Neocloud Business Model: Why Is Google Willing to Pay SpaceX $920 Million a Month?

- Core Thesis: The current computing power market faces a severe shortage, making the construction of data centers and the rental of computing power (neocloud model) an exceptionally high-return business. Taking the lease Google pays to SpaceX as an example, the payback period for a 100MW data center under optimistic rental rates is less than one year, and even at conservative prices, it only takes about two years.

- Key Elements:

- Real Lease Data: Google pays SpaceX $920 million per month to lease a data center containing 110,000 GB200 GPUs, translating to $11.6 per GPU per hour.

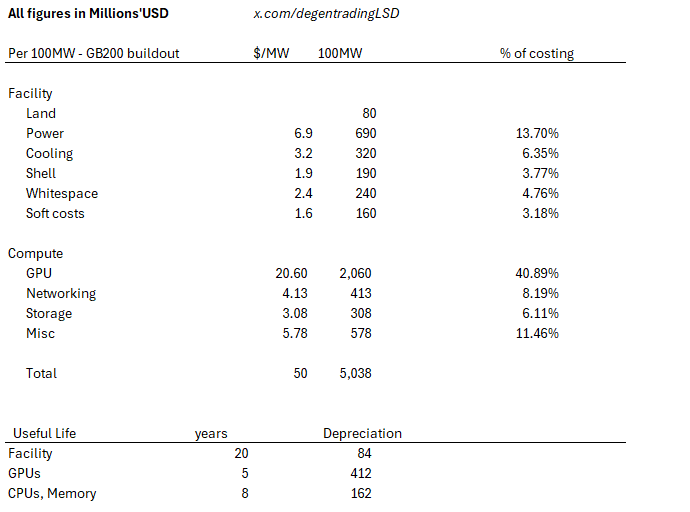

- Construction Cost Estimate: The construction cost of a 100MW data center (configured with GB200 GPUs) is approximately $5 billion, or about $50 billion per GW; using more advanced chips (such as GB300 or Rubin) would increase costs by 20% to 100%.

- Profitability Calculation: A 100MW data center can accommodate approximately 83,333 GB200 GPUs. At a rental rate of $11.6 per hour, the annual revenue would reach as high as $8.467 billion. After deducting electricity, maintenance, and labor costs, the payback period is less than one year.

- Market Pricing Reference: The estimated rental price for long-term contracts is $4 per GPU per hour, while the resale price by hyperscale cloud providers (such as AWS) exceeds $12 per GPU per hour, indicating a huge profit margin in the middle.

- Depreciation Cycle Debate: Although chips like the GB200 may lose value after 5-6 years, analysts believe that against the backdrop of surging inference demand, the GPU depreciation cycle can be extended to approximately 10 years. Older chips like the A100 still have market rental prices today.

Original Author: degentrading

Original Translation: TechFlow

Foreword: Everyone wants to become a neocloud, from xAI and Meta to SoftBank, all jumping into the business of selling compute power. Author degentrading uses a real contract Google paid to SpaceX to work backwards: 110,000 GB200 GPUs, rented at $11.6 per card per hour, a 100MW data center breaks even in less than a year. This article step-by-step breaks down the cost structure and profit model of a neocloud, answering one core question: why building data centers and selling compute is the best business right now.

"xAI has partnered with Google."

"Meta has signaled it is willing to sell its spare compute infrastructure."

"SoftBank plans to provide 10GW of AI compute capacity in the US."

No matter where you look, it seems everyone wants to become a neocloud and start selling compute. Why is that?

Let me walk you through the books of a neocloud, starting with a real-world example.

On June 5, 2026, Google announced it would pay SpaceX $920 million per month to rent compute capacity from xAI's data center.

This compute capacity includes 110,000 NVIDIA GPUs, plus CPUs and other memory components – essentially a fully equipped data center (Colossus 2).

The GPUs in question are NVIDIA GB200 NVL72s.

Based on this amount, the unit price per GPU is $920 million / 110,000 / 720 = $11.6 per hour.

Let's create a hypothetical 100MW data center, packed with GB200s.

Note: Author's estimated build cost for a 100MW data center, roughly $50 billion per GW

My estimate is about $50 billion per GW. This puts the build cost for a 100MW facility at around $5 billion.

This number aligns with industry estimates. Note, this is the build cost for GB200. More advanced chips are more expensive; for example, a GB300 build would be 20% higher.

Jensen Huang's statement that per GW costs $10 billion is actually realistic – if you factor in Rubin's compute cost, which is double that of Blackwell. Costs for power, etc., are also rising.

We also know each GB200 draws roughly 1200 watts, so 100MW translates to about 83,333 GPUs.

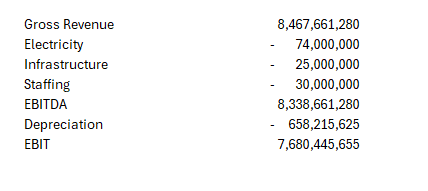

Applying the economics of the xAI contract, revenue would be 83,333 × $11.6 × 365 × 24 = $8.467 billion annually.

The cost structure is as follows:

$740,000 per MW annually for electricity, $250,000 per MW annually for infrastructure maintenance, $300,000 per MW annually for labor.

Note: Ledger for a 100MW data center based on the xAI contract rental rate ($11.6 per card per hour), with a payback period of less than one year

So we see a crazy scenario: a payback period of less than a year.

I'll say this now, this contract with SpaceX is astonishingly generous. Is Google facing a severe compute shortage?

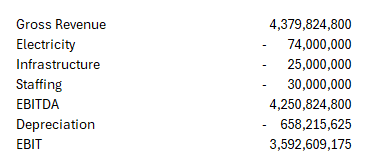

If we use a less crazy, more normal assumption, say a price of $6 per hour.

Note: Projection after reducing the rental rate to $6 per card per hour, extending the payback period to approximately two years

The payback period extends to roughly two years.

I estimate long-term contracts signed between neoclouds and hyperscalers are priced around $4 per hour. The hyperscalers then resell this compute at higher prices, like AWS's $12+.

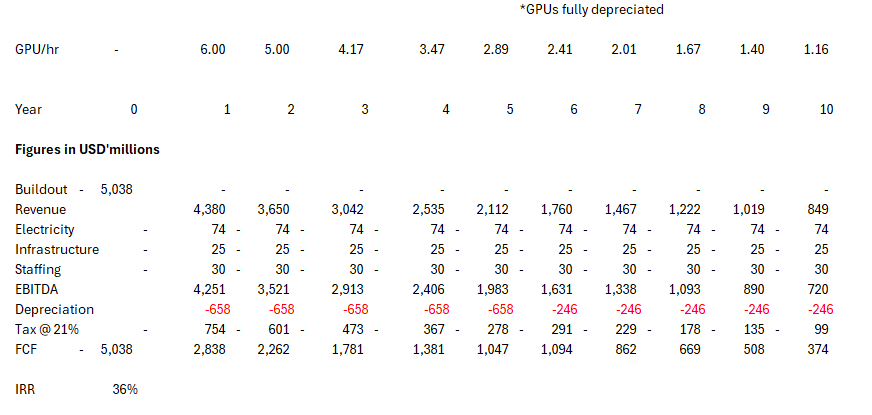

Just for fun, here's a projected income statement for building a single data center.

Note: Projected income statement for a single data center build

Of course, one could argue that GB200s will be worthless after 5-6 years. But the A100 was released in 2020 and is still being rented out for $1 to $2 per hour. This card rented for about $3 in 2021, and hyperscalers are still renting it for $2 to $3.5 per hour now.

Gavin Baker believes the depreciation cycle for GPUs should be stretched to about 10 years. I agree with him, especially with the rise of agentic AI and inference demand.

Ultimately, the current compute market is pricing in a severe shortage.

If anyone tells you otherwise, they are burying their head in the sand.

SpaceX rents compute because, at the price it's renting it out, it's making a killing (also because of connectivity issues with Colossus 1 and 2). Musk included an early termination clause in this contract, stating, "If compute becomes particularly tight, I said we might need to take it back at some point."

TL;DR: Everyone wants to be a neocloud now because compute is extremely tight, and it prints money.

Looking at the current reality, being able to build a data center and sell its compute capacity is the best business available.

This is also why hyperscalers are willing to prepay neoclouds to lock in compute supply.

To reiterate, a neocloud's valuation should equal the sum of the net present value of all the compute contracts it can secure. Therefore, financing ability, accurate depreciation schedule, and execution capability are the three most important levers affecting valuation.

For those who casually dismiss this as all circular financing (or whatever term you use), you should know: Anthropic's inference service is currently generating gross margins of over 70%. The frontier labs that consume the most compute can switch to being cash flow positive anytime they want.