Corning (GLW): A Three-Layer Value Breakdown – What Is the 100x PE Actually Paying For?

- Core Thesis: Corning's stock price has surged approximately 200% driven by growth in its AI optical communications business, pushing its P/E ratio above 100x. Its value needs to be understood across three layers: already delivered financial results, secured but not yet recognized orders (e.g., cooperation with NVIDIA), and the still-validating Glass Bridge technology. The market's high valuation heavily bets on the latter two layers, posing risks related to technology execution and customer concentration.

- Key Elements:

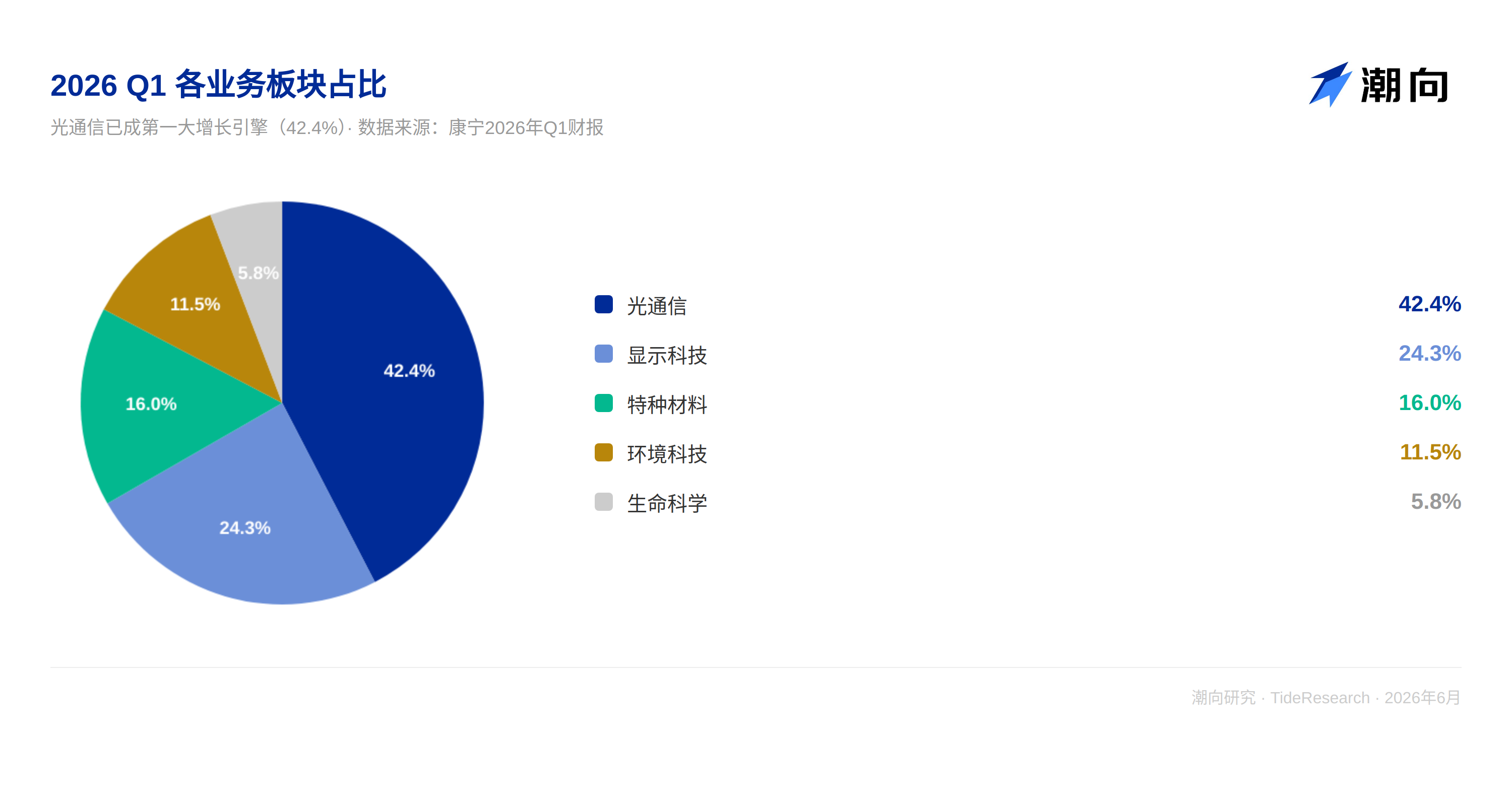

- Core Role: Corning positions itself as the turn-key optical fiber infrastructure contractor for AI data centers, offering a complete solution from optical fiber to optical connectors, benefiting from the "optical fiber replacing copper" trend.

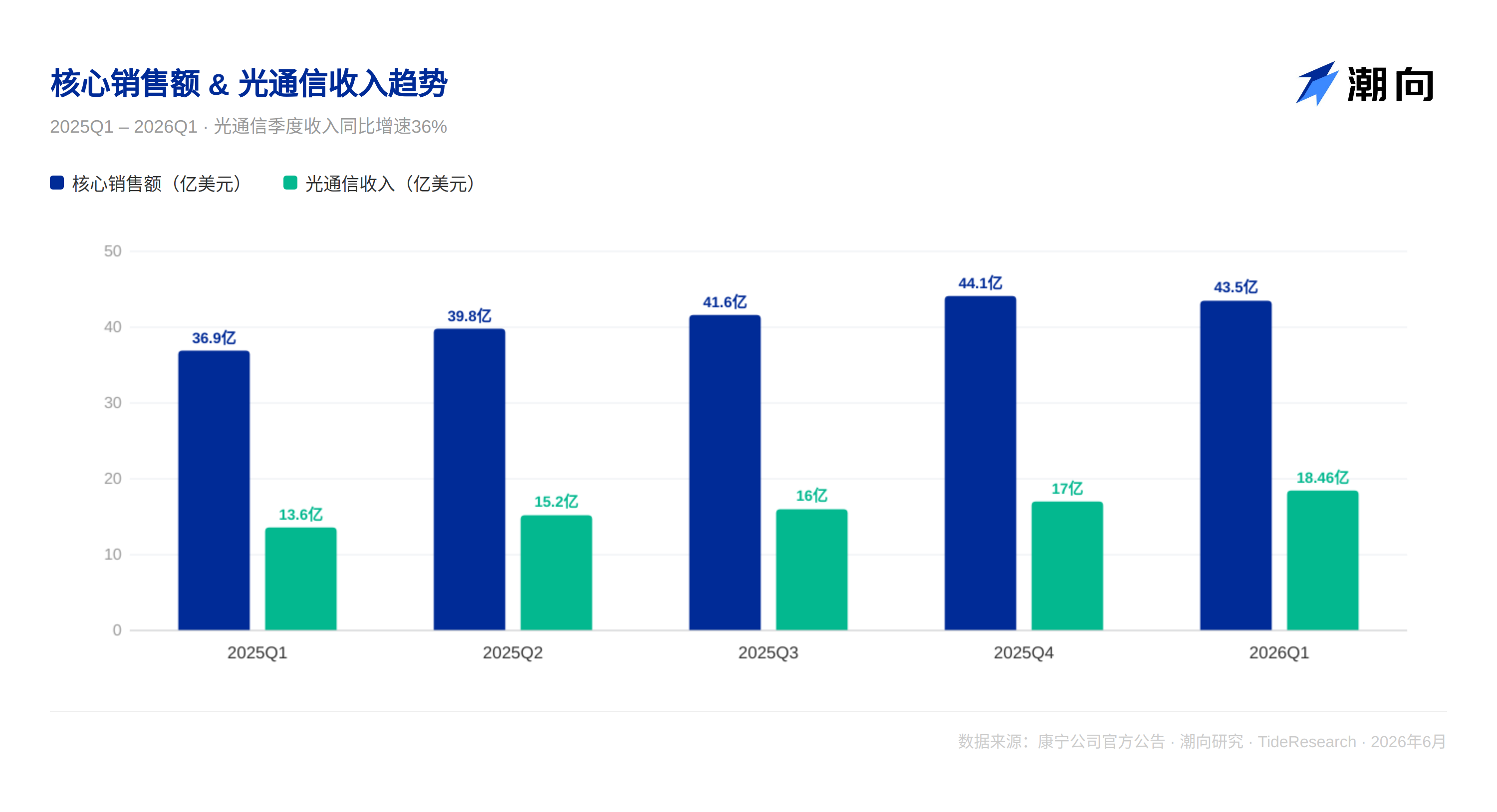

- Layer 1 Value: Q1 optical communications revenue reached $1.85 billion (+36%), net profit was $387 million (+93%), and the Springboard plan exceeded expectations, but this is already fully priced in by the market.

- Layer 2 Value: A strategic partnership with NVIDIA provides up to $3.2 billion in investment and prepayments to support capacity expansion. The Springboard target has been raised to $30 billion in annualized sales by 2028, underpinning the high valuation.

- Layer 3 Value: The Glass Bridge technology enables passive alignment optical connectivity, aiming to upgrade to an optical packaging solution. However, mass production validation requires 1-2 years, and it is positioned as a complement rather than a replacement.

- Risk Factors: The high valuation makes the stock sensitive to "in-line" results (falling nearly 9% post Q1 earnings). Customer concentration relies on cloud providers, while geopolitical and technology execution timelines remain uncertain.

Original Author: Chaoxiang Research

Corning, a 175-year-old glass company, has recently been making the market jittery.

On June 24, 2026, the day it announced its Glass Bridge technology, the A-share CPO sector plummeted over 6%. Capital frantically fled midstream manufacturers like Zhongtian Technology, FiberHome Communications, and YOFC, surging towards the glass substrate concept. The market deemed it a disruptive technology.

Two months prior, Corning's Q1 earnings showed optical communications revenue of $1.85 billion, up 36% year-over-year, with net profit surging 93%. The numbers were solid, yet the stock price plunged nearly 9% after the earnings report. The reason was simple: Q2 guidance was "in line with expectations," not "a beat."

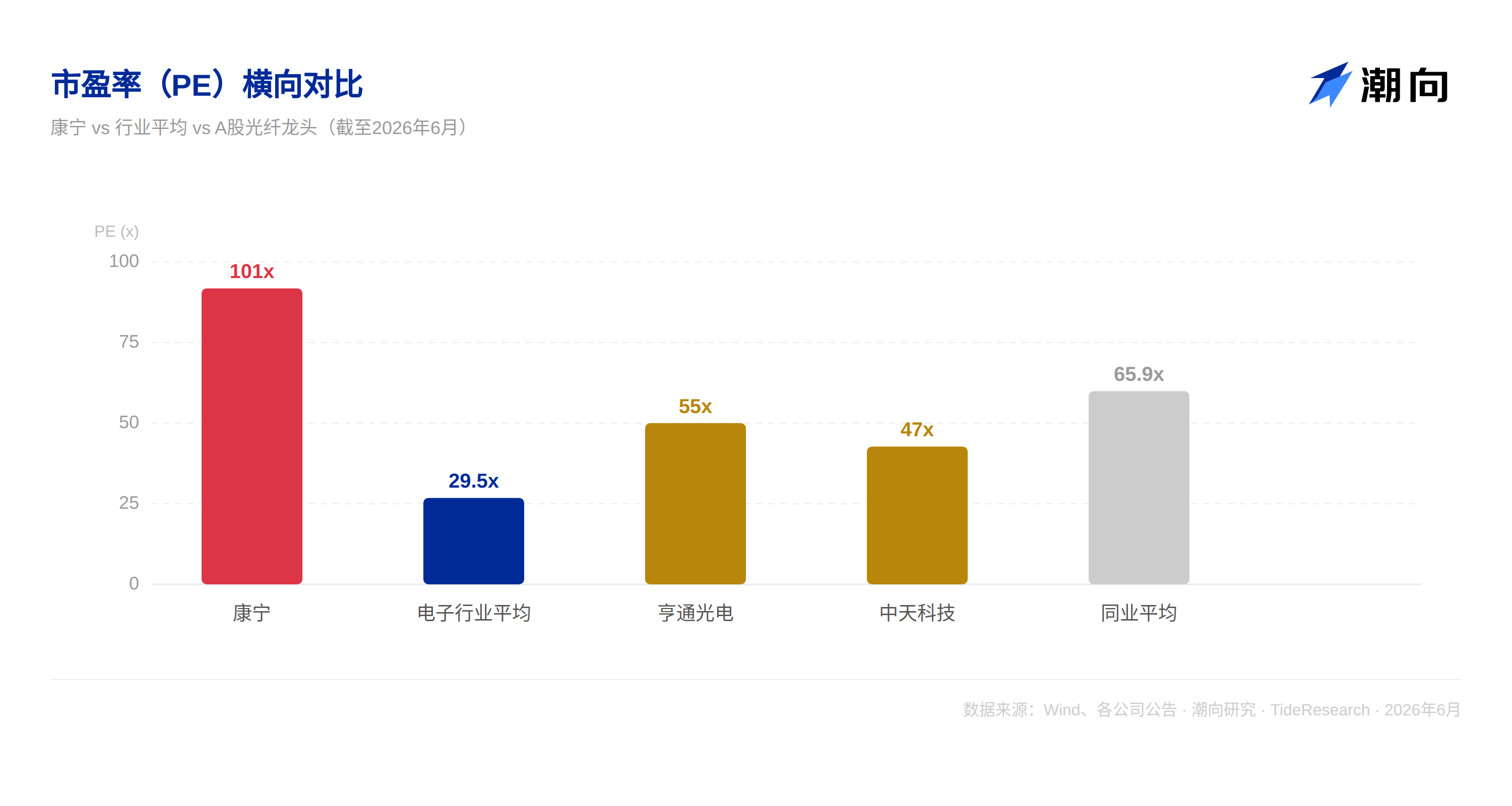

On one hand, a frenzy over "disruption," on the other, a stampede on "in-line expectations." Corning's stock has risen about 200% from its early-year low, pushing its P/E ratio beyond 100x.

Most people misunderstand Corning by treating it as a optical module company or optical fiber manufacturer, then applying industry average valuations. The real question is far more complex.

After sifting through public information, we found it can be explained in three layers.

I. What Role Does Corning Actually Play in the AI Supply Chain?

First, let's get Corning's positioning right. It's neither an optical module company nor a small fiber manufacturer.

Corning's core role is the general contractor for optical fiber infrastructure in AI data centers. As AI models scale from hundreds of billions to trillions of parameters, hundreds of thousands of GPUs within a data center must exchange massive amounts of data over very short distances. Traditional copper cabling has become inadequate in terms of bandwidth and energy efficiency. As the inventor of low-loss optical fiber, Corning stands at the center of the irreversible technological trend of "optics replacing copper."

Corning's uniqueness lies in the fact that it doesn't just sell fiber; it sells complete optical connectivity solutions. From fiber to connectors, from intra-data center interconnects to intercity backbones, from traditional fiber array units to the latest Glass Bridge wafer-level optical interconnects. Management stated on the earnings call: "We are transforming from a materials company into a system solutions provider."

But this "system solutions provider" faces a set of sharp contradictions. The most certain parts are already priced in, while the most valuable parts have yet to be realized. To calculate this equation, we divide Corning's value into three layers. The only dividing line is: has this money already appeared in the financial statements?

II. Layer One: Already Reflected in the Financials

Open the Q1 earnings report and you'll see:

Optical Communications is the absolute engine. Revenue of $1.85 billion, up 36% year-over-year. Net profit of $387 million, a massive 93% increase year-over-year. Both Enterprise Network and Carrier Network segments grew 36% simultaneously, indicating demand isn't concentrated on a single customer. Core operating margin expanded from 16.3% at the launch of the Springboard plan to 20.2%. Profit growth far outpaces revenue growth, fully demonstrating operating leverage.

Customer acquisition has been exceptionally aggressive. In Q1, Corning finalized a multi-year fiber supply agreement with Meta worth up to $6 billion. It also added two new hyperscale customers, each at a scale comparable to the Meta deal. On the carrier side, Corning signed and extended a multi-year cooperation agreement with Lumen.

The Springboard plan is outperforming expectations. Since its launch in Q4 2023, core revenue has grown a cumulative 33%, EPS by 79%, and core operating margins have expanded by 390 basis points.

This layer is solid, and the market has fully priced it in. In fact, it might already be overpriced.

But no matter how high the certainty of Layer One, it alone cannot support a 100x P/E ratio. The real divergence lies in the next two layers.

III. Layer Two: Secured But Not Yet Booked

This is the most controversial part of Corning's current valuation and the fundamental reason the market is willing to offer a high premium.

NVIDIA Strategic Partnership. On May 6, 2026, NVIDIA and Corning announced a multi-year strategic partnership. Corning will build three new advanced manufacturing plants in the US, increasing optical connectivity capacity tenfold, expanding fiber capacity by over 50%, and creating over 3,000 jobs. This is capacity expansion, but more importantly, it marks Corning's transformation from a materials supplier to a core partner in AI infrastructure.

NVIDIA has the right to invest up to $3.2 billion in Corning, including an immediate $500 million prepayment for 3 million shares, plus an additional $2.7 billion to subscribe for up to 15 million shares at $180 per share. Corning's CFO explained at a JPMorgan conference: "NVIDIA provided billions in prepayments to support capital deployment, in addition to an equity investment."

The customer is funding your capacity expansion. This fundamentally changes the risk profile of capital-intensive expansion. Orders are locked in; Corning doesn't need to build the factory first and then wait for customer orders.

Upgraded Springboard Targets. On May 6, during Investor Day, Corning significantly raised its Springboard targets: annualized sales of $30 billion by the end of 2028 and $40 billion by the end of 2030. This implies Corning needs to more than double over the next 4 to 5 years. Management defined the $35 billion to $40 billion range as "high confidence targets."

The COO explained: when AI cluster sizes exceed 130,000 GPUs, the network will add a third switching layer, fueling an additional 50% growth for Corning. The enterprise business is expected to grow at 1.3 to 1.5 times the rate of GPU growth.

This layer supports the core of Corning's valuation premium. But it's important to note that $30 billion and $40 billion are targets, not contracts. A significant portion of these figures still relies on "clients in discussion," not "signed orders."

The market has already priced in a considerable amount of expectation for Layer Two. However, what truly makes Corning a "completely different valuation species" rather than just a "larger-scale fiber company" is Layer Three.

IV. Layer Three: Still Being Validated, Not Yet Signed

Let's return to the opening scene. On June 24, Corning launched Glass Bridge, and the A-share CPO sector crashed 6%. What was the market fearing? What was it excited about?

Glass Bridge creates optical waveguides inside glass using a wafer-level ion-exchange waveguide process, enabling direct optical connectivity between fibers and photonic chips. Traditional solutions require precise active alignment of fiber array units; Glass Bridge achieves passive alignment. Each connector supports 24 fiber channels, with coupling loss controlled within 1.5dB, and is deeply integrated with GlobalFoundries' silicon photonics platform.

If this technology achieves mass production, the business of traditional fiber array unit suppliers will face long-term contraction. This is why the CPO sector crashed. Capital voted with its feet, seeing this as the beginning of a restructuring of the industry's value chain.

But let's calmly look at a few facts.

First, Corning officially positions it as a complement to, not a replacement for, existing solutions. Traditional fiber array units remain effective for current applications; Glass Bridge targets incremental demand in scenarios requiring extremely high fiber counts. They will coexist long-term, not substitute each other.

Second, mass production and validation will take at least 1 to 2 years. The validation cycles with wafer-level manufacturing and top-tier cloud providers are simply that long. Mainstream computing hardware will still rely on traditional solutions through 2026 and 2027. Corning itself continues to advance the R&D and expansion of its next-generation fiber array units.

Third, Glass Bridge is not Corning's only bet. Chip-level optical coupling is a multi-pronged race. NVIDIA, Broadcom, and Intel each have differentiated photonic chip solutions, and no unified standard exists. Corning's Glass Bridge must be compatible with the GlobalFoundries platform to be effective.

Layer Two determines Corning's revenue growth for the next 2-3 years. Layer Three determines whether Corning's valuation framework can be rewritten. If Glass Bridge merely sells a few more connectors within the existing optical module supply chain, it won't support a 100x P/E ratio. However, if it can upgrade Corning from "selling connectors" to "selling optical packaging solutions," the market's pricing logic for Corning becomes entirely different. This is the true value of Glass Bridge, and also its greatest uncertainty.

V. Putting the Three Layers Together: What Is the 100x P/E Actually Pricing In?

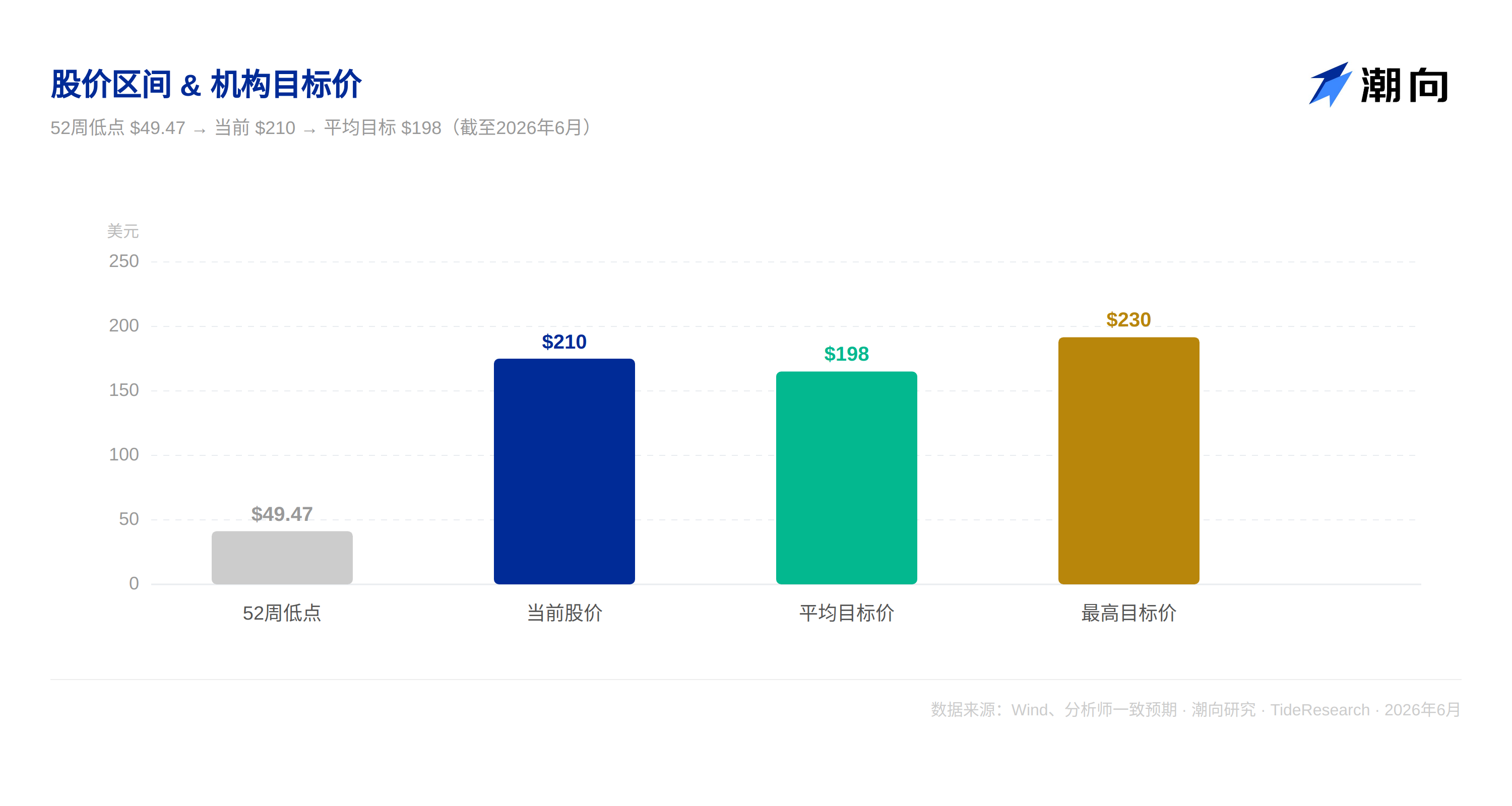

As of late June, Corning's stock price was around $210, with a P/E ratio of approximately 100x. This valuation level is typically given to software companies, not capital-intensive manufacturers.

The average price target from 16 analysts is $198, with a range from $149 to $230. UBS raised its target from $223 to $228 on June 8, while Truist raised its from $149 to $205. Morgan Stanley and Barclays have targets of $180. Analyst opinions are significantly split: 10 "Buys," 5 "Holds," and 1 "Sell."

Look at the three layers together. Layer One: Existing optical communications business and realized Springboard profits. High certainty, fully priced. Layer Two: NVIDIA partnership for expansion and upgraded Springboard targets. Medium certainty, partially priced. Layer Three: Large-scale commercialization of Glass Bridge. Low certainty, with market sentiment potentially over-reacting.

Conclusion: If you only consider the certainty of Layer One, Corning isn't worth this price. A significant portion of the current valuation is paying for Layer Two and Layer Three, and the realization of these layers will take at least 2 to 3 years.

VI. Don't Let Glass Bridge Cloud Your Judgment

Corning's story is compelling, but amidst the optimism, investors must stay clear-headed about the following risk factors.

Technology Realization Timeline. Glass Bridge is a long-dated option, not a near-term catalyst. This is the easiest risk for the current market to misjudge. On the day the A-share CPO sector crashed, the market had already priced in the "disruption" narrative. But Corning's official communication is clear: mass production and validation will take at least 1 to 2 years. This means that in the 2026 and 2027 financial reports, Glass Bridge's revenue contribution will be nearly negligible. If customer validation progress falls short of expectations in 2027, the "technology premium" embedded in the current valuation could face a concentrated sell-off.

Customer Concentration. Corning's revenue growth is highly dependent on a few hyperscale cloud vendors. If one of these customers decides to develop in-house solutions or switch suppliers, Corning's orders will come under direct pressure. Cloud providers are increasingly inclined towards developing their own chips and networking solutions. Amazon's Annapurna team, Microsoft's Maia, and Google's TPU – these trends are eroding traditional supply chains while also changing the procurement decision-making logic of Corning's customers.

Geopolitical Risks. Corning faces dual pressure in China. The US may impose stricter controls on the export of high-end technology, while Chinese domestic manufacturers are accelerating their efforts to catch up. Both factors threaten Corning's long-term competitiveness in the Chinese market.

Valuation Itself. A static P/E ratio exceeding 100x has already priced in a multitude of optimistic expectations. Following the Q1 earnings release, the actual performance numbers weren't bad. However, simply because the Q2 guidance was "in line" rather than "a beat," the stock fell over 10% in pre-market trading and closed down nearly 9%. This is the rule for high-valuation stocks: You must beat expectations every single time. Any "in line" report is treated as a negative signal.

VII. A Compelling Story at a Steep Price

Corning is a company with solid fundamentals and a clear strategic direction. Optical communications is experiencing sustained high growth amid the AI computing infrastructure boom. The deep partnership with NVIDIA and the upgraded Springboard targets provide a narrative for long-term growth. The Glass Bridge technological breakthrough represents a promising long-term industry direction.

However, a good company is not always a good investment at any price.

With a P/E ratio exceeding 100x, Corning has become one of the most sensitive AI infrastructure stocks in the US market – most critical of "good news" and most vulnerable to "bad news." The post-Q1 earnings plunge proved this; an "in-line" report was enough to trigger a nearly 9% drop.

For long-term investors, Corning's strategic position in AI optical communications, the capital commitment from NVIDIA, and the long-dated option value of Glass Bridge are all worth monitoring. However, at the current valuation, waiting for a pullback to a price with a better margin of safety might be the more prudent choice. If the stock price were to return to the $150–$170 range, the risk-reward profile would improve significantly.

For short-term traders, key catalysts to watch include: quarterly order announcements, tangible progress in Glass Bridge customer validation, and the stage-by-stage achievement of Springboard targets.

Disclaimer: This article is for analytical reference only and does not constitute any investment advice. Stock markets involve risks, and investment should be undertaken cautiously. All data is derived from public information, and the author assumes no responsibility for its accuracy or completeness.