In-depth Analysis: Tracing From 1996, Who Is Building the Underlying Infrastructure for the Next Generation of Capital Markets

- Core Thesis: The underlying infrastructure of traditional finance, worth hundreds of trillions of dollars—clearing, settlement, and payment systems—is being reconstructed by blockchain, which is far more transformative than simple asset tokenization. Institutional-grade infrastructure based on the Canton Network is already operational in core markets such as repo, securities settlement, and capital raising. Standardization and network effects are forming, granting first movers a structural advantage.

- Key Elements:

- Real-world cases prove that on-chain finance is no longer an experiment: Broadridge DLR processes $7.7 trillion in repo transactions monthly; the Hong Kong government issued HK$6 billion in digital bonds via HSBC Orion, which were immediately used as repo collateral.

- On-chain infrastructure addresses structural inefficiencies in traditional finance: eliminating counterparty risk and settlement delays through atomic settlement and DvP; slashing massive reconciliation costs via a shared ledger.

- The core prerequisites for institutional participation are simultaneously achieving transaction-level privacy, atomic settlement interoperability, and a permissioned public structure. The Canton Network achieves this design through the Daml language and subnet architecture.

- The Basel Committee on Banking Supervision classifies assets from permissionless chains as Group 2 (1250% risk weight), while Canton's permissioned structure meets Group 1 requirements, allowing regulated banks to compliantly hold tokenized assets.

- Clear signs of market acceleration: on-chain issued assets have reached $34 billion (20x growth in 5 years); core infrastructure providers like DTCC and LSEG have obtained regulatory approval and begun migration; regulatory and institutional deployment in Asia (South Korea, Japan, Hong Kong) is progressing simultaneously.

Introduction: The Submerged Part of the Iceberg

This article is from Tiger Research. What the market calls asset tokenization is just the visible tip of the iceberg. The real transformation is happening beneath the surface, where the multi-trillion-dollar traditional financial infrastructure rails are being fundamentally rebuilt.

Many observers equate tokenizing U.S. Treasury bonds with the entire RWA market, seeing only the surface layer. The true transformation lies not in the visible part of asset digitization but in the comprehensive rebuilding of the financial infrastructure that has long been submerged – the underlying rails supporting every transaction: clearing systems, settlement layers, and liquidity networks.

The scale is already undeniable. According to Broadridge, its DLR platform processes approximately $7.7 trillion in on-chain repo transactions monthly; the DTCC has also entered the Treasury tokenization space. Neither is a pilot experiment; they are operational components of the financial market structure. The Hong Kong government issued HKD 6 billion in digital green bonds via HSBC Orion, immediately deploying them as repo collateral, demonstrating a future where issuance and circulation merge into a single, uninterrupted process.

The infrastructure layer for new financial standards is being assembled right now. Institutions joining in this moment will participate in defining the very architecture before latecomers arrive.

1. 1996's Internet and the RWA Market

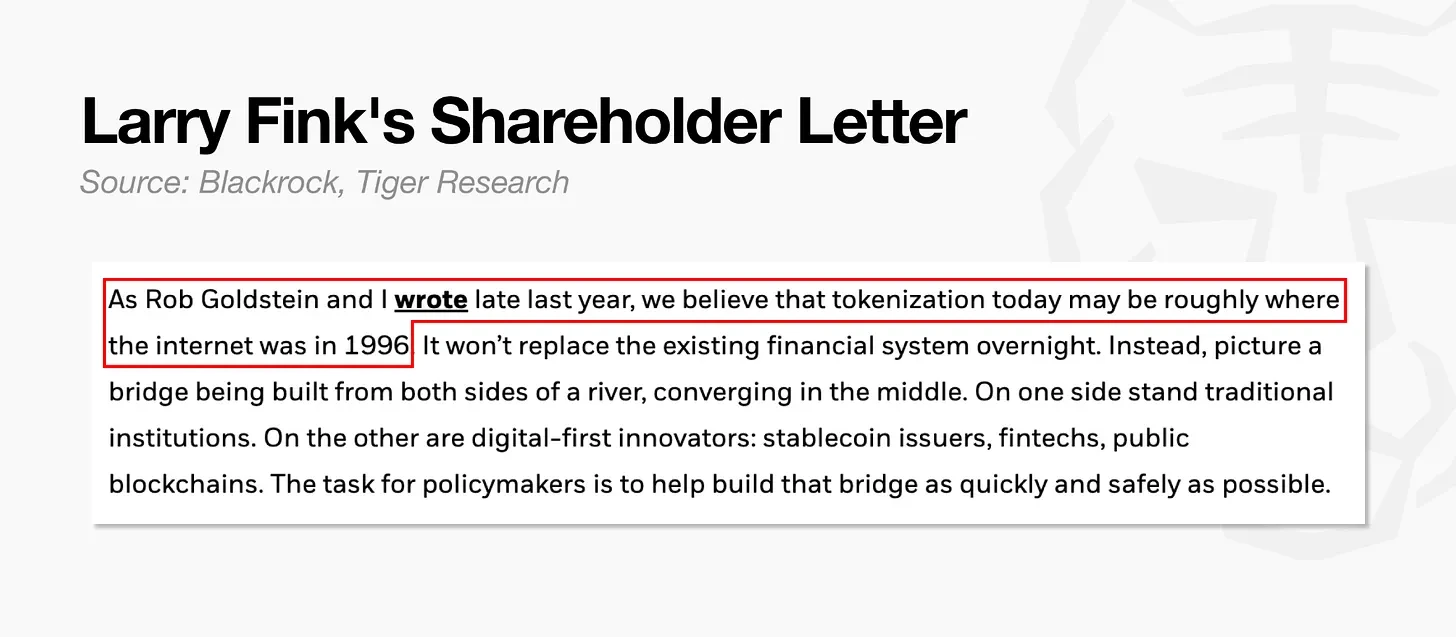

BlackRock CEO Larry Fink wrote in his 2026 annual shareholder letter: "We believe tokenization today is roughly where the internet was in 1996."

1996 was an inflection point. The internet existed, but most businesses held back. Only 26% of Fortune 500 companies had integrated online operations at the time. When early adopters demonstrated success, others rushed in, but by then the pioneers had already secured their positions.

The RWA tokenization market is at a similar juncture. Many institutions are still waiting on the sidelines, but leading cases have already emerged. The most prominent is BlackRock's BUIDL (BlackRock USD Institutional Digital Liquidity Fund), an on-chain tokenized fund holding U.S. Treasuries. Launched in March 2024, it expanded to seven blockchains within 18 months. According to rwa.xyz data, the fund's market capitalization grew to approximately $2.5 billion.

Scale alone doesn't capture this shift. The market has moved beyond simply putting real-world Treasuries on-chain. New financial services are stacking layers on top of issued assets. Multiple DeFi protocols use BUIDL as a base asset, and Binance officially accepts BUIDL as trading collateral.

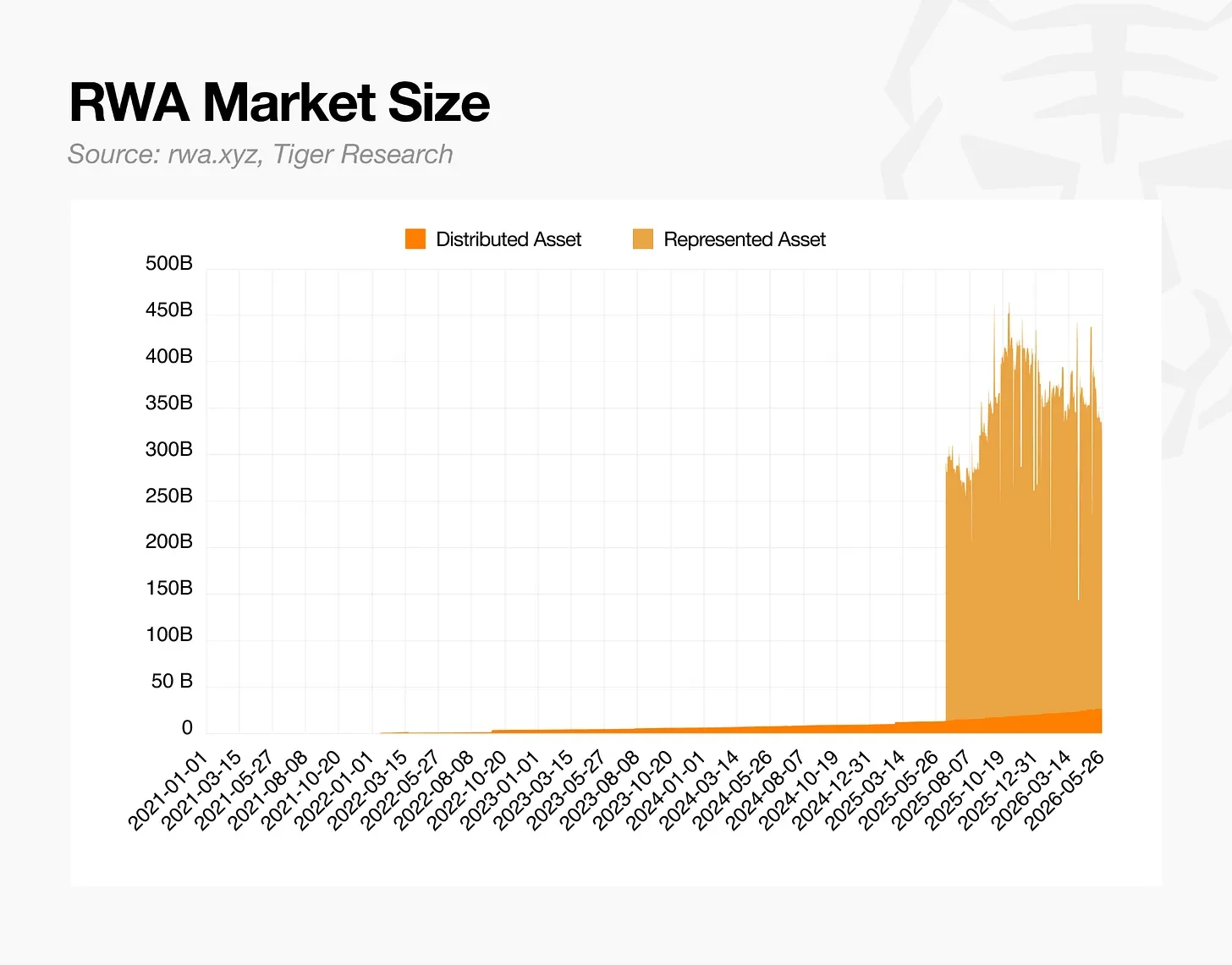

According to rwa.xyz, as of May 2026, on-chain issued assets (Distributed Assets) totaled approximately $34 billion, over 20 times the $1.5 billion seen in early 2020. When including Represented Assets—where physical assets are custodied and ownership recorded on-chain—the total reaches around $360 billion.

2. The RWA Market Has Launched

Asset tokenization isn't just converting existing financial products into digital form. It changes the underlying way products operate, including settlement speed, post-trade infrastructure, and the entire end-to-end processing flow. This approach doesn't aim to replace old systems but to build faster, more precise new rails on top of them.

Most discussions about RWA tokenization stop at BlackRock's BUIDL. BUIDL is indeed a landmark case for the RWA market, but a single example can't answer why tokenization matters.

Finance is far more than bond issuance. Repo markets, securities settlement, and capital raising each carry their own structural inefficiencies, and the value tokenization can unlock varies accordingly. To understand why tokenization matters, these sub-markets need to be examined individually within their respective contexts.

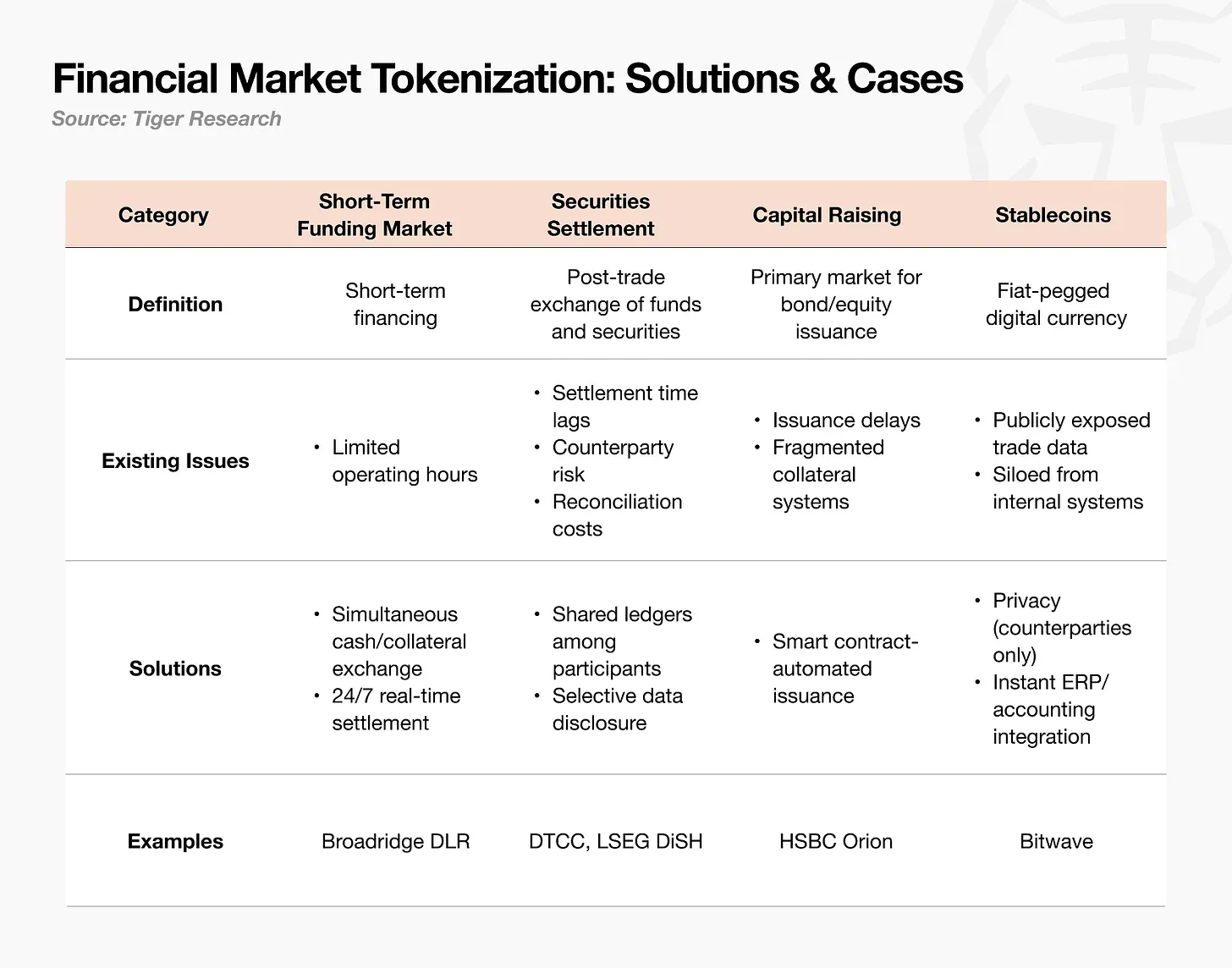

2.1 Short-Term Funding Market (Repo)

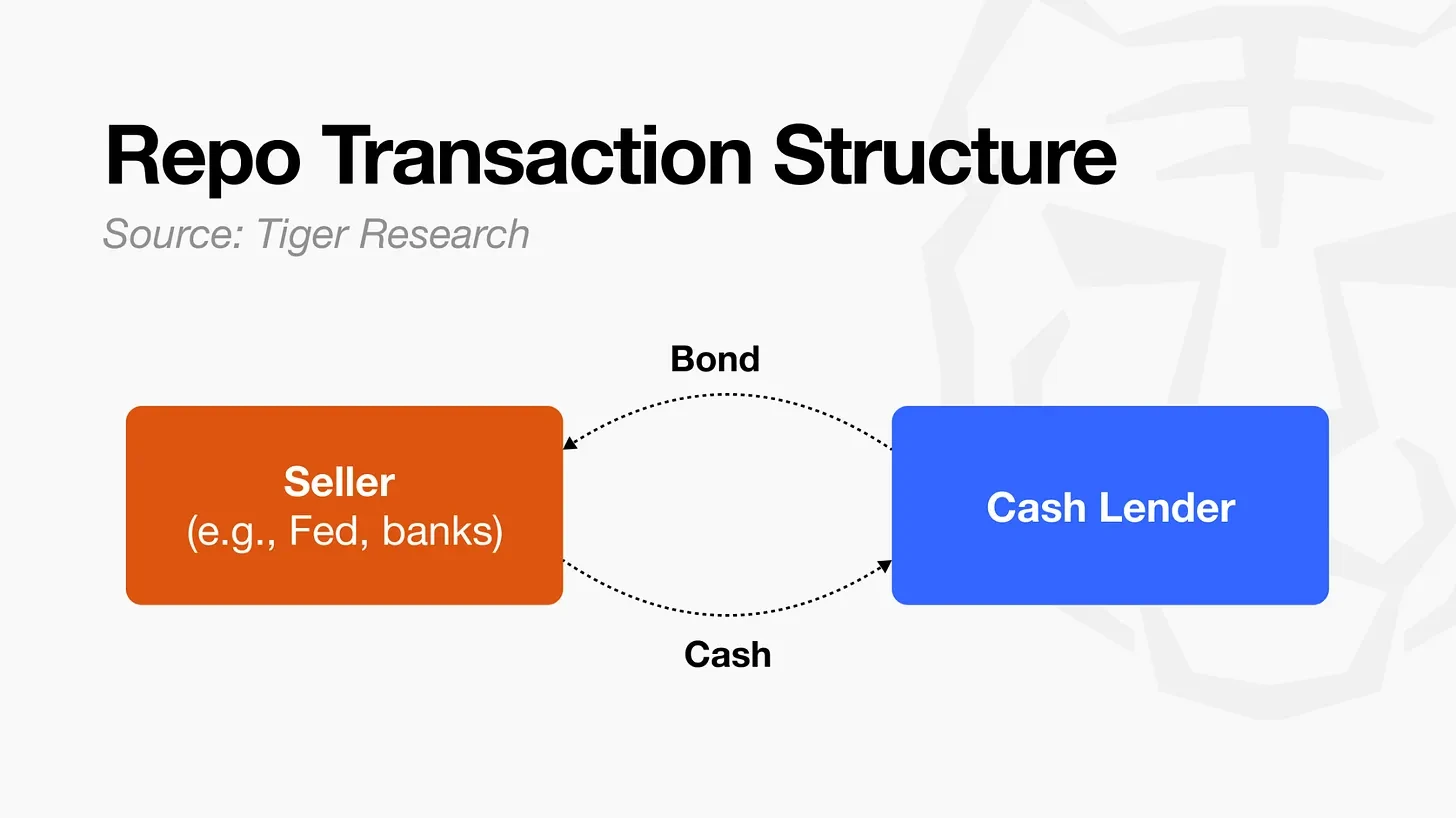

A repurchase agreement (repo) is the defining transaction of the short-term funding market. An institution lends cash against bonds as collateral, agreeing to repurchase the bonds at maturity by repaying principal plus interest. Most contracts are overnight, collateral is safe, interest rates are low, and the transactions are routine.

Problem: Limited Operating Hours. The repo market operates only during system working hours. Settlement happens once daily on business days and stops entirely on weekends and holidays. But risk doesn't stop. If adverse news emerges over a weekend, mark-to-market losses accumulate while settlement is impossible. When markets open on Monday, the entire weekend's accumulated exposure hits as a single margin call. Responding immediately is unrealistic: selling bonds or raising cash via repo takes time. The only solution is to pre-hold cash reserves, capital that sits idle precisely because the settlement infrastructure cannot function continuously.

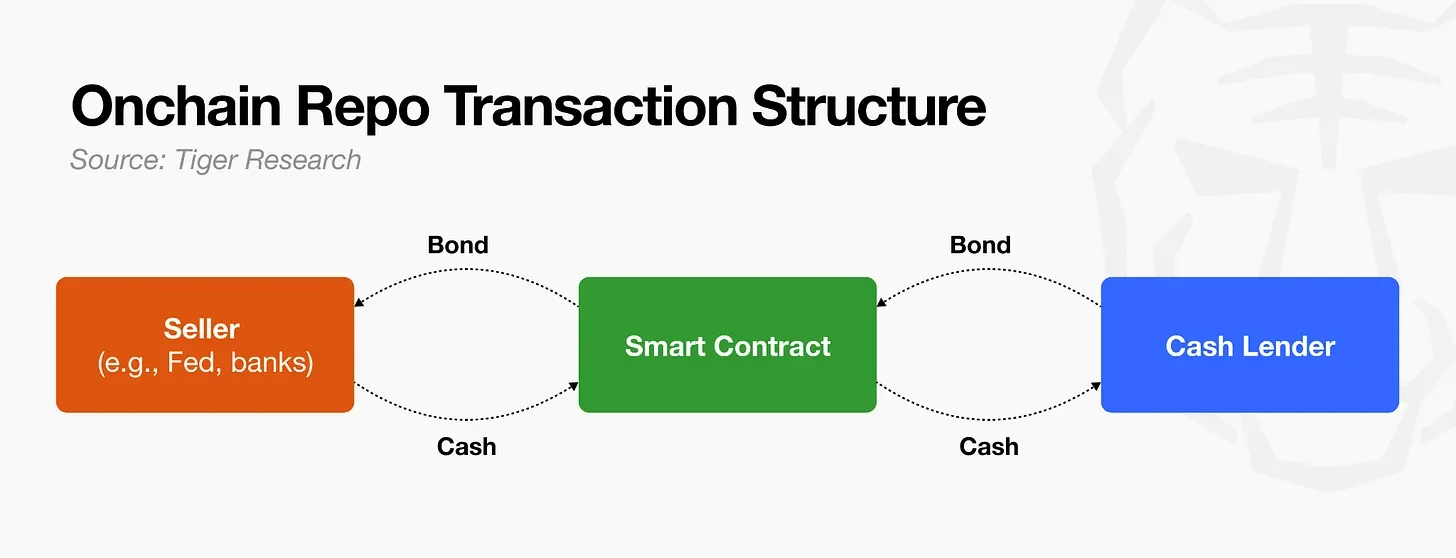

Solution: DvP Mechanism for On-Chain Repo. On-chain repo structurally solves this problem, with the core being the Delivery versus Payment (DvP) mechanism. It works like paying at a checkout counter: collateral and cash are exchanged simultaneously, making it structurally impossible for one party to transfer first.

In practice, the party seeking funds posts the amount, interest rate, and maturity conditions; a counterparty accepts. Both parties deposit their assets into a smart contract—a digital agreement that executes automatically when conditions are met. The borrower deposits tokenized bonds, the lender deposits tokenized cash. Once both confirm receipt, the exchange completes automatically.

Tokenized bonds and stablecoins move on-chain 24/7. Since they don't rely on old settlement infrastructure, collateral can move on Friday afternoon or Sunday morning, eliminating the constraint of system operating hours. Settlement frequency also changes. Manual confirmation under the old system limits settlement to once daily; smart contracts automatically trigger margin calls and settlement the moment a position incurs a loss. Without time gaps, there is no need to pre-position excess cash reserves.

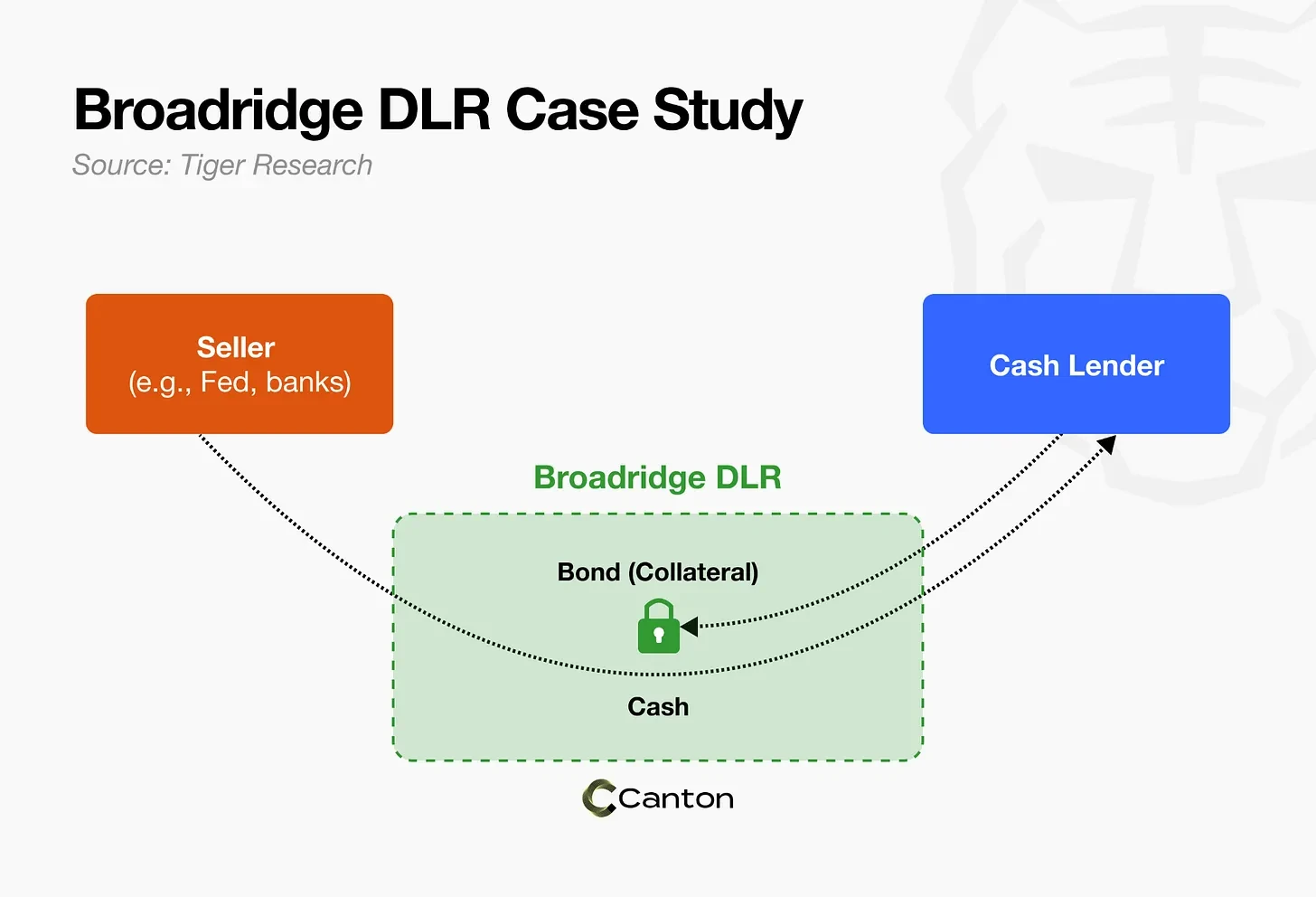

Case Study: Broadridge DLR.

Broadridge is a global capital markets infrastructure company that processes settlement and clearing for banks and brokerages via technology. Its DLR (Distributed Ledger Repo) is a distributed ledger repo trading platform built on the Canton Network's underlying blockchain.

Because it's blockchain-based, DLR is not subject to the operating hour constraints of legacy settlement infrastructure. Collateral moves and settles on weekends and public holidays. Repo transactions can be initiated and closed at any time of day, structurally mitigating the risks stemming from limited operating hours. Smart contracts also automate the entire repo lifecycle, reducing settlement failures and disputes while improving collateral reuse efficiency.

As of April 2026, DLR processed $7.7 trillion in monthly settlement volume, with an average daily volume of $368 billion. Global banks including HSBC, UBS, and Societe Generale participate on the platform.

2.2 Securities Settlement Infrastructure

Securities settlement is the post-trade execution phase where the buyer delivers funds and the seller delivers securities. T stands for trade date. Standard practice settles on T+1 or T+2, meaning funds move at least one to two days after the trade.

Problem 1: Settlement Lag and Counterparty Risk. A real estate transaction is a useful analogy. Signing a purchase contract doesn't immediately transfer title or complete the final payment; that happens days later. The trade and asset transfer occur at different points in time.

Similarly, existing securities settlement infrastructure creates a time gap between trade execution and asset transfer. If a counterparty defaults within this window, significant losses can occur. Central Counterparty Clearing Houses (CCPs) exist to prevent such events. A CCP interposes itself between buyer and seller, so if one party defaults, the other doesn't bear the loss directly. In the U.S., the NSCC plays this role; in Korea, it's the clearing and settlement division of the Korea Exchange (KRX).

Historically, no CCP has fully defaulted because the systemic consequences of a CCP failure are severe enough that member institutions and governments always intervene beforehand. However, CCPs have been pushed to their limits under extreme market conditions. During Black Monday in 1987, the Hong Kong Futures Exchange Clearing House neared bankruptcy due to massive failed margin calls; the Hong Kong government injected capital and halted trading for four days to resolve the situation. During Lehman Brothers' bankruptcy in 2008 and the Nasdaq clearing crisis in 2018, some loss absorption funds were indeed depleted.

Problem 2: Fragmented Ledgers and Reconciliation Costs. When an equity trade executes, the issuer, custodian, clearing house, and settlement institution each record the transaction in their own separate ledgers. The same trade is entered four times across four institutions. Because these ledgers aren't synchronized in real-time, they need to be matched post-trade using standardized message formats. This process is called reconciliation.

Ledgers don't always match. Each institution processes the same trade at different times, and differences in internal system formats can cause data loss or alteration during message conversion. When records are inconsistent, staff must manually identify and correct discrepancies. While some steps are automated, errors still occur frequently. This is why the personnel and system costs for reconciliation and position discrepancy handling persist. Corporate actions (events affecting company structure or shareholder rights, like dividends, stock splits, M&A) add further complexity, as each institution must independently update its ledger and then re-reconcile, multiplying the workload.

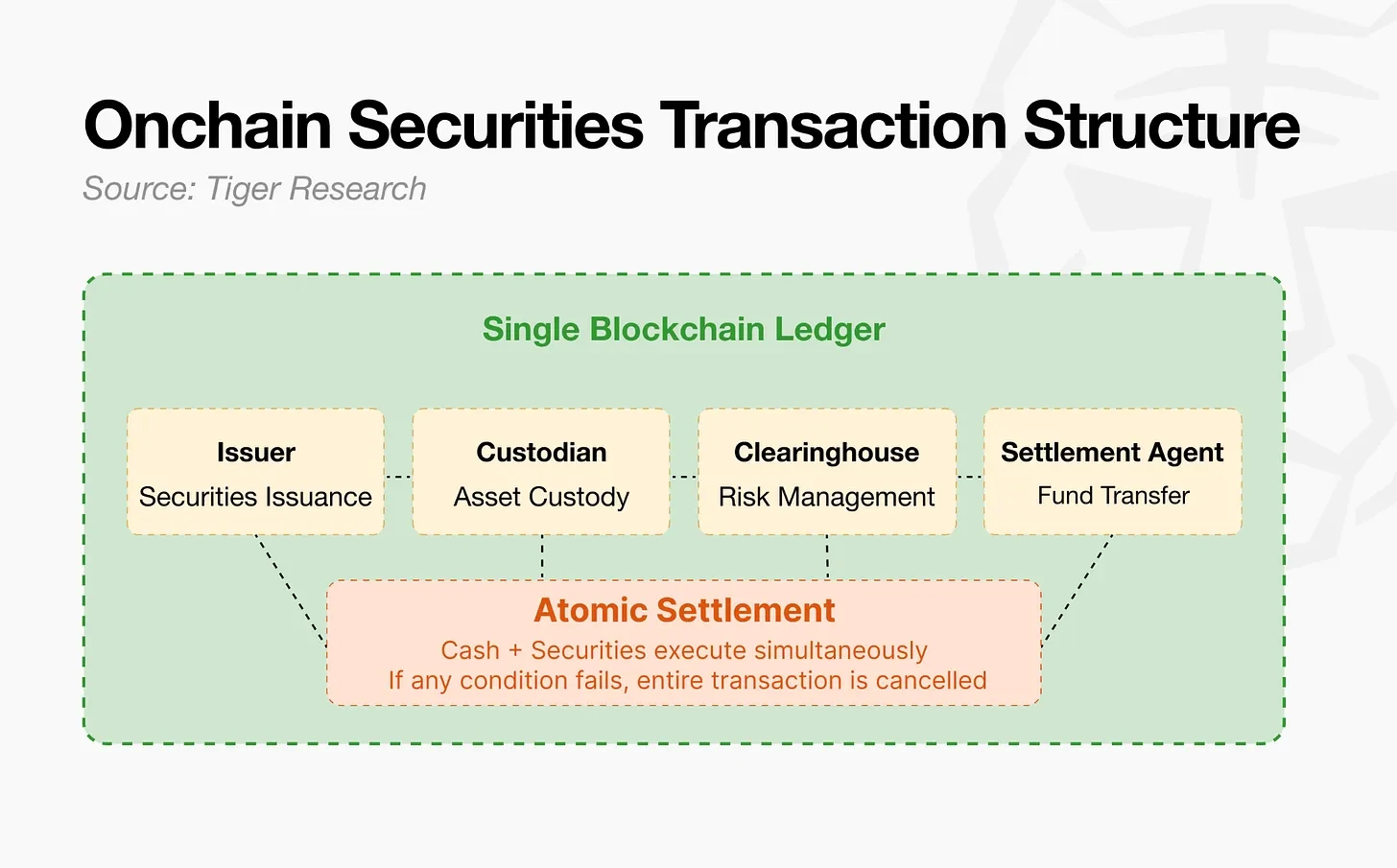

Solution: Shared Ledger + Atomic Settlement. Putting securities settlement infrastructure on-chain changes two things: all participants see the same ledger, and trade execution and asset transfer happen simultaneously.

A shared ledger means each participant's data updates simultaneously when a transaction is recorded, eliminating post-trade reconciliation. Placing cash and securities in the same environment eliminates settlement delays that create counterparty exposure. When both cash and securities are on-chain, trade execution and asset transfer can be bundled into a single transaction. Currently, cash flows through the banking system and securities through central securities depositories, which are separate. On-chain, both exist in the same environment and execute simultaneously.

This is atomic settlement: all conditions must be met for the entire transaction to succeed; if any condition fails, the entire transaction is cancelled.

Case Study: DTCC.

On-chain securities settlement is already running in live trading. The London Stock Exchange Group (LSEG) deployed its Digital Settlement House (DiSH) platform on Canton for securities settlement. Lloyds Banking Group completed a transaction using tokenized deposits to purchase tokenized UK gilts, with the entire process from issuance to settlement handled on-chain.

The most significant case is the DTCC. The Depository Trust & Clearing Corporation is the core infrastructure for U.S. securities settlement, handling clearing and settlement for most U.S. tradeable securities. DTCC, in collaboration with Digital Asset (the company behind Canton Network), obtained a no-action letter from the SEC in December 2025 – a pre-commitment from the regulator not to take action on specific activities. The goal is to launch an MVP (Minimum Viable Product) in the first half of 2026.

DTCC is an institution that could have its license revoked for a single settlement failure. Its decision to adopt on-chain infrastructure is by no means a casual experiment. It represents a deliberate judgment: the risks embedded in the current settlement architecture now outweigh the operational risks of migrating to new rails.

2.3 Capital Raising Market

The capital raising market is where governments and companies issue bonds and equity to raise funds. It comprises the primary market (issuance of new securities) and the secondary market (trading and utilization of issued securities among investors). Bonds represent a promise to repay principal plus interest; equity grants holders an ownership stake in the issuing company.

Problem 1: Issuance Process Delays. The longer the preparation period, the more variables accumulate that the issuer cannot control. Hedging costs rise, investor demand may shift, and in the worst case, the entire transaction falls through. Every additional week on the timeline exposes the issuer to another week of market conditions beyond their control.

Problem 2: Fragmented Collateral System. Institutional investors buy assets for yield, but the real challenge comes after. If purchased assets can be deployed in repo, used as collateral, or linked to other transactions, capital can keep working. The smoother these connections, the more transactions a single asset can support, making the asset more valuable from the issuer's perspective.

However, even when counterparties agree on collateral use, executing it is difficult. Collateral transactions require sequential eligibility verification, haircut calculation, and title transfer. Each step involves different institutions whose systems are not interconnected. Staff at each stage must send messages and wait for confirmations. In this structure, there is a vast gap between the sheer volume of issued assets and the volume that can actually be mobilized.

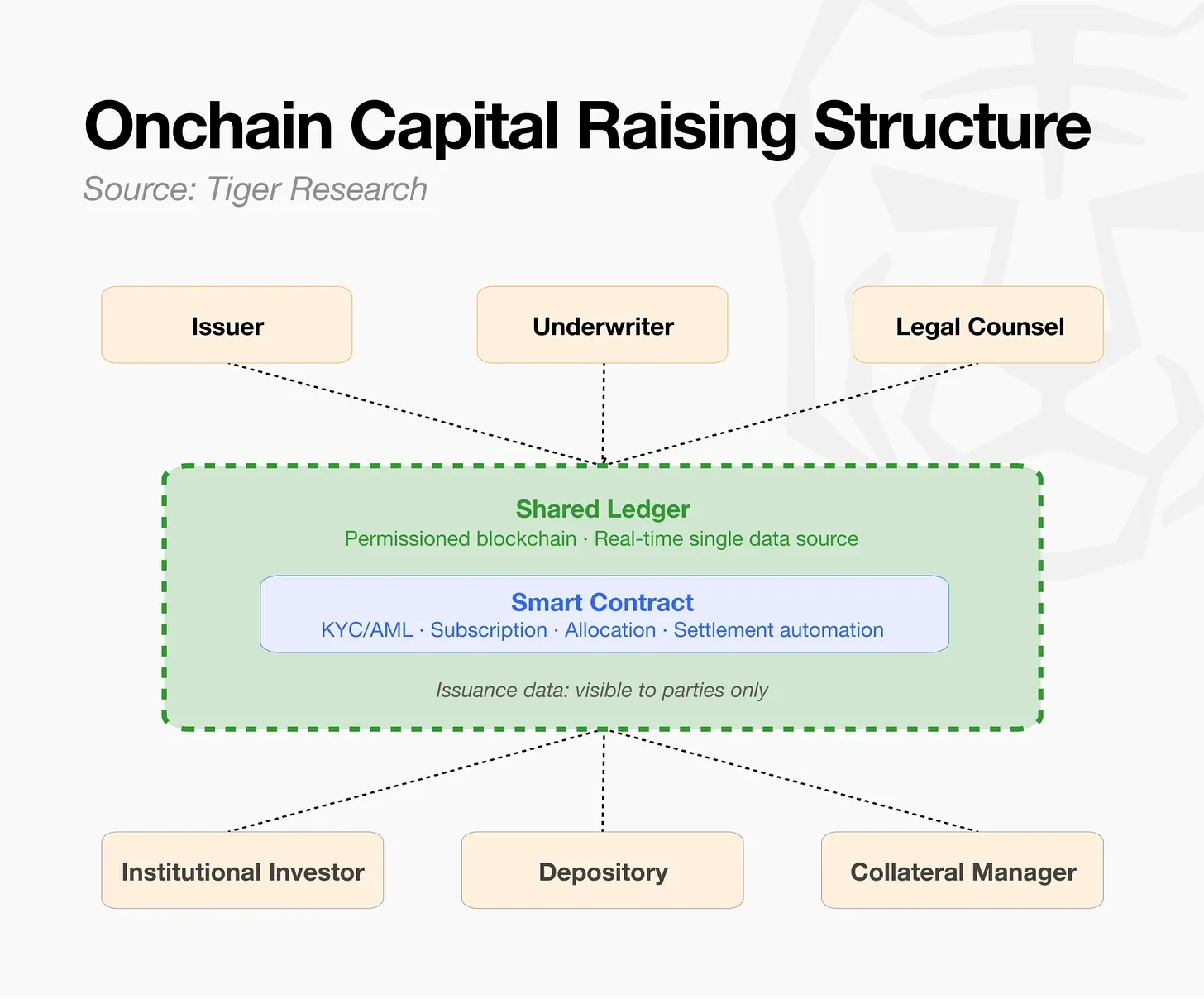

Solution: On-Chain Issuance.

The entire issuance process runs on smart contracts. Within regulatory parameters, agreed issuance terms are defined in code. After KYC and AML verification, subscription registration, allocation, and payment settlement are automated. This eliminates manual confirmation steps and message conversions, significantly compressing the issuance cycle.

The post-issuance utilization structure also changes. Tokenized assets exist in an environment where all participating institutions share the same real-time data on a single network. Eligibility verification, haircut calculation, and title transfer for collateral transactions are handled in a single process, without shuttling between disparate systems. The ledgers previously maintained by the issuer, underwriter, depository, and collateral manager are consolidated into one. Once an asset is issued and adopted, it can immediately serve as collateral or a base asset for other transactions.

This model presupposes issuance privacy. Issuance terms, underwriter allocations, subscription prices, and investor lists are data that cannot be made public. If such information is leaked, market prices move prematurely, and the issuer bears higher costs. Existing public permissionless blockchains only hide wallet addresses but expose all transaction data to everyone. For on-chain issuance to scale, it must run on permissioned infrastructure where transaction data is visible only to relevant parties.

Case Study: HSBC Orion. HSBC is a UK-headquartered global bank with $3 trillion in assets and a leader in bond underwriting and issuance. It launched its own digital asset platform, HSBC Orion, in 2023 as a digital bond issuance infrastructure. HSBC Orion runs on the Canton Network.

In February 2024, the Hong Kong government issued HKD 6 billion (approximately $770 million) in digital green bonds via HSBC Orion. This was the first multi-currency digital bond issued by a government, covering HKD, offshore RMB, EUR, and USD. Over 50 global investors from eight nationalities participated, an exceptionally broad base for an early digital bond issuance. The settlement cycle was compressed from T+5 to T+1.

The significance of this issuance lies not in the issuance itself, but in what followed. Within days of issuance, HSBC executed a repo transaction with Bank of East Asia (BEA) using the digital green bond as collateral. The moment the bond went live on the market, it was directly put to use as collateral on the same network. This was the first confirmed instance of issuance and utilization connecting seamlessly without interruption.

The structure is as follows: When HSBC Orion issues a digital green bond, it is recorded as a token in the Bond Registry on Canton. When HSBC and BEA execute the repo transaction, another application on the same Canton network uses that token as collateral and settles the payment simultaneously.

The Hong Kong government did not treat this issuance as a one-off event. The Hong Kong Monetary Authority subsequently launched a digital bond subsidy scheme, committing to subsidize half the issuance costs for digital bond issuers, transforming a single experiment into a standard market infrastructure.

2.4 Stablecoins and Payments

Stablecoins are digital currencies pegged 1:1 to the US dollar. Unlike regular cryptocurrencies, their value remains broadly stable, and they function like money circulating on a blockchain. USDC and USDT are the most typical examples.

Problem 1: Completely Public Transaction Data. On public blockchains, all transactions are visible to everyone. Who sent how much to whom and when, and what their balances are, can be instantly retrieved by searching a wallet address on a block explorer. Analyzing a company's stablecoin payment history can reveal unit prices negotiated with counterparties, seasonal revenue patterns, timing of entry into new markets, M&A funding flows, and executive compensation. The efficiency