한국 증권사가 실적이 "기대에 미치지 못했다"고 발표하자 SK하이닉스가 12% 급락하며 메모리 섹터 전반이 하락 압력을 받았다

- 핵심 의견: 한국 증권사 KIS가 SK하이닉스의 2분기 실적 전망을 하향 조정하면서 주가가 급락했으나, 이는 펀더멘털 악화가 아니라 HBM(고대역폭 메모리) 매출 비중이 너무 높고 장기 계약 가격 고정으로 인해 평균 판매 가격 상승률이 시장 기대치에 미치지 못했기 때문이며, 장기 수익 지속 가능성에 대한 논리는 변하지 않았다는 분석이다.

- 핵심 요소:

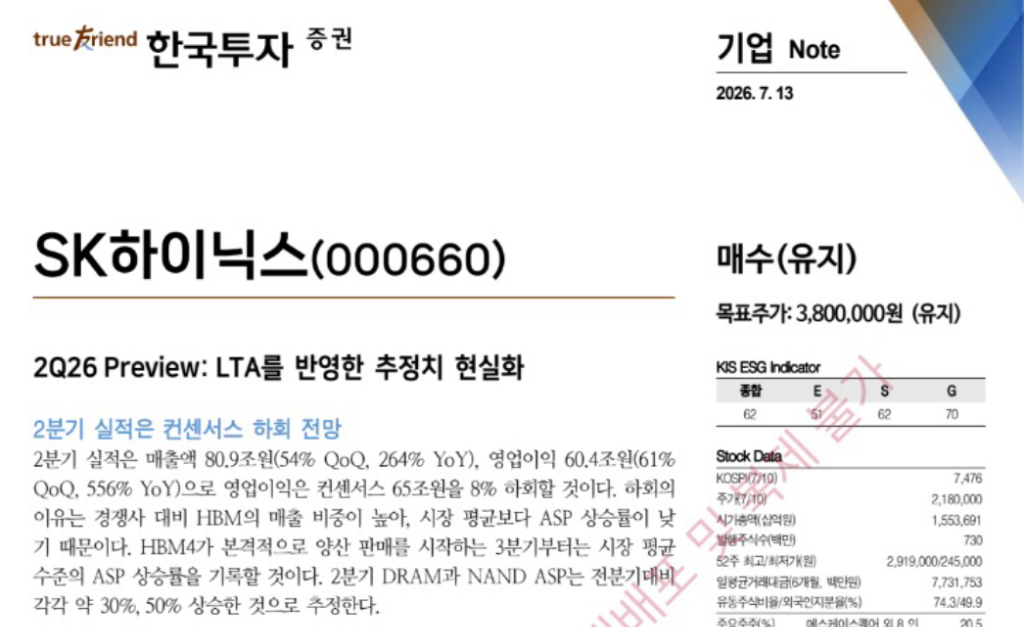

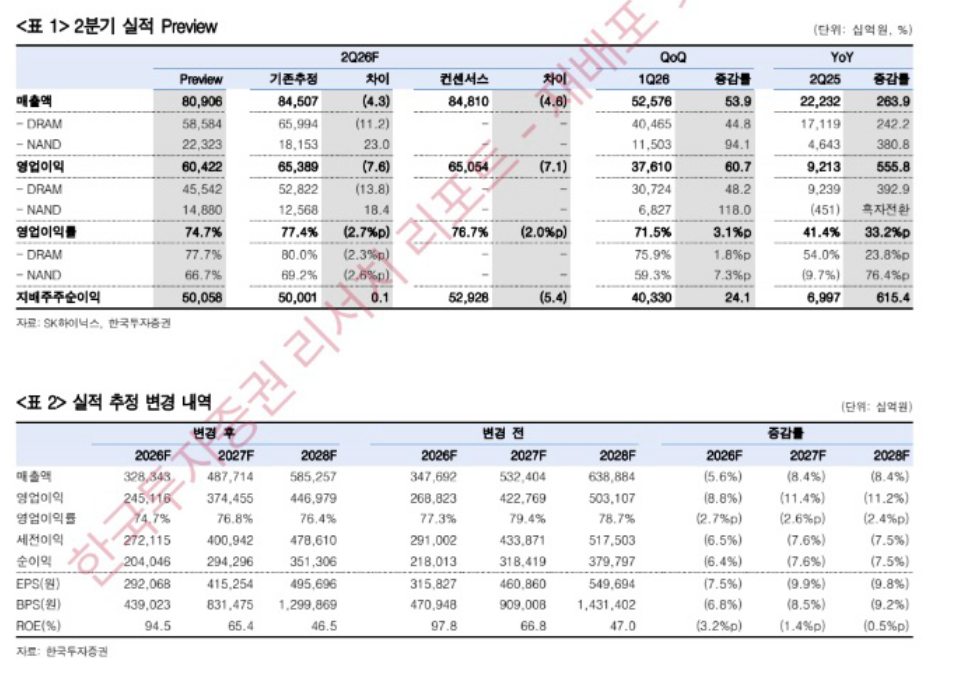

- KIS는 SK하이닉스의 2분기 영업이익을 약 60.4조 원으로 예측했으며, 이는 시장 컨센서스인 65조 원보다 약 8% 낮은 수준으로, 이로 인해 주가가 하루 만에 10% 이상 급락하며 사상 최고가 대비 33% 조정을 받았다.

- 이익이 기대에 미치지 못한 핵심 원인: HBM은 장기 계약(LTA)으로 가격이 고정되어 있어, 같은 기간 DRAM(평균 가격 30% 상승)과 NAND(평균 가격 50% 상승)의 현물 가격 상승 혜택을 충분히 누리지 못했다.

- KIS는 이번 전망 하향 조정이 LTA 가격 가정을 수정한 것에 불과할 뿐 실적 우려 때문이 아니라고 지적하며, 목표 주가 380만 원과 비중 확대 의견을 유지하고, 2026년 2분기 영업이익률이 74.6%를 기록하며 사상 최고치를 경신할 것으로 예상했다.

- 시장 심리가 취약한 가운데, SK하이닉스의 미국 ADR 상장 이후 자금 차익 실현이 매도 압력을 가중시켰고, 이는 홍콩 레버리지 ETF(하루 만에 22% 이상 급락) 및 A주 메모리 관련주로 전이되었다.

- 업계 트렌드: LTA 계약 구조가 3~5년으로 확장됨에 따라, 밸류에이션의 핵심 동력이 분기별 ASP 상승폭에서 수익 지속 가능성으로 전환되고 있으며, 계약 매출 비중 증가는 실적 변동성을 낮출 것이다.

Original author: Long Yue

Original source: Wall Street Insights

On July 13, Korean local brokerage KIS released a report forecasting SK Hynix's second-quarter performance. It is estimated that SK Hynix's Q2 revenue will be 80.9 trillion won, up 54% quarter-on-quarter and soaring 264% year-on-year; operating profit will be 60.4 trillion won, up 61% quarter-on-quarter and 556% year-on-year.

The numbers look impressive, but here’s the issue: The market consensus expectation was 65 trillion won, and KIS’s forecast is about 8% below that consensus.

This deviation directly ignited the market.

After the Korean stock market opened, SK Hynix's stock price quickly fell over 10%, breaking through the 2 million won mark. From its all-time high on June 25, it has corrected by 33% in just three weeks.

High HBM Share Actually Drags Down ASP

KIS explained the core reason for the profit falling short of consensus in its report: SK Hynix's HBM (High Bandwidth Memory) revenue share is higher than its peers, with a higher sales proportion, leading to its average selling price (ASP) increase being below the market average.

This logic seems counterintuitive at first glance — isn't HBM a high-end product, so a higher share should mean higher profitability?

The key lies in the pricing structure. HBM is typically priced through Long-Term Supply Agreements (LTAs), where contract prices are relatively fixed and do not rise significantly in the short term with market fluctuations. In contrast, ordinary DRAM and NAND have higher price elasticity in the spot market. When the overall market price rises, the ASP increase for these types of products is actually larger.

SK Hynix's higher HBM share means it benefits less from the "price increase dividend" in this round of rising average market prices compared to its peers.

During the same period, the average spot prices of ordinary DRAM and NAND are still soaring — KIS predicts Q2 DRAM average prices will rise about 30% quarter-on-quarter, and NAND by about 50% — but Hynix's overall ASP increase is being "held back" by HBM's contract prices.

Downgrade Due to LTA Recalculation, Not Fundamental Deterioration

KIS clearly stated in the report that this downward revision is not due to performance concerns, but is a correction resulting from incorporating the price assumptions of already-signed Long-Term Supply Agreements (LTAs) into the forecast.

The report's original wording is: "This is the result of incorporating signed LTAs into price assumptions and adjusting the forecast realistically, not a concern about performance."

KIS also lowered its operating profit forecasts for 2026 and 2027, which are about 9% and 11% lower respectively than before. However, the brokerage emphasized that as HBM4 begins mass shipment officially from the third quarter, the rising average market price will drive overall ASP higher. At that point, SK Hynix's ASP increase will return to the market average.

KIS predicts that the operating profit margin for Q2 2026 will reach 74.6%, a historic high, and will continue to rise each quarter thereafter.

The brokerage maintains its target price of 3.8 million won and a buy rating, believing that this forecast revision is only a short-term disturbance and does not change the mid-to-long-term upward performance trend.

"A 556% Surge That Missed Expectations": The Crack in Market Sentiment

A year-on-year increase of 556% is an extremely strong number in any industry. But the logic of the capital market is: What matters is not how much it has risen, but whether it met expectations.

The market had already fully priced in the consensus expectation of 65 trillion won. KIS's forecast was about 4.6 trillion won lower than this number, which is essentially a declaration that "expectations were too high."

This triggered a two-fold concern: first, the direct impact of the short-term performance falling short; second, whether the high HBM share constitutes a structural risk — meaning the more SK Hynix bets on HBM, the more limited its ASP elasticity becomes during the contract price lock-in period.

Compounding this, SK Hynix just listed on the US stock market last Friday. Some funds that bet on the IPO chose to cash out after the ADR listing, further intensifying the selling pressure.

Contagion Spreads: Hong Kong ETFs and A-Share Memory Stocks Fall Simultaneously

SK Hynix's decline quickly transmitted to neighboring markets.

In Hong Kong stocks, the 2x Long SK Hynix Leveraged ETF fell over 22% in a single day, and the 2x Long Samsung Electronics ETF fell over 13%.

A-share memory concept stocks followed suit. Core stocks like GigaDevice, Ingenic Semiconductor, Longsys, and Biwin Storage all fell over 7%.

However, from a broader perspective, the memory semiconductor sector has been in an adjustment period for nearly half a month. Some individual stocks have fallen over 20%, touching the technical bear market line. Behind this lies the factor of global funds rebalancing their allocations within AI and across different markets, including the rotation logic of "selling chips, buying cloud," as well as the phased rebound in the Hong Kong stock market attracting capital back.

Brokerage: Long-Term Thesis Unchanged, Focus on Earnings Sustainability

Despite triggering market turmoil, KIS's overall stance in the report is not pessimistic.

The brokerage believes that as the memory industry shifts towards a 3- to 5-year LTA contract structure, the core driver of corporate valuation will shift from "single-quarter ASP growth" to "how long high profitability can be sustained."

The KIS report states: "From now on, the focus needs to be on the sustainability of earnings. The expansion of LTAs is reducing the long-standing performance volatility of the memory industry."

The brokerage expects that as the proportion of contract-based revenue increases and HBM capacity expansion squeezes overall supply, SK Hynix's high profitability level can be maintained long-term, leading to a re-rating of its valuation.

The target price of 3.8 million won still implies significant upside from the current stock price, and KIS maintains its buy rating.