Coding's betting panel made money, but Polymarket is really not a good place for "arbitrage"

- Core Argument: Polymarket is not a stable income tool suitable for arbitrage. Its binary market structure harbors tail risk and a mathematical expectation trap. The core value of building your own risk control panel (T1/T2/T3 tiers, thematic cluster exposure monitoring) lies in disciplined risk management rather than profit statistics. The sustainability of the tested 30%+ returns relies on information asymmetry and position diversification.

- Key Elements:

- Panel Construction Logic: By using two tabs, "Position Dashboard" and "Opportunity Monitor", to achieve real-time PM data fetching, tier-based risk control (Tier), thematic cluster exposure caps (12%), and pop-up alerts for anomalies, thereby reducing emotional betting.

- Mathematical Expectation Trap: Even if q≥c (e.g., q=90%, c=80%), a wrong judgment results in a 100% loss, not the expected 12.5% profit. The long-term IRR of high-conviction bets might only be 3-4%, locking up capital and missing better opportunities.

- T1/T2/T3 Tiering Principles: T1 (high conviction) requires controlling long-term positions to avoid capital efficiency loss; T2 (has edge) has a single-bet limit of 8-10%, allowing for mistakes; T3 (high odds) uses minimum positions for contrarian bets to build market intuition.

- Tail Risk Quantification: For 10 consecutive independent bets with a 95% win probability, the chance of at least one loss is ≈ 40%. In reality, correlations between multiple markets (e.g., Middle East theme) create collective loss risks.

- Practical Advice: Don't treat it as a stable income tool. High win rate doesn't equal a good trade (requires comparing the q-c spread). Avoid pseudo-diversification (where underlying variables are the same). Treat PM as a training ground for judgment, not an arbitrage playground.

A couple of days ago, I published an article titled "I Built My Own Investment Dashboard with AI", where I shared several tools I coded: a cross-market asset panel, an investment map, a personal content operation console, and a Polymarket betting monitoring panel that I've been using frequently lately.

Over the past two and a half weeks, I ran a test with a principal of around $1600, achieving a return of over 30%. The real-time statistics from the panel basically matched the final actual net profit, with only a discrepancy of about $6, which can be attributed to small errors like pending orders or liquidity rewards.

However, what I really want to discuss in this article is not that "Polymarket is a great way to make money," nor is it meant to be packaged as some kind of arbitrage tutorial.

Quite the opposite. After completing this round of testing, I increasingly feel that Polymarket is not a place suitable for charging in with the mindset of "arbitrage."

1. First, Let's Talk About What This Panel Is

I probably started building this panel around May 21st.

The initial requirement was simple: I didn't want to keep opening a dozen betting pages to toggle back and forth on yes/no price changes, nor did I want to manually record everything in Excel.

Yes, before this, I was using Excel to track buys and sells, unrealized profits and losses, settlement nodes, and event types – a clumsy method for a clumsy person.

But as anyone who's actually played it knows, many bets on Polymarket can easily spiral out of control, precisely because manual recording is highly inefficient. For example, you might start with a small bet, but then the odds move and you feel tempted to add more, lacking an intuitive overall sense. Or, a betting event suddenly fluctuates, and you fail to update the spreadsheet in time, missing the window for stop-loss or adding to the position, and so on.

Ultimately, the whole process is too fragmented. Without a system, people easily place orders based on emotions.

So, from the very beginning, the purpose of building this panel was to place every single bet back into a unified framework, turning this feeling into a relatively visual and comparable presentation of information.

After several iterations, I split it into two tabs: "Position Dashboard" + "Opportunity Monitor."

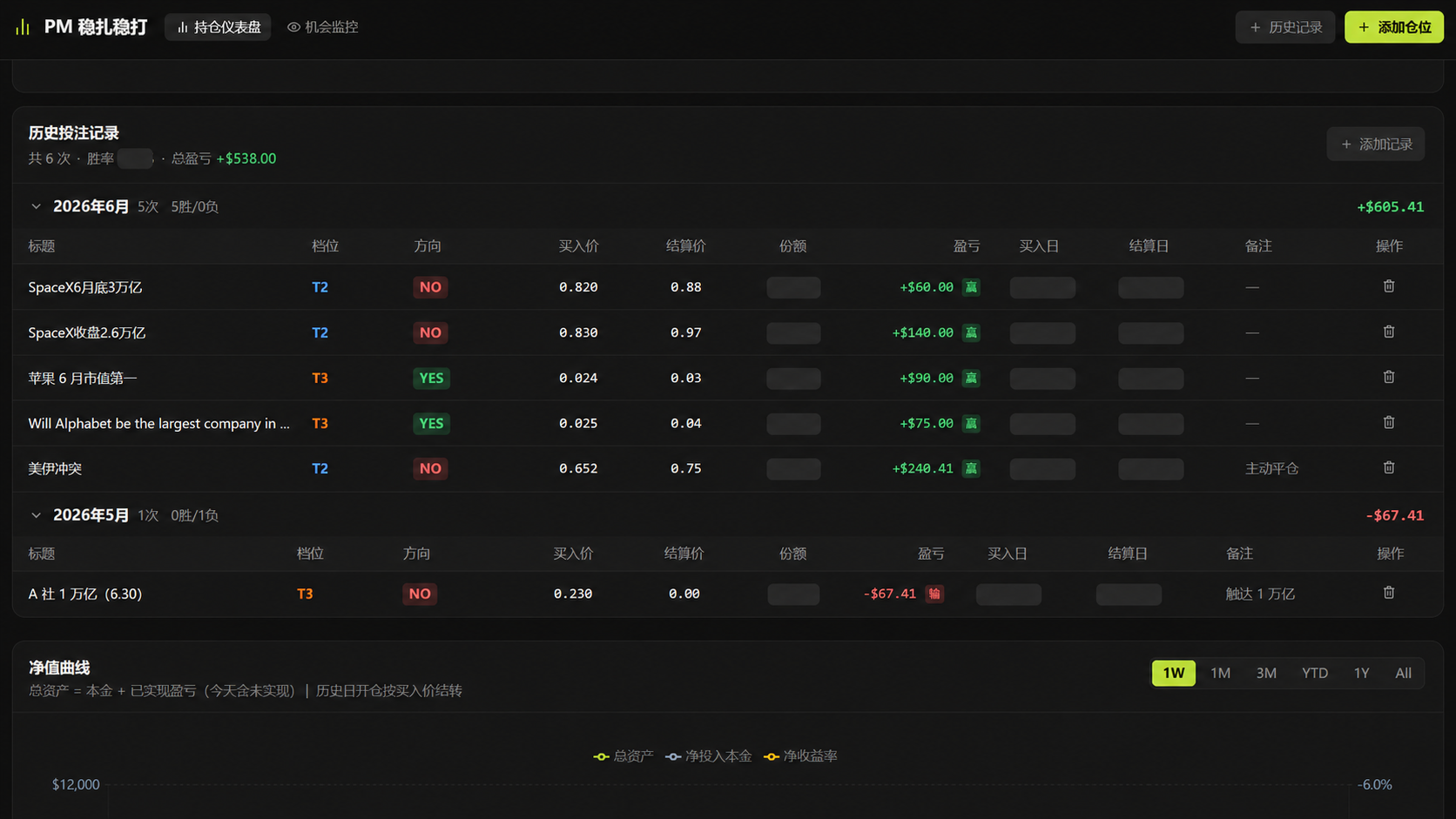

The "Position Dashboard," as the core of the entire panel, is a dynamic system that can fetch real-time data from PM and recalculate. It's divided into several functional areas (refer to the image at the beginning of the article):

- Overview Bar: Total Principal (planned, not very meaningful in practice), Invested Principal, Position Value, Position Floating P&L, Total Floating P&L (including closed positions) – get a full picture of the account at a glance;

- Tier Allocation Ratio: This is the core risk management module of the panel, and I believe it's the most counter-intuitive and important area. I'll save the details for the next chapter;

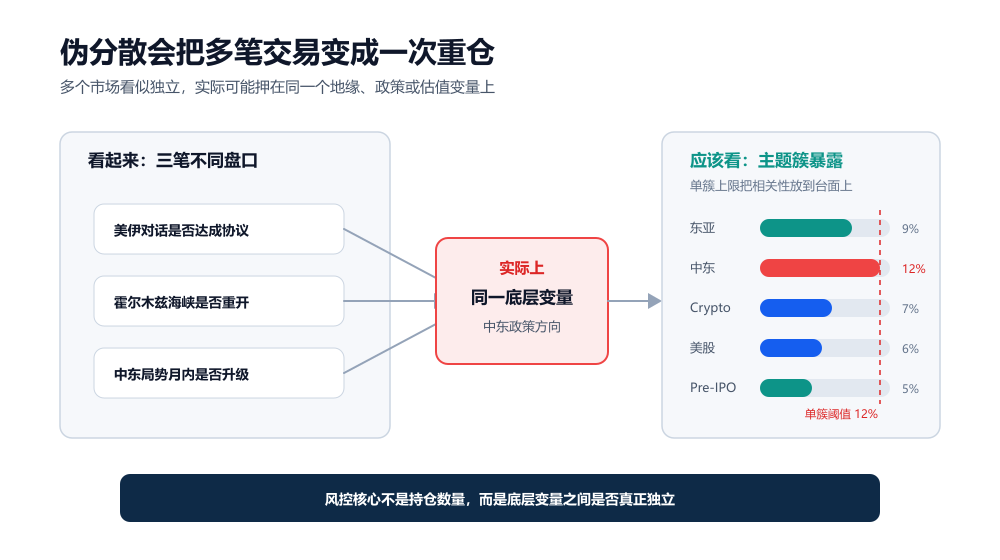

- Thematic Cluster Exposure: I tag each bet with a "thematic cluster" label, dividing them into East Asia, Middle East, Crypto, US Stocks, Pre-IPO (customizable for adding/deleting). The panel automatically aggregates the proportion of each cluster and sets a 12% upper limit threshold per cluster. Why design it this way? Mainly to combat the most insidious trap on PM – false diversification. More on this in the next chapter;

- Individual Position Details: Tier, Direction, Entry Price, Settlement Price, Shares, P&L, Entry Date, Settlement Date, Notes – everything is clear in one row, with options for ascending/descending order and filtering by tags;

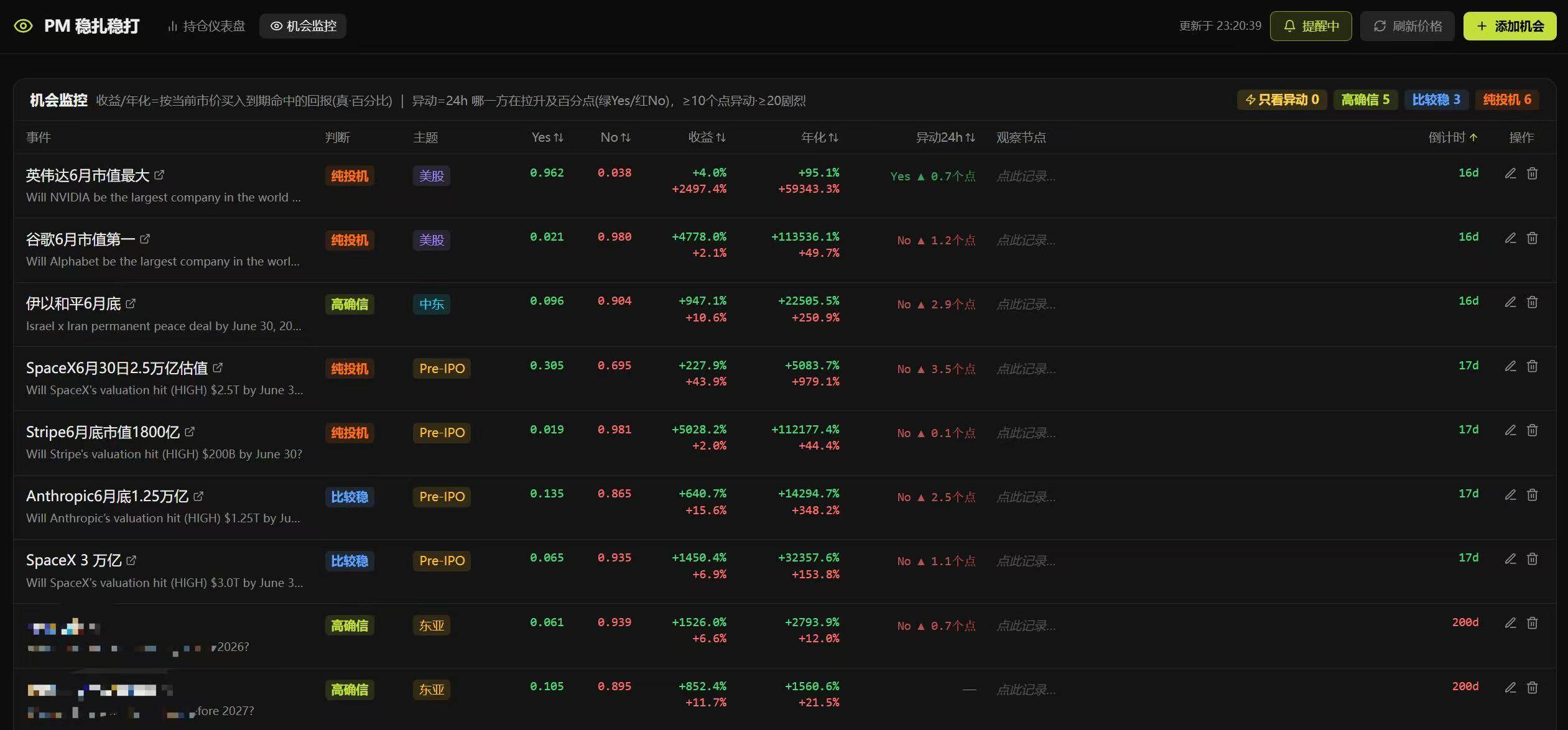

The "Opportunity Monitor" is a watchlist where I place markets I'm interested in but haven't bet on yet.

For each market, I record several key fields, including the event name (with a hyperlink directly to the trading page), T1/T2/T3 tier judgments, current yes/no prices, returns, annualized returns, anomalies (customizable thresholds, e.g., if an anomaly exceeds 20% within 24 hours, a pop-up alert appears as long as the webpage is open), my set observation nodes, and the countdown until the bet expires.

There are two designs I'm particularly satisfied with: First, I found a suitable PM interface. By simply pasting the betting event's webpage link into it for parsing, it automatically prompts the yes/no options, corresponding prices, and the classification of different options under the same event, significantly reducing manual entry effort. Second, the Tier assignment for the same bet is automatically reorganized based on the remaining days.

Shortly before Anthropic released Mython, the watchlist showed clear price anomalies, which could essentially be judged as high-probability deterministic events. Entering at that time would have yielded a return of about 10 points – opportunities like this are hard to capture consistently without a watchlist.

2. PM's Expected Value Trap and the "T1, T2, T3" Design Principle

The above is a brief introduction. What I really want to discuss is a reflection after my actual testing.

That is, within binary markets like PM, there exists a significant structural trap. It's unfriendly to players who like "single large positions," but comparatively more suitable for diversified allocators who prefer to "open a supermarket and buy in bulk."

I'll try to articulate my thoughts clearly. If there are any errors or omissions, just pretend you didn't see them:

Suppose the yes price c for a certain betting event is 0.80, meaning the market believes there's an 80% probability of it happening. If my own judgment of the true probability q is 0.90, then the expected return for this bet can be roughly calculated as:

EV = q / c - 1 = 0.90 / 0.80 - 1 = 12.5%

This looks good, but PM is not a bond. Behind this 12.5% lurks a very sharp tail risk: if your judgment is wrong, the loss isn't 12.5%, but 100%.

So, in my panel, I don't just look at "expected return." I simultaneously monitor two things:

- One is the gap between my own probability judgment and the market price, i.e., q - c (I've set an automatic take-profit reminder target value, which is the midpoint between the entry price and 100). This is the core criterion for whether a real edge exists;

- The other is the impact on the total account if this bet goes wrong and the entire position goes to zero;

The second reason is also the origin of the T1, T2, T3 stratification I mentioned in the first chapter.

Simply put, I divided them into three categories:

- T1 High Conviction: For me, my comfort zone lies in matters related to East Asia and some geopolitical topics where I believe there's an information asymmetry between East and West, added after repeated verification;

- T2 Fairly Stable: Some opportunities where I feel the current implied probability is significantly lower than the actual yes or no pricing;

- T3 Pure Speculation: The kind with very high odds, not meant for long-term holding. Best for contrarian plays, betting on reversals. It tends to revert to a certain price, allowing for short-term gains;

However, it's important to note that T1 has implicit costs, especially for long-duration targets. For instance, a T1 bet might have a static return of 18%, but if it settles in 180 days, the annualized IRR might only be 3-4%. You might be better off just holding the cash, because your principal is locked up during this period, causing you to miss out on high-IRR opportunities that arise later.

Therefore, within T1, I further break it down into different time frames (this part is purely personal methodology, so I won't share the details, same below). Anyway, short-term T1-A can be larger bets, while long-term T1-C requires restraint. Allocating too much capital to low-IRR long-duration targets is an implicit efficiency loss.

T2 has an edge, but you need to leave room for "being wrong." The limit per bet is 8-10%. This means even if this bet is a total loss, the overall account impact is controlled to under 10%, allowing you to continue participating in subsequent opportunities.

T3 odds are very attractive, but use minimal positions for observation. Don't rely on it for big profits. Instead, use it for contrarian plays and short-term mean reversion – to continuously track high-odds events and build a feel for this type of market.

Overall, the position size limit essentially reserves affordable room for the possibility that "my judgment might be wrong."

Here's a very counter-intuitive but crucial point: High conviction does not equal large position size. Even if you think an event has a 95% probability of happening, as long as there's a 5% chance of it going to zero, the position must be limited.

Take an extreme example. Suppose you make 10 bets, each with a self-assessed 95% win rate. Sounds stable, right? But assuming they are independent, the probability of at least one being wrong is roughly 1 - 0.95^10 ≈ 40%.

If you trade enough times, you will eventually encounter that one loss.

And this is just for independent events. In reality, many PM markets are not independent; they often have correlations. For example, "Will a US-Iran dialogue agreement be reached?", "Will the Strait of Hormuz reopen?", "Will Middle East tensions escalate within the month?" – these three bets look like three independent markets, but the underlying variable is almost the same: the direction of Middle East geopolitical policy. If your judgment on this direction is wrong, all three bets bleed simultaneously.

This is the biggest help for me – not improving win rate, but limiting my ability to make big mistakes. Frankly, the core value of this panel isn't profit statistics; it's risk management.

3. My Real View on Polymarket After This Round of Testing

After over two weeks of deep-dive testing, my biggest takeaway is that opportunities do exist on Polymarket, but it's definitely not the arbitrage paradise that many imagine it to be.

Previously, on-chain arbitrage we played with mostly had clear rules, and price discrepancies could be locked in. Polymarket is different. It really tests your logical understanding of the shifting dynamics of a bet (this feeling is quite hard to articulate precisely with text).

For example, regarding political and economic dynamics related to East Asia, Chinese-speaking users might indeed have a certain information asymmetry advantage. This is worth exploring, but it doesn't guarantee you will win. Polymarket ultimately settles not based on "your understanding of reality," but according to market rules and specified data sources (UMA's manipulation issues are also not uncommon).

Furthermore, what seems like a sure thing in the Chinese context doesn't mean the definition is the same under English rules. The rule settings for each bet often contain some textual pitfalls.

So, based on my actual experience, PM doesn't have that many arbitrage opportunities. It mainly relies on information asymmetry and position diversification. Even with high conviction, you might encounter a black swan event.

Once you do, your principal is completely lost.

As a friend put it, "In investing, even a 1% probability of going to zero shouldn't be approached with wishful thinking."

Because, in the long run, such an expected value is negative.

So, my current understanding of PM has become more conservative:

- First, don't treat it as a stable income tool. Even for high-conviction bets, especially after you've won several times in a row, don't feel like you've found an ATM. The scariest thing about binary markets is that they make you believe you can predict everything after a winning streak, leading you to make a large final bet that gives back all your previous profits;

- Second, don't equate high win rate with a good trade. If an event has a 90% win rate but the market price is already 0.95, it might actually have a negative expected value. Conversely, an event with only a 40% win rate could have a positive expected value if the market only prices it at 0.20;

- Third, don't ignore tail risk. This is particularly important. Many people see a 10% or 20% return and think it's stable. But if being wrong on this trade means going to zero, it's not a low-risk return in the traditional sense (From this perspective, I even think there are no so-called low-risk opportunities on PM; every single one is high risk);

- Fourth, avoid false diversification. Buying positions in many different markets doesn't necessarily mean diversification. As mentioned earlier, "Will a US-Iran dialogue agreement be reached?", "Will the Strait of Hormuz reopen?", "Will Middle East tensions escalate within the month?" These three bets look like three independent markets, but the underlying variable is almost the same;

So, I now prefer to view PM as a judgment training ground.

It perfectly aligns with the political, economic, tech, and financial news that I, a homebody, browse daily. It turns judgments that usually stay at the "I think" level into something that can be positively reinforced.

These skills are equally useful beyond PM.

As a side note, besides this PM betting panel, I also used Codex to build a dynamic monitoring panel for private market valuations. It mainly tracks valuation changes for unicorn companies that haven't gone public yet – Anthropic, OpenAI, Stripe, Kraken – and the relationship between these changes and the corresponding bets on PM.

Polymarket is essentially a market for expectations. Sometimes, signals start changing in the private market, but PM prices haven't moved yet. Other times, PM prices move first, before the actual data catches up. The discrepancy between the two is worth continuous observation.

Of course, this isn't risk-free arbitrage either. Private market valuations themselves aren't completely transparent, and different data sources may differ. But as an observational framework, it's quite interesting. I'll look for an opportunity to write a separate article about it later.

Summary

The entire point of this article has never been "I made 30% with my panel, so you can too."

What I find more useful is being able to create a tool that helps you turn feelings into frameworks, and frameworks into discipline. Many times, many people make money not because they've found some secret, but because their judgment happened to be right in that particular round.

That distinction is very important.

I also suggest everyone try Vibe Coding. It doesn't have to be Claude Code specifically. You can start with Codex, or even Kimi's recently launched Kimi Work to get a feel for it. If anyone finds it inconvenient to subscribe to overseas services, I can share some smooth methods I use later on.