The "Chinese Hynix" Earning 400 Million a Day, Even Apple Is Begging to Buy

- Core Thesis: As the world's fourth-largest DRAM manufacturer, CXMT is about to list on the STAR Market. Leveraging Qimonda's technological legacy and support from Hefei state capital, it achieved a staggering profit reversal during the 2026 DRAM super-cycle, earning back nine years of losses in six months. However, this profitability primarily depends on the cycle rather than structural advantages.

- Key Factors:

- In Q1 2026, CXMT reported revenue of 50.8 billion yuan and a net profit of 33 billion yuan, earning nearly 4 billion a day, surpassing Kweichow Moutai in profitability. Market expectations suggest its market cap could challenge for the top spot in A-shares.

- Founded in 2016, the company leveraged Qimonda's technical documents (2.8TB of data) and approximately $2.5 billion in redesign costs to achieve mass production of 19nm DDR4, filling a gap in China's independent DRAM production.

- Cumulative losses reached 36.65 billion yuan by the end of 2025, but with a net profit of 33 billion yuan in Q1 2026, it turned profitable and covered years of losses within six months, primarily driven by the DRAM price cycle (contract prices up 93%-98% quarter-on-quarter).

- Customers include major domestic and international companies such as Apple, Google, Tencent (with a supply agreement exceeding 20 billion yuan), Alibaba Cloud, and ByteDance, indicating rapidly growing market recognition.

- The IPO aims to raise 29.5 billion yuan, one of the largest fundraising amounts on the STAR Market, for backend technology upgrades and new projects. The valuation is anchored at 158.4 billion yuan, but institutions anticipate a market cap of 3-4 trillion yuan.

Original Author: Jialiu

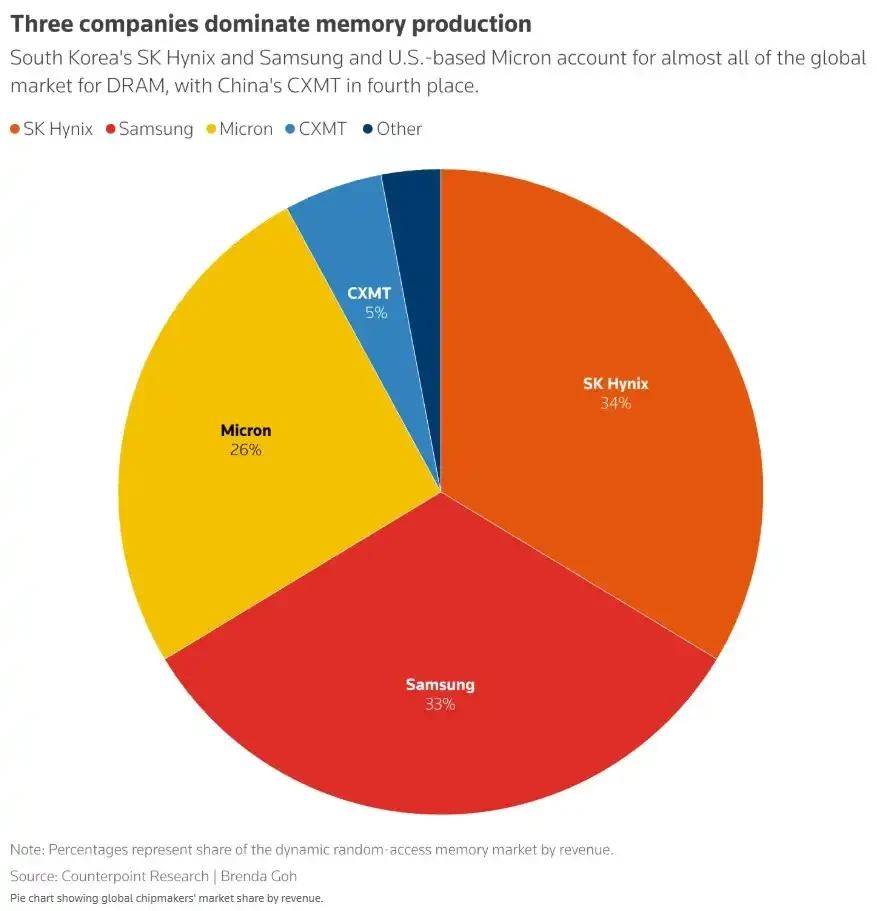

When it comes to the global memory storage industry, most people only know Samsung, SK Hynix, and Micron. However, many are unaware that the world's fourth-largest player is a Chinese company yet to be listed, named CXMT (ChangXin Memory Technologies).

On July 9, CXMT updated its latest IPO prospectus for the STAR Market. Timing-wise, subscriptions start on July 16, payments are due on the 20th, and trading on the STAR Market could begin as early as the end of the month.

China's strongest memory storage leader is arriving on the market by the end of this month.

Data shows that for Q1 2026, projected revenue is 50.8 billion yuan, a year-on-year increase of 719%. Net profit is 33 billion yuan. Earning nearly 4 billion yuan per day, its profitability surpasses Kweichow Moutai. The market values it at trillions of yuan, potentially challenging for the highest market cap on the A-share market.

Yet, by the end of 2025, the company's accumulated losses were still 36.65 billion yuan.

In other words, ChangXin Memory earned back nine years of losses in just half a year. This domestic chip company, which had been losing money for nearly a decade, suddenly became one of the most profitable hard-tech enterprises on the A-share market.

Over the past week, the name 'ChangXin Memory' has appeared frequently in global tech media. Apple is lobbying the U.S. government for a special license, planning to include CXMT in the memory supply chain for Macs and iPads. Google has also initiated a procurement evaluation for CXMT's DRAM. Other reports mention that HP and Dell are validating CXMT's DRAM, while Acer and ASUS are requesting Chinese partners to use more domestic memory chips. In the same week, Reuters disclosed that Tencent signed a long-term server DRAM supply agreement with CXMT worth over 20 billion yuan, lasting three to five years. CXMT's prospectus also lists clients like Alibaba Cloud, ByteDance, Lenovo, Xiaomi, OPPO, vivo, and Honor.

Leading companies in the global memory manufacturing field; CXMT's share ranks fourth globally, following SK Hynix, Samsung, and Micron. Source: Reuters

Suddenly, ChangXin Memory has become a favorite for almost all major domestic and international companies.

How did CXMT go from zero to fourth in the world? How much of its current profit is due to strength versus luck? Can its trillion-yuan valuation hold?

CXMT's Predecessor: GigaDevice

The origin story of CXMT begins with why China has been lacking DRAM.

Memory chips come in various types. NAND Flash retains data even when power is off, used in hard drives, SSDs, and USB drives. DRAM is volatile runtime memory—data is lost when power is off, but it's fast, serving as the immediate workspace for CPUs, GPUs, mobile SoCs, and AI accelerators.

Both NAND and DRAM are commodity semiconductors, but DRAM manufacturing is more akin to a steel mill combined with high-precision manufacturing. Each generation of process technology pushes capacitors, transistors, word lines, and bit lines to their limits, replicating billions of highly consistent units on a single wafer. Even a slight deviation can crash yields and explode costs, potentially hemorrhaging money during a market downturn.

This is why the DRAM market ended up with just three giants: Samsung, SK Hynix, and Micron. This table isn't something you can join just by having a "tech team"; you must survive over a decade-long cycle of price wars, capacity wars, patent wars, equipment restrictions, and customer qualifications.

ChangXin Memory was initiated around 2016, based in Hefei. Its key figure is Zhu Yiming.

Photo of Zhu Yiming in a meeting

The name Zhu Yiming is not unfamiliar in the Chinese semiconductor circle.

Born in 1972, Zhu Yiming was a child prodigy. He entered Tsinghua University's Physics Department at 17. Although he studied physics, he excelled at programming, earning over 300,000 yuan a year in the late 1990s by writing software for other companies. During this work, he realized that chips were all designed in the U.S. at the time. Believing chip technology was more advanced, he went to the U.S. to study electronic engineering and later worked in Silicon Valley.

A younger photo of Zhu Yiming (right)

In Silicon Valley, Zhu noticed that the memory industry had shifted from the U.S. to Japan, then to South Korea and Taiwan. He judged that China had a significant opportunity to emerge as a "Chinese version of Samsung." He designed an SRAM (Static Random Access Memory) chip and returned to China in 2005 to found a company called GigaDevice.

From its inception, GigaDevice was a pure design house. It didn't manufacture chips itself; all wafer fabrication was outsourced to foundries. Its main products were NOR Flash (used in routers, game console boot code) and MCUs (microcontrollers for refrigerators, washing machines). Zhu led his team to create China's first SRAM and IP technology, first serial NOR Flash product, and first 32-bit general-purpose MCU based on the ARM Cortex-M3 architecture. By its IPO in August 2016, it was China's largest code-storage flash memory chip design company, with revenue growing from 1.489 billion yuan in its IPO year to 9.203 billion yuan.

Asset-light, high gross margin, no need to build your own factory. This was the smartest way for China's IC design industry at the time.

However, this model had a prerequisite: ample foundry capacity and stable prices. In the second half of 2020, Zhu hit a roadblock. SMIC's 8-inch wafer capacity became severely tight, forcing GigaDevice to shift some NOR Flash orders to Hua Hong Semiconductor's 12-inch fab, incurring higher production costs. Consequently, its gross margin for Q4 2020 plummeted from its previously stable level above 37% to 29.49%. The impact of foundry capacity constraints was directly reflected on the income statement.

During the same period, GigaDevice was also paying for another acquisition. In 2019, it acquired Shanghai Silead for 1.7 billion yuan, a premium of 16 times, creating 1.305 billion yuan in goodwill. Silead made in-display fingerprint chips. Zhu aimed to combine memory, controllers, and sensors into a platform-type design company. However, Goodix sued Silead for patent infringement, leading to a price war. Silead only fulfilled 58% of its three-year performance commitment. From 2020 to 2023, GigaDevice took goodwill impairment charges for Silead for four consecutive years, totaling about 900 million yuan, consuming most of the 1.3 billion goodwill. The strategy of horizontal acquisitions to expand product categories also proved unworkable.

The lesson Zhu learned from these two events was: the ceiling for an asset-light design company isn't design capability, but capacity. Furthermore, the real battleground for memory chips isn't in NOR Flash, which accounts for only 2.5% of the global market, but in DRAM. However, DRAM can't be produced by general-purpose foundries like NOR Flash. DRAM processes are highly proprietary. Each company's cell structure, capacitor design, and word line processes are customized. Samsung, SK Hynix, and Micron all operate an integrated design and manufacturing model. To make DRAM, there's only one path: build your own fab.

This is the background and reason for the birth of ChangXin Memory.

After BOE and NIO, Hefei's Third Major Bet

GigaDevice's financials and shareholder structure could not support the investment scale required for building a DRAM fab. After all, Phase 1 alone cost 18 billion yuan, with total investment exceeding 100 billion yuan, accompanied by nearly a decade of losses. This capital could only come from a different source.

In 2016, the Hefei municipal government extended an olive branch.

The market often calls Hefei "the city best at venture capital." Its most famous successful venture was BOE. This company, now the world's number one LCD panel shipper with annual revenue exceeding 200 billion yuan and China's panel makers holding over 70% of the global LCD market, started its journey in Hefei.

In September 2008, BOE signed a framework agreement with Hefei for a Gen 6 line investment. The project had a total investment of 17.5 billion yuan. The 6 billion yuan registered capital was provided by Hefei, injected through a BOE private placement, and then all put into the project company. Instead of just giving BOE a simple subsidy, Hefei used local government platforms to take a controlling stake, provide bridging funds, offer loan interest subsidies, and supply land and energy support, shouldering BOE's most difficult construction phase. Hefei then attracted glass substrates, polarizers, driver chips, equipment, and materials around BOE, earning itself the city label "Capital of New Displays."

The second typical story is NIO. In April 2020, NIO was just climbing out of its near-death experience in 2019. Hefei Construction Investment and Anhui Emerging Industry Investment jointly invested 7 billion yuan in cash in NIO China, and NIO China's headquarters was established in the Hefei Economic Development Zone. Later, NIO became one of the representative brands of high-end electric vehicles in China, with its market capitalization briefly exceeding 100 billion USD.

The strategy: find asset-heavy leaders, use transaction structures to replace simple subsidies, help companies through the construction phase, and then use the leader to anchor upstream and downstream industries locally.

In 2016, Hefei applied the same investment logic for its next major bet.

Yuan Fei, an early key figure at Hefei Industry Investment Group, later said: "Whether from Hefei Industry Investment or the industry side, everyone involved in CXMT's early stages bore unprecedented risk and pressure."

After all, DRAM is harder than displays or complete vehicles, with higher risks related to technology, equipment, yields, patents, and export controls. But from the perspective of local industrial organization, it was similar to BOE and NIO: consuming cash in the short term, but if successful in the long run, it would significantly change the supply-demand dynamics of a whole supply chain.

Hefei, Anhui Promotes the Integrated Circuit Industry

Hefei Industry Investment contributed 14.4 billion yuan in CXMT's Phase 1 alone, with a total project investment exceeding 100 billion yuan.

In July 2018, GigaDevice issued an announcement: Zhu Yiming resigned as the company's General Manager, retaining only the Chairman position, and officially became CXMT's Chairman and CEO. The industry called it Zhu Yiming's "second entrepreneurial venture."

Current shareholder lists reveal the composition of this bet. The top five shareholders are Qinghui Jidian (21.67%, wholly controlled by Hefei state capital), CXMT Integrated (11.71%), Phase II of the Big Fund (8.73%), Hefei Jixin (8.37%), and Anhui Investment Group (7.91%). Hefei state capital holds a combined stake of over 36%.

Among other shareholders, Alibaba Cloud holds 3.85% (6.1 billion yuan investment, valuing CXMT at 158.4 billion yuan), and GigaDevice holds 1.8%. The investor list also includes China Structural Reform Fund, CICC Capital, Legend Capital, China Merchants Capital, Yunfeng Fund, Tencent, and Alibaba.

The money and momentum were in place. But Zhu Yiming's "second entrepreneurial venture" still lacked one thing: core technology.

The Technological Legacy of a Bankrupt German Company

Around 2016, Samsung, SK Hynix, and Micron collectively controlled over 90% of the global DRAM market share—the result of a decade-plus elimination tournament.

The DRAM industry, starting in the 1980s, killed off players every few years.

Japan once held over 80% of global DRAM production capacity. By the 2010s, only Elpida was left struggling, eventually acquired by Micron in 2012. Europe once had Infineon's subsidiary Qimonda, which went bankrupt in 2009.

Zhu Yiming's solution lay hidden within this German company that had gone bankrupt in 2009.

The name Qimonda combines two words. "Qi" is Chinese for "energy," the flowing vitality. "Monda" is Latin for "world." The literal meaning: the key to opening the world.

It was a beautiful name, but the company's fate was tragic.

Qimonda was spun off from its parent company Infineon in May 2006 and listed on the NYSE on August 9, 2006, under the ticker QI. At its IPO, it was already a major global supplier of memory products and a leader in 300mm wafer manufacturing technology. By 2008, Qimonda had completed the development of its 46nm Buried Word Line trench-based product, offering 100% capacity improvement over the previous 58nm generation. It was ready for mass production.

Image of Qimonda DDR2/GDDR chip products

But the financial crisis hit. DRAM prices crashed. Samsung, willing to produce at a loss, expanded capacity to pressure competitors. Qimonda's new technology couldn't reach mass production before its cash flow ran out. It went bankrupt in 2009. The lights went out for Europe's last major memory manufacturer. The Munich R&D center was vacated, its 12,000 employees scattered, absorbed by Samsung, Micron, and SK Hynix. In 2012, Qimonda's bankruptcy administrator began selling its 7,500 patents.

Zhu Yiming saw his opportunity in this history.

Qimonda died from the cycle, not its technology. The 2.8 TB of technical documents and tens of thousands of patents it left behind were a legacy frozen for nearly a decade. Traces of Qimonda's original buried word line and honeycomb capacitor structures can still be found in the DRAM products of Samsung, Micron, and SK Hynix today, having indirectly flowed into their process systems through partners like Inotera and Winbond.

But how to acquire this legacy and use it to build a fab was a huge challenge, with a bloody lesson preceding it.

2016 was considered the "Year One" for the resurgence of memory in China. Before this, China's DRAM industry had completely declined, facing technological monopolies from the U.S., South Korea, and other foreign companies, with no capability to fight back.

At that time, alongside CXMT, two other parallel national storage projects were launched: YMTC (Yangtze Memory Technologies Corp) in Wuhan for NAND Flash, and Jinhua Integrated Circuit (JHICC) in Fujian for DRAM.

In 2017, Micron filed lawsuits simultaneously in the U.S. and Taiwan against UMC and JHICC, accusing three employees who moved from Micron to UMC of stealing Micron's DRAM trade secrets. One was accused of stealing over 900 technical documents. In October 2018, the U.S. Department of Commerce placed JHICC on the Entity List for national security reasons, imposing export controls. UMC immediately announced the suspension of its technology cooperation with JHICC. Equipment supply was cut off, technical cooperation was frozen, and the project stalled. The U.S. Department of Justice also filed a criminal indictment against JHICC and UMC for economic espionage, facing potential fines of over $20 billion. It wasn't until late 2023 that Micron and JHICC reached a global settlement, ending a dispute lasting six years.

The lesson from JHICC was clear: getting involved in trade secret disputes related to Micron led to being placed on the Entity List, equipment cutoffs, and project shutdowns. A new DRAM company that triggers intellectual property issues would find commercial clients unwilling to use its products, equipment suppliers unwilling to supply, and its international market strangled by litigation.

Therefore, when Qimonda's bankruptcy administrator began selling the 7,500 patents, Zhu Yiming quickly acquired over ten million DRAM technical documents (about 2.8 TB of data), which included around 16,000 patent applications at the time. Subsequently, he spent approximately $2.5 billion on a complete redesign of the original architecture, advancing Qimonda's 46nm process to the 10nm level. He also signed patent