苹果 AI 到底行不行?WWDC26 最值得关注的一轮美股映射链

- 核心观点:苹果WWDC 2026的关键不在于是否发布AI,而在于能否将Apple Intelligence从软件更新转化为系统级AI入口,从而驱动新一轮硬件换机周期和开发者生态重构,这可能是短期预期差交易的核心来源。

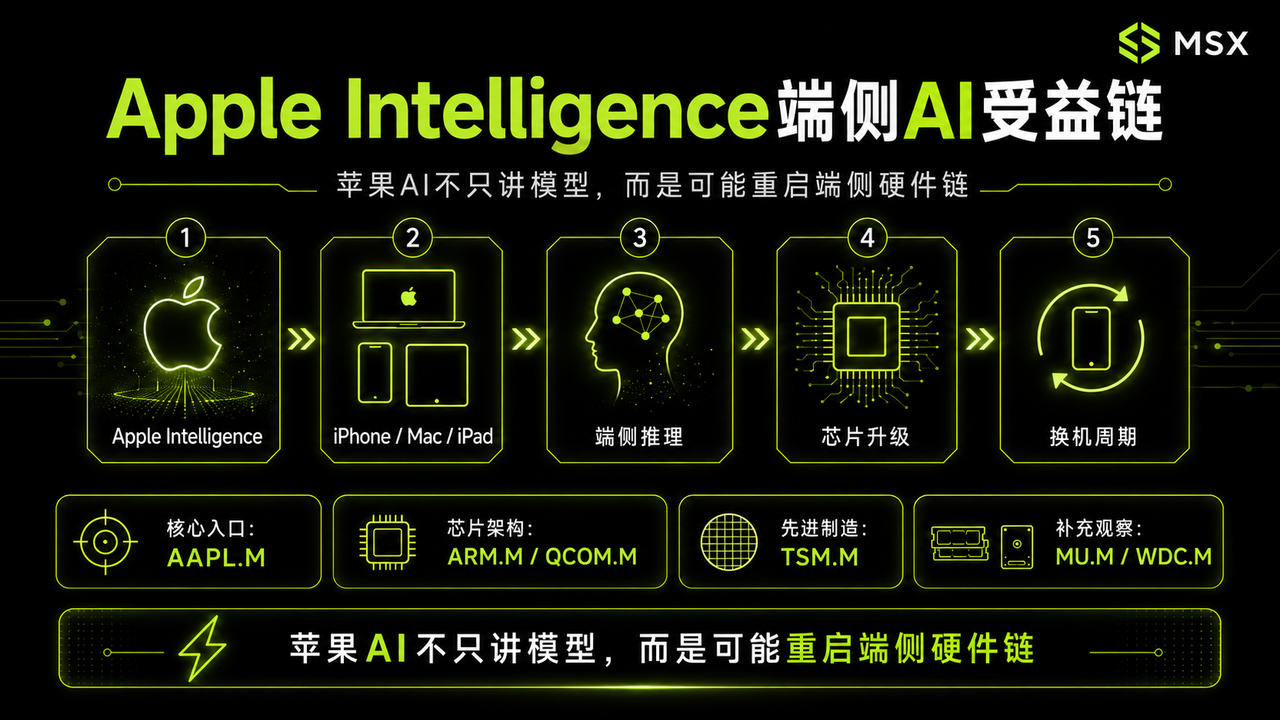

- 关键要素:

- WWDC是预期差事件:历史数据显示WWDC并非稳定上涨事件(2022年跌5.7%,2024年涨7.9%),股价反应取决于AI、Siri和开发者生态是否超预期。

- Siri升级成核心观:如果Siri从“语音助手”升级为能够读取上下文并跨应用执行任务的系统级AI Agent,将是苹果AI重估的关键。

- 端侧AI驱动换机逻辑:Apple Intelligence若需更强芯片和本地推理能力,将绑定新硬件,推动旧设备向新设备迁移,形成换机周期财富效应。

- 生态开放是更大外溢机会:若苹果将AI能力开放给第三方开发者,Apple Intelligence将从苹果自身故事扩展为整个App Store生态的故事。

- 概念股分层映射:影响从核心入口(AAPL.M)到端侧AI链(ARM/TSM/QCOM)、模型云合作(GOOGL/MSFT/AMZN)、开发者工具(MSFT/TEAM)及App生态(ADBE/INTU)五层。

In the early hours of June 9, Beijing time, Apple's WWDC26 officially presented the answer the market had been waiting for:

Can Apple AI finally catch up?

As is well known, over the past two years, the strongest players in the AI narrative have been tech giants like NVIDIA, Google, Microsoft, and Meta, as well as large model companies such as OpenAI and Anthropic. In contrast, although Apple possesses the world's strongest hardware entry points—including the iPhone, iPad, Mac, Apple Watch, and Vision Pro—along with a complete App Store ecosystem, the rollout progress of Apple Intelligence and Siri has consistently fallen short of expectations.

Therefore, the core focus of this WWDC is no longer just whether Apple will talk about AI, but rather whether it can convince the market that Apple Intelligence will truly become an AI entry point capable of reigniting the upgrade cycle, developer ecosystem, and application ecosystem.

1. WWDC Doesn't Necessarily Boost Apple's Stock, But It's Most Likely to Create Expectation Gaps

Let's first look at historical performance.

In recent years, WWDC has not been an event that guarantees an Apple stock price increase. Based on rough calculations from the Friday close before WWDC to the Friday close of WWDC week:

- In WWDC week 2022, AAPL fell approximately 5.7%;

- In the week of the Vision Pro launch in 2023, AAPL was roughly flat;

- On the day of the Apple Intelligence launch in 2024, AAPL initially fell about 1.9%, but as the market subsequently re-evaluated the logic of "on-device AI + upgrade cycle," it eventually rose about 7.9% for the week;

- After WWDC 2025, the market was dissatisfied with Siri delays and AI progress, leading to a weekly decline of about 2.4%;

Thus, WWDC itself is not a consistently positive event for the stock, but it frequently creates "expectation gap trades." From this perspective, if this year's event only features routine system updates, the stock price reaction will likely be muted. However, if AI, Siri, on-device capabilities, and the developer ecosystem exceed expectations, it could generate short-term wealth effects.

This is also why this year's WWDC deserves early attention.

2. Apple AI's Key Battleground: Not the Model, but the Entry Point and Upgrade Cycle

It's worth noting that many companies approach AI by first building a model and then seeking user entry points. Apple is the opposite; it already possesses the entry point, it just needs to enhance its AI capabilities.

This is because Apple's true advantage lies not in parameter count but in its system-level entry point. It can embed AI into iOS, macOS, iPadOS, watchOS, and visionOS, allowing AI to directly integrate into Mail, Photos, Calendar, Messages, Notes, the App Store, and third-party applications.

This is why Siri is so crucial.

If Siri remains merely a tool for "checking the weather" or "setting alarms," it will struggle to underpin a revaluation of Apple AI. But if Siri can read user context, invoke different apps, and complete cross-application tasks, it will evolve from a simple voice assistant into the AI Agent entry point within the Apple ecosystem.

Therefore, the primary focus of WWDC is whether Siri can be upgraded from a "voice assistant" to a "system-level AI entry point."

The most direct target corresponding to this narrative is, of course, AAPL.M. If Apple continues to rely on external models or cloud-based inference, GOOGL.M, MSFT.M, and AMZN.M might also be used by the market as proxy plays.

However, the true wealth effect of Apple AI may not lie solely at the software level but at the hardware level. If new Apple Intelligence features require more powerful chips, larger memory, and better on-device inference capabilities, it will transform the narrative from a software update into a hardware upgrade cycle.

The advantages of on-device AI are clear: it allows many tasks to be processed without full reliance on the cloud, leading to faster response times; it aligns better with Apple's long-standing emphasis on privacy and security; and, crucially, it is naturally tied to new hardware, incentivizing users to upgrade from older iPhones and Macs to newer devices.

After Apple announced Apple Intelligence in 2024, a key reason the market repriced the stock after brief hesitation was the emerging thought process: if AI features are tied to new devices, could this trigger a new upgrade cycle?

This is another critical source of potential wealth effects from this year's WWDC.

For the on-device AI supply chain, key stocks to watch include AAPL.M, ARM.M, TSM.M, and QCOM.M. Among these, AAPL.M represents the terminal entry point; ARM.M embodies low-power architecture; TSM.M is a key foundry partner for Apple's chips; and QCOM.M, despite its competitive and collaborative relationship with Apple, will also be used by the market for comparison within the on-device AI and mobile chip ecosystem.

3. The Real Spillover Opportunity: From the Chip Supply Chain to the App Ecosystem

It's important to note that WWDC is not just a single day or just Apple's own product launch; it is fundamentally a developer conference.

If Apple merely adds a few AI features to its systems, that's primarily a story for AAPL itself. However, if Apple opens its AI capabilities to developers, allowing third-party apps to access on-device models, system-level Agent capabilities, privacy computing frameworks, and new developer tools, then Apple Intelligence will evolve from an Apple story into an ecosystem story.

This narrative is very important.

Because Apple's true moat is not a single AI function but the App Store ecosystem. If developers can integrate Apple Intelligence into creative, productivity, document, e-commerce, financial, and business applications, it could give rise to a wave of new AI application scenarios.

From an investment mapping perspective, Apple Intelligence concept stocks can be categorized into five layers.

The first layer is the core entry point, AAPL.M. If Siri and Apple Intelligence exceed expectations, Apple itself will be the most direct beneficiary. Apple controls both the hardware entry point and system permissions for app distribution. Once AI capabilities are truly embedded in the system, AAPL.M will be the first to undergo revaluation.

The second layer is the on-device AI supply chain, including stocks like ARM.M, TSM.M, and QCOM.M. If Apple moves more AI capabilities to run on local devices, low-power chip architecture, advanced manufacturing processes, and mobile AI capabilities will all come back into focus.

The third layer involves model and cloud partnerships, for instance, GOOGL.M, MSFT.M, and AMZN.M. If Apple continues to enhance Apple Intelligence through external models or cloud capabilities, these giants will also be used as proxy plays by the market. Especially against the backdrop of Apple's insistence on privacy, security, and on-device-cloud collaboration, identifying the underlying model or cloud inference partner will influence the market's short-term perception of these related companies.

The fourth layer comprises developer tools, such as MSFT.M, TEAM.M, DDOG.M, and GTLB.M. If WWDC emphasizes AI coding, Xcode upgrades, developer APIs, and application building efficiency, the AI development ecosystem could be stimulated. For the market, this narrative doesn't trade on direct revenue generated by Apple for these companies, but on the theme of "continuously lowering the barrier for AI application development."

The fifth layer is the app ecosystem, including stocks like ADBE.M, DOCU.M, INTU.M, and SHOP.M. These companies are not direct beneficiaries of Apple AI. However, if system-level AI capabilities are opened up, applications in creative, document, financial, and e-commerce sectors will be the easiest to integrate new features. They represent potential mapping targets for the spillover effects of Apple Intelligence into the application layer.

Of course, while this narrative offers potential, it also carries risks.

First, Apple AI could be "all bark and no bite." If it's just routine system updates without substantial Siri upgrades or the opening of developer capabilities, the market will likely be disappointed.

Second, spillover targets may not immediately realize revenue. For example, ADBE.M, SHOP.M, DOCU.M, and INTU.M, even if they could integrate Apple AI capabilities in the future, may not quickly see the impact in their financial reports.

Third, Apple's AI catch-up might primarily benefit AAPL.M itself. If new capabilities are mainly confined within Apple's closed system, the gains for external concept stocks will be relatively weak.

Fourth, the valuation recovery of AAPL.M ultimately depends on iPhone demand. AI can tell a compelling story, but hardware sales, services revenue, and profit margins remain the core drivers of long-term pricing.

Therefore, Apple Intelligence concept stocks can be traded based on expectations, but they cannot be simply viewed as a guaranteed "WWDC rally."

Final Thoughts

Before WWDC, the market trades on expectations; after WWDC, the market will begin to verify whether Apple's AI has truly brought about substantive changes.

If Apple merely adds a few AI functions, it might just be an ordinary software update.

But if Siri becomes a system-level AI entry point, on-device AI is tied to new hardware, and developer tools unlock new capabilities, then Apple Intelligence becomes more than just Apple's own story. It could potentially drive a new mapping chain for U.S. stocks.

It all depends on whether Apple can embed AI into the world's largest consumer electronics ecosystem.