BiCS-10 Mass Production Success: Kioxia's AI Storage Narrative Enters the Execution Phase, Morgan Stanley Sees 32% Upside

- Core View: Kioxia has commenced production of BiCS-10 (332-layer) 3D NAND and shipped 1Tb TLC samples, demonstrating technological leadership. However, near-term profitability still relies on BiCS-8. The approximate 32% upside to the target price stems from the long-term expectation of this technology translating into market share in AI data center SSDs, rather than short-term volume increases.

- Key Elements:

- BiCS-10 interface speed has increased to 4.8Gb/s (a 33% improvement), bit density is up by 59%, and power efficiency has improved by 18%-30%, primarily targeting enterprise and data center AI SSDs.

- As of March 2027, BiCS-8 is still expected to account for over 80% of Kioxia's shipments, with short-term profit improvement primarily driven by this mature process.

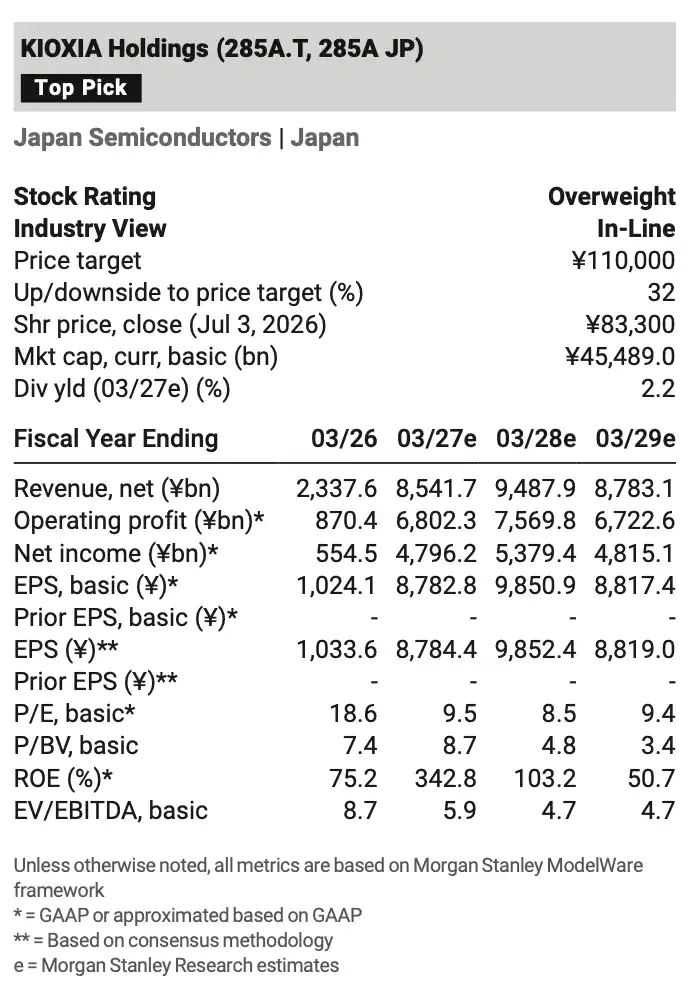

- Morgan Stanley maintains an "Overweight" rating with a target price of approximately 110,000 yen, representing about 32% upside from the current stock price. This valuation is based on a free cash flow yield of approximately 10% for FY2028e.

- Key risks include lengthy customer qualification cycles, yield ramp-up challenges for new processes at the K2 fab, supply disruptions from NAND expansion by Chinese manufacturers, and currency risk from yen appreciation against the US dollar.

TL;DR

- Kioxia and SanDisk have initiated BiCS-10 production at K2 in Kitakami, with 1Tb TLC samples beginning shipment.

- BiCS-10 interface speed increased to 4.8Gb/s, but volume ramp-up will still primarily rely on BiCS-8 until March 2027.

- Target price of approximately 110,000 JPY implies about 32% upside; risks lie in customer qualification, K2 ramp-up, and supply-side disruptions.

Kioxia and SanDisk announced on July 3 that they have commenced production of the 10th generation 3D Flash memory, BiCS-10, at the Kitakami plant Fab2/K2 in Iwate Prefecture, Japan. On the same day, Kioxia began shipping 1Tb TLC BiCS-10 samples, primarily targeting enterprise and data center SSDs.

This move brings Kioxia's AI data center storage roadmap into the pre-production ramp-up phase, though it is not yet a signal of immediate profit realization. Samples are intended for customer functional verification, and mass production specifications are still subject to adjustment. This will be followed by enterprise SSD qualification, product integration, and the K2 factory ramp-up.

Morgan Stanley maintains an "Overweight" rating on Kioxia in its latest report. Based on the report's target price of approximately 110,000 JPY and the July 3 closing price of 83,300 JPY, this implies roughly 32% upside potential. This assessment doesn't rely on short-term volume growth from BiCS-10 but on Kioxia's ability to translate faster interfaces, higher bit density, and lower power consumption into AI data center SSD market share and improved cash flow.

The financial forecast table shows FY2027e revenue of approximately 8.54 trillion JPY and FY2028e revenue of approximately 9.49 trillion JPY, with the profit outlook tied to product mix upgrades.

Interface Boosted to 4.8Gb/s, Kioxia Targets High-Bandwidth AI SSDs

The most immediate change with BiCS-10 is the NAND interface speed increase from 3.6Gb/s in BiCS-8 to 4.8Gb/s, a roughly 33% improvement. For consumer storage, this metric may not be directly apparent, but for enterprise SSDs and AI servers, interface speed impacts data throughput, latency, and cache efficiency.

The 1Tb TLC samples Kioxia is currently shipping are aimed at enterprise and data center SSDs. In its 2026 Investor Day materials, Kioxia positioned the CM Series as "High Bandwidth SSDs with TLC Flash Memory," mentioning compatibility with NVIDIA CMX Servers and optimized KV cache workloads. This indicates that NAND in AI servers is not just for inexpensive, high-capacity storage but also handles data caching and access tasks closer to the compute side.

BiCS-10 is also a 332-layer 3D Flash memory. Compared to BiCS-8, officially disclosed figures show a 59% improvement in bit density, 18% better write power efficiency, and 30% better read power efficiency. Bit density affects output capacity per wafer, while power consumption impacts data center operational costs. Cloud providers ultimately care about cost per TB, SSD performance, and overall system energy consumption.

However, leading technical specifications do not equal commercial success. Enterprise SSDs typically require long qualification cycles, especially for high-performance, low-latency, and AI workload products. BiCS-10 production has started and samples are shipping, but becoming a major source of Kioxia's shipments and profits requires confirmed customer orders.

Short-Term Profits Still Rely on BiCS-8, Not an Immediate Volume Ramp from BiCS-10

What is often overlooked is that Kioxia's cost improvements over the next one to one-and-a-half years will primarily still come from BiCS-8.

Morgan Stanley's model projects that from 2026 to the first half of 2027, the company's output expansion and GB cost reductions will still be driven by BiCS-8. By the end of March 2027, BiCS Gen.8 is expected to account for over 80% of total production by GB. BiCS-10 is more of a starting point for medium-to-long-term product mix upgrades rather than a single catalyst that will immediately change short-term financial results.

This pacing is not contradictory. Transitioning to a new generation of NAND process – from trial production and sample shipping to mass adoption – typically involves production line conversion, yield ramp-up, customer validation, and product portfolio adjustments. The K2 factory has been operational since September 2025, previously producing the 8th generation 3D Flash. As the 10th generation product is introduced, overall capacity will continue to expand, but the income statement will need to catch up with capacity utilization, yields, and customer orders.

Kioxia's medium-to-long-term goal is to increase the proportion of sales to data center and enterprise markets to over 60%. This is where BiCS-10's significance lies: if the new generation of NAND successfully enters high-end enterprise SSDs and gains share in AI server storage, Kioxia's revenue structure will become more tilted towards the enterprise market.

The ~32% Upside Stems from Valuation and Product Mix Execution

The roughly 32% upside potential is not merely a bet on NAND price increases, but combines technology upgrades, data center SSD share gains, and free cash flow improvements.

In terms of valuation, the target price is based on a free cash flow yield of approximately 10% for FY2028e, implying a P/E ratio of about 11x. The model projects FY2027e revenue of approximately 8.54 trillion JPY and FY2028e revenue of approximately 9.49 trillion JPY; basic EPS is estimated at around 8,782.8 JPY and 9,850.9 JPY, respectively. The prerequisite here is that Kioxia can translate its technology upgrades into better product pricing and cost structures amidst demand growth and supply constraints.

The market's willingness to assign a higher valuation to Kioxia partly stems from AI storage demand. Compared to consumer electronics and traditional PC cycles, data center SSDs are more driven by cloud capital expenditure, AI cluster construction, and enterprise storage upgrades. If BiCS-10 penetrates high-end enterprise SSDs, Kioxia's revenue quality and cyclical volatility could improve.

However, this execution chain is long. Technical specifications must first become products. Products must pass customer qualification. Qualification must lead to shipments, which eventually translate into revenue and profit. Any delay in any of these links will impact earnings expectations for 2027 and beyond.

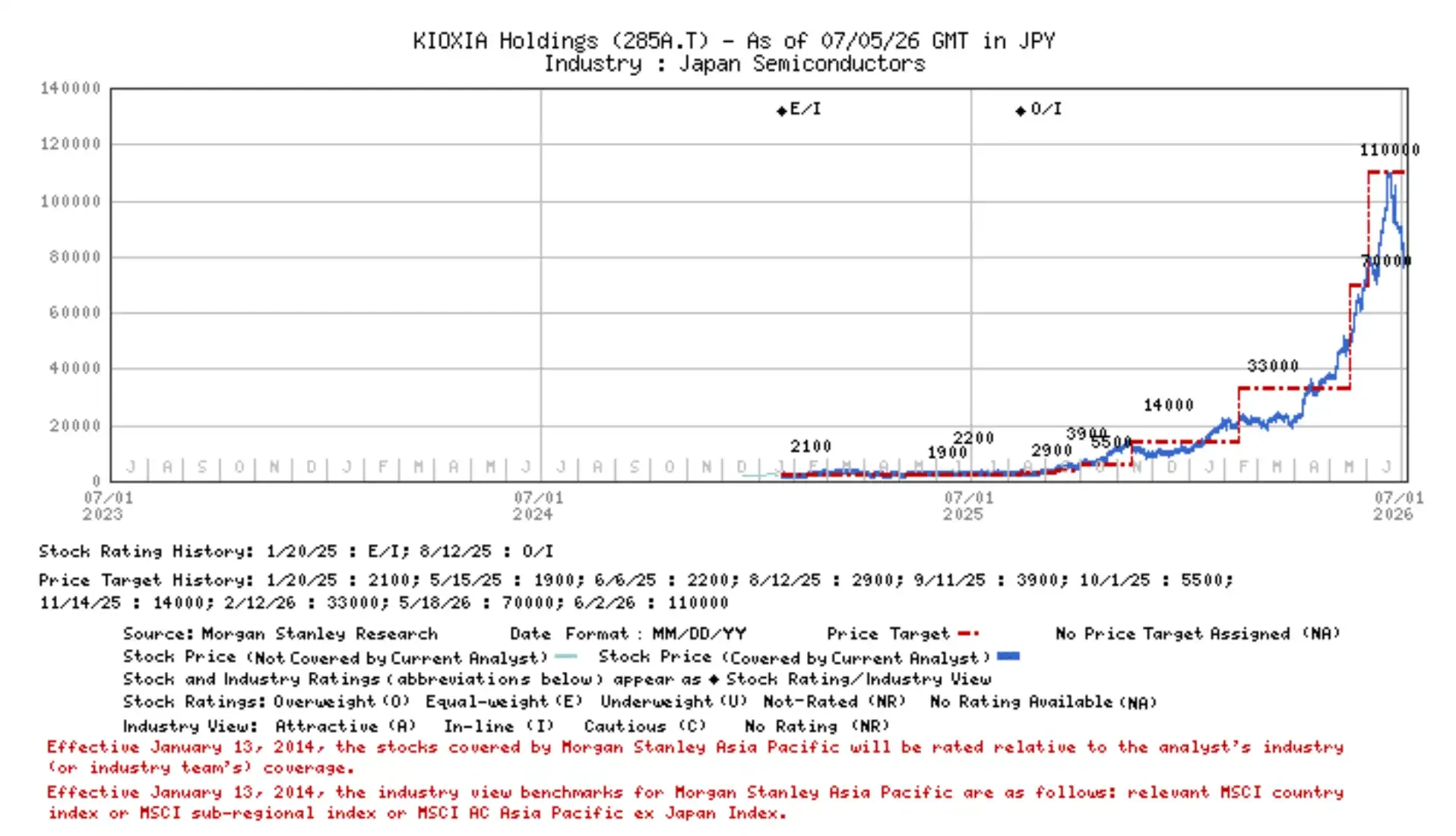

The stock price chart shows Kioxia's share price at approximately 83,300 JPY as of July 3, 2026, with an "Overweight" rating mark superimposed.

Disagreement Lies Not in Technical Specs, but in Ramp-Up and Supply-Demand Dynamics

The direction of BiCS-10 is relatively clear; the real uncertainty lies in execution.

First is customer qualification. Entering the customer systems of cloud vendors and data centers with high-end enterprise SSDs requires meeting performance, reliability, power consumption, and long-term supply requirements. Sample shipment is just the beginning. The qualification timeline and order size will determine when BiCS-10 makes a material contribution to revenue.

Second is the K2 factory ramp-up. Switching to a new process typically impacts yields and the cost curve. Even though the production line has started, increasing capacity utilization takes time. If the ramp-up is slower than expected, BiCS-10's unit cost advantage and bit density benefits will be delayed.

Third is industry supply. NAND capacity expansion by Chinese manufacturers could disrupt global supply-demand balance, especially if demand recovery falls short of expectations. New supply would depress prices and margins. For Kioxia to achieve a higher revenue share from AI SSDs, it still must navigate storage price cycles and shifting competitive dynamics.

Currency exchange rates are also a direct risk. Morgan Stanley's sensitivity analysis shows that for every 1 JPY appreciation against the USD, Kioxia's annual operating profit decreases by approximately 60 billion JPY. For a storage manufacturer with global sales but reporting in JPY, exchange rate fluctuations amplify the uncertainty of earnings predictions.

BiCS-10 is more like Kioxia's ticket to compete in the AI data center SSD market, rather than a victory already realized. Short-term financial results will still depend on BiCS-8's share increase and cost reduction. In the medium-to-long term, the focus will be on BiCS-10 qualification, the K2 ramp-up, and enterprise SSD customer adoption. If these steps proceed smoothly, the ~32% upside potential will be on firmer ground. If any link is delayed, the technology lead will still need confirmation from financial reports.