Bank of America's Latest Analysis: After Three Major Bearish Shocks, the Memory Price Hike Cycle Is Far from "Peaking"

- Core View: The pullback in memory stocks on July 2 stemmed from market doubts over whether the AI memory cycle had peaked. However, a Bank of America report argues that current short-term supply-demand data remains strong, while long-term AI demand realization and supply risks are the key points of market divergence.

- Key Factors:

- Meta's compute leasing, CXMT's entry into the iPhone supply chain, and Korea's 800 trillion won investment plan are the three bearish clues that triggered market concerns. But Bank of America believes these factors are not yet sufficient to prove the cycle has reversed.

- Bank of America confirmed from the supply chain that Meta has not cut orders due to an AI server surplus. Its AI data centers are still actively adopting advanced memory, and capital expenditure continues to expand.

- CXMT's entry into the iPhone supply chain is more likely a bargaining chip for Apple in the short term. Constrained by technology, patents, and certification barriers, it will not change the global mobile DRAM supply-demand structure in the near term.

- Korea's 800 trillion won investment plan is a long-term industry blueprint. It will not release significant new capacity in the next two to three years, thus having a limited impact on the current cycle.

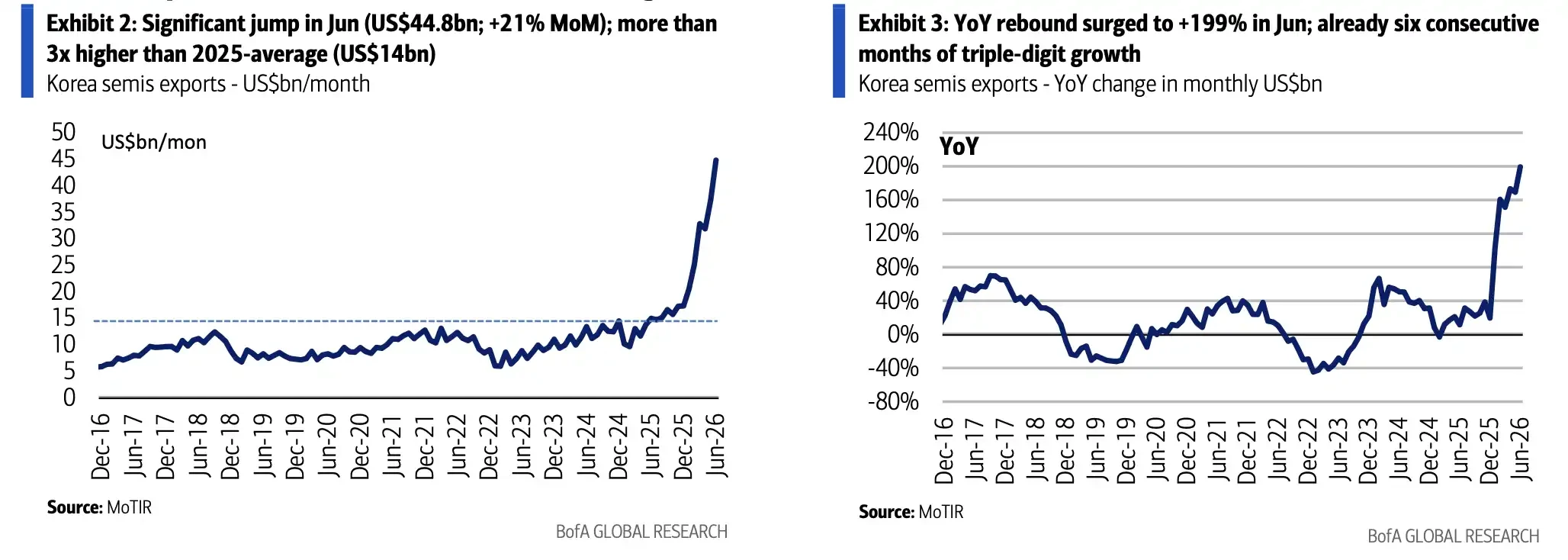

- Current short-term data remains robust: South Korea's semiconductor exports grew 199.5% year-over-year in June. The forecast for DRAM prices in Q3 2026 has been raised to a 13%-18% quarter-over-quarter increase, and spot prices have hit new highs.

- Samsung's preliminary Q2 results (to be released on July 7) will serve as an important window to test memory industry health. If the memory business segment outperforms expectations, it will alleviate market concerns about the cycle's peak.

- Whether AI demand can be sustained after 2027, along with the impact of geopolitics and China's localization process on the supply chain, remains the core point of divergence for long-term market focus.

TL;DR

- After a broad correction in memory stocks on July 2, the market has begun questioning whether the AI-driven memory price upcycle is nearing its peak.

- Bank of America believes that Meta's AI computing rental plans, CXMT's entry into the iPhone supply chain, and South Korea's 800 trillion won investment plan have not yet altered short-term supply-demand dynamics.

- South Korean export data, price forecasts, and cloud capex remain strong, but debate persists over whether AI demand will materialize as expected beyond 2027.

On July 2, AI and semiconductor stocks faced a concentrated selloff, dragging the memory sector down with them. Stocks like SK Hynix, Samsung, Micron, Kioxia, and Western Digital saw notable declines. The market's concern wasn't triggered by a single earnings report but by three bearish signals appearing simultaneously: reports that Meta plans to rent out its AI computing power, news that CXMT (ChangXin Memory Technologies) could enter Apple's iPhone supply chain, and South Korea's announcement of an approximately 800 trillion won semiconductor and memory investment plan. Bank of America's latest memory industry report assesses that while these developments warrant attention, they are not yet sufficient evidence of a reversal in the AI memory cycle.

The central theme of this memory cycle isn't traditional PC or smartphone inventory restocking, but rather the sustained demand from AI data centers for high-end memory such as HBM, LPDDR5, and enterprise SSDs. For the market, the question behind the stock price correction is straightforward: Is AI demand starting to be disproven, and could supply suddenly surge? Bank of America offers a cautiously optimistic view. Short-term price and export data still support an upward memory cycle, but investors are no longer just looking at price increases; they are now questioning how long these increases can last.

Meta's Computing Rental Doesn't Equal AI Order Cuts

The market's most direct concern stems from Meta. According to a Bloomberg Law report, Meta is planning a cloud infrastructure business to sell AI computing power and model access to external customers. Media outlets like Tom's Hardware interpreted this as a source of concern over "excess computing capacity." If Meta were to reduce long-term chip and component orders due to an AI server surplus, demand for HBM, LPDDR5, and enterprise SSDs would be impacted.

Feedback from the chip supply chain, according to Bank of America, does not support this inference. The report states that Meta's AI data centers are still more aggressively adopting advanced memory, with long-term chip and component orders strengthening, and there is no evidence of "order cuts due to server surplus." At least based on current supply chain data, Meta appears to be continuing its expansion of AI infrastructure rather than contracting prematurely.

This explains why memory stocks are so sensitive to rumors about a single customer. AI servers consume far more memory than traditional servers, with HBM used for GPU acceleration, and LPDDR5 and enterprise SSDs required to meet higher bandwidth, lower power consumption, and greater storage performance needs. Once large cloud providers cut capital expenditure, high-end memory prices and order expectations would quickly face pressure. Conversely, as long as hyperscale cloud providers continue to increase spending, short-term supply tightness will be difficult to resolve quickly.

CXMT's iPhone Entry: A Short-Term Bargaining Chip for Apple

The second worry is CXMT potentially entering Apple's iPhone supply chain. If Apple were to adopt CXMT's DRAM on a large scale, the pricing power of Korean and American memory giants in the mobile DRAM market could be weakened, reinforcing expectations of accelerated domestic substitution in China.

However, this impact has significant short-term limitations. Citing Bank of America, public reports suggest that for CXMT to enter Apple's supply chain, it would need to navigate U.S. semiconductor restrictions on China, pass Apple's quality and specification certifications, and overcome potential intellectual property litigation risks. The relevant low-power DRAM must also meet requirements for speed, power consumption, and ECC, while Korean and American companies maintain high technological and patent barriers in advanced mobile DRAM.

Even if Apple experiments with small volumes of CXMT chips in low-end models like the iPhone 18e, actual order volume would likely be limited. Bank of America believes the market demand for low-end models in China is relatively limited, and their contribution to procurement scale would be small. A more realistic impact is that Apple could use this to strengthen its bargaining position with Korean and American manufacturers for contract prices in the second half of 2026 or 2027, rather than immediately changing the global mobile DRAM supply-demand structure.

CxMT's long-term impact cannot be ignored. China's localization efforts will continue to shift procurement choices for some customers. However, for the current cycle, it is not evidence of "sudden supply influx." What the market truly cares about is whether CXMT can consistently pass Apple's quality certifications, how U.S. restrictions will be enforced, and whether its capacity can expand from low-end models to higher-specification products.

South Korea's 800 Trillion Won Plan: Not New Supply for the Next Two Years

The third concern stems from the large-scale semiconductor and memory investment plan announced by the South Korean government. According to information released by South Korea in late June, the plan is worth approximately 800 trillion won, or about $520 billion, involving Samsung, SK Hynix, new fab construction, and HBM capacity expansion. Such a figure can easily be interpreted as a new wave of massive capacity expansion.

However, Bank of America believes this is not a direct supply signal for the current cycle. The report states that the related new clusters and supporting infrastructure are more of a long-term industrial plan. Some projects are still far from actual mass production and will not suddenly release a large amount of new capacity in the next two to three years.

The memory industry has a history where "capex highs correspond to cycle highs," making any large-scale fab plan trigger vigilance. However, current enterprise demand is concentrated on AI-related products like HBM, SOCAMM, and enterprise SSDs, where constraints from advanced process nodes, packaging, yield rates, and customer certification are stronger than for traditional DRAM. Long-term investment plans do not equate to short-term effective supply, especially when high-end memory capacity remains constrained.

Exports and Prices Still Rising, Market Begins Questioning Sustainability

Short-term data still supports the bull case. South Korean official data shows semiconductor exports reached approximately $44.8 billion in June, a year-over-year increase of 199.5%, driven by overall exports of about $102.25 billion, up 70.9% YoY. This data corroborates continued upward memory prices.

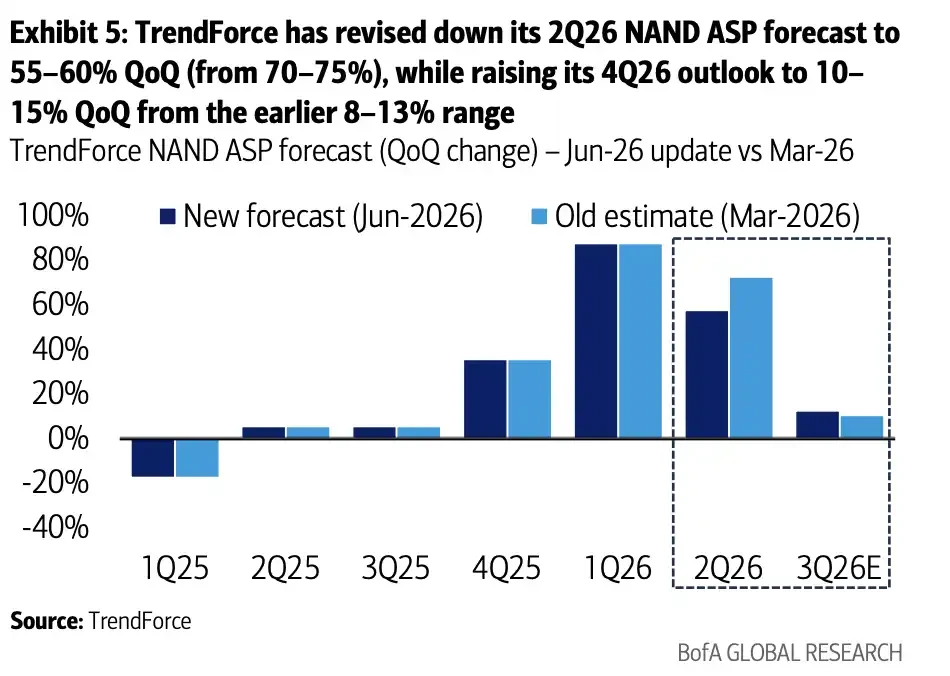

Price forecasts are also strong. In its June update, TrendForce raised its Q3 2026 DRAM ASP forecast to a sequential increase of 13%-18%, up from a previous estimate of 3%-8%. Bank of America's report estimates DRAM price sequential increases of 53%, 17%, and 7% for Q2, Q3, and Q4 2026, respectively, with NAND expected to increase by 65%, 13%, and 1% over the same periods. The two sets of forecasts are broadly aligned for Q3 and Q4, with differences mainly in Q2 timing and some NAND price assumptions.

June semiconductor exports were approximately $44.8 billion, up 199.5% YoY.

The Q3 2026 DRAM price forecast was raised to a sequential increase of 13%-18%.

The spot market also indicates continued supply tightness. According to the Bank of America report, the spot price of 16Gb DDR5 reached a new high of $4.7 in early July, the 16Gb DDR4 price was around $7.5, and 512Gb NAND wafer prices hovered near $2.0. Prices corrected between April and May but rebounded in June. DRAM manufacturers prioritizing HBM production has further constrained traditional DRAM supply.

The higher prices go, the more the market fears a cycle reversal. The current debate is not about whether the memory market is strong in the short term, but whether this strength is already fully reflected in stock prices, and whether AI demand can continue to absorb high prices.

Samsung's Q2 Preliminary Results: A Near-Term Test for Memory Market Health

Samsung is expected to release its preliminary Q2 results on July 7, providing a short-term window for the market to assess memory market health. According to Moneycontrol citing Bloomberg, the market is focused on whether Samsung's operating profit can alleviate concerns about cooling AI trades.

Overall profit may be impacted by factors like special bonuses booked in Q1 and margin pressure from the smartphone business, potentially falling short of some optimistic expectations. However, Bank of America believes that memory division operating profit is likely to exceed market consensus, primarily benefiting from higher ASPs.

This highlights the nuanced situation for memory stocks. Overall company profit can be distorted by phone business, bonuses, and other factors, but the memory business itself remains in a price upswing. If Samsung's memory division performs significantly better than expected, it would reinforce the view that the July 2 selloff was more about sentiment and concentrated worry. Conversely, if price pass-through or margins disappoint, concerns about a cycle peak will continue to escalate.

Valuations do not eliminate risk entirely. Despite significant earnings expansion, memory stocks currently trade at relatively modest P/E ratios, with notably improved ROE. However, given the sector's substantial gains since 2026, the July 2 correction indicates that investors are becoming more sensitive to any potential bearish news.

The Ultimate Debate: AI Capex Post-2027

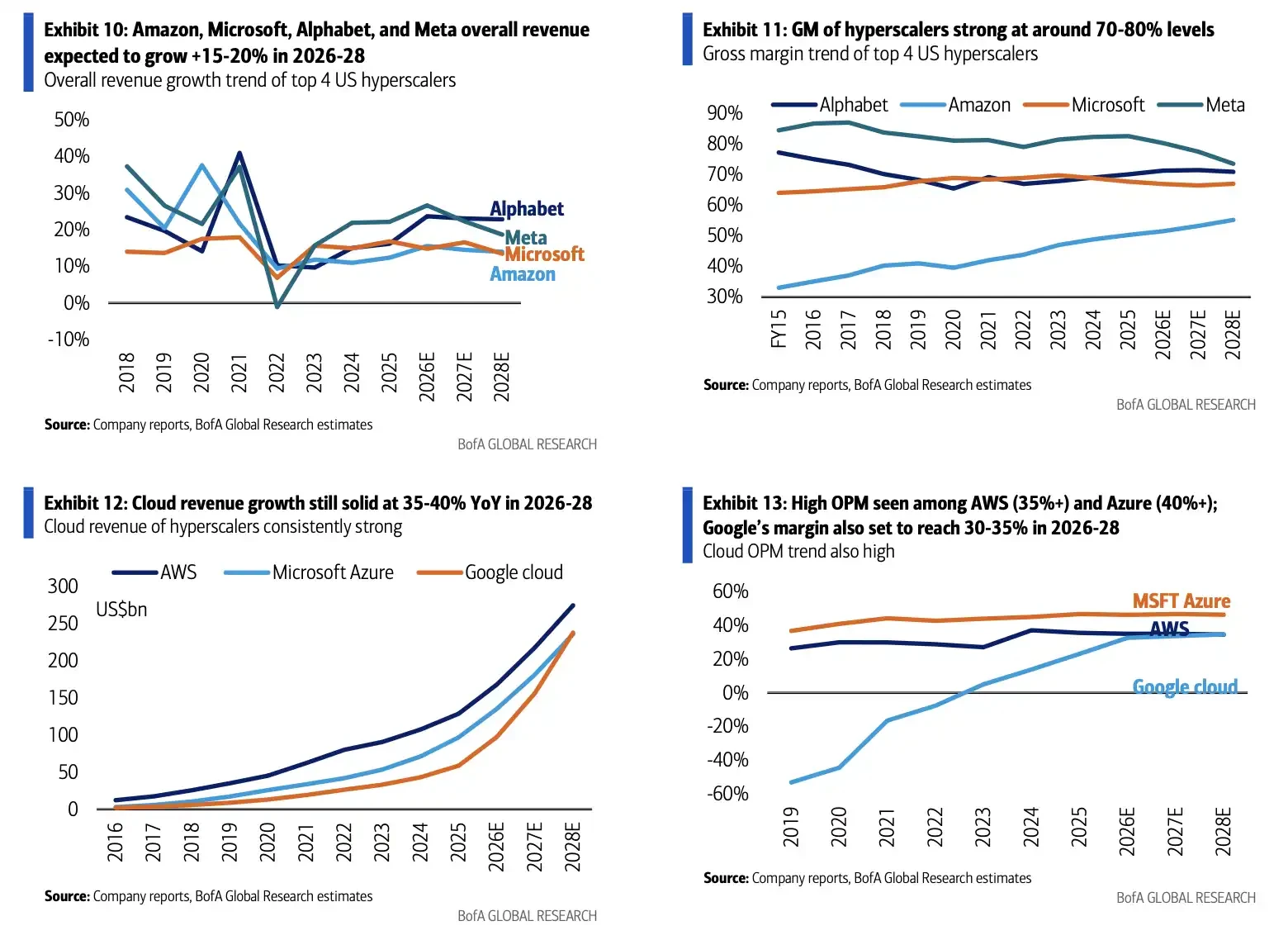

The broader backdrop supporting memory demand is the ongoing expansion of cloud giants' capital expenditure. According to media summaries and analyst estimates, the combined AI-related capital expenditure of major cloud providers like Amazon, Microsoft, Alphabet, and Meta could reach approximately $700 billion in 2026, a significant increase from the previous year, with spending potentially remaining high through 2027-2028. This figure is not an official joint guidance from the four companies, and including companies like Oracle can change the calculation.

Trends in capital expenditure, cloud revenue, and profit margins for major cloud providers. 2026 capex is expected to be around $700 billion, a crucial support for continued high-end memory demand.

Therefore, this correction in memory stocks appears more like the market stress-testing three questions: Is Meta actually cutting back on AI infrastructure investment? Can CXMT transition from a symbolic entry into the Apple supply chain to a scalable substitution threat? Will South Korea's long-term investment plan eventually create a new wave of supply pressure?

Currently, these questions lack answers sufficient to overturn the cycle. Exports, spot prices, price forecasts, and cloud provider capex all point to strong demand. But risks have not disappeared. AI capex needs to continue delivering beyond 2027, geopolitical restrictions could alter supply chain choices, and China's localization process will persistently influence negotiations between Korean/American giants and their customers.

Whether the memory cycle has peaked is not yet a conclusion confirmed by data. More accurately, the market has shifted from a phase of "only looking at price increases" to a phase of "verifying how long the price increases can last."