Gate Institutional Monthly Report | ETF Capital Continues to Net Outflow, Crypto Market Enters a Period of Wide-Range Volatility

- Core Thesis: In May 2026, the crypto market entered a consolidation phase under the alternating influence of geopolitical risks and policy expectations; ETF capital inflows slowed, and the industry's focus is shifting from trading towards compliance-driven and real-revenue-oriented infrastructure building. The stablecoin market capitalization exceeded $300 billion, and VC funding saw a significant recovery.

- Key Factors:

- Repeated geopolitical disruptions (Middle East, Russia-Ukraine) suppressed risk appetite, leading to a more zero-sum game in the crypto market. Bitcoin remained relatively stable, while altcoins faced pressure.

- Capital inflows into crypto ETFs slowed noticeably and experienced periodic net outflows. Institutions shifted from active allocation to a cautious stance, with both Bitcoin and Ethereum ETFs showing adjustment trends.

- Global equity markets continued to rise. The U.S. stock market was led by the AI theme (semiconductors) and the healthcare sector. A decline in the VIX index indicated improved risk appetite, while gold experienced high-level range-bound corrections.

- Prediction market trading volume remained in the tens of billions of dollars. Kalshi led in volume and fees under a compliant framework, while Polymarket faced both global traffic growth and regulatory scrutiny.

- Crypto payment card transaction volume increased to $752 million. Stablecoins (USDT, USDC) dominated payment use cases. This Red Sea market is highly concentrated, dividing into two models: large-scale withdrawals and small-value, high-frequency transactions.

- Stablecoin market capitalization surpassed $300 billion (tripling in one year), driven by the implementation of regulatory frameworks, emerging market demand for dollars, and the expansion of on-chain finance. However, the market remains highly concentrated around Tether and Circle.

- Crypto VC funding recovered, with a16z raising $2.2 billion and Haun Ventures raising $1 billion. Capital is flowing towards real revenue-generating directions such as stablecoins, RWA, and AI Agent financial rails.

Abstract

• In May 2026, global markets oscillated between geopolitical disruptions, policy expectations, and a recovery in risk appetite. The crypto market overall entered a period of consolidation dominated by structural opportunities.

• ETF inflows slowed notably and turned to net outflows periodically, reflecting institutional capital shifting from active allocation to cautious观望. The market lacks a clear short-term directional consensus.

• Global equity markets continued their upward trend overall. U.S. stocks remained strong, driven by the AI narrative, with the semiconductor and healthcare sectors leading. Sentiment for risk assets generally improved.

• Gold traded at high levels with volatility, while oil prices dominated commodity fluctuations. This indicates that demand for safe-haven assets hasn't fully subsided, and global macro pricing remains influenced by geopolitical risks and inflation expectations.

• Prediction markets and crypto payment cards continued to expand. The industry's focus is shifting from trading narratives towards compliance, payment-oriented, and real revenue-driven infrastructure building.

• Gate officially launched stock trading, allowing users to directly trade stocks and ETFs from major U.S. securities markets using USDT on the platform.

1. Macro Market Trends

1.1 Recurring Geopolitical Tensions, Persistent Pressure on Global Risk Appetite

The macro environment in May was characterized by recurring geopolitical turmoil. While signals of ceasefires and negotiations emerged in the Middle East during the month, overall progress was unstable. Localized conflicts and implementation setbacks made it difficult for the market to fully digest the associated risks. There were also brief attempts at de-escalation between Russia and Ukraine, but their sustainability was limited, indicating that global political uncertainty remains high. Against this backdrop, safe-haven sentiment rose periodically, supporting assets like crude oil and gold, while global risk assets performed more cautiously.

For the crypto market, the external environment in May was not favorable. Rising geopolitical risks tend to suppress overall market risk appetite, with capital flowing towards defensive assets like cash and gold. Highly volatile crypto assets are more susceptible to sentiment shocks, amplifying short-term price fluctuations. Structurally, Bitcoin, with its liquidity and market consensus advantages, typically shows relative stability, while altcoins and high-volatility sectors are more prone to pressure when risk appetite declines. Consequently, the crypto market in May leaned more towards a battle among existing capital, with trading logic dominated by defense, wait-and-see, and event-driven actions. A broad-based rally would require a further reduction in external uncertainties.

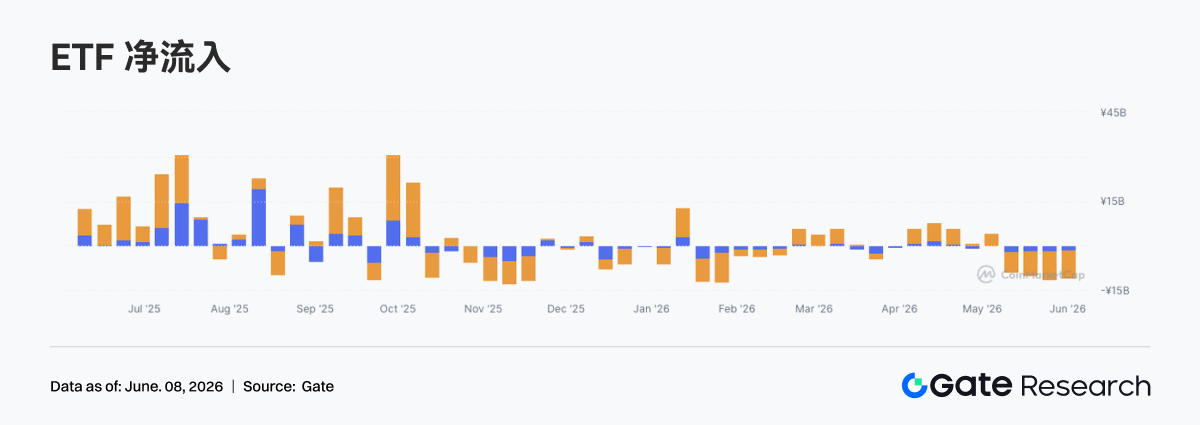

1.2 ETF Flows: Significant Slowdown in Inflows, Market Sentiment Turns Cautious

In May 2026, the crypto ETF market showed a clear trend of slowing inflows and increasing net outflows. Correlated with market performance, as Bitcoin and Ethereum prices gradually weakened during the month, investor risk appetite notably decreased. Institutional capital shifted from its previous active allocation phase to cautious观望. Compared to the continuous inflow period in late 2025 and early 2026, ETF capital flows in May showed clear signs of cooling, reflecting the market's lack of a clear short-term direction.

Structurally, Bitcoin spot ETFs remained the core driver of overall capital flows. During May, Bitcoin's price corrected after high-level volatility, prompting some institutional investors to lock in profits and reduce risk exposure. Towards the end of the month, the scale of ETF net outflows expanded further, resonating with BTC breaking below key support levels, indicating a market sentiment shift from optimism to caution. The increase in outflows also suggests heightened concerns among institutional investors regarding short-term market volatility.

Meanwhile, Ethereum spot ETFs also exhibited relatively weak capital performance. Although the Ethereum ecosystem and its long-term development prospects remain under market focus, the willingness for new capital to enter was insufficient amidst the broader market adjustment, leading to a noticeable decline in ETF capital liquidity. Overall, the crypto ETF market showed a net outflow trend in May. Institutional allocation turned conservative, entering a phase of periodic adjustment. In the near term, investors are more inclined to wait for greater clarity in the macro environment and market sentiment before making large-scale allocations.

1.3 Global Capital Market Trends

1.3.1 Major Global Indices: Improved Risk Appetite, Continued U.S. Stock Rally

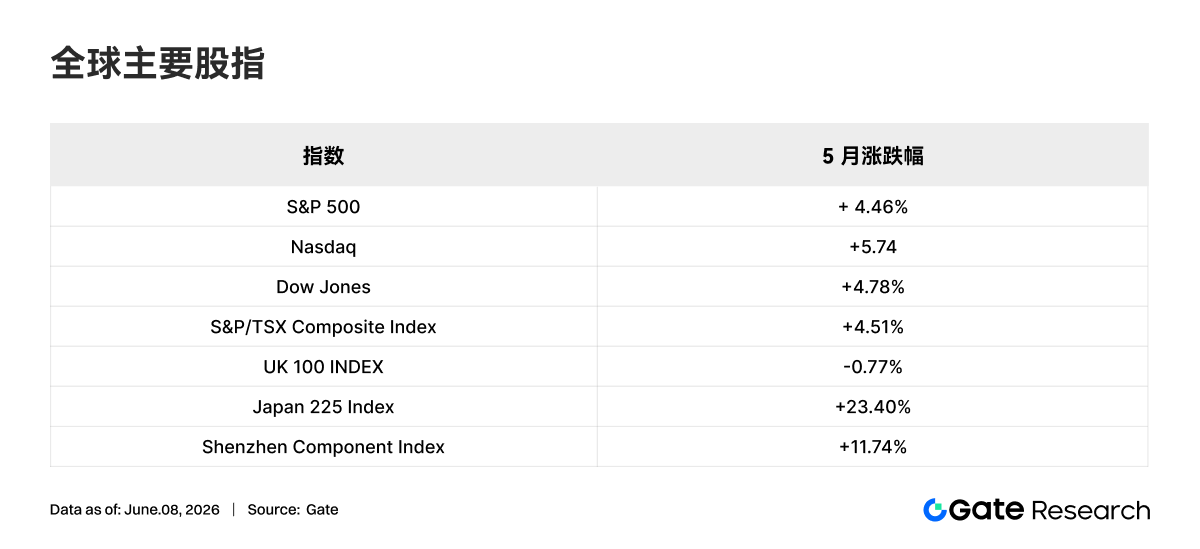

In May 2026, major global stock indices generally continued their upward trend, with the U.S. market performing particularly strongly. The Nasdaq Composite Index rose 5.61% for the month, the S&P 500 Index gained 4.39%, and the Dow Jones Industrial Average increased by 4.77%, reflecting strong market confidence in U.S. economic growth prospects and corporate profitability. The technology sector continued to be a significant driver of the market rally.

Among other major markets, Canada's S&P/TSX Composite Index rose 4.60%, largely in sync with the U.S. market. The UK's FTSE 100 Index edged down 0.26%, showing relative weakness. Meanwhile, the VIX volatility index, a measure of market fear, fell by 12.70% during the month, indicating an improvement in investor risk appetite and a significant decrease in demand for safe-haven assets.

Overall, global equity markets showed strong resilience in May 2026, with major economies' stock markets generally posting positive returns. Risk assets outperformed safe-haven assets, and market sentiment was broadly optimistic, providing a favorable investment environment for global capital markets. However, against the backdrop of rising valuations, investors still need to monitor the potential impact of macroeconomic data, monetary policy changes, and geopolitical factors on the markets.

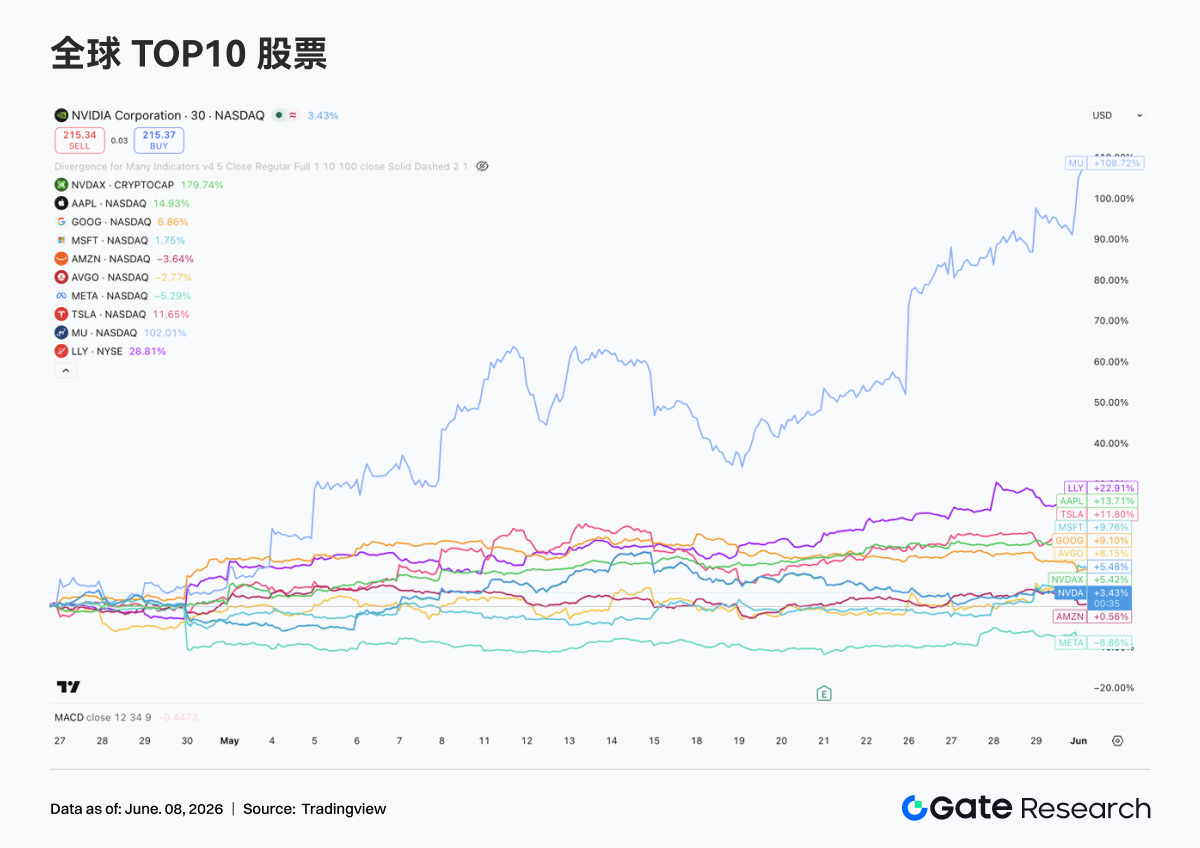

1.3.2 Stocks: AI Narrative Continues to Strengthen, Semiconductors and Healthcare Lead

In May, the top ten U.S. companies by market capitalization generally continued their upward trend, but divergence between sectors and individual stocks widened significantly. The market narrative remained centered around Artificial Intelligence, with capital concentrating on leading enterprises possessing AI infrastructure, cloud computing capabilities, and predictable profit growth. In terms of performance, the semiconductor sector clearly led the way, with tech giants generally posting positive returns, while some internet platforms and e-commerce companies lagged.

Semiconductors emerged as the strongest theme in this cycle. Growing market expectations for AI computing power demand drove valuation increases across the entire chip industry chain. Micron Technology (MU) stood out the most, benefiting from the explosion in HBM (High Bandwidth Memory) demand and data center expansion, achieving a doubling of its stock price. NVIDIA (NVDA) saw relatively modest gains but remained strong after significant increases over the past two years. Meanwhile, network and custom chip suppliers like Broadcom (AVGO) also continued to benefit from the AI infrastructure build-out cycle, indicating that capital has expanded from a single GPU logic to the entire computing ecosystem chain.

The healthcare sector became another important investment theme in May. Eli Lilly (LLY) achieved significant excess returns driven by the continued strong sales of its GLP-1 weight loss and diabetes drugs. The market increasingly views it as a scarce asset combining tech-growth attributes with pharmaceutical defensive characteristics.

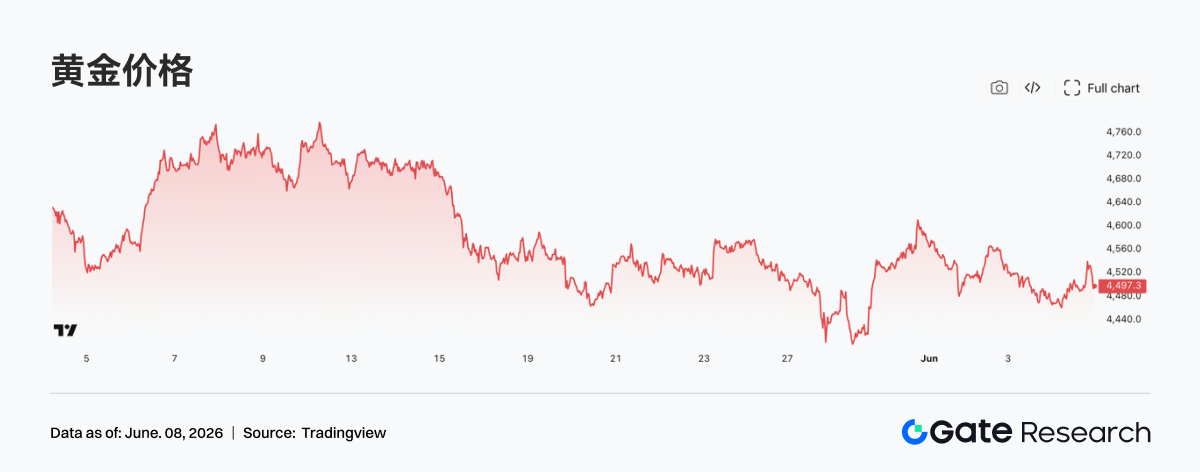

1.3.3 Gold: Safe-Haven Demand Cools, Gold Price Corrects at High Levels

In May, international gold prices exhibited a high-level consolidation trend. After previous consecutive rallies leading to new all-time highs, the market entered a phase of profit-taking. Gold prices edged down by about 0.8% during the month. Although the correction was limited, it reflects investors reassessing short-term safe-haven demand and expectations for interest rate cuts.

However, the long-term supportive logic for gold hasn't fundamentally changed. Central banks globally continue to increase their gold reserves, the dollar-based credit system faces challenges, and expectations of a rate-cutting cycle in major economies still provide medium-to-long-term support for gold. During this correction, gold prices have generally remained near historical highs, indicating that market demand for gold as an allocation asset remains strong.

Overall, the gold market in May appeared more like a technical consolidation following a significant rally, rather than a trend reversal. Against the backdrop of slowing global economic growth, lingering geopolitical uncertainties, and the gradual shift towards looser monetary policy by major central banks, gold retains strong strategic allocation value.

1.3.4 Commodities: Oil Price Dominates Volatility, Industrial Metals Reprice Around "Inflation Expectations"

In May 2026, the most critical change in the commodity market was energy prices re-emerging as the pricing anchor for the entire market. Affected by recurring situations in the Middle East, transportation risks in the Strait of Hormuz, and expectations of supply disruptions, international oil prices experienced multiple sharp rallies and declines throughout the month. The market's sensitivity to geopolitical risk premiums notably increased. A Reuters report on May 12 showed Brent crude oil briefly rising to about $107.77 per barrel, and WTI to about $101.89 per barrel, reflecting a shift in trading logic from "demand concerns" to "supply security priority." This indicates that commodities in May were no longer simply following macro growth expectations but were more driven by unexpected events and re-emerging inflation expectations. Crude oil, in particular, has once again become a key variable affecting global asset pricing.

Amidst oil price disruptions, the performance of industrial metals also showed significant divergence. Metals like copper reflected a characteristic of "coexisting macro expectations and supply-demand expectations," showing price elasticity, but with less sustainability than the energy sector. Overall, the commodity market in May moved from a phase of predominantly macro-driven trading to a new stage driven jointly by "geopolitical shocks + interest rate expectations + supply constraints." Short-term high volatility is likely to persist, with energy commodities clearly dominating precious and base metals.

2. Analysis of Trending Sectors

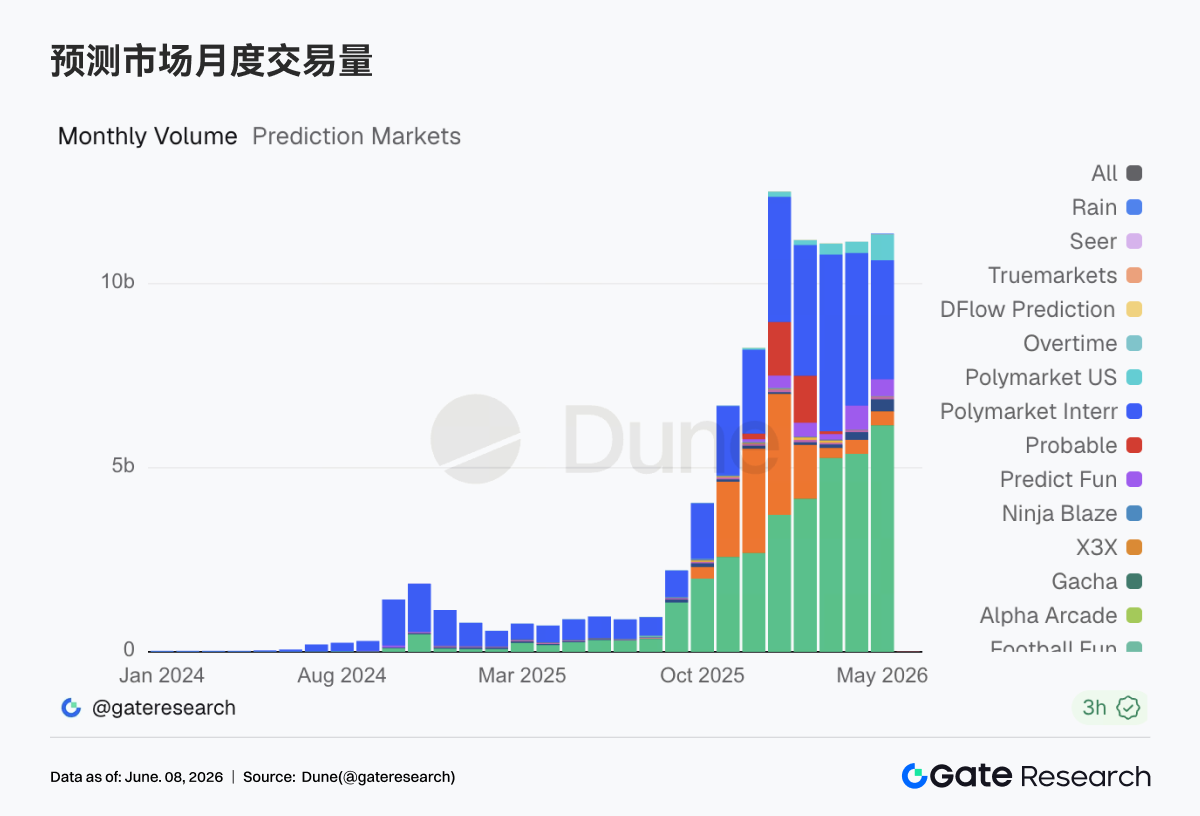

2.1 Prediction Markets: Institutional Inflection Point, Regulatory Trials, and Liquidity Redistribution

In May, prediction market taker volume was approximately $11.36 billion, a slight increase of about 2% from ~$11.14 billion in April. Since the start of 2026, monthly volumes have remained above $10 billion for five consecutive months. Meanwhile, internal structural changes are evident. Kalshi's May volume was about $6.15 billion, representing ~54% of the total market. Polymarket International had about $3.23 billion (~28%), and Polymarket US reached $695 million, doubling from April. The industry's growth is shifting from purely crypto-native traffic towards trading scenarios that are more regulated and closer to traditional derivative markets.

Beyond trading volume, primary market valuations for prediction markets continued to grow. Kalshi completed a $1 billion funding round, raising its valuation to $22 billion. Participants included Coatue, Sequoia, a16z, Morgan Stanley, and ARK. Prediction markets are now viewed by mainstream capital as an event-risk trading infrastructure. In its fundraising materials, Kalshi explicitly stated its intent to use the funds to expand institutional clients like hedge funds, asset managers, proprietary trading firms, and insurance companies, and to develop block trading, risk management products, and brokerage integration. This aligns with what institutions are truly interested in: transforming uncertainties related to macroeconomics, elections, policy, sports, and geopolitics into standardized contracts that can be traded, cleared, and risk-managed. Data supports this assessment. Kalshi's current 30-day average daily taker volume is about $199 million, its 7-day average is about $218 million, and its 7-day market share has risen to about 57%. Its open interest stands at about $674 million, also ranking first.

In contrast, Polymarket still possesses strong global traffic and brand recognition. However, Polymarket International's May volume was about $3.23 billion, down from ~$4.15 billion in April, marking a second consecutive month of significant decline after introducing full fees. Meanwhile, Polymarket US rose from ~$302 million in April to ~$695 million in May, indicating that Polymarket's compliant return path to the U.S. is gaining traction.

Fee data further illustrates that the commercialization capacity of prediction markets is concentrating on leading platforms. Total industry fees in May were about $184 million, up from ~$155 million in April, with fee growth significantly outpacing volume growth. Kalshi contributed an estimated ~$138 million in fees, accounting for about 75% of the total. Polymarket International contributed ~$28.07 million, and Polymarket US ~$12.78 million. For institutional investors, volume indicates market heat, while fees demonstrate a platform's true revenue-generating capability and pricing power. If prediction markets are eventually valued like exchanges, brokerages, or derivative infrastructures, fee concentration, client structure, and sustainable revenue will become more important than single-month volume.

Regulatory events in May constituted the largest source of risk premium for the industry. The House Oversight Committee launched an insider trading investigation into Kalshi and Polymarket, demanding details on identity verification, geographic restrictions, and abnormal trading detection mechanisms. In the same month, Kalshi supported the formation of the advocacy group "Americans for Fair Markets," pushing for a federal regulatory framework centered around the CFTC. These two events appear to be one pressure and one defense, but both essentially point to the same thing: prediction markets are being incorporated into more serious financial regulatory discussions. If institutional capital intends to use prediction markets for macro, policy, and geopolitical risk hedging, issues like insider information, government employee trading, market manipulation, and restrictions on markets related to violence or terrorist events must be institutionally addressed.

Polymarket's actions in May also highlight the tension between global expansion and regulatory boundaries. Polymarket is preparing to enter the Japanese market while simultaneously facing regulatory scrutiny in jurisdictions like the U.S., India, and South Korea. Its advantages lie in crypto-native users, global event coverage, and on-chain transparency. However, its challenge is the inconsistent legal classification of "prediction markets," "gambling," "derivatives," and "information markets" across different countries.

For institutions, Polymarket represents an open, globalized, crypto-native growth path, while Kalshi represents a regulated, centralized path geared towards institutional access. May's data suggests the latter temporarily holds an advantage in volume, fees, and OI. However, the former may still maintain strength in global markets and long-tail event categories.

Overall, May was a crucial transitional month for prediction markets moving towards becoming financial infrastructure. The key question is whether prediction markets can evolve into a new type of event derivatives market – one that allows expressing views, managing risks, and supplementing the non-standardized event risks not covered by traditional futures, options, and macro hedging tools. Kalshi's fundraising and data leadership indicate that the compliant path is gaining capital recognition. Polymarket's U.S. return and Japan expansion suggest the global platform is still searching for regulatory breakthroughs. Long-tail platforms like Limitless, Predict Fun, and Opinion mainly serve as vertical niche and high-turnover experimentation grounds. The future winners are likely to be platforms that can simultaneously satisfy compliance, liquidity, market surveillance, institutional access, and deep event coverage.

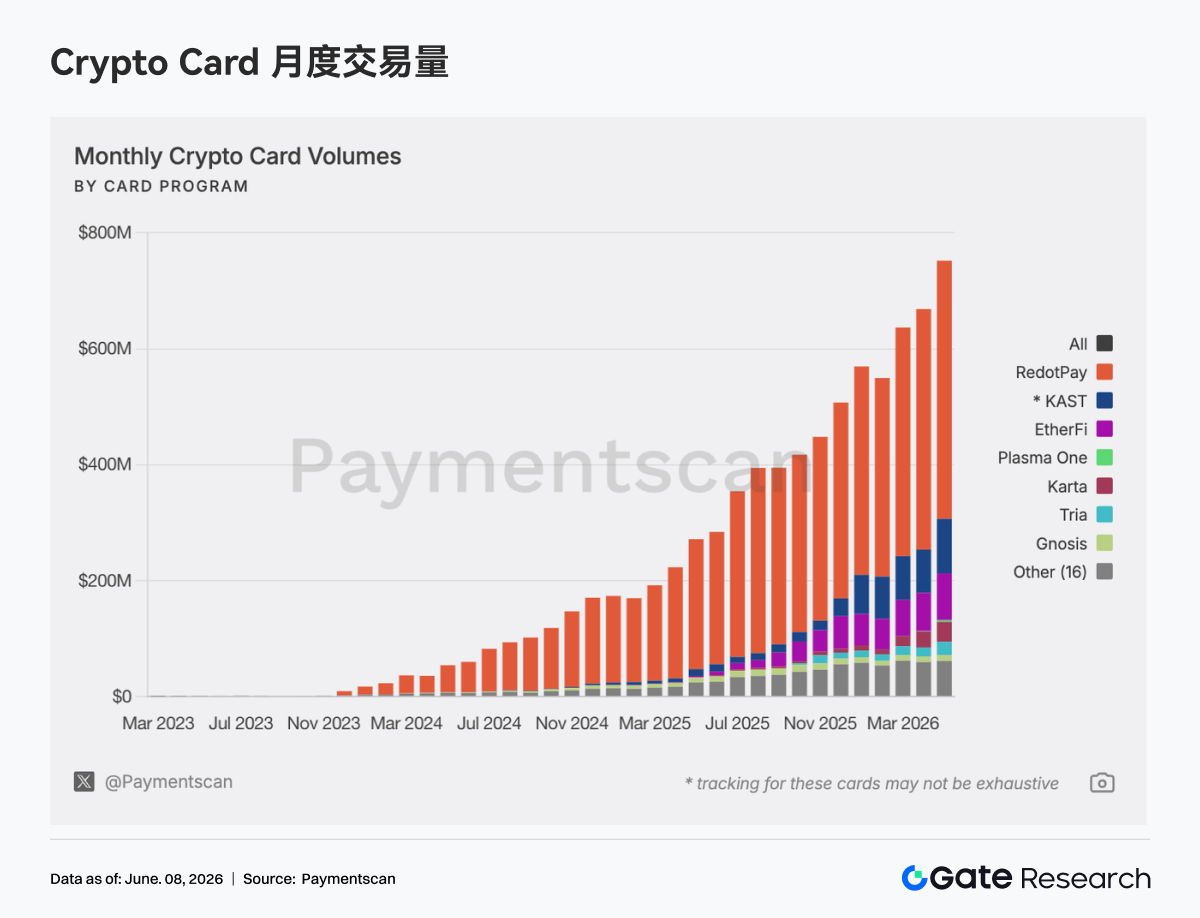

2.2 Crypto Payment Cards: Steady March Towards Stablecoin Payment Infrastructure

In May, trading volume for crypto payment cards continued to expand. Attributable on-chain payment card volume reached approximately $752 million, up about 12.5% from ~$669 million in April. The number of transactions was about 3.05 million, an increase of about 8% from ~2.82 million in April. This growth is driven not only by large capital inflows but also by higher-frequency real-world usage.

From a project landscape perspective, the market was highly concentrated in May. RedotPay accounted for approximately $445 million, representing about 59% of the total market, making it the absolute dominant player. KAST had about $93.88 million (~12.5%), and EtherFi had about $80.4 million (~10.7%). The top three collectively accounted for approximately 82%. While there are many projects in the crypto payment card market, only a few top-tier products can achieve scale in payments or on/off-ramp scenarios. This concentration implies the emergence of clear channel gateways in the market. Future business partnerships, card issuance collaborations, stablecoin distribution, and payment network negotiations will likely prioritize data-heavy entities like RedotPay, KAST, and EtherFi.

From a daily consumption perspective, the average transaction values for RedotPay and KAST were approximately $766 and $931 respectively, leaning towards large-value on/off-ramps, stablecoin off-ramping, or high-net-worth user spending scenarios. EtherFi processed about 977,000 transactions in May, with an average value of about $82, more closely resembling real daily consumption. Gnosis had about 220,000 transactions (~$46 average), and Bitget Wallet had about 450,000 transactions (~$14 average), also showing small-ticket, high-frequency characteristics. This indicates an internal divergence in the crypto payment card market into two business models: one is the stablecoin off-ramp/large-value spending card (contributing the bulk of transaction value), and the other is the wallet-embedded daily payment card (contributing user habits and transaction frequency).

On the chain level, payment card activity in May remained heavily reliant on high-liquidity stablecoin chains. By attributed chain, Tron accounted for