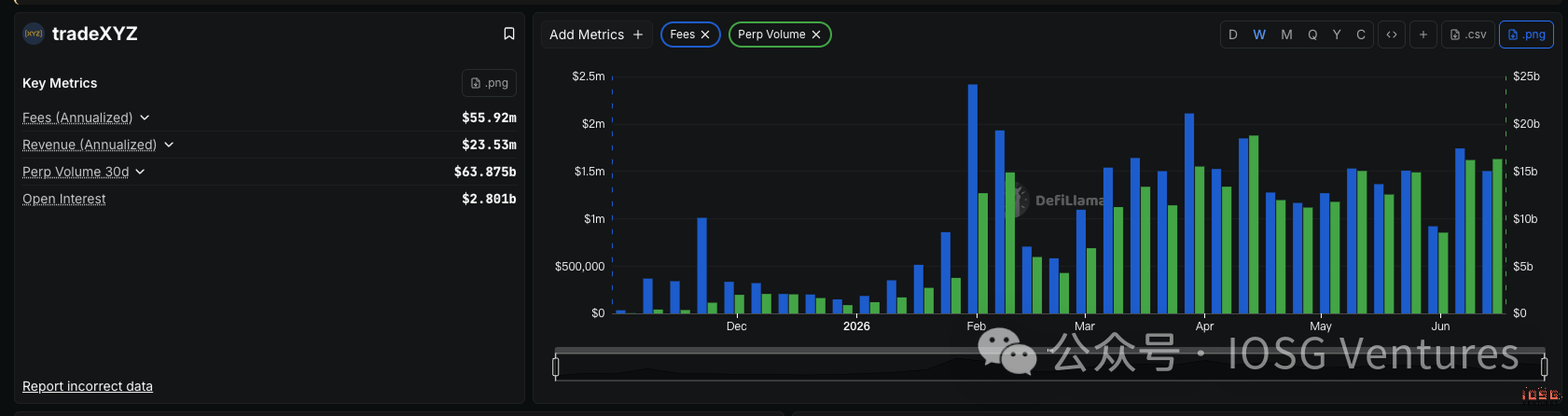

Trade.xyz has accumulated ~$658M in volume, with SPCX contributing $552M and its second asset QNT adding $106M, all within about three weeks. Ventuals has accumulated ~$152M, more evenly distributed across SPACEX ($53M), OPENAI ($43M), and ANTHROPIC ($56M), spread over about seven months.

Placing them on the same timeline reveals the stark difference. During the overlapping window since SPCX launched, trade.xyz accounted for ~96.5% of on-chain Pre-IPO volume. This aligns with third-party trackers' estimates that it holds ~95% of the Hyperliquid Pre-IPO basket. Ventuals lists more assets, including the only currently online Anthropic and OpenAI contracts, but captures only a tiny fraction of the flow. Listing isn't the moat; liquidity is.

HIP-3: The Platform Layer Underpinning All This

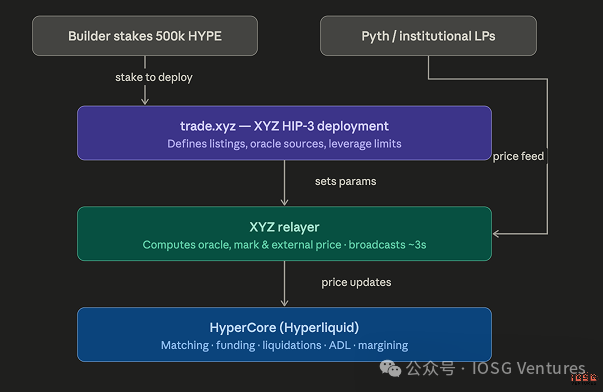

HIP-3 was an upgrade for Hyperliquid. It transformed a single perpetual venue into a platform for builders to deploy their own perpetual DEXs. Any team staking 500,000 HYPE tokens can deploy their own perpetual market on HyperCore, Hyperliquid's matching layer. Builders control listing, oracles, leverage limits, and contract parameters; HyperCore controls execution, funding, liquidation, and margin. Trade.xyz is a HIP-3 deployment focused on traditional assets: turning stocks, indices, and commodities into 24/7 perpetual contracts, margined and settled in USDC, using isolated margin only.

How Trade.xyz Prices a Market Without External Truth

Let's start with the problem, because only by feeling the problem first does the design make sense. A normal perpetual copies a live spot price from an exchange. A Pre-IPO perpetual has no spot price to copy – and might not have one for months. So the venue is forced to manufacture a credible price using the only tool at hand – its own order book – and make it expensive enough not to be pushed around. Everything in this section answers the same question: How do you price an asset when it doesn't have a price yet?

Two Oracle Mechanisms for After-Hours Stock Perpetuals

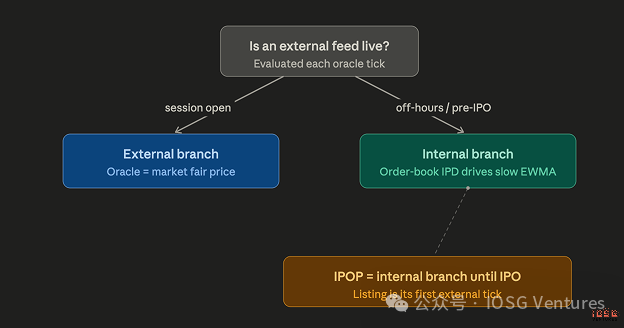

To understand Pre-IPO perpetuals, first understand after-hours stock perpetuals. Crypto perpetuals have real-time external prices 24/7; stocks do not. AAPL only has a real market price during US equity trading hours. So the oracle feeding the funding rate and mark price needs two mechanisms: one when external data is available, another when it's not. When the external market is open, a relayer directly feeds an institutional fair price (sources include Pyth) as the oracle. When the market is closed, the oracle must rely on the perpetual's own order book – this is the truly sophisticated part of the design.

Internal Oracle: Three Core Ideas

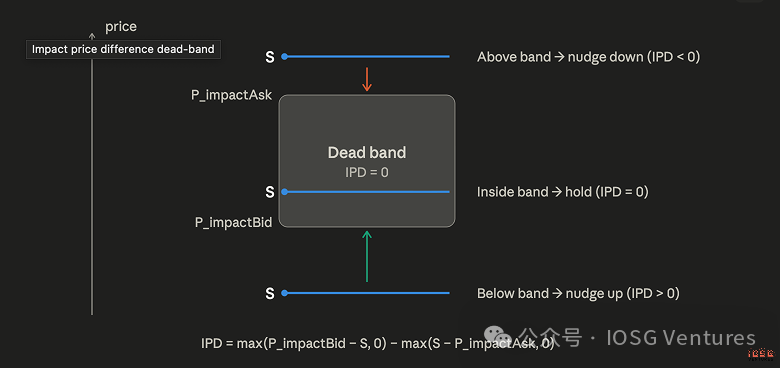

Look at where the executable order book actually sits.

The relayer calculates the average execution price for a fixed $1,000 order pushed into each side of the order book, yielding an executable bid price and an executable ask price. If the current oracle price falls within this range, nothing happens – order book and oracle agree, the oracle stays. Only when the oracle price falls outside the range – meaning real order depth is willing to trade at a deviating price – does the oracle get pushed towards the order book. Heavy buying lifts it, heavy selling pushes it down; noise within the range is completely ignored. To move this oracle, you must commit real liquidity, not just book a few trades.

The oracle never jumps.

It converges slowly toward the order book with a thirty-minute time constant, and a hard cap ensures a single update can only close about 9.5% of the remaining distance, regardless of time elapsed since the last update. Halts and irregular updates cannot cause gap moves.

The mark price is the median.

The mark price driving margin and liquidation is the median of three candidates: the oracle itself, the oracle plus a short-term moving average of the perpetual's basis, and an order book snapshot (best bid, best ask, last traded price). The median structure means that fast variables alone can never drag the mark price too far from the slow oracle. Hourly funding then pushes the market back toward the oracle, with standard multipliers and caps ensuring any single hour's payment is small.

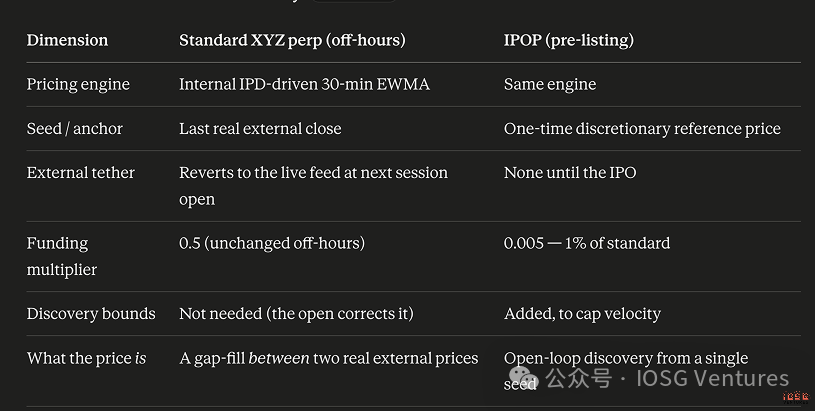

Pre-IPO Perpetuals: Same Engine, Three Modifications

IPOP (Pre-IPO Perpetual) is essentially an after-hours stock perpetual that can never rely on a "Friday close" price. Before the IPO, there is no external price, so the market must run its internal pricing mechanism continuously, sometimes for months. Trade.xyz made three modifications for this, each revealing the nature of the problem.

- The funding rate was slashed to 1% of the standard rate. Weekend perpetuals can drift for up to two days but get corrected Monday open, so standard funding is tolerable. An IPOP might trade for over sixty days without any anchor, and markets tend to settle into persistent premiums or discounts reflecting pure sentiment. At standard rates, anyone holding a position against the prevailing sentiment would be bled dry by funding long before the IPO arrives. Reducing the multiplier to nearly zero is what makes this contract actually holdable. Our view: more than any oracle ingenuity, this single parameter makes trade.xyz's product tradeable, as the funding data later in this report confirms.

- Initial seed price. Weekend markets initialize at the last real external price. An IPOP has no history, so trade.xyz sets an initial reference price. It's not a prediction, just a mathematical starting point. For SPCX (launched late UTC on May 17), the reference price was set at $150 per share: the midpoint of SpaceX's publicly reported ~$1.75T–$2T target valuation, divided by a hypothetical fully diluted share count of 11.87 billion.

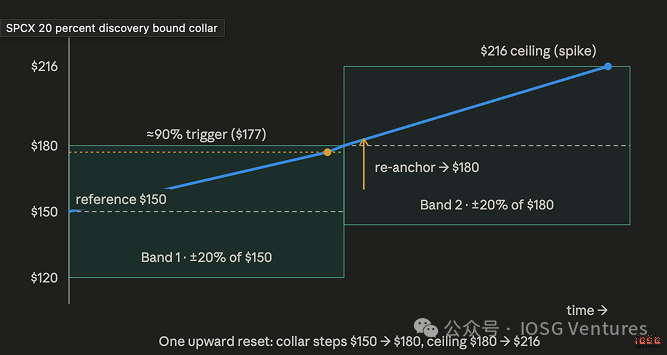

- Discovery bound. A price collar around the reference price that the mark price cannot breach, with a rule that positions whose liquidation price falls outside the current collar will not be liquidated while the collar is active.

For the 5x leverage SPCX, the collar width is ±20%. A static collar would either freeze the price or be useless, so this collar is stair-stepped: when the slow oracle climbs to 90% of the upper band, the reference price re-anchors to that band, and a new 20% collar opens around it.

SPCX has seven steps in each direction. Compounding these steps, the contract's hard lifetime range, starting from the $150 seed price, is approximately $25 to $645 per share.

How Much It Costs to Manipulate This Market: Expensive, Obvious, Slow

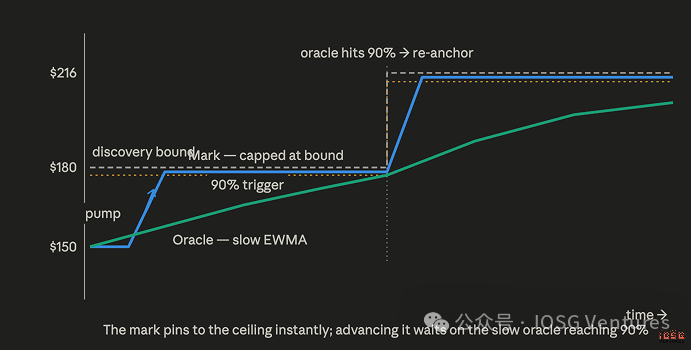

This division of labor is critical for anyone trying to manipulate. The mark price reacts quickly but has a hard cap; a single pump can almost instantly hit the ceiling and then freeze there.

The oracle is a slow thirty-minute average; it's the gatekeeper. Only when the oracle touches the 90% trigger line does the step move up. To push the price up one step, an attacker must hold the entire order book elevated against arbitrageurs for nearly an hour, then repeat for the next step. Expensive, obvious, slow. That's the design intent, and so far, it has held steady.

The Two Builders: Trade.xyz vs. Ventuals

Ventuals: Partially Trusting External Data

Pre-IPO perpetuals on Hyperliquid come from two HIP-3 builders that approach the same problem from opposite directions: trade.xyz trusts its own order book; Ventuals partially trusts external data. Ventuals prices valuations, not share prices: a SPACEX price of 1,989 implies an implied company valuation of $1.989T. Its oracle is a weighted blend: one-third from external valuation estimates by Notice.co, and two-thirds from a two-hour moving average of Ventuals' own mark price.

Notice aggregates secondary trades, indicative bid/ask quotes, financing announcements, mutual fund valuations, 409A valuations, and comparable public company data, polling at least every minute. The deliberately set one-third weight is Ventuals' answer to the "IPO spike problem": anchor to primary market reality while giving the market mathematical room to price upwards. Also worth noting: two-thirds of this oracle is Ventuals' own market – this design is more self-referential than its marketing suggests.

Its anti-manipulation mechanism is built on the price path, not a stair-stepped collar. Orders cannot deviate more than 20% from the oracle, enforced by the matching engine. The mark price updates every three seconds, with a maximum move of 1% per update. If the short-term impact price deviates more than 2% from its one-minute average, the mark price update coefficient immediately drops to zero, so sudden volatility must persist for the mark price to follow. Funding is dynamic: around 15% annualized when the market is close to the oracle, rising exponentially as deviation increases, approaching nearly 1% per hour near the collar edge.

The endgame design is also entirely different. When a company lists, Ventuals settles the market and halts: funding goes