No matter how many GPUs you have, you might still lack power? JPMorgan: $19.2 Billion Power Chips Are the Real Key

- Core View: A JPMorgan report predicts that the rapidly growing power demand of AI data centers will trigger a boom in the power semiconductor market. The core driver is the 800V high-voltage DC architecture revolution, which uses silicon carbide (SiC) and gallium nitride (GaN) devices to replace traditional equipment, significantly increasing semiconductor content.

- Key Elements:

- By 2028, global AI data centers are expected to add approximately 81 GW of installed capacity (including 63 GW from new builds), driving the power semiconductor market from $2.7 billion in 2025 to $19.2 billion (a three-year CAGR of 82%).

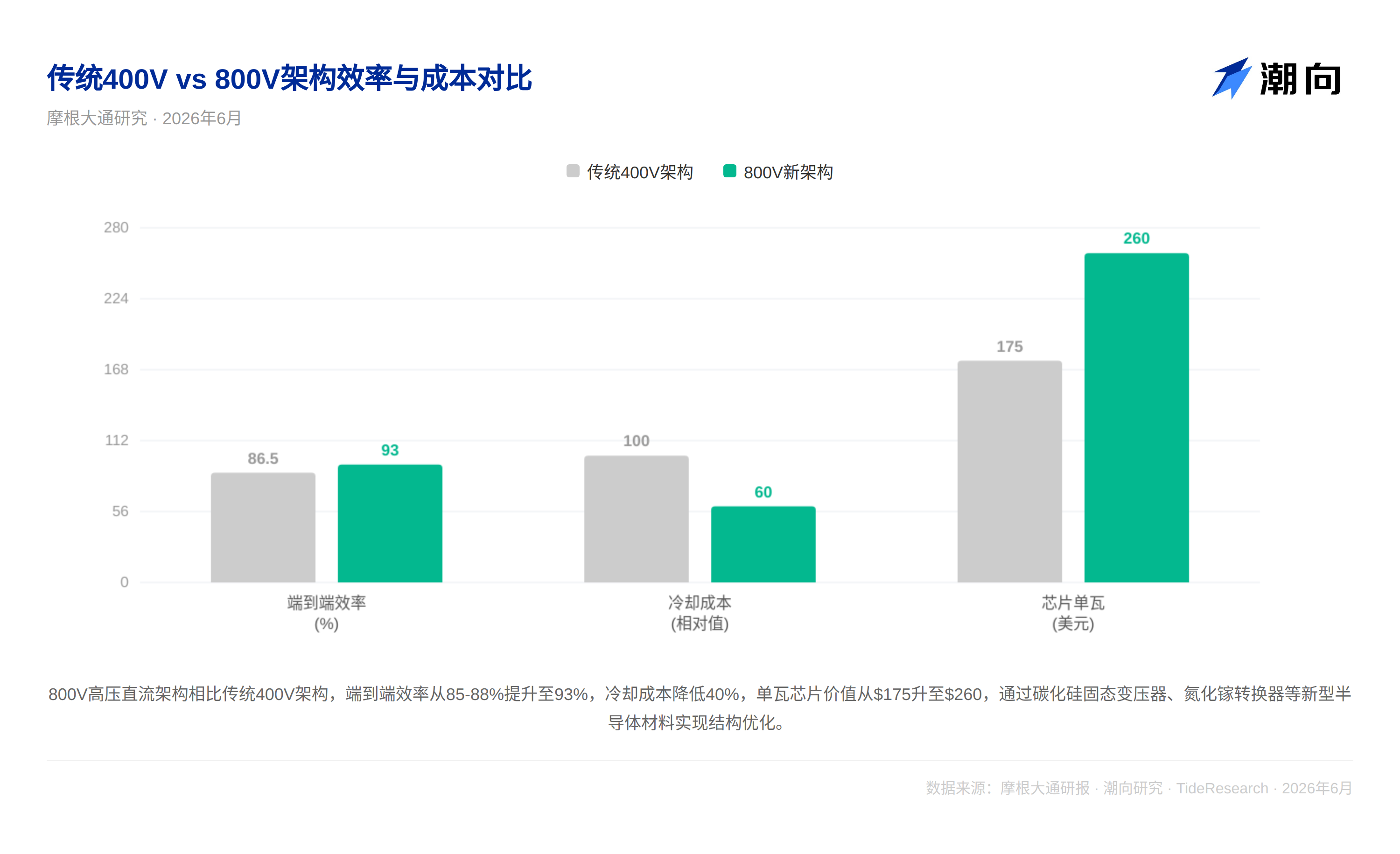

- The current traditional 400V AC power architecture achieves about 85-88% efficiency, with each of the five conversion stages losing 2-5%; the 800V high-voltage DC architecture doubles the voltage and halves the current, reducing copper losses to one-quarter.

- The 800V architecture brings a qualitative leap in semiconductor content, with the unit power semiconductor value rising from the current $175/W to $260/W, adding four key components such as solid-state transformers and solid-state circuit breakers.

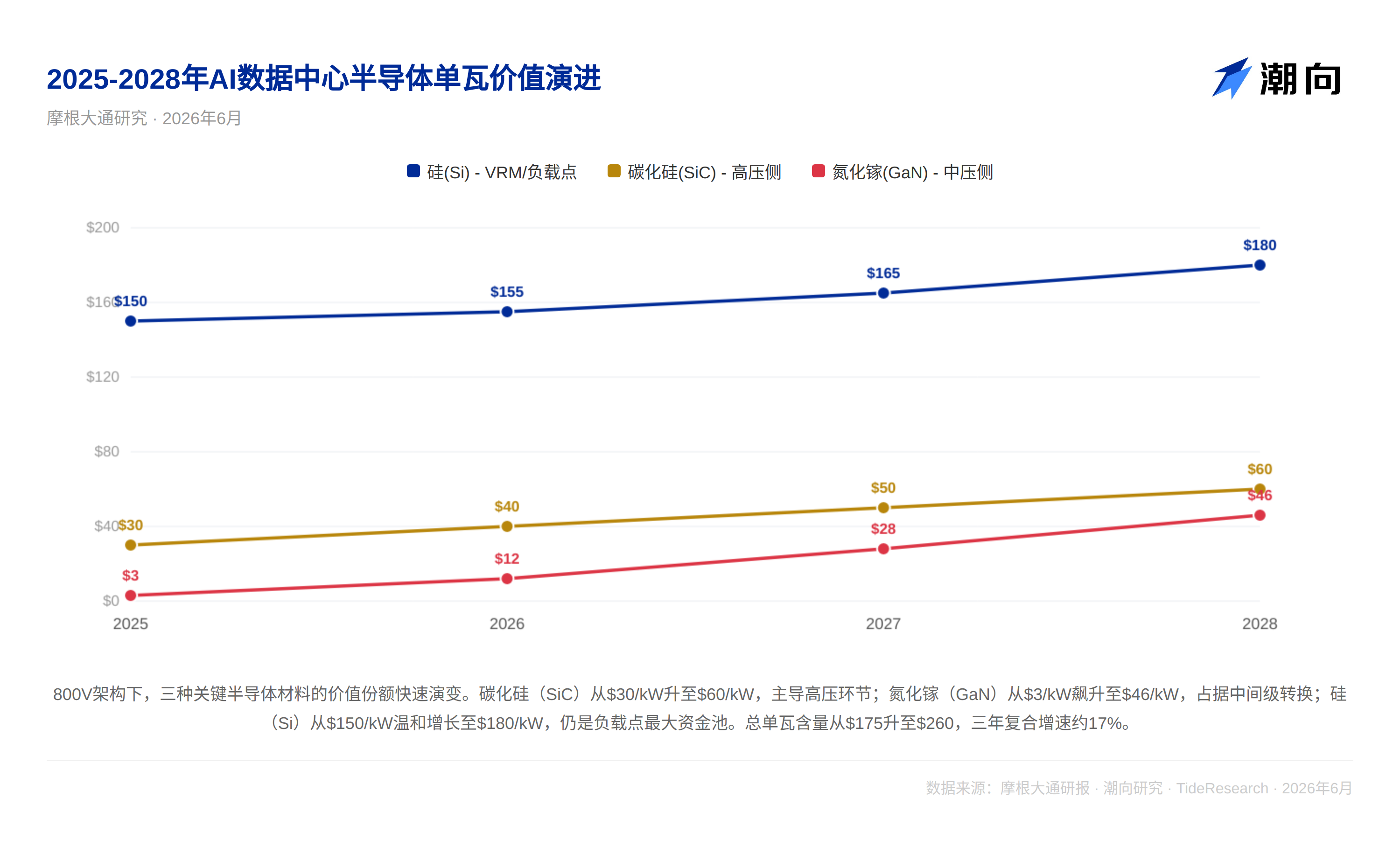

- SiC devices dominate the high-voltage link from the grid to the rack, with long-term value increasing from $30/W to $60/W; GaN excels in intermediate-stage conversion, with its value skyrocketing from $3/W to $46/W.

- Nvidia's Kyber rack plan is expected to be deployed at scale from the second half of 2027 to 2028, with a single rack of 600kW driving the adoption of the 800V solution. Silicon will continue to hold the largest share of capital in the VRM segment ($180/W).

Original Author: Rita

Introduction

J.P. Morgan applies first principles reasoning to deduce the complete power supply chain for AI data centers. The core conclusion: The AI power semiconductor market will be approximately $2.7 billion in 2025, surging to $19.2 billion by 2028, representing a three-year compound annual growth rate (CAGR) of 82%. A larger variable is the revolution of the 800V high-voltage DC architecture, which replaces traditional electromechanical equipment with silicon carbide (SiC) solid-state transformers and gallium nitride (GaN) converters. This increases the semiconductor content per watt from $175 to $260. This signals an emerging value chain previously overshadowed by the spotlight on GPUs.

Behind 80 GW of Computing Power: A Five-Stage Relay for Every Watt

Everyone counts GPU shipments, but few count the power. Current data center power distribution is an inefficient, lengthy chain: AC power from the grid at 10-35kV is first stepped down to 400-480V by a transformer, then passes through the UPS, across the PDU, to the server power supply which converts AC to DC, and finally through the VRM to the sub-volt levels required by the GPU core. This five-stage conversion, with 2-5% loss at each stage, results in an end-to-end efficiency of only 85-88%. For a single rack drawing 100kW, 15kW is lost as waste heat, which must be managed entirely by the cooling system.

Based on internal AI server models, J.P. Morgan estimates that global AI data centers will require approximately 81 GW of new installed capacity by 2028, comprising roughly 63 GW of new builds and 18 GW of replacements. AI chip power consumption accounts for about 54 GW, with the final number reached after including networking equipment and the PUE factor. For the power semiconductor market supporting this 81 GW, the report estimates that semiconductor content per watt will rise from the current $175 to $260, driving the total market to $19.2 billion.

The 800V Architecture Revolution: Double the Voltage, Triple the Chips

The core technological insight of the report is the replacement of conventional AC architectures with an 800V High-Voltage DC (HVDC) architecture. The physics are straightforward: Power equals voltage multiplied by current, and heat loss is proportional to the square of the current. By increasing voltage from 400V to 800V, current is halved, and copper losses (I²R) are reduced by a factor of four. However, the true significance of this architectural shift lies in the qualitative change in semiconductor content.

In traditional architectures, many links involve electromechanical equipment, with semiconductor concentration primarily in the PSU and VRM. The 800V architecture introduces four new nodes: Silicon Carbide (SiC) solid-state transformers replacing conventional copper-wound transformers; SiC solid-state circuit breakers enabling microsecond-level fault interruption; native DC battery backup units with bidirectional DC-DC converters and BMS chips; and rack-level 800V-to-low-voltage DC-DC conversion.

The report provides a clear timeline: 2026-2027 will still be dominated by traditional 400V architectures, but transformation has already begun with the emergence of sidecar power shelves and power distribution shelves. From the second half of 2027 into 2028, NVIDIA's Kyber rack platform (600kW per rack) will drive the scaled deployment of native 800V solutions. After 2028, solid-state transformers will mature, merging the functions of the sidecar power shelf and transformer into a single SST device.

SiC Dominates High Voltage, GaN Captures the Mid-Range, Silicon Guards the Last Mile

The report provides a quantitative roadmap for the changing share of different semiconductor materials. Silicon Carbide (SiC) content per watt is projected to rise from the current $30 to a long-term $60, dominating the high-voltage segment from grid to rack. Gallium Nitride (GaN) is expected to surge from $3 to $46, winning in the mid-range conversion stage from 800V to low voltage. Silicon is projected to grow more modestly from $150 to $180, still holding the largest pool of spending in the VRM/point-of-load segment, defending its position on cost-performance grounds.

The landscape of key players is also taking shape. Infineon (strongest across the full-chain layout), MPS (VRM leader, key NVIDIA supplier), and Renesas capture the largest shares in the intermediate conversion and point-of-load segments, with NVIDIA having already selected multiple suppliers among them. The report covers 12 core companies in detail: Infineon, MPS, Renesas, Texas Instruments, STMicroelectronics, Navitas (GaN technology leader), Analog Devices, onsemi, Rohm Semiconductor, Innoscience, Alpha and Omega Semiconductor (AOS), and Wolfspeed.

View from the Tide

The core value of J.P. Morgan's report lies in its framework construction, rather than providing a specific price target. The $19.2 billion scale is not enormous within the overall AI infrastructure picture, but the key point remains: Without sufficient power semiconductors, no amount of GPUs can run effectively.

The report contains two assumptions that are not fully explored. First, there is a significant mismatch between the delivery cycle for grid expansion (median 3-5 years in the US) and the typical two-year build cycle for data centers. The 81 GW capacity forecast for 2028 may face execution risk on the grid side; that is, the US grid's ability to upgrade may not keep pace. Second, NVIDIA holds significant pricing power throughout the entire value chain. Its choice of power suppliers for the Kyber rack platform will directly impact the competitive landscape. It is important to note that J.P. Morgan has investment banking relationships with several covered companies, including Infineon and STMicroelectronics, a factor to consider when evaluating specific company recommendations.