ウォルシュ、初登板で着地:ドットチャートはまだあるが、FRBはすでに変わった可能性がある未来を説明するのではなく、現在の判断のみを行う。- 核心となる見解:新たにFRB議長に就任したウォルシュ氏は、初のFOMC会合において、自身がドットチャートを提出せず、曖昧な政策指針を示したことで、将来の見通しを示すガイダンスを弱め、「データ重視」の意思決定へと移行するシグナルを発した。これにより、市場は利上げ経路を再評価し、リスク選好度が低下した。

- 重要要素:

- 今回の金利決定は据え置かれたが、焦点はウォルシュ氏による初の政策コミュニケーションにあり、市場はこれを事前に十分織り込んでいた。

- 19名のFRB理事のうち、ドットチャートを提出したのは18名のみ。ウォルシュ氏自身は意図的に提出を見送り、同メカニズムのガイダンスとしての重要性を弱める意図があった。

- ウォルシュ氏はデータへの依存と会合ごとの決定を強調し、将来の政策シグナルを頻繁に発することを否定。パウエル氏時代の透明性重視のコミュニケーションモデルから転換した。

- 決定後、市場は政策反応関数を再評価。一部の金利先物は、早ければ2026年10月頃にも再利上げのシナリオを議論し始めた。

- 米国の主要3株式指数は揃って下落。S&P500(-1.2%)とナスダック(-1.3%)は1%を超える下落率となり、リスク選好度は著しく冷え込んだ。

- 核心となる見解:新たにFRB議長に就任したウォルシュ氏は、初のFOMC会合において、自身がドットチャートを提出せず、曖昧な政策指針を示したことで、将来の見通しを示すガイダンスを弱め、「データ重視」の意思決定へと移行するシグナルを発した。これにより、市場は利上げ経路を再評価し、リスク選好度が低下した。

- 重要要素:

- 今回の金利決定は据え置かれたが、焦点はウォルシュ氏による初の政策コミュニケーションにあり、市場はこれを事前に十分織り込んでいた。

- 19名のFRB理事のうち、ドットチャートを提出したのは18名のみ。ウォルシュ氏自身は意図的に提出を見送り、同メカニズムのガイダンスとしての重要性を弱める意図があった。

- ウォルシュ氏はデータへの依存と会合ごとの決定を強調し、将来の政策シグナルを頻繁に発することを否定。パウエル氏時代の透明性重視のコミュニケーションモデルから転換した。

- 決定後、市場は政策反応関数を再評価。一部の金利先物は、早ければ2026年10月頃にも再利上げのシナリオを議論し始めた。

- 米国の主要3株式指数は揃って下落。S&P500(-1.2%)とナスダック(-1.3%)は1%を超える下落率となり、リスク選好度は著しく冷え込んだ。

- 核心观点:新任美联储主席沃什在其首场FOMC会议上通过自身缺席点阵图及模糊政策指引,释放了弱化前瞻指引、转向“数据依赖”决策的沟通框架转向信号,导致市场重新定价加息路径,风险偏好下调。

- 关键要素:

- 本次利率决议维持不变,但焦点在于沃什首次政策沟通,市场此前已充分定价。

- 19位美联储委员中仅18人提交点阵图,沃什本人主动缺席,意在弱化该机制的指引意义。

- 沃什强调数据依赖和逐次会议决策,反对频繁释放未来政策信号,改变了鲍威尔时期的透明沟通模式。

- 决议后市场重估政策反应函数,部分利率期货定价开始讨论最早2026年10月前后再次加息的情景。

- 美股三大指数集体收跌,标普500(-1.2%)和纳指(-1.3%)跌幅超1%,风险偏好显著降温。

Original: Odaily Planet Daily (@OdailyChina)

Author: Azuma (@azuma_eth)

Early in the morning of June 18, Beijing time, the Federal Reserve officially announced its latest interest rate decision. As expected, the federal funds rate remains unchanged within the established range, in line with market expectations.

In the weeks leading up to the decision, there was little debate over the rate path in market pricing, and the market had already fully priced this in. Therefore, the real focus of this rate decision was not on "whether to cut rates," but on how the new Fed Chair, Warsh, would conduct his first policy communication — this was Warsh's first FOMC meeting as Chair, and the first opportunity for the market to observe how he will shape the monetary policy communication framework for years to come.

The Dot Plot Remains, but Warsh is Absent

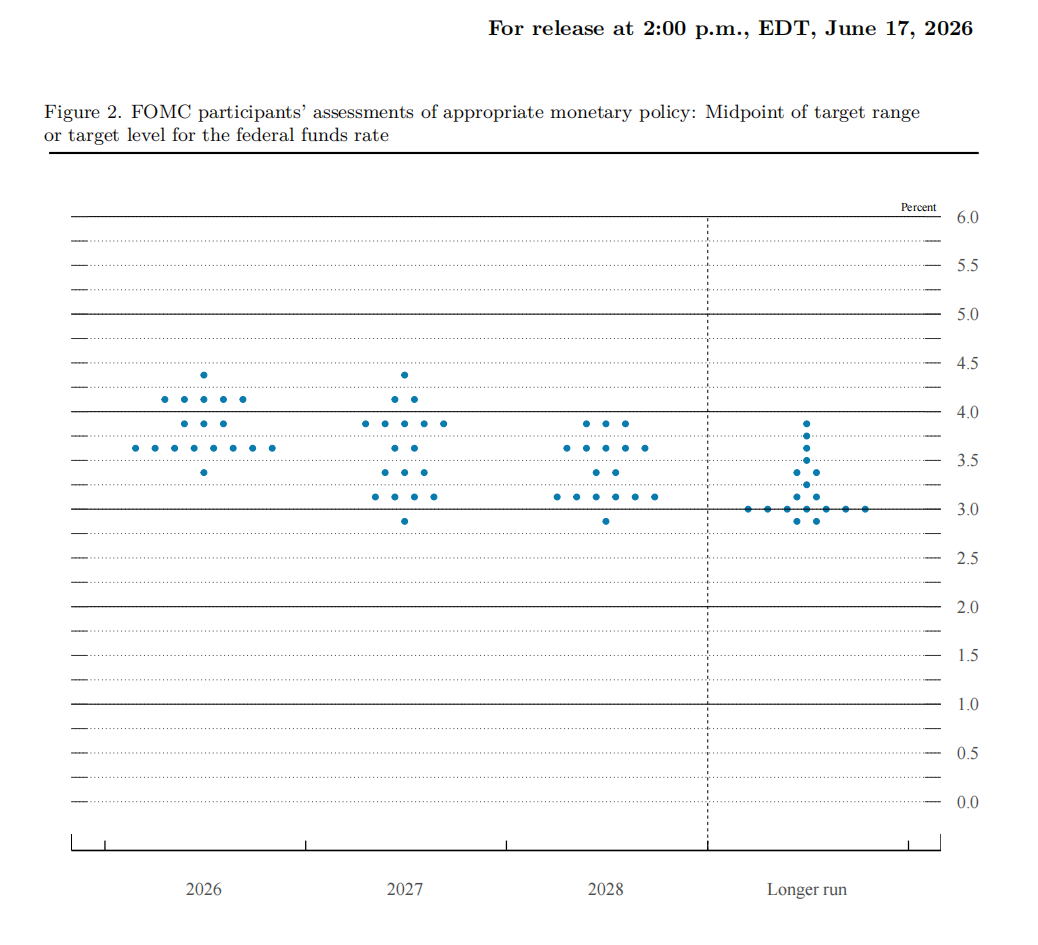

The most discussed change from this meeting came from the structure of the economic projections and the dot plot itself.

- Odaily Note: The so-called "Dot Plot" is the Fed's quarterly interest rate projection tool. Each dot represents an FOMC member's expectation for the future federal funds rate. Although these projections are not official policy commitments, they reflect the committee's overall view on the economic and inflation outlook, and have long been regarded by the market as a key reference for interpreting the Fed's policy direction.

In the latest FOMC economic projections, only 18 of the 19 Fed officials submitted dot plot forecasts. Among them, 1 member believes the Fed should cumulatively raise rates by 75 basis points for the remainder of 2026, 5 members favor a cumulative 50 basis point hike, 3 members favor a cumulative 25 basis point hike, 8 members prefer to keep rates unchanged, 1 member advocates for a cumulative 25 basis point cut, and 1 member is absent.

Warsh later acknowledged during the press conference that it was he who did not submit a rate projection. Warsh explained, "I did not put forward any of my own projections, which is consistent with my long-held view, at least regarding its current structure."

In contrast to his predecessor Powell's highly transparent and frequent communication style, Warsh has long been a representative of the "less is more" school. He has repeatedly expressed skepticism about "the effectiveness of the dot plot," "excessive forward guidance," and "frequent release of policy signals." In Warsh's view, the Fed does not need to tell the market every step it will take in the future, but should make decisions based on real-time economic data.

Although the market once speculated that Warsh might promote reforms to the dot plot mechanism, or even abolish it directly, the dot plot was not directly canceled after this meeting. However, Warsh's own absence still sends a clear signal — the Fed is downplaying the guiding significance of the dot plot.

The Implicit Shift in the Fed's Communication Framework

Warsh also stated at the press conference that the Fed would implement a series of reform measures in the future, including establishing multiple special working groups to explore more open data collection methods and study improvements to the existing statistical indicator system.

During the subsequent Q&A session, when repeatedly pressed by reporters about the next step on rate hikes and whether current rates are restrictive, Warsh repeatedly refused to provide clear guidance.

Over the past decade, one of the Fed's core capabilities has been to continuously lower market uncertainty through the dot plot, the Summary of Economic Projections (SEP), and press conferences. The market's intense focus on the Fed's every move is fundamentally because it provides a "predictable path."

But Warsh's stance is changing this logic. Clearly, Warsh emphasizes data dependence, making decisions meeting by meeting, and maintaining a more restrained expression regarding the future path.

If this tendency continues, the market will face a structural change — the Fed will no longer try to "explain the future," but only describe "its current judgment." This will directly weaken the certainty function of forward guidance.

Rate Hike Expectations Heat Up, Market Risk Appetite Declines

Following the rate decision, the market quickly repriced the policy path.

After Warsh emphasized that "the central bank will not tolerate high inflation," the market began to reassess the upper bound of the Fed's policy reaction function, i.e., whether there is a possibility of more aggressive tightening than previously expected when inflation hasn't significantly declined.

This change first manifested in short-term assets.

Traders began to bet on a higher terminal rate. Pricing in some interest rate futures contracts indicates the market is already discussing the possibility of another rate hike around October at the earliest, while not ruling out tail risks of a more aggressive path. Polymarket probability data also rose in tandem, reflecting that the market is opening a window for pricing a "window for re-tightening."

U.S. stocks fell significantly after the decision. All three major indices closed lower, with the S&P 500 (-1.2%) and the Nasdaq (-1.3%) both falling over 1%. Tech stocks led the decline, and market risk appetite noticeably cooled.

Structurally, this adjustment is not a simple "rate hike shock" driven by a single factor, but a more typical triple repricing:

- Higher short-term rates: The path for rate hikes has been reopened.

- Risk asset pullback: Valuation sensitivity to interest rates has amplified.

- Stronger dollar + yield curve volatility: Reflecting increased policy uncertainty.

Importantly, the market is not simply trading on "a weakening economy" or "the disappearance of rate cut expectations," but on a more complex logic — under Warsh's new communication framework, inflation constraints have been re-elevated, and the "upside tail risk" of the policy path is becoming more real.

In other words, if inflation does not fall quickly, will the Fed return to a tightening stance earlier and faster than the market originally expected?

Warsh's Shift May Be Just Beginning

In conclusion, looking only at the outcome of this meeting, the Fed has not undergone a radical shift. Rates are unchanged, the dot plot remains, and the system is still functioning. However, if the focus shifts from "policy path" to "communication style," the change has already begun.

Warsh's debut felt more like a signal test. He didn't abolish old tools, but he didn't fully rely on them either. He chose to "diminish their effect and lower their weight."

Looking at the longer-term implications, the biggest question left by this debut is not "whether the Fed will raise rates next," but "when the Fed stops spoiling the market path, how will the market reprice the world?"