比特币四年周期:规律不变,玩法已变

- 核心观点:比特币的4年周期并未消亡,2025年顶部如期而至,但传统链上指标因机构主导市场而集体失效,散户资金在涌入比特币前已被Memecoin和高FDV代币耗尽。

- 关键要素:

- 比特币于2025年10月6日触及126,296美元顶部后下跌约50%,符合减半后480-550天见顶的历史规律,但传统顶部指标(如MVRV、Pi周期、NUPL)均未触发。

- 机构买家(ETF、Strategy公司)取代散户成为主导,ETF净流入峰值达631亿美元,但交易通过托管机构进行,导致链上活动减少,指标无法反映真实需求。

- 散户资金在到达比特币前已被摧毁:超1000万种Memecoin和高FDV(完全稀释估值)代币发行结构吸走了零售流动性,84.7%的2025年新代币交易价低于发行估值。

- 底部预测基于历史周期节奏和结构指标:200周移动平均线(约68,832美元)是历史支撑位,结合死叉及跌幅递减趋势,基准底部区间为45,000-55,000美元,时间指向2026年第三至第四季度。

Original Author: Bull Theory

Original Translation: Yuliya, PANews

Is Bitcoin's 4-year cycle still valid? This is the most predictable crash in crypto history, yet no one was prepared for it.

At the peak of the 2025 bull market, one of the most common narratives in the crypto space was that the 4-year cycle was dead, that institutional entry had changed everything, and that the old rules no longer applied. However, Bitcoin topped out almost exactly as expected, subsequently dropped 50%, and is now exactly where the cycle framework predicted it would be. So, let's have an honest conversation about what actually happened.

The Four-Year Cycle Isn't Dead, the Buyers Just Changed

Throughout 2024 and early 2025, a persistent narrative filled the crypto market: Bitcoin ETFs had changed everything, institutions were buying, and the traditional 4-year cycle driven by halvings and retail FOMO was no longer applicable. This was a supercycle; the bear market wasn't coming back.

This argument sounded convincing. Bitcoin hit a new all-time high before the halving even occurred, something unprecedented. ETF inflows broke records. Michael Saylor was buying billions of dollars worth of Bitcoin weekly. Mainstream financial media was covering Bitcoin as a legitimate asset class for the first time. The overall market sentiment was that the old rules were obsolete.

Yet, Bitcoin peaked at $126,296 on October 6, 2025, and then began to decline. It has now dropped roughly 50% from its high. The Fear and Greed Index is in extreme fear territory, and a death cross has appeared on the charts. The cycle that was thought to be dead is playing out with the precision of 2013, 2017, and 2021.

The 4-year cycle isn't dead; it just became more subtle. The reason it became subtle, the reason no one saw the top coming, the reason none of the top indicators warned us, is the most crucial point for understanding where we are now and where we are headed.

But before diving into that, it's necessary to understand what the cycle actually is and why it has persisted for over a decade. Because those who deny the cycle aren't entirely wrong. The market has indeed changed. However, the cycle wasn't broken; it evolved alongside the market.

Every four years, a halving event cuts the number of newly issued Bitcoins in half by 50%. Miners are Bitcoin's largest and most consistent sellers; they mine Bitcoin and sell it to cover operating costs. When a halving cuts their production in half, the daily sell pressure hitting the market drops dramatically. If demand remains constant or increases, the price must eventually rise. This is the fundamental mechanism of Bitcoin's price movement. It's not a theory; it's supply and demand.

Looking back at halvings since 2012, Bitcoin's price transitions from bull to bear market have repeated without exception.

Four cycles, four halvings. The basic structure of each is identical. And this is what those proclaiming the cycle's death missed: the cycle doesn't care about narratives. It operates on the mechanism of supply and demand, and that mechanism doesn't change just because institutions start buying via ETFs. The April 2024 halving happened as scheduled. Bitcoin topped on October 6, 2025, 535 days later. This falls perfectly within the historical window of 480 to 550 days post-halving seen in every previous cycle.

The cycle never died. It only appeared different because the buyers were different. And this difference – institutional demand replacing retail demand – is precisely why no top indicator was triggered and why most people watching top signals completely missed the peak.

Tracing these four Bitcoin cycles, recording tops, bottoms, death crosses, golden crosses, and the 200-week moving average.

A stable pattern within these cycles that hasn't received enough attention is that the bottom almost always occurs approximately one year after the top. While not exactly a year, the range is remarkably tight. After the 2013 top, the bottom came 410 days later. After 2017, it was 363 days. After 2021, it was 376 days. If this rhythm holds for the current cycle, the bottom of this cycle should fall between late September and mid-November 2026.

There's also a clear trend in the decline data: 86%, 84%, 78%, and now potentially 50% to 65%. Each bear market has been shallower than the last. This isn't accidental. It reflects a maturing asset: one that now has institutional buyers who don't panic sell, a regulated ETF market creating structural demand, and corporations holding Bitcoin on their balance sheets as a treasury reserve. As the buyer base matures, volatility is being compressed.

This cycle also saw something unprecedented: Bitcoin made a new all-time high before the halving. In March 2024, a full month before the April 20 halving, Bitcoin reached $73,581, breaking the previous all-time high of $69,000 set in 2021. This was a new high, but it wasn't the cycle top. Every past cycle eventually topped months after the halving, and this one was no exception – the real cycle top came at $126,296 on October 6, 2025, well after the April 2024 halving. The difference was that hitting a new all-time high before the halving had never happened before. This was due to the approval of spot Bitcoin ETFs in January 2024, which pulled institutional demand into the market before the halving, front-running the cycle timeline and confusing those tracking typical post-halving timeframes.

What Actually Happened to Retail This Cycle?

To understand why Bitcoin topped without any of the usual signals, you have to understand what happened to retail capital in the 18 months leading up to the peak. Simply put: most retail capital was exhausted before Bitcoin even reached $126,000.

In previous Bitcoin bull runs, retail played a specific role. They provided the final fuel, creating the final frenzy and parabolic blow-off top. It was retail FOMO that pushed Bitcoin from a reasonable price to an extreme price in the final stage of each cycle. This is precisely why top indicators were triggered – these tools were originally designed specifically to measure retail behavior, not institutional behavior. Without retail mania, there are no indicator triggers.

In this cycle, retail never materialized in Bitcoin at scale. It's not that they didn't participate in crypto; they did. They just got 'cleaned out' elsewhere first.

The Memecoin Liquidity Trap

The single biggest factor destroying retail liquidity this cycle was the extreme ease of creating and launching memecoins. Token launch platforms (especially on Solana) allowed anyone to issue a token in minutes for nearly zero cost. By mid-2025, the total number of tokens had exploded from roughly 10,000 to 20,000 at the peak of 2021 to over 10 million.

Think about what this means for a retail investor trying to navigate this market. In 2021, you had maybe 200 tokens worth serious consideration – real projects with users, revenue, or at least a credible team and product roadmap. The path from "I want to invest in crypto" to "I bought ETH and SOL" was short and obvious. That's where retail capital concentrated, and it's why ETH hit $4,800 and SOL hit $260.

In 2025, however, you had to choose from 10 million options. The vast majority of these tokens were designed with one purpose: to extract capital from retail buyers and funnel it to insiders as quickly as possible. The playbook is simple: create a token, manufacture hype, sell into retail buying, and cash out. This happens thousands of times daily across the ecosystem.

A retail investor in 2021 faced a manageable number of options, most of which were legitimate projects. A retail investor in 2025 faced millions of options, the vast majority structurally designed to harvest their capital. The result was predictable: retail capital entered the crypto market in 2025, but most of it never flowed to Bitcoin or quality altcoins. It was drained by the memecoin extractive industry first.

The involvement of influential public figures amplified this problem. Numerous high-profile personalities from politics, entertainment, and social media launched their own memecoins this cycle. The pattern was identical every time: a token bearing a celebrity's name launches with massive hype, the price soars as retail buys expecting the fame effect to generate returns, insiders and early holders sell into the rally, and the token crashes 80% to 95% within days or weeks. Retail is left holding worthless tokens worth a fraction of what they paid.

This happened over and over again throughout 2024 and 2025. Each time, a significant chunk of retail liquidity was permanently destroyed in the ecosystem. The people who lost money on these projects didn't take their remaining funds and go buy Bitcoin. They either left the market entirely or had no capital left to deploy.

VC Coins: High FDV, Low Circulating Supply

The second major factor destroying retail capital was the issuance structure of new tokens this cycle. This is discussed less but is equally destructive.

In 2021, new crypto projects typically launched with a fully diluted valuation (FDV) between $100 million and $1 billion. This left real upside for public market buyers. A project launching at a $200 million FDV that grew to a $2 billion FDV could generate a 10x return for retail investors. This is what people remember about 2021 – stories of "I bought this token early and turned $5,000 into $50,000."

This cycle, the structure changed completely. Venture capital funds raised tens of billions of dollars in 2021 and 2022 to invest in crypto infrastructure. By 2024 and 2025, their portfolio companies were ready to launch tokens, and VCs needed to show returns to their Limited Partners (LPs). Consequently, projects began launching with fully diluted valuations of $5 billion, $10 billion, or even $20 billion, while only having 5% to 15% of the circulating supply available on day one.

What does this mean in practice? A retail investor sees a token trading at what appears to be a $500 million market cap and thinks there's room for growth. But the true fully diluted valuation at that price is $10 billion, and 85% of the tokens are sitting in VC wallets waiting to unlock over the next two to four years. Every month, more tokens unlock and get sold. The price faces a structural ceiling because the supply pressure never stops. Retail buyers are essentially buying into a persistent sell-off they don't know about.

An independent study tracking 118 tokens launched in 2025 found that 84.7% were trading below their launch valuation, with a median price decline of 71%. These weren't obscure projects; many were listed on major exchanges, had massive marketing budgets, and received significant media coverage. Yet they still lost most of their value because their tokenomics were designed from the outset to benefit insiders at the expense of public buyers.

The combined consequence of memecoins and high-FDV VC token launches was this: retail crypto capital was destroyed on a massive scale before Bitcoin even approached its cycle top. By October 2025, most retail participants who entered the market in 2024 were either heavily down or had left entirely. There was no liquidity left to rotate into Bitcoin. There was no FOMO wave. The fuel needed for the final, manic top was already gone.

Where Was Retail Capital Supposed to Go?

The 2021 cycle worked because retail capital followed a clear path: Buy Bitcoin → Bitcoin pumps → Rotate to large-cap altcoins → Large-caps pump → Rotate to mid-cap alts → Mid-caps pump → Rotate to small-cap coins. Capital cascaded down a predictable market cap chain, generating returns at each layer.

In 2025, this cascade never kicked off. The mass retail buying of Bitcoin never happened because their capital was already depleted. Bitcoin's market dominance remained above 60% for almost the entire bull market. The altcoin season index peaked at 78% for about three weeks in September 2025 before immediately crashing. There was only a brief window where altcoins outperformed Bitcoin before dominance rapidly climbed back above 60%.

The much-anticipated alt season didn't occur because the market misjudged, but because the mechanism that creates an alt season – retail capital rotating down the market cap chain – was broken. The capital had already been drained.

How Did Institutions Change the Entire Cycle Structure?

Just as retail was losing money on memecoins and VC token launches, something entirely new was happening with Bitcoin. For the first time in the asset's history, a regulated institutional product was funneling tens of billions of dollars into Bitcoin on a structured, continuous schedule.

The approval of spot Bitcoin ETFs in January 2024 wasn't just a headline. It fundamentally changed Bitcoin's marginal buyer, and this change created a cascade of effects that made everything about this cycle different from the past.

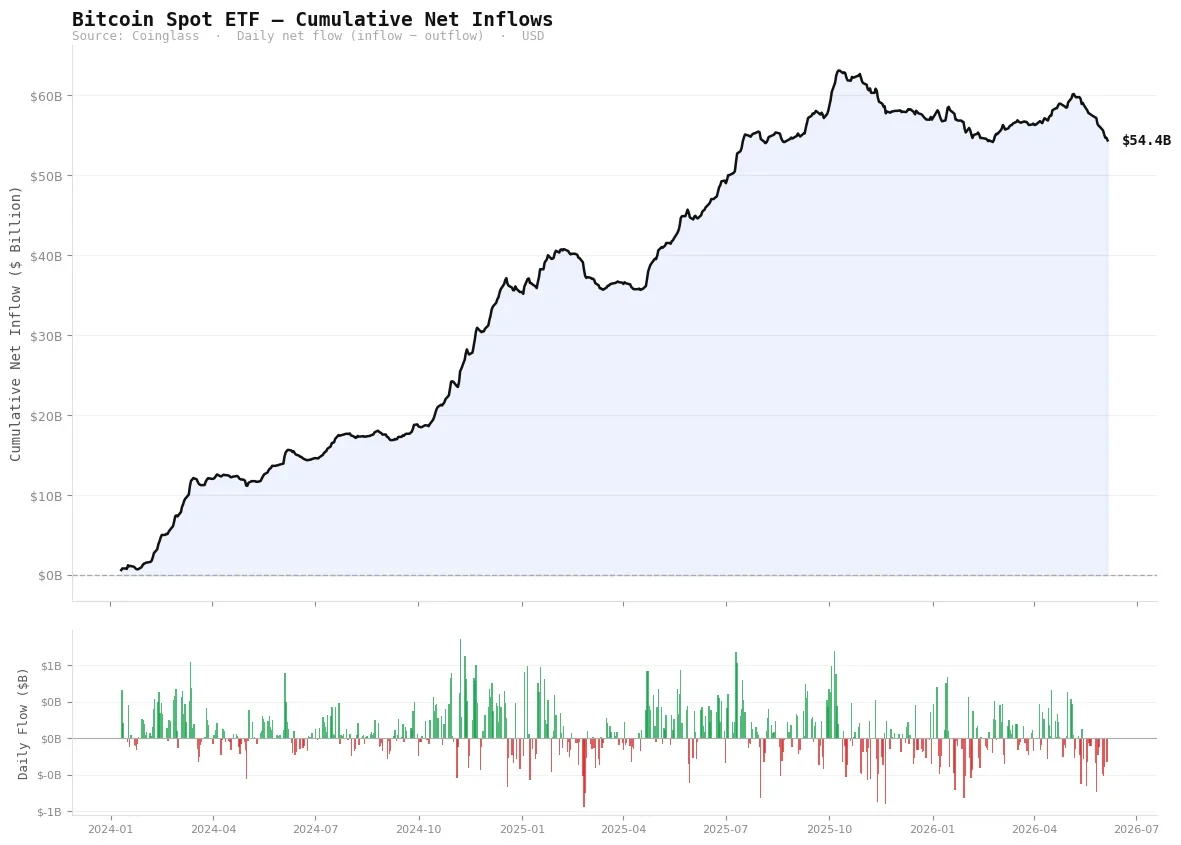

Cumulative net inflows into Bitcoin spot ETFs peaked at $63.1 billion in October 2025 and currently stand at $54.4 billion (Source: Coinglass).

From January 2024 to October 2025, spot Bitcoin ETFs accumulated $63 billion in net inflows. At the peak, average daily inflows exceeded $350 million, 8 to 9 times the value of the new Bitcoin mined by miners each day. On the largest single day, over $1 billion flowed in within one trading session.

These aren't retail investors. They are pension funds, Registered Investment Advisors (RIAs), family offices, endowments, and hedge funds making asset allocation decisions on a quarterly basis. They don't check Bitcoin's price in the middle of the night. They don't FOMO over a green candle on X (Twitter). They receive an asset allocation mandate and execute it systematically over weeks and months.

When this type of buyer becomes the dominant market force, price action looks fundamentally different from a retail-driven market. You don't see long periods of sideways consolidation followed by explosive vertical pumps. Instead, you get a slow, persistent grind higher. No parabolic weekly candles. Just a steady uptrend that doesn't look exciting but produces massive gains over time.

Bitcoin went from $40,000 in January 2024 to $126,000 in October 2025, a 215% gain. In any previous cycle, a move of this magnitude would have inevitably included weeks with single-week gains of 30% or 40%. In the current cycle, the weekly gains were, by historical standards, quite modest. The total gain was huge, but the way it arrived felt methodical, even boring, rather than explosive.

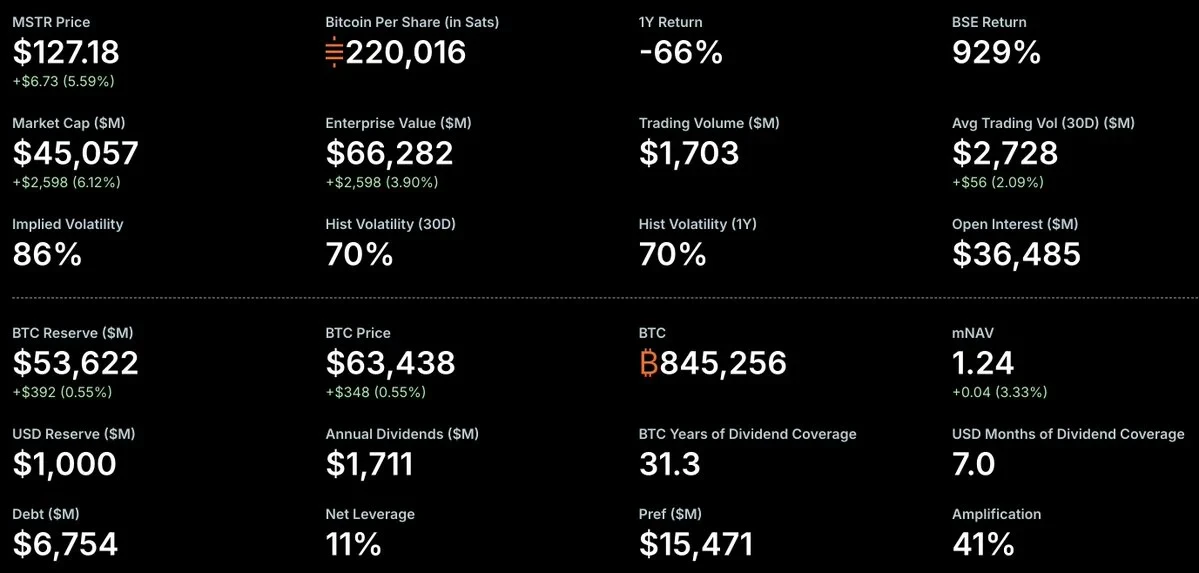

Strategy holds 845,256 BTC, representing 4.02% of Bitcoin's total supply, accumulated through persistent corporate treasury purchases.

Then there's Strategy. Their model is the most extreme version of the institutional buying that defined this cycle. They turned their entire corporate treasury strategy into a Bitcoin accumulation machine, raising capital through stock and preferred share offerings and deploying it directly into Bitcoin purchases. As of June 2026, they hold 843,706 Bitcoin, 4.02% of the future total supply.

In 2025 alone, they raised $25.3 billion from capital markets to buy Bitcoin. They don't sell. They don't hedge. They accumulate continuously, regardless of price. This is a structural buy-side pressure that simply didn't exist in previous cycles.

The key thing to understand about this institutional structure is how it impacted on-chain data. When BlackRock buys Bitcoin for its IBIT ETF, those coins are moved to Coinbase Prime for custody. They become nearly invisible in on-chain analysis, untraceable like retail activity. ETF purchases don't show up on-chain as coins changing hands like retail trades do. The Bitcoin accumulated by Strategy via equity offerings is reported to the SEC, not on-chain. Every dollar of demand generated less on-chain activity than in any prior cycle.

This is the core technical reason every top indicator failed. These indicators measure activity on the blockchain: coin movement, realized profit behavior. Their validity is predicated on retail being the dominant buyer. When the dominant buyer operates through off-chain custodians and registered financial products, the indicators look eerily calm even as hundreds of billions of dollars flow into the asset. The math of the indicators isn't wrong; they are measuring the wrong subject.

Why Did the Eight Top Indicators Fail One by One?

These indicators had a near-perfect track record. In 2013, 2017, and 2021, they signaled tops within days or weeks of the actual peak. Analysts stared at them obsessively throughout 2025, waiting for a signal. Bitcoin broke $126,