Gate 机构周报:BTC 杠杆多头承压,Gate 正式推出股票交易

- 核心观点:上周加密市场在加息预期与宏观不确定性中持续承压,BTC与ETH周跌幅约4-5%;全球加密ETF连续两周净流出累计达25.4亿美元,资金向AI科技股转移;链上交易重心向深度更强的平台(如PancakeSwap)集中,杠杆多头坚守反弹预期,但市场整体风险偏好谨慎。

- 关键要素:

- 宏观施压:美国PCE通胀升至3.8%,CME FedWatch显示约68%交易员预期2026年底前至少加息25BP,30年期美债收益率突破5.14%,压制风险资产。

- ETF资金流出:BTC ETF连续14日净流出,创2025年12月以来最长记录;ETH ETF连续11日净流出;两周全球加密ETP合计净流出25.4亿美元。

- 链上交易集中:PancakeSwap交易量反超Uniswap,链上资金向流动性更深、执行效率更高的平台聚集;Solana生态Meme交易热度降温。

- 衍生品结构背离:BTC价格下跌但资金费率维持正值,显示杠杆多头仍在坚守;期权25D Skew持续为负,DVOL处于低位(34-38),市场等待方向性催化。

- TradFi与稳定币进展:Gate推出股票交易,支持超1万支美股及ETF;稳定币进入基础设施竞争期,Circle推出ChainBench强化多链开发与USDC集成。

Summary

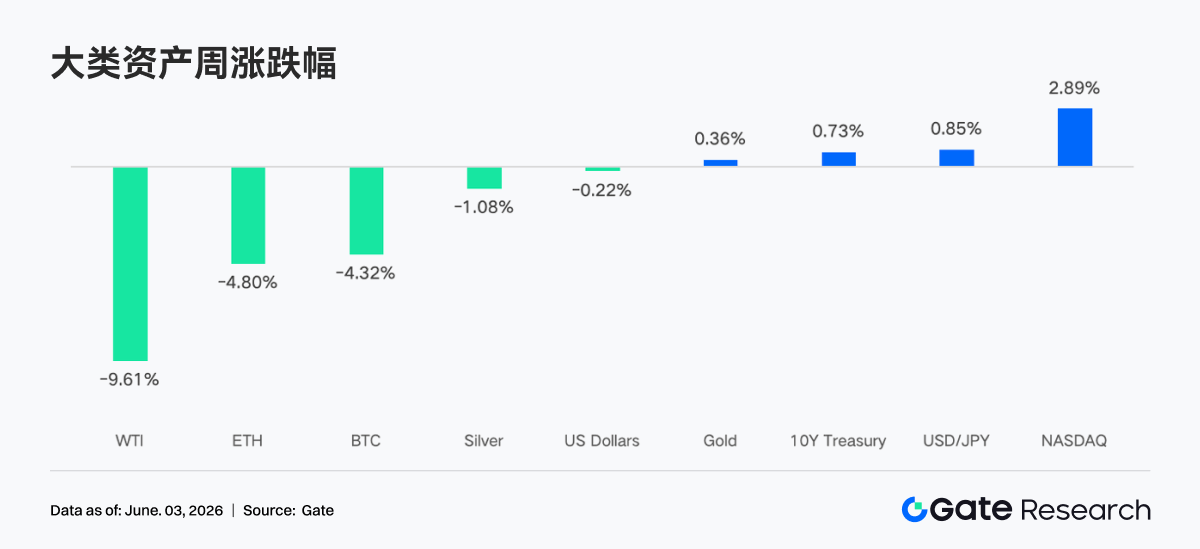

• The market is repricing Fed rate hike expectations, keeping the crypto market under pressure. BTC fell approximately 4.3% WoW, and ETH fell approximately 4.8% WoW. Global crypto ETFs saw net outflows for the second consecutive week, totaling $2.54 billion.

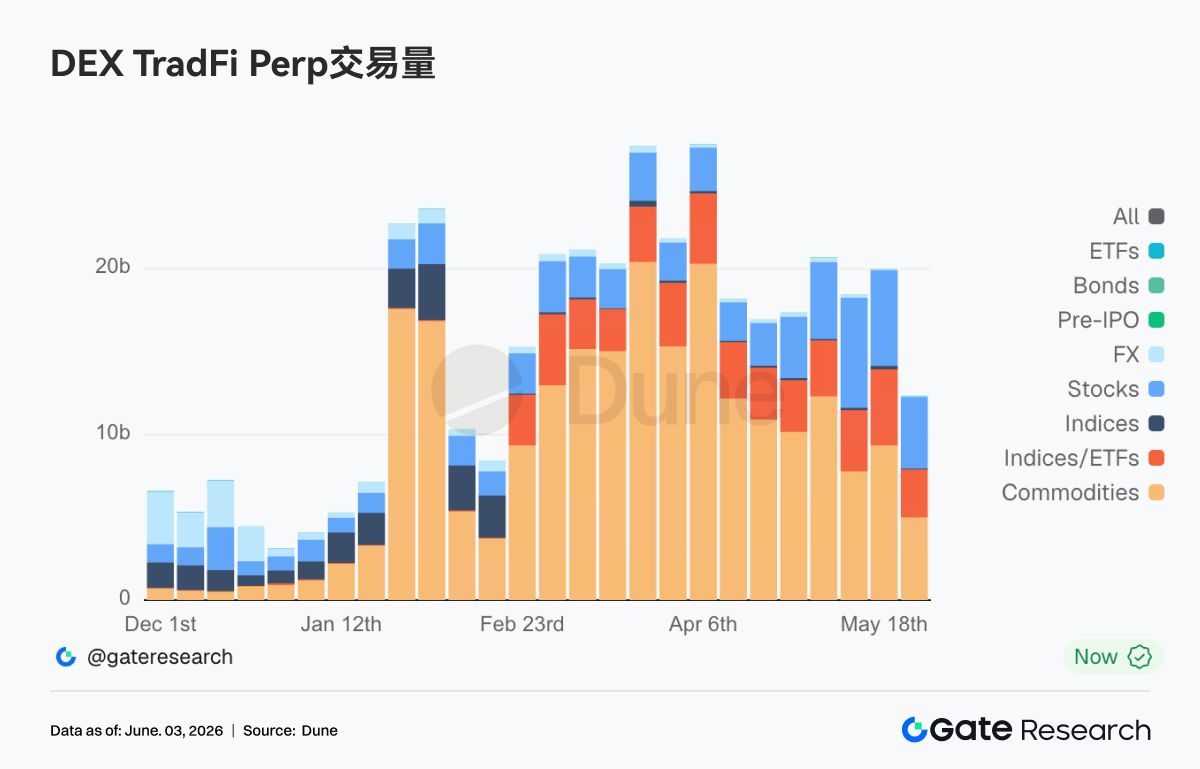

• Total trading volume on TradFi Perp DEXs declined to around $12 billion. Gate officially launched its stock trading service, supporting over 10,000 US stocks and ETFs. The total number of TradFi assets continues to grow, with the stock category leading the industry in expansion speed.

• On-chain capital is concentrating on platforms with deeper liquidity and higher execution efficiency; PancakeSwap's trading volume has overtaken Uniswap. The overall supply of stablecoins saw limited changes, with no concentrated capital flow into specific yield-bearing stablecoin products. The LST sector is cooling, but the SOL ecosystem has shown relative stability.

• DeFi risk appetite remains cautious. Aave's lending scale continued to decline, and lending rates for its three core assets have generally stabilized.

• In the derivatives market, BTC is characterized by "falling prices, positive funding rates, and compressed volatility," suggesting that leveraged long positions are still holding onto rebound expectations.

• The market next week will face key macroeconomic data tests like the May nonfarm payrolls and ISM Services PMI. Regarding token unlocks, special attention should be paid to HYPE's large unlock worth approximately $684 million, which could significantly impact market liquidity and sentiment.

1. Market Focus Interpretation

The Fed's monetary policy stance remains the market's focus. The US PCE inflation rate rose to 3.8%, the highest level since August 2023, with core PCE also increasing. This has sparked market concerns about a Fed rate hike. According to the CME FedWatch Tool, about 68% of traders anticipate at least a 25bp rate hike by the end of 2026, with zero probability of a rate cut for the full year. The 30-year US Treasury yield broke through 5.14%, and Japan's 10-year government bond yield reached 2.8%, indicating a structural loosening in the global fixed-income market. In the energy market, the US-Iran conflict hasn't fully subsided, with another round of attacks occurring on May 27, driving oil prices up and exacerbating inflation expectations, further dampening market risk appetite. In the stock market, the S&P 500 and Nasdaq showed relative strength, with tech stocks driven by the AI sector continuing to attract capital. In contrast, Bitcoin significantly underperformed equities, with some institutional analysts pointing to capital rotating from crypto assets to AI tech stocks.

In the crypto market, BTC fell from $77,027 on Monday, briefly dipping below $73,000 on Thursday, recording a -4.3% decline over seven days. ETH also declined, hitting a weekly low of $1,967, a drop of approximately -4.8%. Global crypto ETP products saw net outflows for two consecutive weeks, totaling a high of $2.54 billion, with the US contributing the vast majority. Institutions are generally adopting a "de-risking" approach. The consecutive net outflows from ETFs have set the longest record since December 2025, and overall market sentiment is cautious. On the regulatory front, reports suggest Bitcoin and Ethereum saw gains amid regulatory progress, with federal regulators speaking at the 2026 Bitcoin Conference, aiming to provide regulatory clarity for critical current issues. These factors collectively create a complex macroeconomic environment, with persistent inflation concerns, an unclear Fed policy outlook, and the cryptocurrency market continually influenced by regulatory developments. Notably, Gate recently launched stock trading, allowing users to directly trade assets in major US securities markets using USDT on the platform, currently supporting over 10,000 stocks and ETF assets.

2. Liquidity Analysis

2.1 BTC and ETH ETFs Continue to Show Significant Capital Outflows

BTC ETFs have experienced net outflows for 14 consecutive days, breaking the record for the longest streak since December 2025. Data from CoinShares shows that global crypto ETPs had total net outflows of $2.54 billion over the past two weeks. The capital flow exhibits clear characteristics of "macro hedging + tactical de-leveraging." Multiple institutional analysts point out that the ETF outflows essentially represent institutions rebalancing their portfolios by treating BTC as a macro risk asset, rather than an endogenous sell-off in the crypto market.

ETH ETFs continued their net outflow streak last week, extending to 11 consecutive days as of May 28, the longest since March 2025. ETH ETFs underperformed BTC ETFs overall, with no significant signs of institutional block buying. Alternative ETFs like XRP and SOL recorded net inflows during the same period, indicating some institutional capital is rotating among non-BTC/ETH assets.

As of May 29, the total asset under management (AUM) of BTC ETFs was approximately $94.17 billion, representing 6.38% of Bitcoin's total market cap, with a historical cumulative net inflow of $55,714 million. The total AUM of ETH ETFs was approximately $11.40 billion, accounting for about 4.5% of the net asset value, with a historical cumulative net inflow of $11,404 million. From an institutional movement perspective, capital flows show clear divergence: BlackRock's IBIT was the main source of BTC outflows last week, with a single-week outflow of $966.3 million, while its ETH product, ETHB, bucked the trend and recorded net inflows, suggesting a slight adjustment in the allocation focus of institutions across different assets.

2.2 TradFi Liquidity

• TradFi Perp DEX: Over the past week, total trading volume on TradFi Perp DEXs declined significantly from the April highs, dropping to around $12 billion, a near two-month low. However, structurally, the market isn't experiencing a broad-based cooling but rather a clear asset class rotation. Commodities remain the dominant sector, accounting for over 60% of total volume, though activity has cooled considerably from the previous $15-20 billion stage, reflecting a retreat in safe-haven assets like gold. Meanwhile, stock trading volume maintained its growth trend, with its share continuously increasing. This suggests that as US stocks maintain high levels, on-chain investors are gradually shifting their trading interest towards individual stocks and stock-related products.

• Gate TradFi Perp: Last week showed significant overall volatility, characterized by a "rapid volume surge – decline – re-surge" pattern. Precious metals remained the absolutely dominant sector. Trading volume noticeably increased from May 27 to 28, with single-day total volume approaching $550-600 million, before subsequently declining. This indicates market capital is still primarily trading around gold-related products, reflecting the persistent attractiveness of gold as both a safe-haven asset and a trading target in the current macro environment. Concurrently, the share of stock-based contract volume increased, with notable thickening on multiple trading days, showing that user participation in US stock-related perpetual contracts is rising. Especially against the backdrop of US stock indices near historical highs and the continued activity of AI and tech stocks, TradFi Perps are beginning to serve part of the demand from crypto users to participate in the US stock market. It's noteworthy that Gate has been steadily advancing its stock tokenization, TradFi asset integration, and multi-asset trading system development. Based on the changes in the trading structure, TradFi Perps are gradually evolving from a single gold trading market towards a dual-core structure of "Gold + US Stocks."

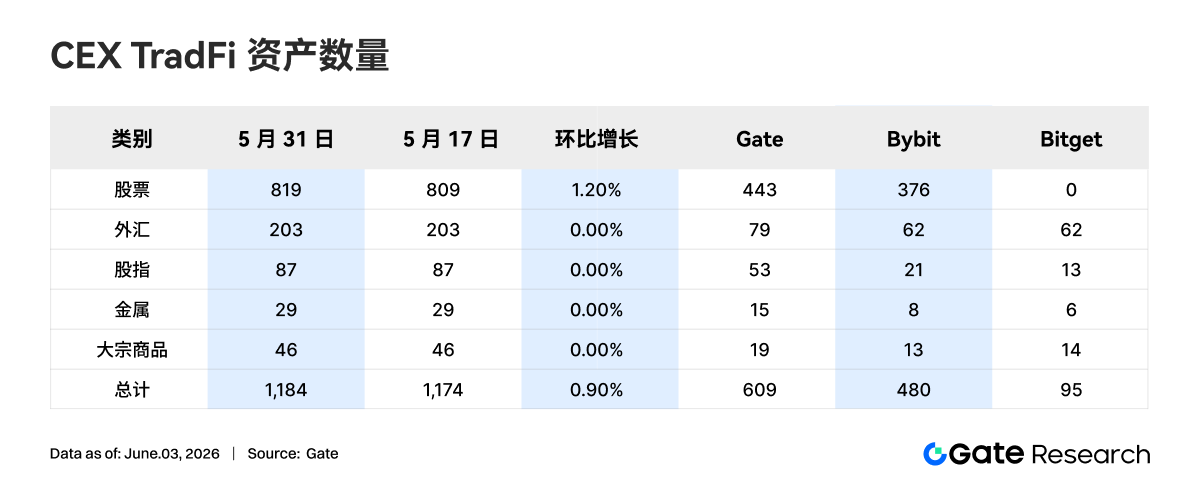

• Number of CEX TradFi Assets: In the past week, the number of TradFi asset categories on CEXs expanded further. The total number of TradFi assets (counting only the TradFi and CFD sections, excluding perpetual contracts) on three major CEXs increased from 1,174 to 1,184, a sequential increase of 0.90%. The growth was most significant in the stock category, rising from 809 to 819 stocks, a sequential increase of 1.20%. Specifically, the increase in stock numbers was contributed by Gate, where Gate TradFi stocks grew by 10 stocks WoW, a 2.3% increase.

• TradFi Order Book Depth: We selected XAUT, the TradFi asset with the highest trading volume, to analyze its order book depth (Delta). Market depth exhibited relatively distinct phased changes, which can be divided into two stages: "liquidity supplementation in the first half of the week, liquidity withdrawal in the second half." Early in the week, the order book consistently recorded positive Delta, with a large number of bid and ask orders entering the market. The net liquidity added per hour often exceeded $1 million. Meanwhile, XAUT prices oscillated within the $4,500–$4,550 range, providing a relatively stable trading environment. In the latter half of the week, the liquidity structure noticeably weakened, with order book Delta remaining in negative territory for extended periods. Although prices still traded around the $4,500 level, market depth continued to decline, suggesting some liquidity providers started reducing risk exposure or taking profits. Looking at the relationship between price and depth, XAUT experienced a brief correction mid-week but quickly recovered. However, order book liquidity did not recover synchronously and instead continued to weaken. This implies that the current price support relies more on aggressive buying pressure than deep resting liquidity. If gold prices experience further volatility in the future, the shallower order book structure could amplify short-term price swings. In the near term, attention should be paid to whether liquidity will return and the market's ability to support the $4,450–$4,500 range.

3. On-Chain Data Insights

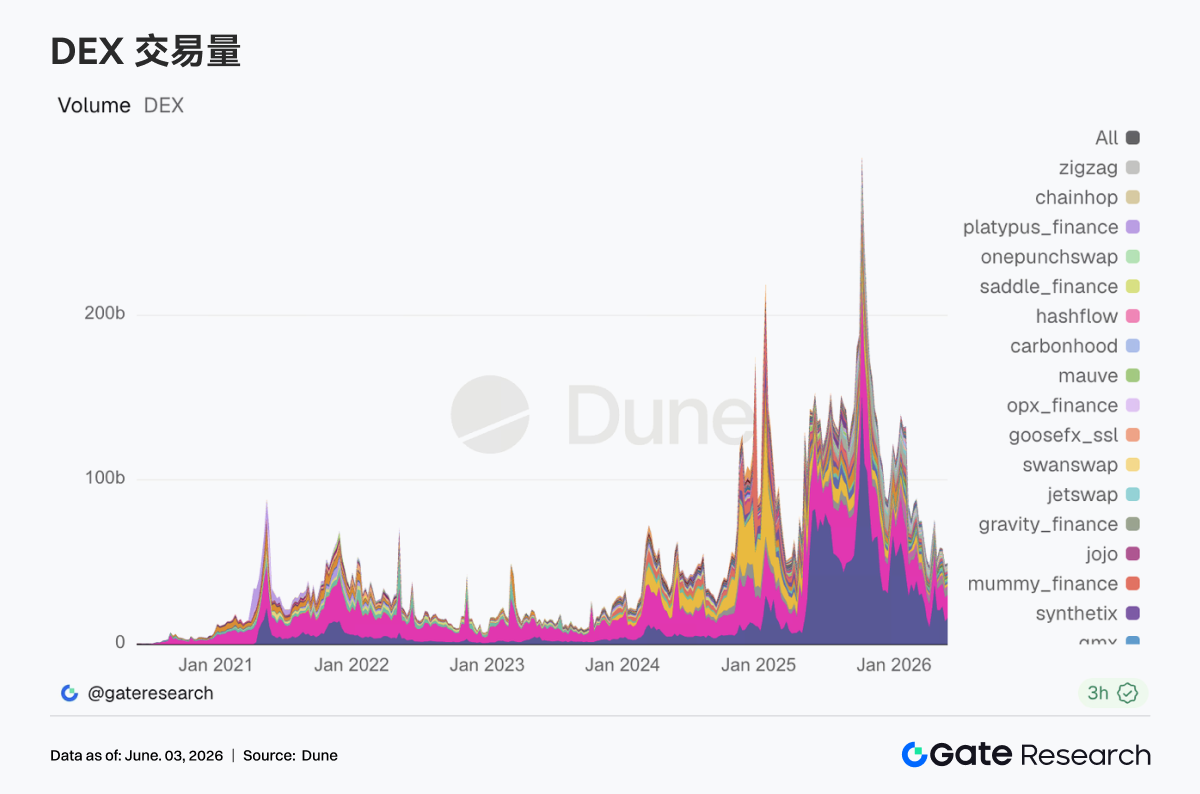

3.1 DEX Trading Shifts Towards Liquidity Concentration, PancakeSwap Overtakes Uniswap

Overall DEX trading volume remained at a relatively high level last week, but a new structural change emerged. PancakeSwap saw a significant recovery compared to the previous week, reclaiming its position above Uniswap. Although Uniswap experienced a slight decline, it remained at a relatively high trading center, indicating that spot turnover demand for major assets still exists. Meanwhile, protocols within the Solana ecosystem like Raydium, Meteora, and PumpSwap generally underperformed, with the trading frenzy associated with Meme coins and high-volatility assets cooling compared to before. Looking at the market context, spot BTC ETF outflows on a single-day basis were also at elevated levels, and risk appetite in traditional market capital retreated. However, on-chain capital did not exit the trading market simultaneously. Instead, it further concentrated on platforms offering deeper liquidity, lower transaction costs, and higher execution efficiency.

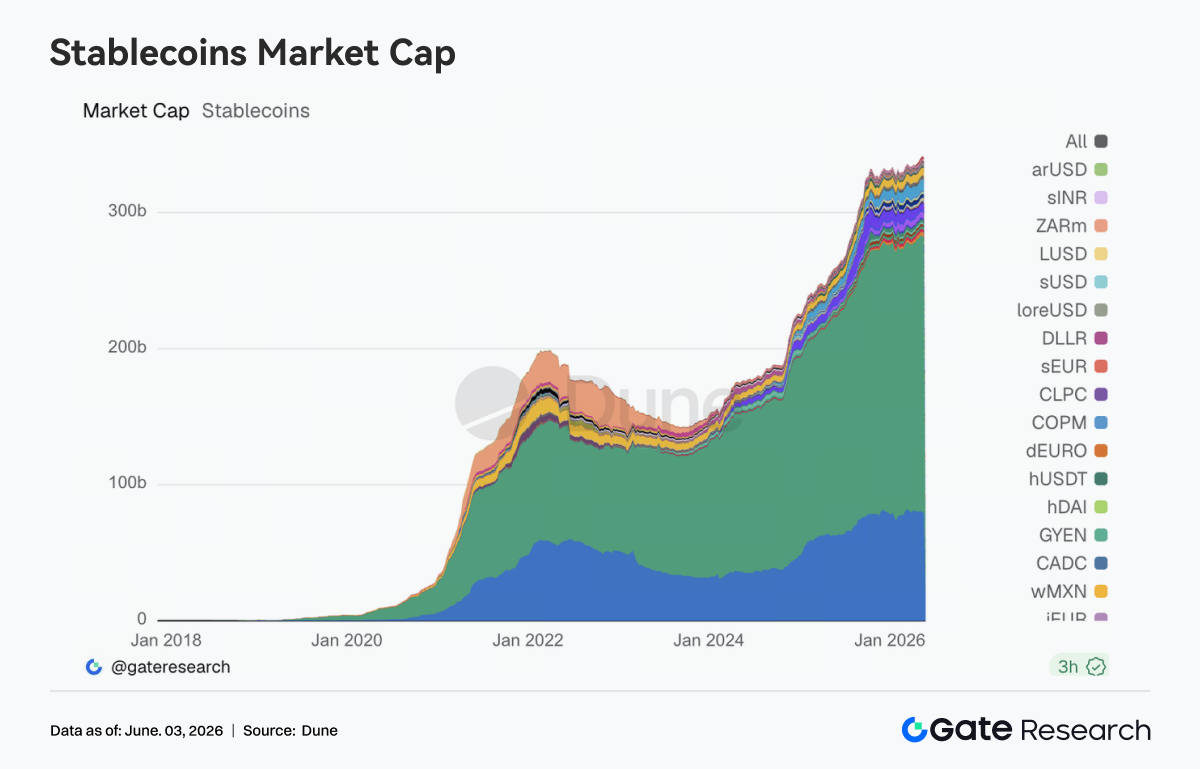

3.2 Stablecoins Enter a Phase Dominated by Compliance and Payment Narratives, USDC's Infrastructure Advantage Continues to Strengthen

The overall supply of stablecoins changed little last week, with no significant expansion for USDT or USDC. Assets like USDS, USDe, PYUSD, and USD1 maintained marginal growth, but capital did not flow centrally into any specific category of yield-bearing stablecoin products. Compared to supply changes, competition at the stablecoin infrastructure level is more noteworthy. Circle launched ChainBench on May 27, further promoting multi-chain development, USDC integration, and the construction of agent financial infrastructure. Earlier, Circle had also been continuously expanding the application scope of USDC within ecosystems like Hyperliquid, strengthening its role in collateral, settlement, and cross-chain capital flows. Concurrently, legislation related to stablecoins and market structure is still progressing. The ongoing interplay between the banking system and the crypto industry regarding revenue distribution, issuance models, and regulatory frameworks will continue to influence future product design.

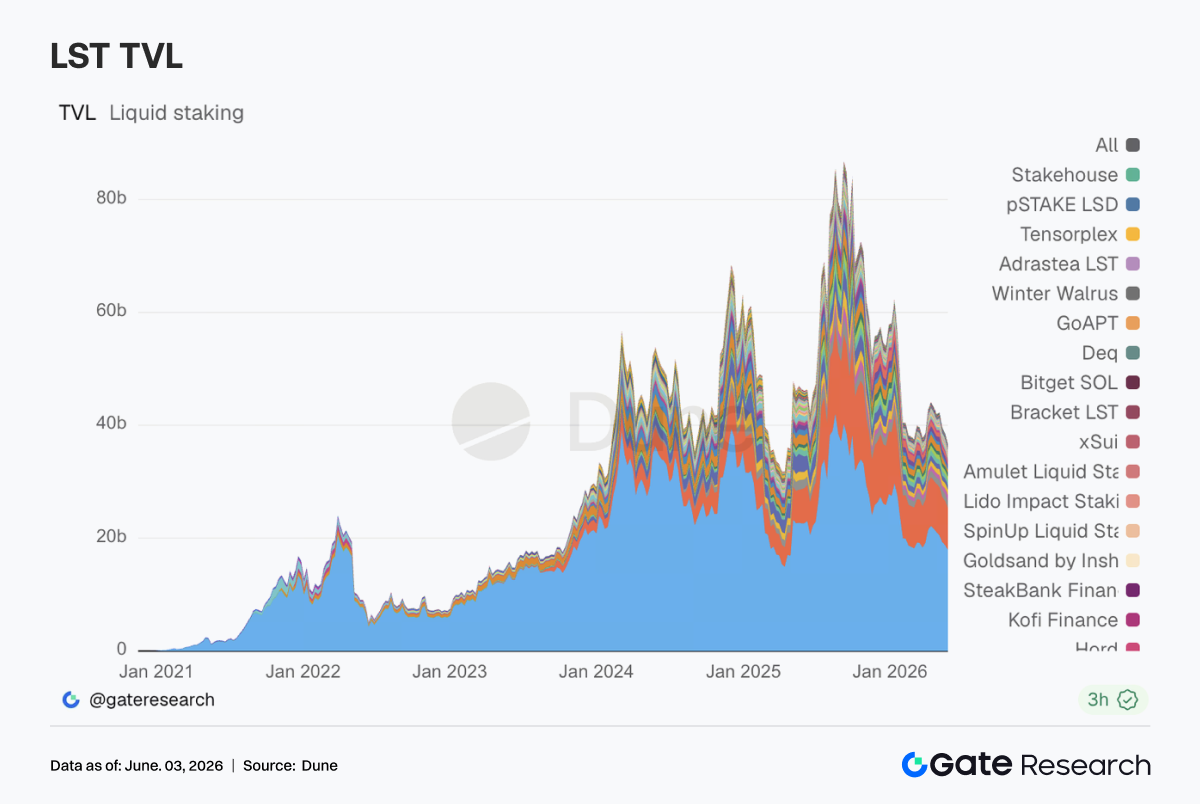

3.3 LST Sector Cools but Remains Stable; Market Reprices Cross-Chain and Security Premiums

The LST sector entered a moderate adjustment phase last week. Protocols like Lido and StakeWise on the ETH side saw varying degrees of TVL decline. Rocket Pool experienced a relatively larger adjustment, but short-term changes are also influenced by factors like asset prices, TVL calculation methodologies, and capital reallocation. In contrast, the SOL ecosystem showed relative stability. Protocols like Sanctum, Jito, and Jupiter Staked SOL broadly maintained their levels from the previous week. From an industry perspective, Lido recently explained its reasoning for choosing Chainlink CCIP for its cross-chain expansion, with core concerns focusing on cross-chain security, issuance control rights, and risk isolation mechanisms. Following the recent market discussions triggered by risk events related to KelpDAO and LayerZero, institutional capital has shown significantly increased attention to bridging security, redemption mechanisms, and governance transparency.

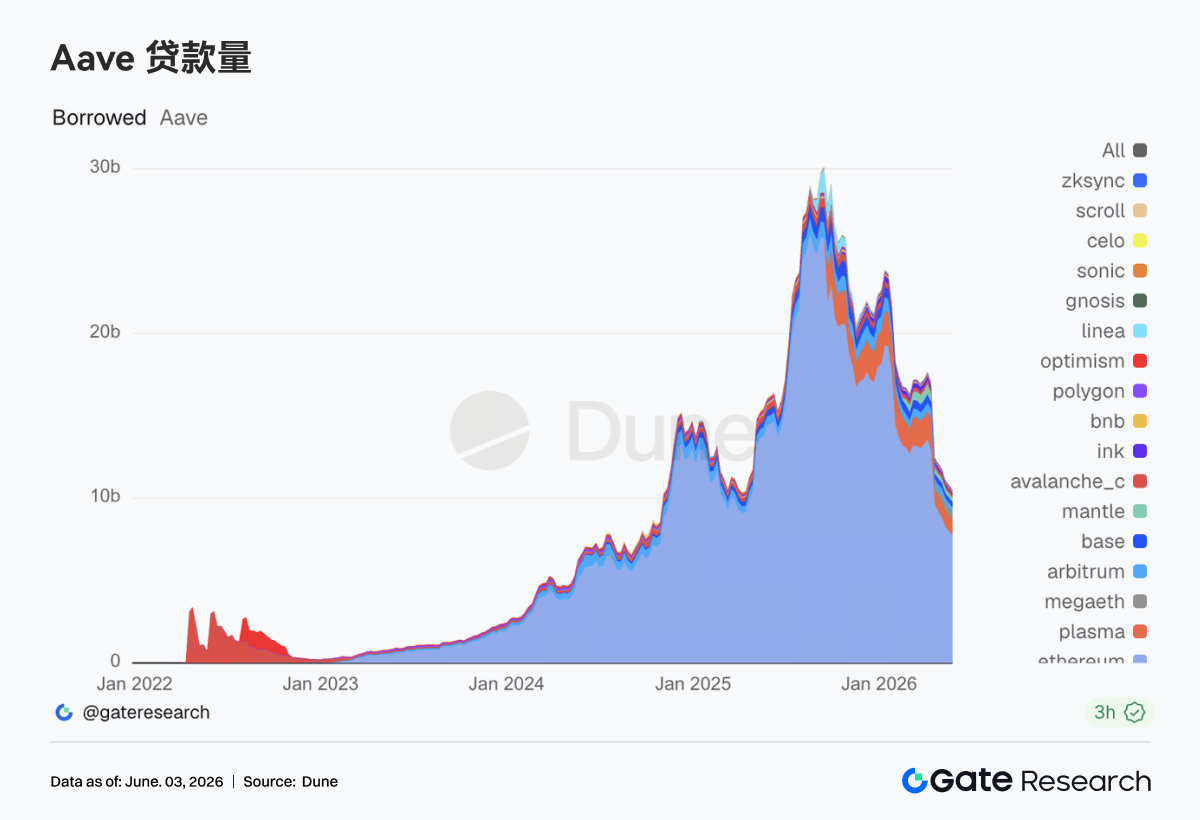

3.4 Aave Lending Balance Continues to Decline, Risk Appetite Recovery Still Underway

Last week, Aave's lending scale continued its slight downward trend. Overall activity on major markets like the Ethereum main market, Plasma, Arbitrum, and MegaETH was lower than the previous week. Although lending demand still exists, the market has yet to return to the expansionary pace seen before the risk events in April. The Ethereum market still holds a dominant position. Plasma and MegaETH, which had previously absorbed some capital inflows, have also entered a consolidation phase. Overall, the current performance of the lending market aligns with the environment of cooling risk appetite. Concurrently, Aave has been engaged in governance discussions regarding optimizing USDC liquidity buffer mechanisms, thawing WETH and restoring LTV, and rotating Emergency Guardian signers. This reflects the protocol's continuous efforts to refine its risk management framework and institutionalize previous emergency handling experiences.

3.5 Aave Core Asset Rates Return to Normal Range; Market Has Moved Past Liquidity Shock Phase

Lending rates for Aave's three core assets have generally stabilized. Borrowing costs for USDC and USDT have declined from earlier periods, while WETH rates have remained low and oscillated narrowly. USDC remains the most closely watched pool. Although there were periodic rate increases during the week, they were short-lived, and the overall volatility was significantly milder than the previous high-utilization phase. The governance discussions around improving USDC liquidity buffer capacity are fundamentally aimed at enhancing the protocol's stability and supply recovery ability during extreme utilization events. On the other hand, WETH borrowing costs did not rise significantly, indicating that the market has not yet re-established large-scale directional ETH leveraged positions. In conclusion, current lending demand is more focused on stablecoin circulation, arbitrage, and position management. While panic has subsided, the market maintains a degree of caution regarding tail risks.

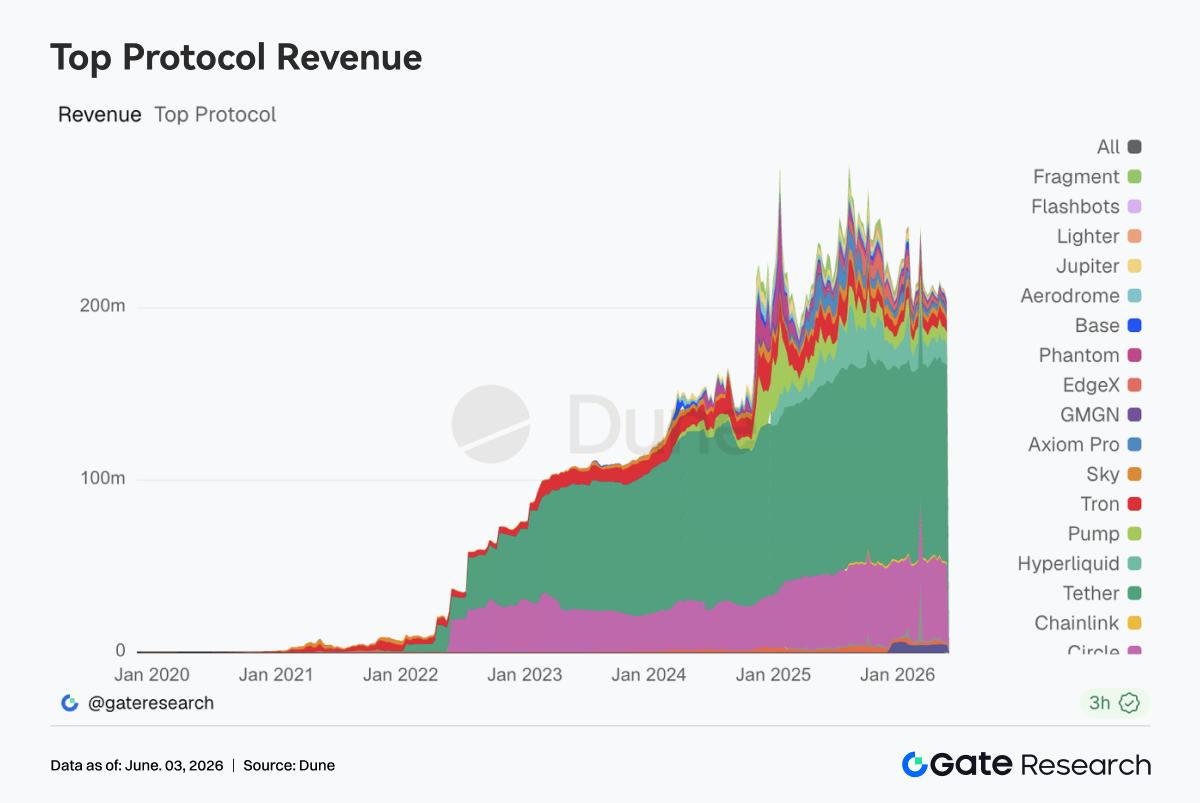

3.6 Protocol Revenue Returns to Financial Services Drive; Stablecoins and Trading Infrastructure Show Greater Resilience

Tether and Circle continue to top the revenue charts, with the stablecoin issuance business remaining the most stable source of cash flow across the industry. Although Hyperliquid's revenue cooled slightly from the previous week, it still operates at a high level, indicating that demand for on-chain derivatives trading has not weakened significantly. In contrast, protocols dependent on front-end traffic and Meme trading activity, such as Pump, PumpSwap, Phantom, and Axiom, generally saw revenue declines, suggesting speculative sentiment is gradually cooling. Aave V3's revenue dipped slightly, which is broadly consistent with the consolidation of lending scale and the normalization of interest rates, having returned to a normal operating phase. Looking at the revenue structure, the notable change last week was the market's shift back from being traffic-driven to being financial-services-driven. Capital is still willing to pay for settlement capabilities, leverage demand, liquidity services, and trading execution efficiency. However, the willingness to pay for pure traffic entry points and short-term attention assets is declining.

4. Derivatives Tracking

4.1 BTC Funding Rate Remains Positive but Price Weak, Leveraged Longs Under Pressure

From May 25 to May 31, 2026, BTC prices exhibited a low-range consolidating structure after a unilateral decline. Prices started the week near $77K but gradually weakened, falling to the $73K-$74K range from May 28 to May 31. Diverging from the price action, the funding rate turned positive after May 26 and rose to its weekly high around May 28-29, peaking near 0.01.

This combination of "falling prices but persistently positive funding rates" indicates that the market did not quickly turn bearish during the decline. Instead, it suggests some leveraged longs were either buying the dip or maintaining