SemiAnalysis:没有看空英伟达,「AI央行」或撬动7万亿债务雪球

- 핵심 주장: SemiAnalysis의 최신 분석에 따르면, 엔비디아는 '후원 계획(Backstop Plan)'을 통해 AI 컴퓨팅 임대 업체에 최소 수익을 보장하며, 일종의 'AI 중앙은행' 역할을 수행하고 있습니다. 이는 은행 대출을 활성화하고 GPU 구매자 기반을 확대하기 위한 전략입니다. 2029년까지 전 세계 AI 부채 금융 규모는 7조 달러를 돌파하여 미국 주택 담보 대출 시장에 이어 두 번째로 큰 자산 담보 부채 시장이 될 것으로 예상됩니다.

- 핵심 요소:

- 엔비디아는 자체 AA/Aa2 신용 등급을 활용하여 Neocloud(Neocloud)에 GPU 임대 수익을 보장합니다(일반적으로 6년 기간). 시장 수요가 부족할 경우, 엔비디아는 사전에 설정된 가격으로 컴퓨팅 파워를 매입하겠다고 약속함으로써 은행의 대출 리스크를 낮추고 GPU 판매를 촉진합니다.

- AI 인프라 금융 모델은 클라우드 거대 기업의 현금 흐름 의존도에서 벗어나 대규모 부채로 전환되고 있으며, '삼위일체'의 난관에 봉착했습니다. 프로젝트를 시작하려면 자본(대출), 청약 계약(고객), 데이터 센터(용량)가 동시에 확보되어야 하며, 이 세 가지 요소는 모두 필수적이면서도 순환적인 딜레마에 빠지기 쉽습니다.

- 보증 구조 아래에서 Neocloud는 프로젝트의 금융 실현 가능성을 얻기 위해 약 18%의 상승 수익(6년 평균 수수료 기준)을 포기해야 합니다. 최악의 시나리오에서 프로젝트 수익률은 0에 가까울 수 있지만, 대출 기관은 해당 시나리오에서도 부채 상환이 가능할 것을 요구합니다.

- 현재 엔비디아의 보증 프로젝트는 아시아 태평양 지역에 집중되어 있습니다. 여기에는 호주의 SharonAI(72MW 공장, 총 보증 가치 488억 달러)와 인도네시아의 Firmus(360MW 클러스터, 6년간 고객 수익 2500~3000억 달러 예상)가 포함됩니다.

Original Author: Zhao Ying

Original Source: Wall Street CN

On July 6, renowned semiconductor research firm SemiAnalysis posted a series of six tweets on X, revealing that NVIDIA's Kyber NVL144 rack is delayed by over 12 months due to PCB mid-plane manufacturing challenges. Asian AI hardware supply chain stocks plummeted in response.

NVIDIA subsequently responded, stating its "roadmap remains unchanged", but did not disclose specific progress details.

The controversy persists. On July 7, SemiAnalysis published another paid long-form article, this time turning its focus on NVIDIA. However, this time the firm did not adopt a "bearish" stance.

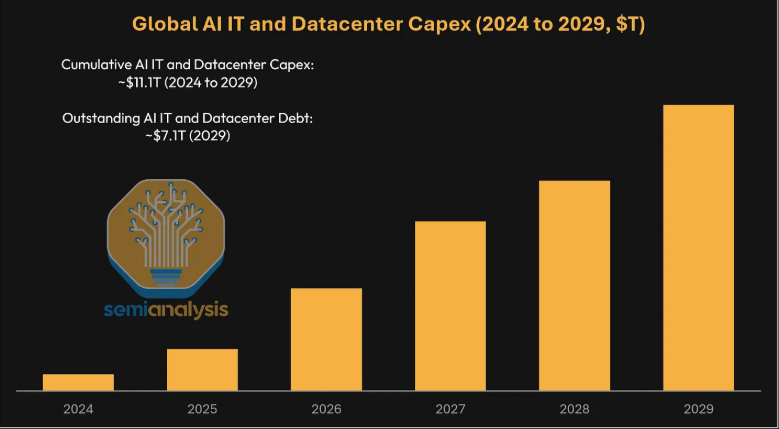

SemiAnalysis projects: By 2029, the global AI debt financing scale will surpass $7 trillion. What does $7 trillion represent? It will become the second-largest asset-backed debt market globally, second only to the U.S. residential mortgage market (approximately $13 trillion).

What is NVIDIA's role in this? SemiAnalysis revealed a strategic initiative by NVIDIA—the "backstop" plan. NVIDIA is leveraging its own AA/Aa2 investment-grade credit rating to provide minimum revenue guarantees for AI computing rental companies, thereby incentivizing bank lending. In other words, NVIDIA is positioning itself as the ultimate lender and insurer of the entire AI ecosystem, recording substantial sales on its books while partially shouldering the risk of insufficient downstream demand. SemiAnalysis likened NVIDIA to the "central bank of the AI field."

Addressing the discussions on X regarding whether SemiAnalysis is "bearish on NVIDIA," the firm stated:

It has not released any positive or negative views on NVIDIA stock, but is merely accurately capturing supply chain and technical details; the market can trade on this information as it sees fit.

AI Debt Snowball: Topping $7 Trillion by 2029, Rivaling the U.S. Mortgage Market

SemiAnalysis believes AI infrastructure construction is forming a multi-trillion dollar credit market. By 2029, outstanding AI-related debt could reach approximately $7.1 trillion, a scale surpassing all other U.S. asset-backed debt markets except mortgage financing.

This debt primarily stems from two types of capital expenditure. One is AI IT CapEx, including GPUs, networking, storage, and supporting CPUs. The other is AI data center CapEx, including the facilities, power, and cooling infrastructure required to house these GPUs.

Historically, cloud giants like Google, Amazon, Meta, Microsoft, and Oracle primarily relied on their own cash flow to build AI clusters. However, over the past year, companies like Oracle, Meta, and even Google have increasingly turned to debt. As project scales continue to expand, the market constraint is no longer just about securing GPUs or finding data center space, but about securing sufficiently cheap and long-term financing.

SemiAnalysis concludes that the financing methods for AI CapEx are changing. The balance sheets of cloud giants are not infinite. If all AI clusters rely on a handful of investment-grade cloud providers for backing, new projects will inevitably hit credit bottlenecks sooner or later.

The "Trilemma": Capital, Customers, and Data Centers Are All Indispensable

SemiAnalysis breaks down AI project financing into a "trilemma": capital, underwriting contracts, and data centers.

First is capital. Lenders typically require long-term take-or-pay contracts from investment-grade cloud providers or similar credit guarantees before they are willing to lend. In other words, what lenders truly value is not the credit of the Neocloud itself, but the credit of its underlying customers.

Second is underwriting. To secure customers, Neoclouds often need to first prove they can pay GPU deposits and lock in hardware. But to secure equity funding, they need to first demonstrate they have customers and loans. This creates a chicken-and-egg cycle in the early stages of a project.

Third is the data center. Neoclouds either need to use customer contracts and financing to convince data center operators to lease capacity, or build their own data centers. The latter option incurs significantly more capital pressure and longer timelines.

This model locks the market into a template of "5-year terms backed by cloud giants." The problem is that many VC-backed AI startups and inference service providers require short-cycle, large-scale computing power, not 5-year long-term contracts. Inference providers are particularly reluctant to bear long-term price and demand risks, often preferring to forgo computing power rather than sign leases exceeding one year.

NVIDIA, the "AI Central Bank": Leveraging AA-Grade Credit to Jumpstart the Market

NVIDIA introduced the "backstop plan" to bridge this funding gap.

According to SemiAnalysis, NVIDIA provides GPU lease revenue guarantees to Neoclouds. If third-party customer demand is insufficient, NVIDIA commits to purchasing computing power at a preset price; if the Neocloud leases the computing power at a higher price, NVIDIA shares in a portion of the excess revenue.

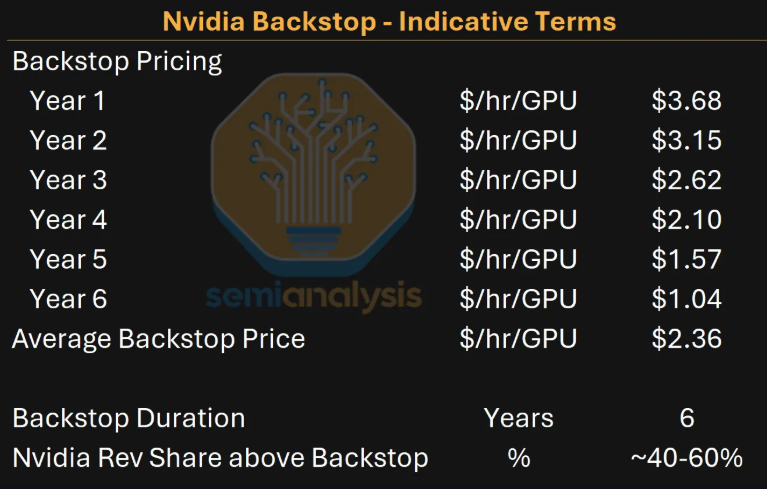

These arrangements are typically for 6-year terms, providing a minimum revenue guarantee for the underlying GPU capacity based on a predetermined price curve. The Neocloud can still lease the computing power to any customer and can offer more flexible lease terms. NVIDIA's guarantee is triggered only when market demand is insufficient to lease the capacity at market prices.

This is the origin of the "AI Central Bank" metaphor. NVIDIA isn't literally issuing currency, but within the AI computing credit system, it plays a role akin to the ultimate buyer and credit endorser. Lenders can evaluate a project's worst-case scenario based on NVIDIA's AA/Aa2 credit rating, making them more willing to extend loans.

For NVIDIA, this helps expand the buyer base for its GPUs. If the market relied solely on a few mega cloud providers signing 5-year underwriting contracts, GPU demand would quickly hit financing constraints. Furthermore, these cloud providers are developing their own custom chips as a hedge against NVIDIA systems. Supporting Neoclouds and more enterprise clients effectively opens new financing channels for GPU demand.

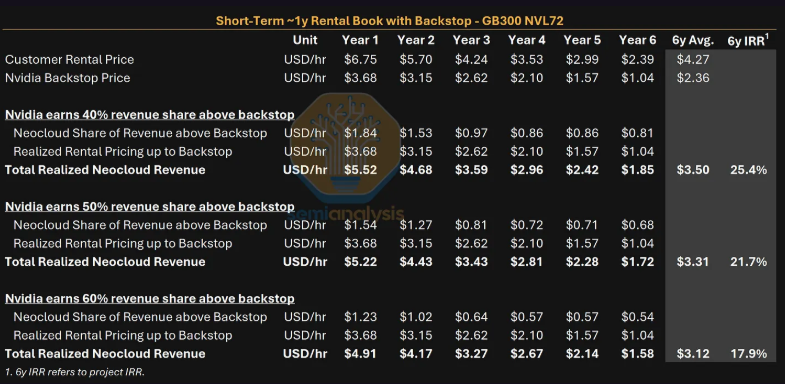

Deconstructing the "Backstop Plan": How Much NVIDIA and NeoClouds Earn

SemiAnalysis emphasizes that Neoclouds do not use NVIDIA's credit for free. Under the backstop structure, Neoclouds must sacrifice a portion of their upside potential in exchange for project financiability.

In an example price curve, the 6-year average backstop price is $2.36 per GPU hour. Assuming a 1-year lease price for the GB300 in the first year is $6.75 per hour, and the first-year backstop price is $3.68 per hour, the difference between the customer price and the backstop price is $3.07. If NVIDIA takes 40% of the amount exceeding the backstop price, NVIDIA receives $1.23, the Neocloud receives $1.84, resulting in an actual first-year revenue for the Neocloud of $5.52 per hour, lower than the $6.75 without the backstop.

Over six years, in this scenario, NVIDIA takes an average cut of approximately 18%. The Neocloud's project IRR also decreases. In a scenario with NVIDIA's backstop and primarily 1-year short-term leases, the project IRR is 25.4%; without the backstop but still able to secure financing and lease capacity, the IRR could reach 40.7%.

The key lies in the worst-case scenario. If demand is insufficient, the Neocloud can only lease computing power back to NVIDIA, potentially resulting in project returns near zero or even slightly negative. Lenders don't require the project to be profitable in the worst case; they only require that debt can still be serviced. Therefore, the viability of the debt increasingly hinges on the reliability of NVIDIA's backstop.

This is the core issue for investors: NVIDIA's arrangement helps drive GPU sales and Neocloud expansion in the short term. However, if computing demand falls short of expectations, the revenue shortfall will be borne by NVIDIA. The debt may not be directly recorded on NVIDIA's books, but the safety net of the financing model is increasingly concentrated on NVIDIA's credit.

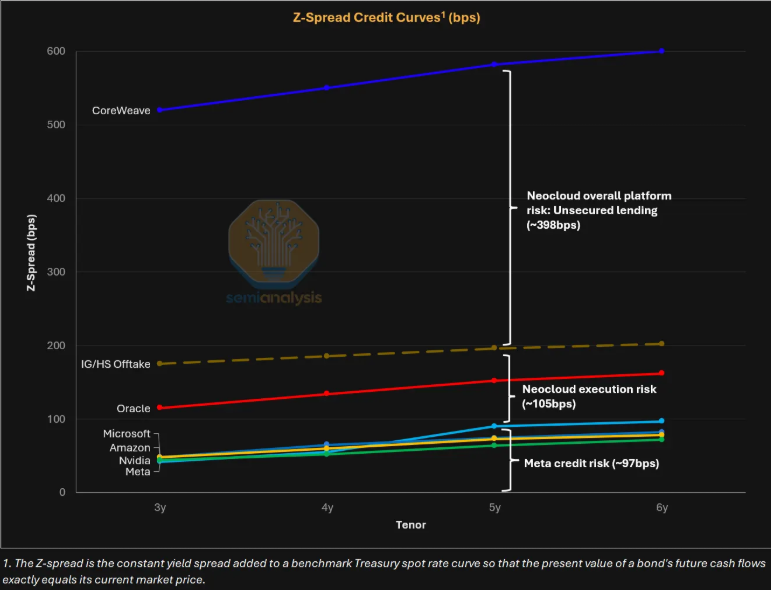

GPU Financing Pricing Ultimately Depends on the Endorser

SemiAnalysis states that current pricing in the GPU financing market is primarily based on who signs the long-term underwriting contract, not the Neocloud's own creditworthiness.

CoreWeave serves as a reference. Its 5-year unsecured bond yield is approximately 10%. However, in the $8.5 billion DDTL 4.0 delayed draw term loan backed by Meta, the fixed-rate portion costs approximately 5.9%, only 90 basis points higher than Meta's own 5-year bond yield of about 5.0%. This 90 basis point spread roughly represents the market's pricing of CoreWeave's execution risk.

If a Neocloud operates without a long-term cloud provider underwriting, financing costs increase significantly. For top-tier Neoclouds, unsecured financing might require paying around 10% interest rates, approximately 4 percentage points higher than backed financing. At a loan-to-value ratio of 70% to 80%, financing costs rise from 5.62% to 10%, causing the pre-tax profit margin to drop from 14.8% to 5.4%.

NVIDIA's backstop positions pricing between these two: higher than the roughly 5.9% total yield of current cloud provider-backed deals, but lower than the approximately 10% yield of CoreWeave's unsecured bonds. Banks prioritize the Debt Service Coverage Ratio (DSCR). For projects with NVIDIA's backstop, loan sizes are typically sized based on the scenario where the backstop is triggered, requiring a minimum DSCR of 1.3x in the early years, corresponding to a loan-to-value ratio usually between 70% and 80%.

Public Projects Amplify in Asia-Pacific, Backstop Model Begins Implementation

Currently disclosed NVIDIA backstop projects are concentrated in the Asia-Pacific region.

The first is the 72MW AI factory by SharonAI in Australia. Announced in June 2026, the project plans to scale up to a maximum of 40,000 GB300 units under a 6-year backstop agreement. SharonAI disclosed a total backstop value of $4.88 billion, translating to an average 6-year floor price of approximately $2.33 per GPU hour.

Another is Firmus's 360MW AI cluster in Batam, Indonesia, potentially located in DayOne's Kabil Industrial Tech Park facility. Announced on June 29, 2026, this project indicates that NVIDIA's backstop is entering a larger scale.

Firmus estimates project customer revenue over six years to be between $25 billion and $30 billion. Target customers include AI-native companies, enterprise clients, and inference service providers, with varying lease terms. However, before deploying GPUs, Firmus still needs to finalize its data center provider or continue with self-building.

SemiAnalysis also notes that NVIDIA is not the only GPU manufacturer using backstop arrangements. AMD has already offered similar arrangements to clients like AWS, OCI, DigitalOcean, Vultr, Tensorwave, and Crusoe last year: clients purchase more AMD GPUs, and if the Neocloud cannot fully sell the capacity, AMD is willing to lease back a portion under long-term contracts for internal software development.

SemiAnalysis Denies Bearish Stance, but Market Remains Highly Sensitive to Its Signals

This article comes amid controversy surrounding SemiAnalysis itself.

On the morning of July 6, SemiAnalysis posted a series of tweets on X, claiming that NVIDIA's Kyber NVL144 rack architecture faced significant delays, pushing it back over 12 months to 2028. The news garnered attention in pre-market trading, causing declines in multiple AI hardware supply chain stocks in Japan, South Korea, and Taiwan. NVIDIA subsequently responded, stating its product roadmap remains unchanged and denying any impact on core progress.

This context makes SemiAnalysis's subsequent article more susceptible to market interpretation as either bearish or bullish on NVIDIA. In response, SemiAnalysis stated on X that it has not released any positive or negative views on NVIDIA stock, but is merely sharing the company's supply chain and technical details.

Crackerjack Finance countered the "bearish" interpretation, noting that SemiAnalysis's charts show H2 actual data is 20% higher than market expectations, leading to a forecast of approximately $15 EPS for the next fiscal year and a stock price target between $300 and $400. THE Grand Poobah commented, "the tripartite circular financing seems insufficient," pointing to market concerns about the increasing complexity of financing structures.

The issue is that AI-related assets have experienced years of appreciation, with valuations and expectations at elevated levels. Any supply chain risk signals or changes in financing structure are rapidly amplified. While SemiAnalysis's clarification shows it did not directly provide a stock opinion, following the Kyber NVL144 incident, the market influence and credibility debate surrounding its supply chain revelations will continue to coexist.

For investors, the true implication of this "long-form" article is: AI competition is no longer just about "who has the GPUs," but about "who can simultaneously piece together GPUs, debt, customer contracts, and data centers." NVIDIA's backstop mechanism may continue to amplify GPU demand, but it could also concentrate the tail-end stress of the AI debt cycle more heavily on NVIDIA's own credit.