史上最大 IPO 落地,与币圈的一地鸡毛

- Key Takeaway: SpaceX (SPCX) surged approximately 19% on its first trading day, reaching a market cap of over $2 trillion. However, this valuation implies extremely high future assumptions: a price-to-sales ratio of nearly 100x, cancelable compute contracts, and potential selling pressure from unlocks, reminding investors to carefully assess the entry price.

- Key Elements:

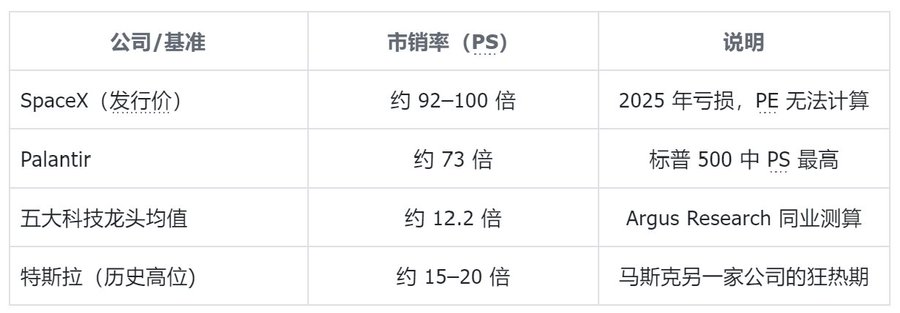

- SpaceX closed at $161 on its IPO day, with a market cap of $2 trillion. However, it posted a net loss of $49 billion in 2025, and its price-to-sales ratio of approximately 92-100x is significantly higher than the S&P 500 top companies' average of 12.2x.

- The core valuation is driven by three business segments: Starlink, contributing 61% of revenue and the majority of profits (39% margin); the launch business, which is loss-making; and the AI business (xAI), which burns cash but supports the narrative of an on-orbit computing TAM of $26.5 trillion.

- Two major compute orders (Anthropic at an annualized $15 billion, Google at $11 billion) can be canceled with 90 days' notice. The certainty of their cash flow is weaker than market expectations, effectively making them short-term leases rather than long-term contracts.

- An index inclusion rule adjustment (Nasdaq-100 Fast Entry) will trigger $22-27 billion in passive buying, providing short-term support within the first three weeks post-IPO. However, the lock-up period (starting with staggered unlocks at the end of July) will bring continuous selling pressure.

- The public float is only 4%, and insider lock-up periods range from 180 to 366 days, making the short-term share structure tight. However, unlocks beginning after the Q2 earnings report will persist through the second half of the year, creating a pressure window once the passive buying is exhausted.

SpaceX is a great company, there is no doubt about that; but even a great company needs to be bought at the right price to make a correct investment.

Preface: From the Chaos of the Crypto Space

On June 12, 2026, Eastern Time, SpaceX officially listed on the Nasdaq under the ticker symbol SPCX. Despite the company recording a net loss of approximately $4.9 billion for the full year 2025, it did not break below its issue price on its debut as many had expected. The initial public offering (IPO) price was set at $135, the stock opened with a jump to $150, climbed throughout the session to a high of $176.52, and finally closed at around $161, marking a gain of about 19% on the first day.

The company's market capitalization exceeded $2 trillion, making it the sixth-largest listed company in the United States. This offering also set a record for the largest IPO in human history.

Source: Nasdaq Stock Exchange

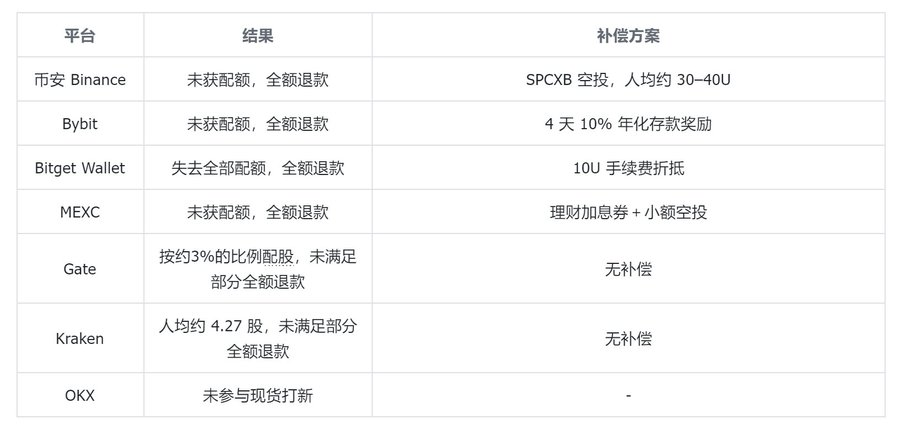

In stark contrast to the enthusiasm in the traditional markets, the crypto space was filled with complaints. Multiple exchanges had previously heavily promoted tokenized IPOs to attract users, but on the listing day, almost all of them fell short. The core reason was the inability to secure the underlying share allocations in time.

A review showed that any platform connected to Kraken's xStocks channel almost entirely failed to obtain sufficient shares.

Source: Exchange announcements on Twitter

Specifically:

- Binance canceled its tokenized IPO event and issued full refunds, compensating users with an airdrop of SPCXB tokens totaling around $1 million, worth approximately $30 to $40 per person.

- Bybit also issued full refunds and additionally offered a 4-day deposit reward with an annualized yield of 10%.

- Bitget Wallet, having integrated xStocks, lost its entire allocation, ultimately providing users with full refunds and a fee credit of about $10.

- Kraken, using its own broker-dealer channel, distributed a fixed small share amount to all subscribing users, averaging about 4.27 shares per person, with full refunds for the unfulfilled portion.

In other words, the IPO results from these platforms generally fell short of users' initial expectations.

The common thread of failure is clear: platforms that bet solely on the xStocks channel collectively missed out because the IPO was oversubscribed by about 4 times, and the underwriters allocated a very limited amount of shares to the crypto channels. Furthermore, xStocks itself is the tokenized stock business acquired by Kraken in late 2025, meaning this supply bottleneck essentially originated from Kraken itself.

One platform worth special mention is MSX (Maitong MSX). During the SPCX IPO process, Maitong differentiated itself from other exchanges by continuing to offer users full allocations, sometimes even at prices below the issue price. This, ironically, sparked concern within the community. Maitong explained that it secured its shares through Republic.

However, Bitget CEO Gracy pointed out that Bitget has an exclusive partnership with Republic, implying that Maitong had not actually reached an agreement with Republic.

Subsequently, numerous doubts arose in the community, leading to suspicions about whether the share source was from an "electronic trading platform," as well as concerns that the platform might be unable to fulfill redemptions, potentially leading to a bank run.

Let's set aside the debate within the crypto space for now. Regardless of the reliability of the IPO subscription channels, what truly determines the profit or loss of an investment is the company's intrinsic value and the price paid.Therefore, the following sections return to SpaceX itself, addressing three questions in turn: whether the company is worth buying at its current price, whether its valuation logic is sound, and the likely direction of its stock price post-listing.

I. SpaceX: A Prospectus with Starry Ambitions

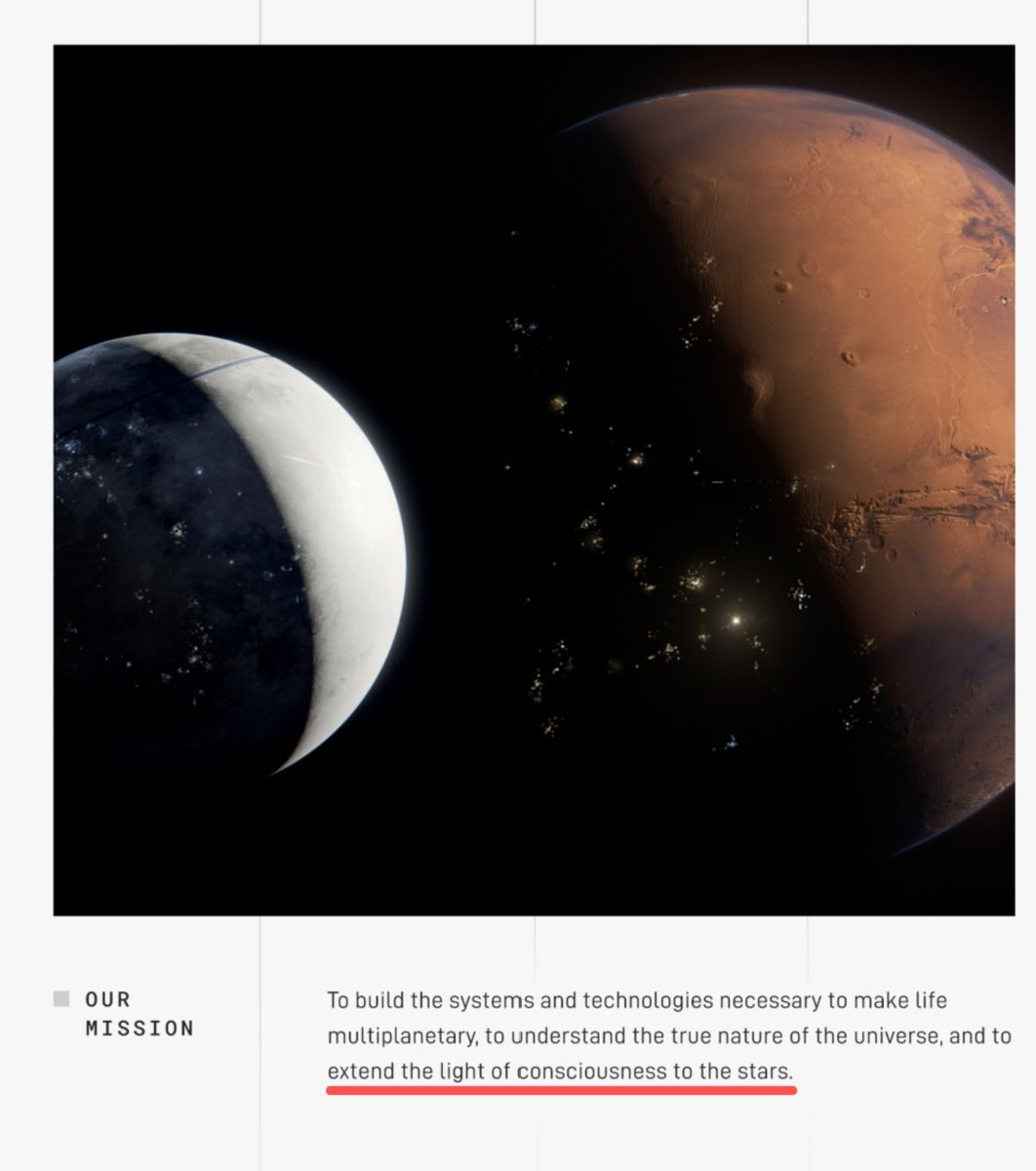

To understand Space Exploration Technologies Corp. (SpaceX), it's best to start by reading the first page of its prospectus. In the opening of its S-1 form filed with the U.S. Securities and Exchange Commission (SEC), SpaceX presents a mission statement that reads unlike a typical financial document:

The Company's mission is to build the systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars.

Source: SpaceX Form S-1, SEC EDGAR

The prospectus further explains that xAI, founded in 2023 and acquired by SpaceX in early 2026, now serves as a pillar within the company's vertically integrated system. It also states that the company plans to begin deploying on-orbit AI computing satellites as early as 2028.

For a company that builds rockets to write about the sun, computing power, and consciousness in the first paragraph of its prospectus, this narrative strength is itself a component of its valuation and the starting point for all subsequent debates.

Sources: SpaceX Pricing Announcement, CNN, NPR, The Motley Fool, June 2026

On its listing day, the stock opened at $150, hit an intraday high of $176.52, eased in late trading, and closed at around $161, a gain of approximately 19.3% from the IPO price. Based on the closing price, the company's market cap exceeded $2 trillion, pushing Elon Musk's personal net worth past the $1 trillion mark for the first time. The table below summarizes the key figures.

The peculiarity of this day wasn't just the price increase, but the structural composition of a deliberate supply-demand imbalance. The Class A shares issued constituted only about 4% of the company's equity, with the rest locked up. Approximately 30% of the offering amount (about $22.5 billion) was allocated to retail investors. In other words,a company worth $1.75 trillion was priced based on trading only about 4% of its outstanding shares, with most sellers locked out of the market. This point will recur, as it explains both the strength of the first day and seeds the potential for future volatility.

II. Valuation Breakdown: Why Dare to Price at Two Trillion?

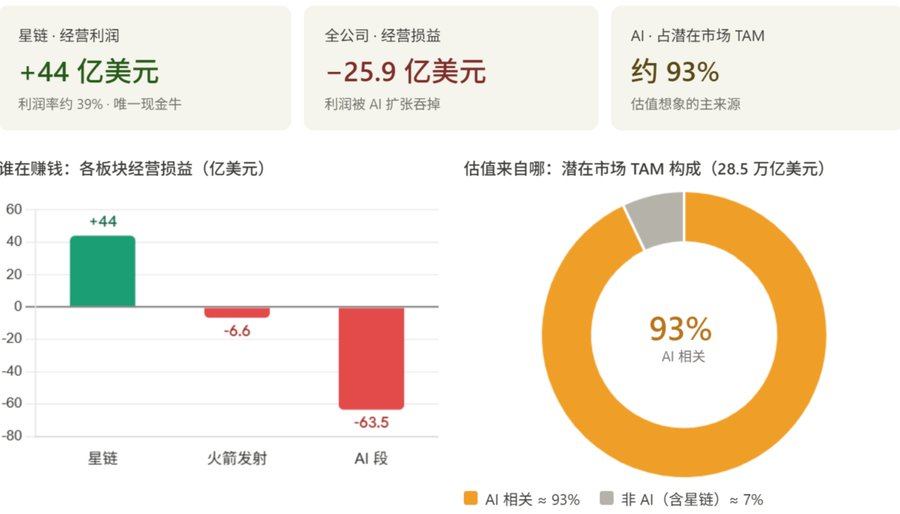

To understand the $2 trillion valuation, SpaceX must be broken down into three business segments, as their profitability and valuation logic are entirely different. According to the S-1 disclosure, in 2025, the company generated consolidated revenue of $18.674 billion, an operating loss of $2.589 billion, and adjusted EBITDA of $6.584 billion. The net loss was approximately $4.9 billion.

SpaceX Three Business Segments Financial Comparison (Source: SpaceX Form S-1)

The first segment is Rocket Launch (Space segment). This is SpaceX's core business and the most publicly known part, yet it is not very profitable on the books. In 2025, this segment generated revenue of approximately $4.1 billion, with a year-over-year growth of only about 8%, and recorded an operating loss of roughly $657 million, largely dragged down by R&D spending on the next-generation Starship program—which alone approached $3 billion in 2025.

The second segment is Starlink (categorized under the Connectivity segment). This is the real profit engine and the cash flow generator supporting the entire company. In 2025, this segment generated revenue of about $11.4 billion, accounting for approximately 61% of the company's total revenue, and produced an operating profit of around $4.4 billion, with an operating margin close to 39%. As of the end of March 2026, Starlink had approximately 10.3 million users across over 160 countries and regions, with about 9,600 satellites in orbit. The key to its business model is economies of scale: once built, the marginal cost per additional subscriber is very low, allowing profit margins to expand with user growth.

The third segment is the AI business, which offers the greatest upside for valuation but also burns cash the fastest. It comprises xAI, consolidated in February 2026, including the Grok large language model, X platform advertising and subscriptions, and the Colossus data center computing power. In 2025, this segment generated revenue of about $3.2 billion but recorded a staggering operating loss of approximately $6.35 billion—the profits earned by Starlink were essentially consumed by the expansion of this segment.

Source: SpaceX Prospectus

Based on the above, we can draw two conclusions:

- The biggest driving force behind SpaceX's IPO is actually AI, not "rocket launches" per se. Therefore, SpaceX also represents a significant layout within the AI narrative—a major embodiment of the "AI bubble" that many have feared.

- What SpaceX is truly selling to investors is not its current financial statements but a blueprint: using Starship to launch data centers into orbit, directly harvesting solar energy to power AI, bypassing the constraints of terrestrial power grids. The company is essentially selling the concept of a "space-grade AI data center," not just rockets and AI models. The prospectus estimates the company's total addressable market (TAM) at a staggering $28.5 trillion, with approximately 93% attributed to AI-related sectors.

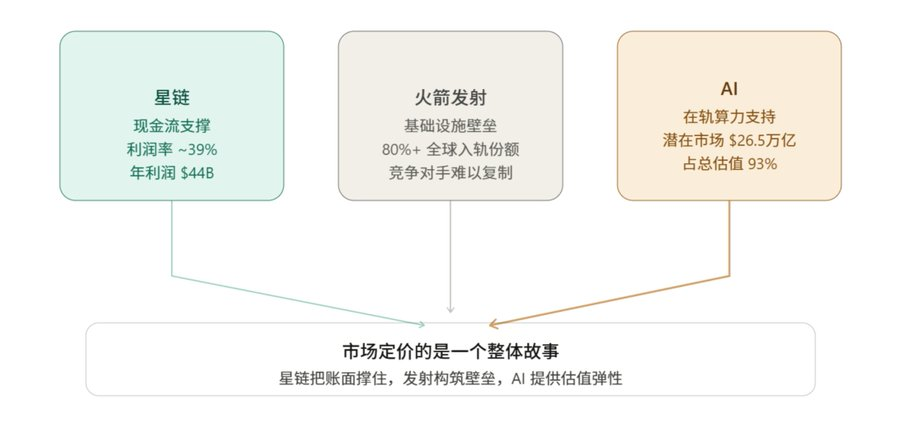

Looking at these three pieces together clarifies SpaceX's valuation logic: the market is not pricing a rocket company or a satellite broadband company. Instead, it's packaging Starlink's cash flow, the moat of its launch capabilities, and the long-term vision of in-orbit AI computing into a single, comprehensive narrative: Starlink supports book cash flow, rocket launches build an irreplicable capability barrier, and AI provides upside optionality.

The question remains: what is this upside optionality actually worth?

III. Valuation Pillars: Two Major Computing Contracts and a Cash Flow Base

A high valuation requires verifiable earnings anchors. SpaceX's S-1 prospectus does contain several clues that could support the story: two signed computing capacity leases, plus the continuous subscription-based cash flow generated by Starlink.

SpaceX Main Profit Support Points (Data Sources: SpaceX Form S-1, DatacenterDynamics, Markman Capital Insight)

Anthropic's $15 Billion Computing Capacity Contract: According to the S-1, Anthropic is indeed paying SpaceX a monthly fee of $1.25 billion to lease computing capacity from the Colossus data center in Memphis. The contract runs until May 2029, representing an annualized value of about $15 billion and a total contract value exceeding $40 billion.

Google's $11 Billion Computing Capacity Lease: Google signed the second major computing lease, paying approximately $920 million monthly for roughly 110,000 GPUs and related computing capacity, with a term from October 2026 to June 2029.

Cash Flow Base and Pricing Strategy Shift: Beyond these two large contracts, Starlink itself is the company's most stable revenue source. In Q1 2026, the Connectivity segment achieved an operating profit of $1.188 billion, with subscriber numbers reaching 10.3 million by the end of March. In May 2026, SpaceX raised prices on all its Starlink consumer plans, by up to $10 per month, signaling a strategic shift from using price cuts to drive user growth in previous years to beginning to monetize its massive existing user base.

Summing the deterministic income from these three sources, SpaceX could potentially generate at least ~$40 billion annually—a figure that already far exceeds its total 2025 company-wide revenue of $18.7 billion.

IV. Questions: The Small Print in Contracts and Outlandish Multiples

After listing the supporting points, it's crucial to also examine the valuation's vulnerabilities. For SpaceX to justify this valuation, the difficulty is immense, for three reasons.

Contracts Run to 2029 but Can Be Terminated at Will

The two large computing contracts appear to lock in multi-year revenue, but the fine print contains a critical clause: either party can terminate the agreement with 90 days' notice. Furthermore, Elon Musk himself clarified publicly on X that the Anthropic arrangement is essentially a 180-day lease, after which both parties have a rolling 90-day cancellation right. The Google contract also allows for termination with 90 days' notice after December 2026.

This means that valuing the company by treating the roughly $26 billion in annual computing revenue as a firm, deterministic backlog is untenable: A lease that can be canceled within 90 days corresponds to a completely different level of cash flow certainty than a long-term contract locked in until 2029. Any valuation model that treats it as a guaranteed backlog will be disproven by this small print.

Price-to-Sales Ratio Near 100x: How Outlandish is This Historically?

From a multiple perspective:

First, the company is currently loss-making, making the Price-to-Earnings (PE) ratio incalculable.

Second, using the Price-to-Sales (PS) ratio common in tech company valuations, the company's $1.75 trillion market cap corresponds to approximately $18.7 billion in 2025 revenue, yielding a PS ratio of about 92 to 100 times.

Price-to-Sales Ratio Horizontal Comparison (Source: Investing.com)

For context, the average PS ratio for the five major U.S. tech giants is about 12.2x. The highest PS stock in the S&P 500, Palantir, trades at around 73x. This means that upon listing, SpaceX's PS ratio is already about 30% more expensive than the most expensive stock in the S&P 500.

Historical precedents are also unfavorable:

- According to Jay Ritter's data from the University of Florida, among 14 IPOs with revenue exceeding $100 million and PS ratios above 40x, 12 underperformed the broader market in the three years following listing.

- Another analysis reviewing over a hundred hot tech stocks found that historically, only about 8 stocks ever broke the 100x PS ratio threshold, and without exception, they experienced significant declines after peaking, with an average drop of over 50% from peak to trough.

So, purely from a valuation and pricing perspective, no matter how you look at it, SpaceX is undeniably overvalued.

What Does a Doubling Imply in Terms of Magnitude?

Another way to do a sanity check is to reverse the question: if someone expects SpaceX's stock price to double again, they need to consider what market capitalization that corresponds to.

The current market cap already exceeds $2 trillion, ranking sixth in the U.S.

- If the market cap doubles to around $4 trillion, it would approach or even surpass the world's most valuable company, Nvidia.

- If the stock price quintuples or sextuples from the IPO price, the corresponding market cap would reach the $10 trillion range, equivalent to combining the market caps of several of the largest U.S. tech companies.

Given that the company is still loss-making, its core profit comes only from Starlink, and its computing contracts can be terminated with 90 days' notice, delivering such scale within the foreseeable future seems incredibly challenging.

This is the source of the oft-heard statement from many bears and institutional investors—they were scrambling for allocations at $135 while simultaneously writing in their models that this price was internally inconsistent.

V. Short-Term Perspective: Index Inclusion and Passive Buying Timeline

Calculating the long-term valuation picture doesn't necessarily mean the stock will fall in the short term. Quite the opposite, due to changes in index rules, SpaceX