Bernstein Analysis: TSMC Target Price Set at NT$2,780, Can CoWoS and N2 Take the Baton?

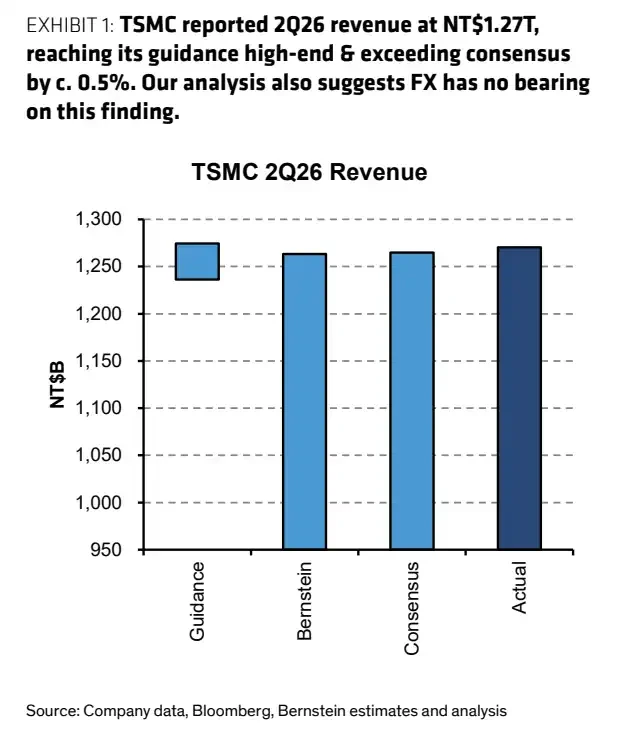

- Core View: TSMC's Q2 2026 revenue reached NT$1.27 trillion, a 36% year-over-year increase, with AI demand continuing to materialize. However, high valuations require support from gross margins and capacity expansion. Customers seeking second sources and geopolitical risks present upward pressure.

- Key Factors:

- Q2 revenue was approximately US$39.6 billion, near the upper end of guidance; June monthly revenue surged 67.9% year-over-year, indicating AI orders are translating into actual revenue.

- Bernstein maintains a NT$2,780 target price, based on roughly 20 times forward P/E. The current stock price of NT$2,440 has already priced in AI dividends in advance.

- Capital expenditure is expected to reach US$56 billion in 2026 and US$68 billion in 2027. CoWoS capacity is projected to increase to 195,000 wafers per month by the end of 2027, focusing on resolving AI capacity bottlenecks.

- The market is focused on the July 16 earnings call: whether gross margins can remain high, the progress of the N2 process ramp-up, and the impact of intensive investment on profit margins.

- Competitive risks arise from customers seeking second sources (e.g., Samsung, Intel). While unlikely to challenge TSMC's leading position in the short term, this could weaken pricing flexibility.

TL;DR

- TSMC's Q2 revenue was approximately NT$1.27 trillion, with June figures up 67.9% year-over-year, indicating AI demand is still materializing.

- Bernstein maintains a target price of NT$2,780, modeling high capital expenditure to secure more AI production capacity.

- The high valuation requires gross margin to keep up; customers seeking second sources and geopolitical risks will continue to cap upside potential.

TSMC's second-quarter revenue reached approximately NT$1.27 trillion, up about 12% quarter-over-quarter and roughly 36% year-over-year, landing within the company's previously provided USD revenue guidance range, near the upper-mid segment. According to TSMC's official monthly revenue report, June revenue alone was NT$442.680 billion, increasing 6.2% from May and surging 67.9% year-over-year.

This data continues to reinforce a key market direction: demand for AI chips, advanced process nodes, and advanced packaging still outstrips supply. Bernstein recently maintained its Outperform rating for TSMC, setting a target price of NT$2,780. Compared to the closing price of NT$2,440 on the Taiwan Stock Exchange on July 13, this target implies further upside. However, investors' focus now shifts beyond single-quarter revenue to production capacity, gross margins, and the ramp-up of the N2 process.

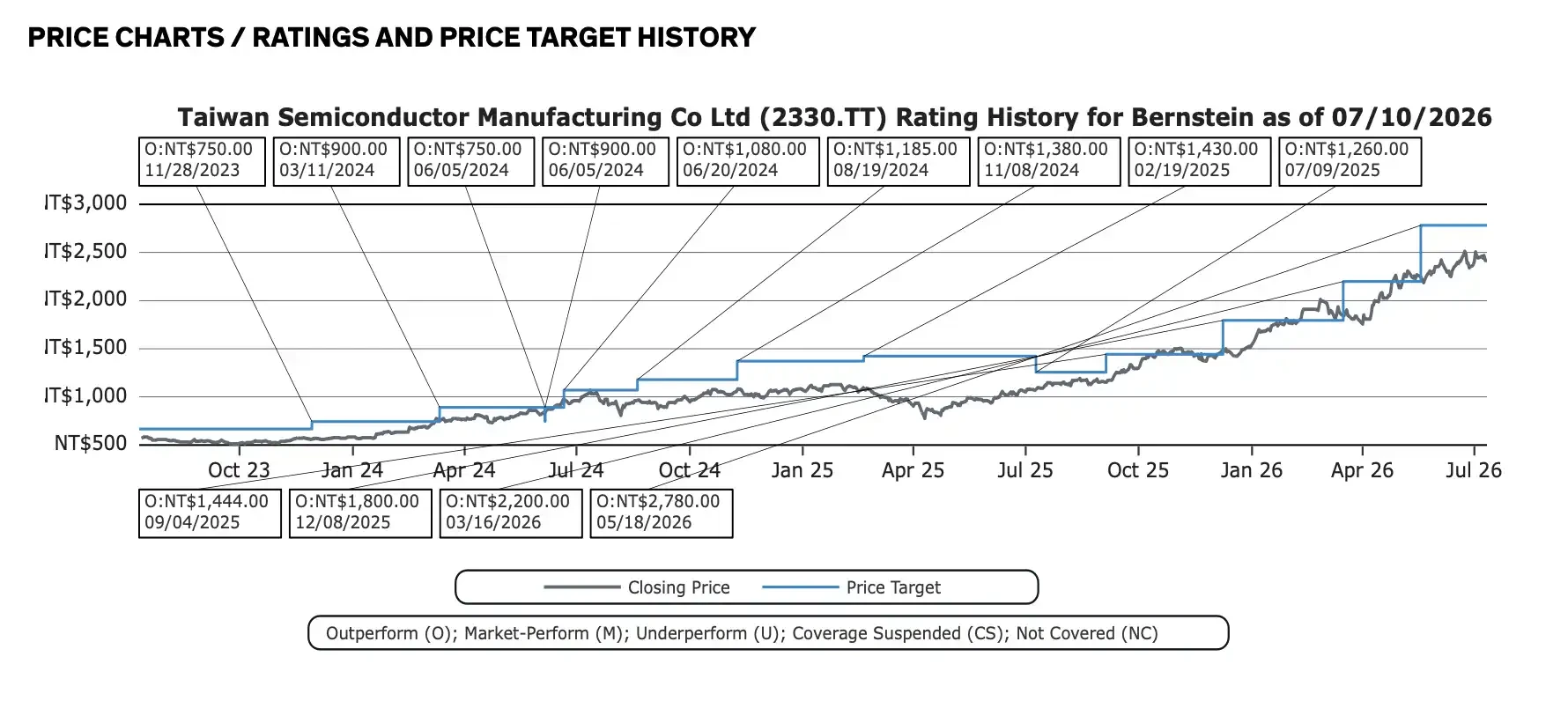

Bernstein has repeatedly raised its TSMC target price

TSMC will hold its Q2 earnings call on July 16. With Q2 revenue already disclosed, the suspense now leans towards how management will update full-year demand, advanced packaging expansion plans, capital expenditure for 2026-2027, and whether the intense investment pressure will start impacting gross margins.

Q2 Revenue Near Upper-Mid of Guidance, June Up Nearly 68% YoY

The Q2 revenue of NT$1.27 trillion is the most direct figure in this report. The company previously guided Q2 USD revenue in the range of $39 billion to $40.2 billion, assuming an exchange rate of 31.7. Based on this, Q2 revenue of approximately $39.6 billion falls within the guidance range, near the upper-mid section.

June's monthly revenue of NT$442.680 billion continued its upward trend from May's NT$416.975 billion. Total first-half revenue reached NT$2.404 trillion, a 35.6% increase year-over-year. This indicates that orders for advanced nodes and AI-related demand are translating into actual revenue, rather than remaining merely as expectations in the capital markets.

Q2 2026 revenue bar chart, actual figure ~NT$1.27 trillion, higher than some market estimates and within the company's guidance range.

Profit margin is another key metric. The source report estimates Q2 gross margin at approximately 65%, but TSMC's official guidance was 65.5% to 67.5%. Before the official earnings release, a safer statement is that the market still expects TSMC's gross margin to remain high, but the final figure will be confirmed in the July 16 report.

For a foundry, maintaining high gross margins depends on the proportion of advanced node revenue, capacity utilization rates, depreciation pressure, and customer pricing power. TSMC's current advantage is that demand from AI and high-performance computing continues to help absorb its higher capital expenditure.

$56 Billion Capex for AI Capacity

Sustaining TSMC's valuation isn't just about how much Q2 revenue beat expectations, but whether it can convert AI demand into deliverable capacity.

Bernstein's model projects TSMC's 2026 capital expenditure at $56 billion, rising further to $68 billion in 2027. This scale reflects dual pressures: increasing demand for advanced nodes, and advanced packaging capacity remaining a bottleneck for AI chip delivery.

Under the source report's framework, CoWoS capacity is expected to reach 135,000 wafers per month by the end of 2026 and 195,000 wafers per month by the end of 2027. For NVIDIA, AMD, and large cloud providers developing custom AI chips, advanced packaging capacity directly impacts timely chip delivery. Even if wafer fabrication is complete, shipments will be constrained if the packaging stage lags behind.

This is why the market will closely watch TSMC's capital expenditure guidance. High capex indicates strong demand, but it also brings higher depreciation and cash flow pressure. As long as customers are willing to lock in capacity and advanced node prices remain firm, high investment is growth investment. If AI demand slows, high capex could conversely squeeze profit margins.

The N2 process will also be a key focus during the earnings call. TSMC's lead in advanced processes remains its primary moat distinguishing it from other foundries. The market seeks confirmation that the N2 ramp is on schedule, customer adoption is proceeding smoothly, and the cost pressures of the new process can be offset by pricing and scale.

NT$2,780 Target Price Isn't Low; Stock Has Priced in AI

As of July 13, 2026, TSMC's stock closed at NT$2,440 on the Taiwan Stock Exchange. The NT$2,780 target price from Bernstein, based on approximately 20 times forward P/E, still implies some upside potential.

However, this is no longer a low-valuation turnaround story. Under the source report's metric, the current stock price corresponds to a P/E ratio of about 21 times forward earnings. The market has already paid a premium price for anticipated AI demand, advanced process leadership, and high gross margins.

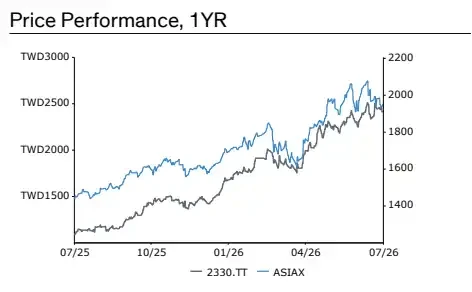

TSMC's stock price has been steadily rising over the past year, currently around NT$2,440, with a TTM relative performance of 86.5%.

Future stock performance will depend more on actual earnings delivery. As long as revenue, gross margins, and capacity expansion continue to beat expectations, the high valuation can be absorbed by profit growth. If capital expenditure continues to rise but profit margins start to loosen, investor tolerance for the current valuation will wane.

Over the past 12 months, TSMC has achieved a relative performance of 86.5%. The market has already positioned it as one of the most core beneficiaries of AI infrastructure expansion. However, the more core an asset is, the more susceptible it is to valuation pressure when expectations cool slightly.

Second Sourcing Heats Up, But Can't Replace TSMC Yet

The immediate competitive risk isn't TSMC's leading position being challenged, but rather customers exploring more options amid capacity tightness.

Samsung has recently been reported to be raising prices for some new clients on its 4/5nm and 8nm nodes by approximately 15%, and is in discussions with Anthropic and Meta regarding 2nm AI chip projects. Intel is also being watched by the market for potential involvement in Google TPU supply, though current discussions point more towards advanced packaging or EMIB, which shouldn't be directly equated to wafer foundry orders.

These developments are unlikely to materially impact TSMC's revenue in the short term. TSMC maintains a clear advantage in leading-edge process yields, scale, and customer base. The real signal is that when advanced node and packaging supply remains tight for an extended period, major customers will more actively seek second sourcing.

Even if alternative solutions have limited short-term capacity and long technology validation cycles, they could weaken TSMC's pricing power flexibility in the medium to long term. Geopolitical uncertainties and customer concerns about over-concentrated supply will also sustain the drive for diversification.

For TSMC at its current valuation levels, these risks don't need to immediately impact revenue. If they affect the valuation multiples investors are willing to assign, that alone is enough to cause stock price volatility. The questions for the earnings call on July 16 are also very specific: How fast will advanced packaging need to expand? Will the N2 ramp-up drag down gross margins? Can high capital expenditure continue to be absorbed by AI orders? TSMC remains one of the strongest companies in the AI manufacturing chain, but realizing the NT$2,780 target price requires more capacity and margin data to catch up.