Goldman Sachs Calls for Going Long on China AI: Behind a $4 Trillion Market Cap, Global Funds Have Only Allocated 1.2%

- Core Thesis: Goldman Sachs recommends going long on the China AI value chain. The core logic lies in a significant mismatch between China's AI assets, which have a market cap of approximately $4 trillion and account for 16% of global revenue, and the allocation of global mutual funds, which have only a 1.2% exposure to Chinese tech. This presents an opportunity for repricing.

- Key Factors:

- Under-Allocation: China AI contributes approximately 16% of global revenues, yet global funds have only a 1.2% allocation to China within their tech exposure, forming the core trading driver.

- Hardware Dominance: This trade differs from traditional Chinese internet plays, covering hardware sectors such as power, semiconductors, and AI infrastructure, the value of which is not fully reflected.

- Policy Support: China is preparing a five-year plan involving approximately 2 trillion RMB (around $295 billion) to build a nationwide AI data center network, directly boosting hardware demand.

- Industry Data: YMTC's Q1 2026 revenue surged 445% year-on-year, with its global NAND market share rising to 13%, indicating the hardware chain is shifting from concept to actual revenue and capacity expansion.

- Risk Note: The trading recommendation relies on policy execution, corporate capacity expansion, and earnings improvement, while US AI remains the primary benchmark for global capital flows.

TL;DR

- Goldman Sachs recommends buying a China AI value chain basket, covering power, semiconductors, AI infrastructure, models, and applications.

- Goldman Sachs estimates that the total market capitalization of China’s AI-related companies is approximately $4 trillion, contributing about 16% of global AI-related revenue. Yet, as of January 2026, global mutual funds had only allocated about 1.2% of their global tech exposure to China.

- The core of this trade is not a single AI application breakout, but a revaluation opportunity driven by underallocated capital, policy investment, and hardware demand.

- Risks include the need for continued delivery on data center investment, storage capacity expansion, IPO financing, and AI hardware exports.

Goldman Sachs’ thematic research team is pushing the "China AI Value Chain" to the center of trading focus.

According to their report titled "Trading Strategy: Long China AI Value Chain," Goldman Sachs recommends a long position in a China AI basket encompassing power, semiconductors, AI infrastructure, models, and applications. Over the past two years, global AI trades have been dominated by large-cap US tech stocks, the NVIDIA ecosystem, and cloud capital expenditure. Now, Goldman Sachs is eyeing the misalignment between the market cap, revenue contribution, and global fund positioning of Chinese AI assets.

By Goldman Sachs’ estimates, China’s AI-related companies have a combined market cap of about $4 trillion and contribute roughly 16% of global AI-related revenue. However, as of January 2026, global mutual fund managers had allocated only about 1.2% of their global tech exposure to China.

This set of figures forms the core investment thesis of the entire report: if China's AI industry already commands a double-digit share of global revenue, but global capital allocation remains significantly underweight, then there is room for repricing within the China AI value chain.

The Biggest Contradiction: Significant Revenue Contribution, Minimal Global Capital Allocation

Goldman Sachs’ breakdown of global AI assets provides a stark comparison.

Since the end of 2022, global AI-related stocks have created approximately $34 trillion in market capitalization, of which China’s AI-related market cap is around $4 trillion, representing about 10% of the global AI market cap. In terms of revenue, China contributes about 16% of global AI-related revenue.

However, capital allocation is far below this ratio. Goldman Sachs estimates that as of January 2026, global mutual fund managers had allocated only about 1.2% of their global tech exposure to China.

This is the core reason Goldman Sachs advocates for going long on the China AI value chain. US AI assets have been repeatedly bought by global capital, with NVIDIA, cloud vendors, semiconductor equipment, and power infrastructure all incorporated into the AI trade narrative. In contrast, while Chinese AI assets have achieved a certain scale of revenue, they remain under-allocated in global fund portfolios.

In other words, Goldman Sachs isn't betting on a purely narrative-driven "China AI story." Instead, they are betting on a more specific capital allocation gap: revenue contribution is already present, but global holdings haven't caught up.

This Isn't Your Typical KWEB Trade; Hardware and Infrastructure Take Priority

Goldman Sachs specifically emphasizes that this trade differs from the traditional KWEB trade.

KWEB typically corresponds to exposure to Chinese internet and platform economies, leading investors to think of e-commerce, advertising, online entertainment, and local services. However, Goldman Sachs has constructed the "GS China AI Value Chain" (GSXACART) basket, which ranges from power and semiconductors to AI infrastructure, models, and applications, closely resembling a complete Chinese AI supply chain.

Within this framework, hardware and infrastructure are positioned higher up.

China's push for technological self-reliance and the development of advanced computing capabilities have brought AI hardware, data centers, power infrastructure, and semiconductors under the simultaneous focus of policy, industry, and capital. Goldman Sachs believes the value of these segments has not yet been fully reflected in the stock market.

Their research estimates that the potential economic benefits of AI through efficiency gains and new profit creation could be 50% to 100% higher than the levels currently priced into AI stocks. This is precisely why power, AI infrastructure, and semiconductors are placed at the core of the basket.

Ultimately, the breakout of models and applications depends on the supply of computing power, storage, electricity, and equipment. And these are precisely the areas where China possesses capabilities in large-scale manufacturing, engineering construction, and industrial supporting chains.

Exports, Policy, and IPOs Are Reinforcing the AI Hardware Narrative

Changes in China's AI hardware chain are moving from concept to more concrete milestones in orders, exports, and financing.

On the demand side, customs data cited by multiple media outlets shows China's May exports grew 19.4% year-on-year, the strongest growth in three months. Within this, integrated circuit exports surged by about 111% year-on-year, while export volumes only saw modest growth. Behind this price and structural shift, AI hardware demand is considered a key driving factor. For storage, semiconductor equipment, and upstream materials, such data points suggest the potential for improvements in orders and capacity utilization.

On the policy investment front, according to Bloomberg News cited by Reuters, China is preparing a five-year plan worth about 2 trillion yuan (approximately $295 billion) to build a national AI data center network. This plan has not yet been officially announced, but if implemented, it would directly stimulate domestic demand for storage chips, semiconductor equipment, power infrastructure, and data center facilities.

On the capital markets side, public reports indicate that A-shares, Hong Kong stocks, and some global indices have increased the weightings of AI and semiconductor companies during their 2026 rebalancings. This will enhance the visibility of related companies for passive funds and direct more domestic and international capital towards advanced computing and semiconductors.

Specific companies and industry cases are also strengthening this narrative. Yangtze Memory Technologies Co. (YMTC) reported a massive ~445% year-on-year revenue increase in Q1 2026. Its global NAND flash market share rose to 13% from 8% a year ago, moving into a tie for fourth place, and it is advancing its domestic IPO plans to support capacity expansion.

ChangXin Memory Technologies (CXMT) is regarded as a critical company in China's DRAM industry. According to third-party research estimates, its 2026 revenue could exceed $50 billion. Based on the company's prospectus, its Q1 revenue was 50.8 billion yuan, and its first-half revenue guidance was 110 billion to 120 billion yuan.

These examples do not mean that Chinese storage companies have fully caught up with overseas giants. However, they illustrate that China's AI hardware chain is transitioning from a "policy concept" to more observable milestones in revenue, market share, financing, and capacity expansion.

Capital is Beginning to Shift; US AI Remains the Primary Benchmark

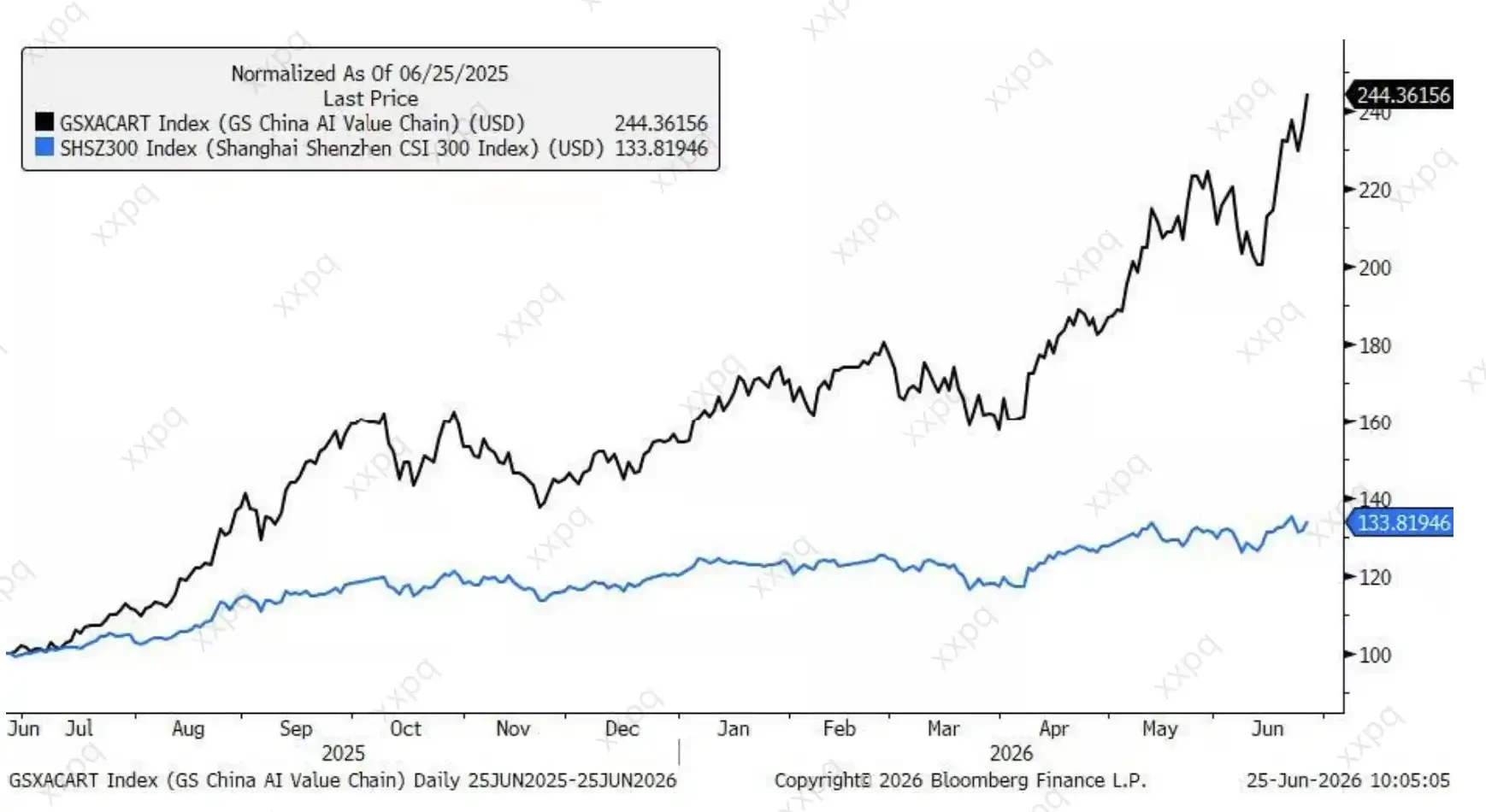

Goldman Sachs also notes that the China AI sector has outperformed other China-related assets, showing signs of capital allocation rotation. However, compared to US AI, the performance of Chinese AI assets still lags significantly.

This is where both the trade's appeal and risk boundaries lie.

The appeal lies in the possibility that if global investors continue to seek growth narratives beyond US AI, China's underweight status could leave room for capital rotation. Especially after US AI leaders have seen high valuations and their capital expenditure expectations are already well-discussed, the market will naturally look for supply chain and application assets that haven't been fully accumulated yet.

The risk is that this remains a trading recommendation, not an already realized industrial conclusion. The 2 trillion yuan AI data center plan depends on policy details and actual execution. The listings, capacity expansions, and profitability improvements of companies like CXMT and YMTC will also take time. The sustainability of chip export and sales data will depend on the global AI hardware cycle and trade environment.

US AI remains the primary benchmark for global capital. Whether in model capabilities, cloud vendor capital expenditure, the GPU ecosystem, or enterprise application revenue, the US market still possesses more mature yardsticks. For Chinese AI to attract more global capital, it must not only prove it is "cheap and under-owned," but also consistently deliver revenue, profit, and technological progress.

The significance of Goldman Sachs’ long position on the China AI value chain isn't about declaring that China's AI has caught up with the US. It's about bringing a market dislocation to the forefront: approximately $4 trillion in market cap and ~16% of global revenue contribution, juxtaposed with only about 1.2% allocation to China in global mutual funds' tech exposure.

Whether capital will fill this gap depends on whether policy investment, hardware demand, and corporate earnings continue to deliver.