写在SpaceX初の上場後:時価総額2.1兆ドル、まだ追う価値はあるのか?

- 核心的見解:SpaceXは6月12日に135ドルでIPOを実施し、初日終値は160.95ドル、時価総額は2.1兆ドルとなった。好調なスタートを切ったものの、一部の市場予想を下回り、高バリュエーションや赤字事業に対する市場の合理的な評価が浮き彫りとなった。

- 主要な要素:

- SpaceXのIPO価格は135ドル、初日始値は150ドル、終値は160.95ドル。株式の所有者は極めて集中しており、経営陣のロックアップ期間は最長366日、初期の浮動株時価総額は約750億ドルにとどまる。

- SpaceXの2025年通期の純損失は49億ドル、2026年第1四半期の損失は42.8億ドル。唯一の黒字事業であるスターリンクは2025年に44.23億ドルの営業利益を計上したが、打ち上げ事業では6.57億ドルの損失を計上した。

- マスク氏は目論見書の中で、宇宙でのコンピューティング能力事業計画(年間100GWのコンピューティング能力容量を展開)を提案し、その潜在市場は28.5兆ドルに達すると主張。実際の収益性をはるかに上回り、「SF小説」と評されている。

- 個人投資家向けIPO株式の割合は約20%と、通常の水準を大幅に上回った。しかし、市場の動向は個人投資家が価格により関心を持っていることを示しており、その行動が最終的な上昇率を押し上げるのではなく、ボラティリティを高めた。

- 主要なタイミングは以下の通り:7月にナスダック100指数に組み入れられる可能性が極めて高く、これにより数百億ドルのパッシブ資金が流入する見込み。8月には第2四半期決算と一部の内部者株式ロックアップ解除が予定されており、市場の不確実性が高まる。

Original: Odaily Planet Daily (@OdailyChina)

Author: Golem (@web 3_golem)

On June 12, local time in the United States, Elon Musk did not go to New York. Before SpaceX stock (Nasdaq: SPCX) officially debuted on Nasdaq, he chose to stay at the company's Texas headquarters, standing among his employees to complete a remote bell-ringing ceremony.

During the ceremony, Musk once again narrated SpaceX's story towards a more distant future. He stated that the company's goal is to send humans to the Moon, Mars, and even farther into interstellar space. After the bell-ringing, Nasdaq's live broadcast channel played Elton John's "Rocketman," adding a romantic footnote to the most anticipated IPO in the history of space commercialization.

But the sentimental part ended there, and the game of capital markets began immediately. SpaceX IPO was priced at $135, opened at $150 on its first trading day, briefly surged past $176 during the session, and ultimately closed at $160.95, temporarily fixing its market capitalization at $2.1 trillion.

Opened at $150, Market Cap Settles at $2.1 Trillion on Debut

SpaceX's IPO has been under global scrutiny since it filed its registration statement with the U.S. SEC. The company ultimately decided to issue approximately 555.6 million shares of Class A common stock at a fixed price of $135, corresponding to a company valuation of $1.77 trillion.

In terms of equity distribution, Musk personally holds approximately 42%, Valor Equity holds about 7.3%, Google holds about 5%, other early venture capital institutions collectively hold 10-12%, employees and former employees hold 10-15%, and the publicly offered shares in this IPO account for only 4.2%. Although Musk and his affiliated interest groups hold the majority of SpaceX shares, none of their holdings can be sold on the listing day. The lock-up period for core investors like Musk and Valor Equity is 366 days, while ordinary IPO shareholders (institutions and employees) must also go through a basic lock-up of 180 days, meaning they cannot sell until at least the end of 2026.

Therefore, on the listing day of June 12, the initial circulating shares were only the approximately 555.6 million Class A common stock offered in the IPO. SpaceX is a typical "low float, high FDV" project. According to its valuation model, the first-day circulating market cap was about $75 billion, which is roughly in line with SpaceX's originally planned fundraising amount.

Investors familiar with crypto projects are no strangers to highly controlled models. Consequently, market sentiment quickly fell into FOMO during the subscription phase. Reports indicate that SpaceX received over four times oversubscription, with combined institutional and retail demand exceeding $250 billion. Retail investor subscriptions alone surpassed $100 billion, far higher than the $75 billion issuance size. Crypto players also participated in this feast, but unfortunately, most ended up empty-handed. (Related reading: SpaceX On-Chain IPO Dreams Dashed: Amid the Trillion-Dollar IPO Feast, I Only Got 4 Shares)

Notably, SpaceX planned to allocate as much as 30% of its IPO shares to retail investors, significantly lowering the barrier to participation in this tech feast. Typically, such large IPO projects only allocate 5% to 10% to retail investors. Although SpaceX ultimately gave only about 20%, it was still double the conventional IPO allocation.

The reason for this is that SpaceX management believes retail investors will hold their stocks long-term, much like Tesla's current core investor base is also predominantly retail. Essentially, they trust that retail investors will pay for the dream Musk describes. However, this time, retail investors were much more rational than expected (detailed below).

Before SPCX officially started trading on Nasdaq, its pre-market quote on Hyperliquid fluctuated between $170 and $175, corresponding to a company valuation exceeding $2.2 trillion. In the Nasdaq call auction phase just before the official open, SPCX's indicative opening price was initially reported at $172, up about 29% from the IPO price, roughly in line with pre-market expectations. But an hour later, the indicative opening price slid rapidly, eventually opening at $150, an increase of only about 11% from the IPO price.

According to Gate's US stock market data, SPCX eventually rose to around $176 during the session before closing at $160.95, up about 19% from the IPO price but only about 7.3% from the opening price. The first-day market cap settled at $2.1 trillion. In terms of results, SpaceX's debut performance was definitely a success, making Musk the world's first trillionaire. However, the result was not spectacular and even failed to meet all market expectations.

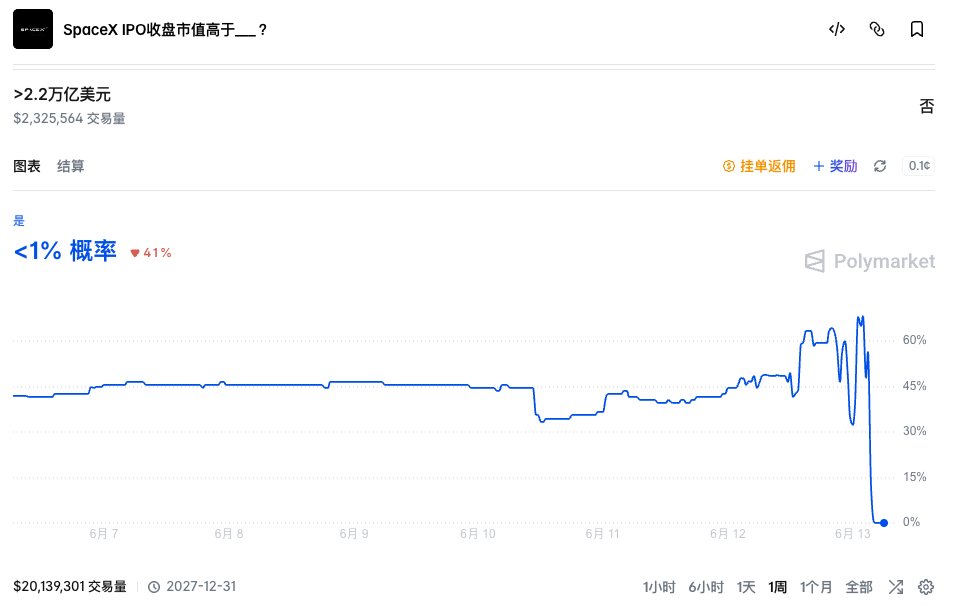

In the pre-pricing of SpaceX, not only did some Pre-IPO platforms stumble, but prediction markets were also off. Just hours before the SpaceX IPO, the market generally expected its market cap to break above $2.2 trillion. On Polymarket, the probability of "SpaceX IPO closing market cap above $2.2 trillion" was still above 65%, once peaking at 70%.

However, as SPCX's price opened "relatively low," the probability of this event began to fluctuate wildly. Ultimately, SpaceX's IPO closing market cap settled near $2.1 trillion, and the event was resolved as "No."

Retail Investors Affect Volatility, Not Price Appreciation

There is only one reason for this phenomenon: although the market is still willing to believe in SpaceX's narrative and the "Musk premium," SpaceX is simply too expensive. Given a good price, even the strongest conviction can be sold.

SpaceX is the first super-behemoth in human history to land directly on the capital market with a "trillion-dollar valuation." On its debut, its market cap surpassed tech giants like Meta and Samsung, making it the world's ninth most valuable company. But even the most frenzied retail investors know that its current revenue cannot support its massive valuation. SpaceX has yet to achieve profitability, reporting a net loss of $4.9 billion for the full year 2025 and a net loss of approximately $4.28 billion in Q1 2026.

Starlink is currently SpaceX's only profitable business. According to the prospectus, Starlink generated $11.387 billion in revenue for the full year 2025, accounting for 61% of SpaceX's total revenue, with an operating profit of $4.423 billion. It has over 10.3 million global users and over 9,600 satellites in orbit. In Q1 2026, it achieved revenue of $3.257 billion and an operating profit of $1.188 billion. However, this "cash cow" business is just SpaceX's side hustle.

Space launches are SpaceX's main招牌. As of the prospectus disclosure, the Falcon rocket family has completed over 650 launches with a success rate of 99%. Its reusable rocket booster technology provides a significant cost advantage and technological leadership within the industry. However, SpaceX's largest external customer for its launch business is the U.S. government, and the business is still operating at a loss. In 2025, the launch business reported an operating loss of $657 million with a loss rate of 16.1%. In Q1 2026, the operating loss soared to $662 million, with a loss rate of 107%.

The reason for the huge losses is SpaceX's increased investment related to Starship. However, given current technological and use-case bottlenecks, Starship is still some distance away from true commercial mass production.

Beyond these two businesses, SpaceX's still-hyped space computing business is also factored into its valuation system. Compared to the mature Starlink and launch businesses, Musk's claims regarding the space computing business might be a bit overblown.

Simply put, SpaceX's plan involves sending GPUs into low Earth orbit, using solar power to provide cloud computing power for global AI computing clusters. In the prospectus, Musk stated that SpaceX's goal is to deploy 100GW of AI computing capacity into orbit annually. Currently, the global AI industry's annual electricity demand is around 15-25GW. This means that SpaceX's planned orbital computing system could theoretically support roughly a fivefold expansion of today's global AI industry scale.

Lest readers don't know what 100GW means: the installed capacity of the Three Gorges Dam is about 22.5GW. So, a single space computing center in Musk's plan would be equivalent to 4.4 Three Gorges Dams operating at full capacity.

Furthermore, SpaceX explicitly stated in the prospectus that its future (primarily AI-related businesses) could potentially tap into a $28.5 trillion addressable market. For context, China, the world's second-largest economy, had a nominal GDP of approximately $19.4 trillion in 2025. The figure proposed by SpaceX is equivalent to 1.47 times China's 2025 nominal GDP.

Reading this content, one might wonder whether this is an IPO prospectus or a science fiction short story. Even the most FOMO-driven investors would need to cool down upon seeing these numbers. Research firm CFRA issued a "Sell" rating on SpaceX after its listing, with a target price of $115.

Besides the mismatch between actual business and valuation, the large proportion of retail IPO shares might also be a reason for the suppression of SPCX's stock price. Musk released 20-30% of SpaceX's IPO shares to retail investors. The larger the retail shareholding ratio, the greater the inherent volatility. Retail investors can buy without regard for cost due to FOMO, and they can also sell emotionally on any slight fluctuation without thinking. Therefore, what retail investors truly affect is volatility, not the final price appreciation.

Key Inflection Points Ahead

Of course, whether you are sitting on the sidelines waiting or have already cashed out, the following three time points are particularly important for investors focused on SpaceX.

Around 15 Trading Days Post-IPO (Approximately July 6 - July 7)

This is the most important time point, as SpaceX is expected to be directly included in the Nasdaq 100 Index after 15 trading days. In March, Nasdaq specifically amended its rules. Previously, newly listed companies had to wait three months to be eligible for index inclusion, but now they can be fast-tracked in just 15 trading days after meeting conditions, and the minimum float requirement of about 10% has also been removed. These new rules seem tailor-made for SpaceX and the subsequent wave of AI tech giants.

If SpaceX is successfully included in the index, it means that over ten billion dollars in global funds will be passively forced to buy SpaceX stock, providing significant support for its share price. So, if it's highly probable that SpaceX will be included in the Nasdaq index in July, and top-tier funds will buy the stock then, as an investor, would you choose to buy in advance now and sell it to them at a higher price later?

On the other end, however, some U.S. pension funds and long-term insurance funds have expressed opposition. In May 2026, three of the largest U.S. public pension fund managers (with over $1 trillion in assets under management) jointly wrote to Musk expressing concerns about the potential passive fund risks associated with rapid index inclusion post-IPO. The same month, Randi Weingarten, president of the American Federation of Teachers (representing approximately 1.8 million teachers, healthcare workers, and public employees), directly wrote to the SEC requesting a special review of the SpaceX IPO.

SpaceX Q2 2026 Earnings Report (Mid-to-Late August)

The second key time point is SpaceX's Q2 2026 earnings report release in August, which will be its first report card as a public company. If the business shows no progress compared to the current situation (and significant progress is unrealistic anyway), the stock price could face further pressure. Furthermore, the SpaceX prospectus stipulates that two days after the company releases its Q2 2026 earnings report, eligible internal shareholders (employees, former employees, and some early investors) can sell a portion of their locked-up shares—up to 20% of their locked holdings. If the stock price has risen 30% from the IPO price and meets this standard for 5 out of 10 trading days, an additional 10% can be unlocked.

This means that in August, the market will not only have to contend with earnings-related volatility from SpaceX but will also face the first major unlock of shares since the listing, posing a significant challenge.

Whether we will ultimately "suffocate" for Musk's dream remains to be seen. Judging from the debut day's performance, while the market chose to believe the story, it did not completely lose its senses. What will determine SpaceX's fate next is its own actual performance.

Recommended Reading:

SpaceX On-Chain IPO Dreams Dashed: Amid the Trillion-Dollar IPO Feast, I Only Got 4 Shares