CXMT IPO Is Imminent, National Team Enters the Fray: Where Else Can the Memory Supply Chain Capital Flow?

- Core Thesis: While "CXMT concept stocks" have broadly risen, the underlying logic has clearly diverged. Stocks in the general DRAM expansion chain (equipment & materials) are near historical highs, with intense capital betting; the HBM packaging chain's earnings are not expected until late 2026, placing them at relatively lower levels. Long-term capital is reducing positions at these highs, with short-term speculative money taking over, making short-term chasing a high-risk, low-reward play.

- Key Factors:

- CXMT's Q1 2026 revenue growth was primarily driven by a 57% QoQ increase in average selling price (ASP), while bit shipments only grew 11%. Profitability remains dependent on the industry cycle rather than a technological breakthrough.

- Stocks in the general DRAM expansion chain (e.g., NAURA Technology, Hwatsing Technology) are generally near their 52-week highs. While the logic is soundest, it is already fully priced in. The HBM packaging chain (e.g., Lianrui New Materials, SJ Semiconductor) still has about 18% upside potential from its highs, but the payoff timeline is later.

- Industrial capital and the "National Team" are reducing holdings at elevated levels: GigaDevice's actual controller, Zhu Yiming, reduced holdings by approximately 6.33 million shares; the National IC Fund cashed out about 3.882 billion RMB from NSIG; Central Huijin reduced positions in broad-based ETFs.

- Short-term speculative capital is driving pricing: northbound capital increased investments by ~400 billion RMB year-to-date, margin financing scale is around 2.8 trillion RMB, premiums on chip ETFs once exceeded 30%, and regulators have initiated cooling measures.

- Mid-term signals to watch: the inflection point in DRAM spot prices, the pace of capital expenditure deployment after CXMT's listing, whether industrial capital reductions expand, and whether chip ETF premiums can converge.

Original Author: David, ChaoXiang Research

In the past couple of days, positive news for the storage sector has come one after another.

On June 29, South Korea launched a mega semiconductor plan totaling over 1,000 trillion won (approximately $650 billion), with an official goal to double DRAM production capacity within five years.

Meanwhile, China's DRAM leader CXMT passed its listing review, with the market expecting it to be listed between mid-July and early August. Institutional valuations are calling for 2 trillion to 4 trillion yuan. Coupled with the judgment that major storage manufacturers face shortages until 2028, the reasons to be bullish on storage and semiconductors have never been as clear-cut and aligned as they are now.

At the same time, this sentiment has even spilled over to overseas networks.

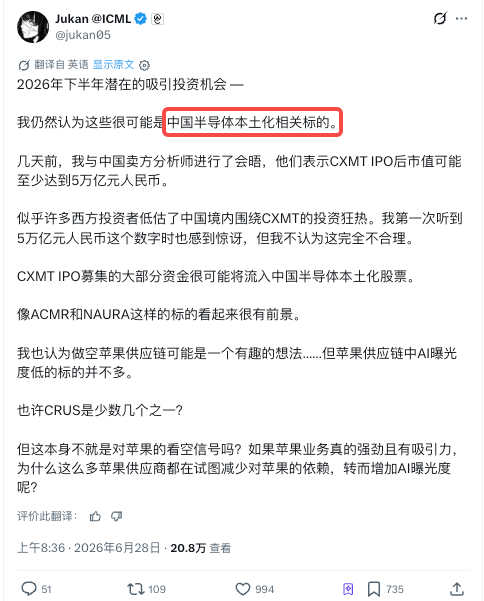

Jukan (@jukan05), a well-known tech investment blogger on X, posted that the most worthwhile direction to bet on in the second half of 2026 might still be China's semiconductor self-sufficiency targets.

Citing a conversation with a Chinese sell-side analyst, he stated that CXMT's market cap after its IPO would be at least 5 trillion yuan, and most of the funds raised would flow into stocks related to domestic semiconductor self-sufficiency. Therefore, he believes targets like ACMR and NAURA still have prospects.

However, rushing in on this wave isn't necessarily always the right timing.

Currently, nearly 30 CXMT concept stocks on the A-share market have a combined market cap exceeding 1.9 trillion yuan. Most leading stocks across the industrial chain's upstream and downstream are generally trading near their 52-week highs. Blindly rushing in is certainly not the optimal strategy.

After a round of gains, there are few links left where market expectations haven't been filled.

Prices Soared, But Sales Volume Barely Budged

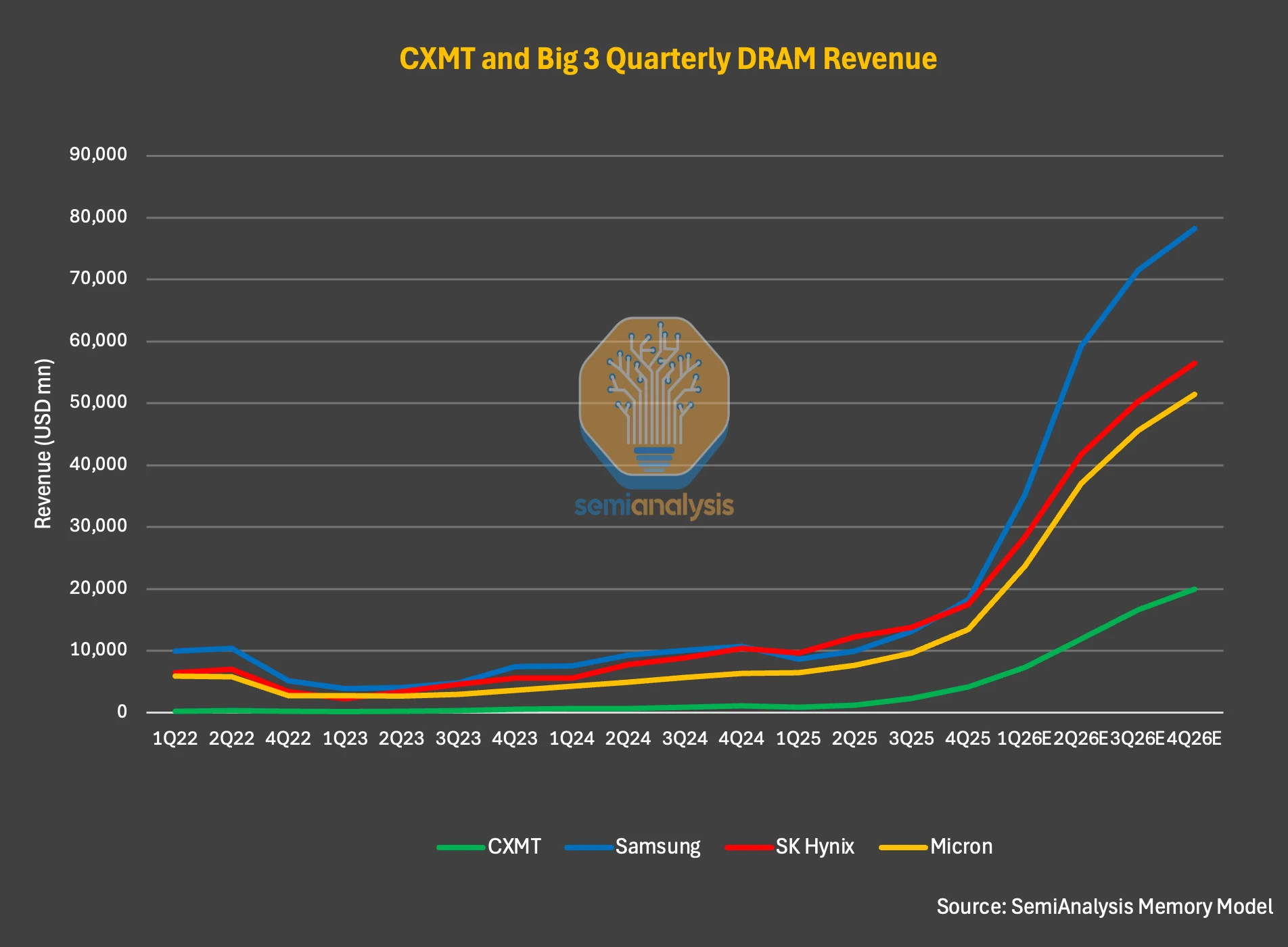

In its June 23 report, "China's CXMT Is Set to Challenge DRAM Incumbents," the US semiconductor research firm SemiAnalysis broke down some data:

In the first quarter of 2026, CXMT's bit shipments grew only 11% quarter-over-quarter, while its average selling price (ASP) surged approximately 57% quarter-over-quarter. Bit shipments measure the actual quantity of goods sold based on storage capacity, gauging "how much was sold"; ASP measures "how expensive the goods were sold."

Putting these two numbers together means that during this quarter, CXMT barely sold more goods; rather, it sold them at higher prices.

Therefore, SemiAnalysis concluded that CXMT's explosive profitability this round relies on the industry cycle itself, rather than a breakthrough in technology or market share.

In a price-driven market, the first to profit are the original manufacturers directly selling chips: Samsung, SK Hynix, Micron, and CXMT itself. Their profits scale linearly with ASP, making them the biggest gainers over the past year.

SK Hynix's stock price once surged over 350% this year. However, at this point, expectations along the original manufacturer chain are already fully priced in: Samsung and SK Hynix currently trade at forward price-to-earnings ratios of only 3 to 5 times. While seemingly cheap, this reflects the market having already factored in the AI-driven demand and profits expected from 2026 to 2027 into their stock prices.

The profits realized through price increases are largely recognized by the market. The same applies to the batch of A-share storage original manufacturers and module stocks; gains have been substantial, leaving limited room for further entry. As for the upstream expansion chain (such as equipment and materials), whether it has been bought up to the same level will be examined later with data; we won't draw conclusions here yet.

Overall, I believe CXMT stands at a delicate crossroads:

On one hand, selling DRAM and profiting from price increases makes it a beneficiary of this cycle. On the other hand, using the 295 billion yuan raised from its IPO for expansion—buying equipment and materials upstream—makes it a spending client.

In the past month or two, a prevailing sentiment in the market has been to directly "buy CXMT's upstream and downstream"; in hindsight, blindly going all-in has indeed yielded substantial returns. However, at this current position, if one judges that the storage and semiconductor rally will continue, it's essential to clarify several things:

First, where exactly in the industrial chain does your target lie, and from what does it benefit?

Second, is its current price still at the foot of the mountain, or has it already climbed to the midpoint or even the summit?

Let's address the first question first.

"CXMT concept stocks" is an overused label. Breaking it down, the demand driven by CXMT follows two paths, benefiting different sets of companies with different realization timelines.

The first path is the expansion chain for standard DRAM. Currently, 99% of CXMT's shipments are standard DDR and LPDDR. Of the 295 billion yuan raised from the IPO, over 220 billion yuan is explicitly earmarked for equipment procurement for wafer fabs and technology upgrades. This money primarily flows to front-end equipment—the machinery for making chips—which represents the largest investment in expansion. Once production lines are operational, they will continuously consume materials.

Representative companies in the equipment segment include NAURA (002371), AMEC (688012), Piotech (688072), Hwatsing (688120), and ACMR Shanghai (688082). In the materials segment, we have Anji Microelectronics (688019), Fuyuan Century (300666), Yoke Technology (002409), and National Silicon Industry Group (688126). This chain benefits from the money CXMT is spending right now, offering the highest order certainty.

The second path is the HBM chain, which involves different players. HBM is the high-bandwidth memory required for AI servers and is technically more challenging than standard DRAM. CXMT's HBM production is still catching up, with mass production expected only by the end of 2026, lagging behind standard DRAM expansion by one cycle. More critically, HBM's value lies not in front-end etching and deposition but in the packaging phase—stacking, bonding, and molding multiple chips. Therefore, the beneficiaries in the HBM segment are a different set of companies:

Testing equipment provider Jingzhida (688627), packaging material suppliers Huacheng Sci-Tech (688535), Lianyungang Zhongfu Lianzhong (688300), Shanghai Sinyang (300236), and advanced packaging & testing firms Shenghe Micro (688820) and Tongfu Microelectronics (002156).

Upstream and Downstream: Lonely at the Top?

Laying out the targets from the two chains above and ranking them based on their current price relative to their 52-week high provides a clear visual of where capital has swept through. The data below is as of intraday on the 29th.

A clear dividing line is visible in the table.

For standard DRAM equipment and materials, almost all targets are trading near their 52-week highs, mostly within 3% of the year's peak. On June 29, Hwatsing hit its daily limit up, closing at a record high. Yoke Technology also refreshed its high, while AMEC, Anji Micro, and National Silicon Industry Group all saw gains around 10%.

This segment is the market-recognized "shovel seller for CXMT expansion," possessing the strongest logic and highest certainty, leading capital to buy it up fully. In other words, the certainty of the expansion chain is already priced in.

Trailing behind is the HBM packaging segment.

Lianyungang Zhongfu Lianzhong is still about 18% below its 52-week high, closing lower against the market trend on June 29. Shenghe Micro is similarly about 18% from its high. Testing and packaging firm Tongfu Microelectronics is about 9% from its high. Their lag isn't because they are cheaper or overlooked, but rather due to a later realization timeline:

CXMT's HBM production line won't be operational until the end of 2026. The orders and performance for this group of companies will only truly be released once the production line is running and yields improve. Their current lower positions reflect "it's not their turn yet." Viewing them purely as "bargains" might incur time and opportunity costs.

As for the overall conclusion, it is already clear.

The so-called "buying CXMT's upstream and downstream" is no longer a question of whether to get on board; we need to assess whether they are already at the summit.

Looking just at price, equipment and materials on the standard DRAM side are mostly at their highest points in a year; cheap entry points are gone. The HBM packaging segment is slightly lower, but requires willingness to wait.

Furthermore, price only answers half the question of "expensiveness." The remaining half, which price itself cannot explain, depends on whose money is buying and selling at this level.

Hot Money Supports, While Others Retreat

The essence of this layer is that pricing power has shifted from long-term capital focused on fundamentals to short-term speculative money driven by sentiment.

On one side, industrial capital, the National Integrated Circuit Industry Investment Fund (Big Fund), and state-backed teams are systematically reducing holdings at high levels. On the other side, hot money and retail investors are rushing in, leveraging the AI theme. The former, perhaps the most knowledgeable about this business, are selling; the latter, seeking to buy low and sell high, are buying.

Let's look at the retreating side first. We have compiled the following from public information:

- Zhu Yiming, the de facto controller of GigaDevice, reduced his holdings by approximately 6.33 million shares between May 11 and 25 (company announcement). He is also the founder and chairman of CXMT—the person who should be most bullish on the CXMT chain—yet he reduced his stake in a leading related company at highs.

- The National Big Fund has been continuously reducing its holdings in National Silicon Industry Group since January, cashing out a total of approximately 3.882 billion yuan by early June (company reduction announcement).

- Multiple heavyweights in the semiconductor sector, including Montage Technology, Hygon Information, and Piotech, have seen shareholders reduce holdings after stock price surges in 2026 (various company announcements).

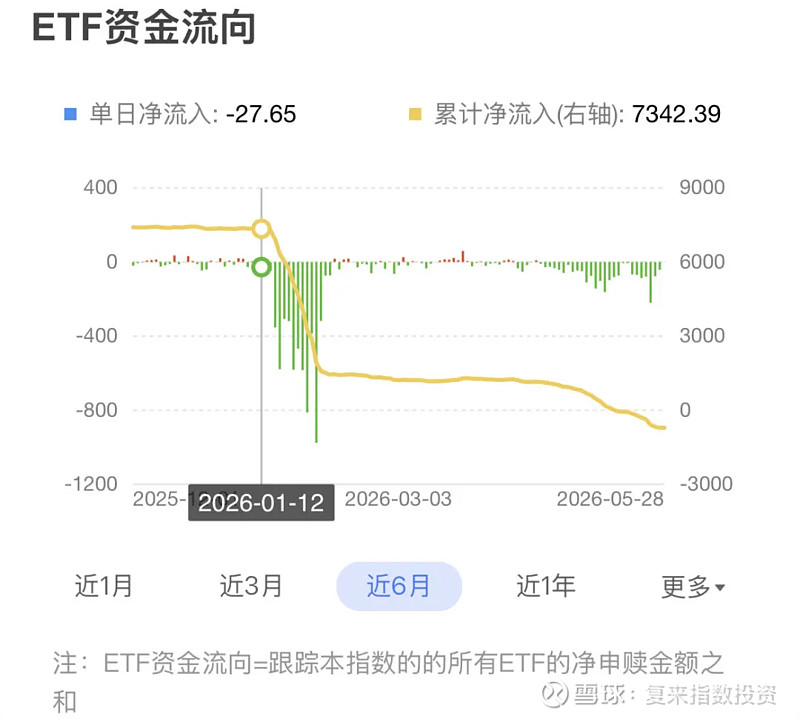

- State-backed teams (Central Huijin) reduced their holdings in broad-based ETFs like the CSI 300 at high levels (per *Caijing*'s estimates based on Central Huijin's positions and fund circulating shares). Their reduction wasn't specifically targeting semiconductors but was a counter-cyclical pullback from the overall high market, and semiconductors represent the segment with the largest gains and most reason to realize profits.

Image source: Fulai Index Investment's Xueqiu Column

The motivations for these reductions cannot be generalized. The Big Fund has an exit cycle, and reducing holdings upon share maturity to recover capital is a routine operation. The state-backed teams adjusting broad-based holdings might be counter-cyclical rebalancing rather than a bearish view on a specific sector. Reasons for industrial capital and executive reductions also vary.

Interpreting them as "collective bearishness" would be an overstatement, but one thing is certain:

At current price levels, these original long-term holders have chosen, almost in unison, to realize part of their gains. Regardless of motivation, this action itself conveys that the current price has reached a level where long-term funds are willing to lock in profits.

Now, let's look at the buying side.

According to market data cited by Sina Finance, the main force driving this tech rally is hot money:

Northbound capital added approximately 400 billion yuan year-to-date, while margin financing expanded to about 2.8 trillion yuan. This type of money bets on themes and momentum. Whether a stock is near its 52-week high or has a high P/E ratio doesn't affect their entry; they buy the rally itself.

Regulators have also sensed the overheating, applying the brakes by raising margin financing deposit ratios and suspending trading to investigate consecutive limit-up stocks. Chip-related ETFs have frequently been suspended due to large premiums over their net asset value, with premiums once exceeding 30%.

Putting the buyers and sellers together, the conclusion is straightforward:

At current levels, long-term capital related to storage and semiconductors is taking profits in batches, while short-term hot money is picking up the baton. Marginal pricing power at this stage increasingly lies in the hands of capital driven by speculative sentiment.

Note: This does not necessarily mean the market will peak immediately. Storage shortages lasting until 2028 and CXMT's expansion require real capital. However, most institutions' judgment is that the sector will digest profit-taking through sharp volatility, entering a phase that prioritizes performance delivery, rather than experiencing a trending decline.

My Views

Combining the two layers of judgment above with the fund flow picture, I believe the inclination is as follows.

In the short term (around CXMT's listing period), sentiment has inertia. The enthusiasm from the new stock subscription and concept fermentation on the listing day could give the sector another boost. However, this is the final part driven by sentiment. Moving forward, it increasingly becomes a game of passing the baton, where the risk of chasing highs outweighs the potential returns.

In the medium term (looking at CXMT's HBM production line realization), what is truly worth waiting for is the diverging realization between the standard DRAM expansion chain and the HBM chain. Equipment and material orders depend on the speed of capital expenditure execution after CXMT's listing. For those HBM packaging stocks with lower positions, their time won't come until the production line starts operation and yields ramp up by the end of 2026. Positioning now is effectively betting on timing.

Several signals worth watching:

- **The inflection point of DRAM spot prices.** The foundation of this cycle is price increases. If spot prices turn downward, the original manufacturers and module makers benefiting from price hikes will be the first to react.

- **CXMT's capital expenditure pace after listing.** Most order fulfillment depends on these figures;