2026 Real Progress and Investment Opportunities in Decentralized AI Computing Networks

- Core Insight: As of early 2026, the Decentralized Physical Infrastructure Network (DePIN) track has shifted from conceptual hype to revenue realization, with annualized protocol revenues exceeding $200 million, primarily serving cost-sensitive AI workloads such as inference and fine-tuning, rather than cutting-edge large model training.

- Key Elements:

- The total market cap of the DePIN track is approximately $9.423 billion. Leading protocols like Aethir achieve annualized revenues of around $150 million, with clients including non-crypto native enterprises, proving the generation of real revenue.

- The price advantage of decentralized GPU networks is tangible, being 60-80% lower than AWS. However, hidden costs such as poor node stability and the lack of SLAs can erode this advantage.

- The market landscape is clearly stratified: Aethir, io.net, Akash, Bittensor, and Render occupy distinct niches in enterprise-grade revenue, ML cluster orchestration, pricing mechanisms, AI model incentives, and rendering, respectively.

- Tokenomics is maturing. Leading projects like Render and io.net are shifting to link token burn/mint mechanisms with real computing consumption, mitigating the "death spiral" risk associated with early inflationary tokens.

- Non-crypto native enterprises (e.g., KREA's clients include Nike and Apple) have begun to procure decentralized computing power, representing a substantial breakthrough in market entry pathways, although the number of cases remains limited.

- Integration with the AI Agent economy is a future growth driver. The permissionless nature of decentralized computing power naturally suits the procurement needs of autonomous Agents.

We must acknowledge that this sector has crossed a significant threshold that no other crypto narrative has successfully cleared—it is generating real revenue from non-crypto-native customers.

Introduction: Decentralized Opportunities Amid the AI Computing Power Contradiction

By 2026, the global AI computing power market has entered a highly tense phase. On one hand, leading tech companies are concentrating GPU resources at an unprecedented pace. For example:

- xAI's Colossus supercomputing cluster has aggregated 550,000 NVIDIA GPUs and is advancing towards a target of 1 million GPUs according to its public roadmap;

- The Project Stargate, jointly launched by OpenAI, Oracle, and SoftBank, has deployed over 450,000 NVIDIA GPUs in Texas, with a target total power of 1.2GW.

On the other hand, a large number of small and medium-sized AI startups and independent research teams are experiencing a computing power blockade. AWS's H100 clusters had waiting periods of 8 to 12 months between 2023 and 2024, with cloud computing bills often exceeding several million dollars.

It is precisely under this condition of severe supply shortage that the Decentralized Physical Infrastructure Network (DePIN) sector has rapidly emerged.

- As of the end of March 2026, the total market cap of the DePIN sector was approximately $9.423 billion, with CoinGecko tracking nearly 250 active projects.

- In September 2025, this sector briefly reached a market cap high of approximately $19.2 billion, achieving a year-over-year growth of about 270% compared to $5.2 billion in the same period of 2024.

- More critically, according to on-chain data aggregated from DeFiLlama and Dune Analytics, the annualized protocol revenue of decentralized GPU computing protocols had exceeded $200 million by early 2026.

We must acknowledge that this sector has crossed a significant threshold that no other crypto narrative has successfully cleared—it is generating real revenue from non-crypto-native customers.

1. Industry Panorama: From Hype to Revenue Realization

In 2026, the DePIN computing power industry began to show verifiable revenue data, moving beyond mere market cap tables and token unlock schedules. The sector has formed a clear hierarchical structure over the past two years. The operational status of the main protocols is as follows:

Table 1: Comparison of Key 2026 Data for Major Decentralized Computing Networks

Source: Official project disclosures, Messari quarterly reports, CoinMarketCap, CoinGecko / Coinbase. Data as of May 2026. Note: Bittensor does not have "protocol revenue" in the traditional sense—it is an AI model incentive coordination layer that rewards participants through inflationary token issuance, with each subnet generating revenue independently.

As shown in the table above, these five protocols occupy different ecological niches.

- Aethir leads with enterprise-grade revenue, boasting an annualized recurring revenue of approximately $150 million, making it the largest protocol in the decentralized computing sector by revenue size. Its clients include game studios, AI inference providers, and model training teams.

- io.net focuses on orchestrating distributed ML compute clusters, with a network covering over 130,000 GPU devices across more than 130 countries.

- Akash, through its reverse auction pricing mechanism, creates genuine price competition. In Q1 2026, compute spending on the platform hit a record high of over $5 million, and the AKT token has risen more than 72% year-to-date.

- Bittensor is entirely different. It doesn't rent out GPU hardware but incentivizes AI intelligence output itself, forming a decentralized machine intelligence marketplace through 128 subnets.

- Render started with 3D rendering, having rendered over 67 million frames, and is now expanding into general-purpose AI computing.

2. Capability Boundaries: What Decentralized GPU Networks Can and Cannot Do

Decentralized GPU networks have long been caught between two extreme narratives: promoters claim costs are only one-tenth of AWS and that it will soon disrupt cloud computing; skeptics argue that distributed GPUs simply cannot support real AI workloads. Both judgments are biased.

The key to understanding this sector lies in acknowledging the structural characteristics of consumer-grade GPUs.

On one hand, a large portion of the computing supply in decentralized networks comes from consumer-grade GPUs, which have limited VRAM capacity and rely on home broadband for inter-node bandwidth. This inherently makes them unsuitable for synchronous training of cutting-edge large models—tasks that require thousands of high-end GPUs to be interconnected with extremely low latency, scenarios designed for hyperscale clouds.

On the other hand, for workloads with higher latency tolerance and cost sensitivity, the cost-effectiveness advantage of decentralized networks is quite evident: parallel molecular screening in AI drug discovery, batch rendering for text-to-image and text-to-video, and large-scale data preprocessing pipelines are all typical matching scenarios.

Furthermore, the continuous expansion of open-source models and the technological evolution of lightweight inference are systematically expanding the serviceable addressable market for decentralized networks. More and more models can efficiently run on single or a few consumer-grade GPUs, lowering the barrier for inference and fine-tuning. This is precisely the zone where decentralized networks are most competitive.

Chart 2: Matching Relationship between AI Workloads and Computing Infrastructure

Source: Compiled from Together AI's multi-node training report (January 2026), Dell's LLM cluster network traffic technical document (December 2025), and Cointelegraph industry analysis (January 2026).

Based on this, the real opportunity for decentralized GPUs lies in fragmented, distributed, price-sensitive scenarios like inference, fine-tuning, data preprocessing, and continuous Agent operation, rather than directly competing with hyperscale clouds for the frontier training market.

It's worth noting that, from the current AI production environment, training accounts for a much smaller proportion of total computing power consumption compared to inference and Agent-like tasks, which are the primary sources of growing computing demand. This means the market targeted by decentralized networks is by no means peripheral—it corresponds precisely to the largest and fastest-growing layer of AI computing demand structure.

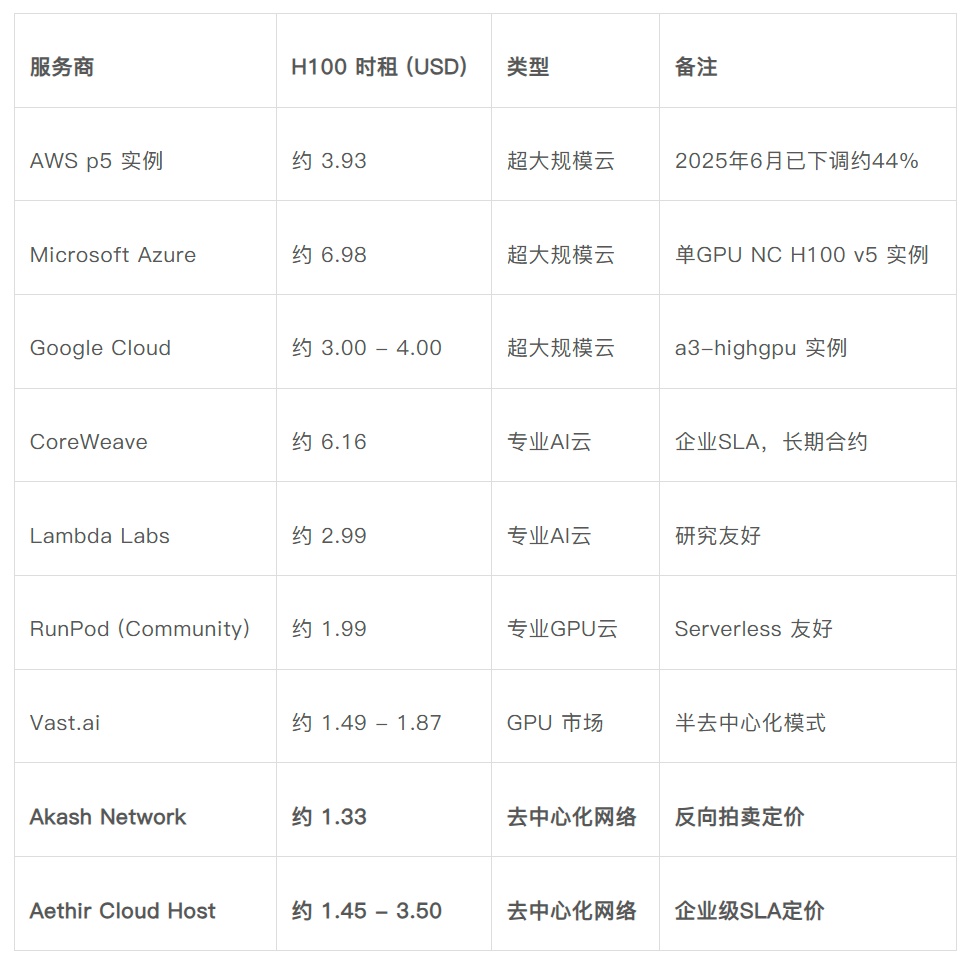

3. Is the Price Advantage Real? Is It Really 60% Cheaper?

One reason for the popularity of decentralized computing power is the widely circulated claim of being "60% cheaper." This claim stems from a comparison of costs. The official public pricing on Akash Network's website shows that the hourly rental for an H100 GPU is about $1.33. After AWS's p5 instances were discounted by approximately 44% in June 2025, the per-GPU hourly rental averaged over 8 cards is about $3.93. This is the most frequently cited comparison in reports and the source of the "decentralized is over 60% cheaper" narrative.

Chart 3: H100 GPU Hourly Rental Price Comparison (Early 2026)

Source: Public pricing from AWS, Azure, Google Cloud; Akash Network website; Aethir official documentation; getdeploying.com (May 2026); IntuitionLabs - H100 Rental Prices Compared (May 2026); Silicon Data - H100 Price Spike (January 2026).

The table above compares the price differences for H100 GPU rentals between centralized platforms and decentralized networks. The following conclusions can be drawn from the comparison:

First, the price advantage of decentralized GPU networks relative to hyperscale clouds is real—approximately 60% lower compared to the average price of AWS's p5 instances, and can be as low as 75% to 80% lower compared to single GPU instances (AWS/Azure).

Second, compared to specialized, highly competitive GPU clouds (RunPod, Vast.ai), the price gap of decentralized GPU networks narrows to 15% to 35%, and in some scenarios, they are essentially on par.

Third, the true differentiation comes more from structural attributes. No need for enterprise accounts, no minimum usage commitments, pay-as-you-go start/stop flexibility, flexible geographic distribution of nodes, and no vendor lock-in—these are the genuine charms of decentralized GPUs.

However, a point that must be raised is: hidden costs are equally non-negligible. The stability of nodes in decentralized networks varies significantly. Production scenarios may require redundant deployment or additional fault-tolerance mechanisms, and these extra costs will erode the nominal price advantage to varying degrees. This is one of the main practical hurdles facing large-scale enterprise adoption of decentralized GPUs in 2026.

4. The Real Changes in the Sector in 2026

Based on the current data, the decentralized computing sector is undergoing two observable deep-seated changes in 2026.

The first is the maturation of tokenomics. Early DePIN projects generally relied on inflationary tokens to subsidize hardware suppliers. This model has inherent flaws: a drop in token price reduces supplier income, leading to supplier exit and decreased network availability, which further depresses the token price, creating a vicious cycle. Between 2025 and 2026, leading projects have gradually shifted towards new models that directly link the token mechanism with real business activity.

The Render Network, through the BME (Burn-Mint Equilibrium) model established by RNP-001, requires creators to pay for rendering tasks in fiat-equivalent amounts, which are automatically converted to RENDER tokens and burned upon task completion. This mechanism has been running for years.

io.net's original tokenomics relied on fixed emissions and price-sensitive supplier income, making it prone to a "death spiral." Its upcoming IDE (Incentive Dynamic Engine), expected to launch in Q2 2026, will replace fixed emissions with a demand-driven model. It aims to stabilize supplier income in USD terms and dynamically adjust the token supply based on real-time revenue and token price.

While these two models differ in their mechanisms, they share a common logic: linking the burning and minting of tokens to real computing power consumption and anchoring supplier income to USD value. This is the first time decentralized infrastructure has had a financial structure logic at the token design level comparable to traditional SaaS businesses.

The second change is the gradual clarification of go-to-market (GTM) pathways. Early DePIN computing networks' customers were almost entirely from crypto-native teams, creating an inherent market ceiling. Since 2025, there have been several cases of traditional enterprises entering the decentralized computing system through specific collaborations.

As early as December 2024, io.net joined the Dell Technologies Partner Program, becoming an authorized partner and cloud service provider. The two parties will collaborate on marketing and demand generation, enabling enterprise customers to integrate and deploy decentralized GPU computing power with Dell hardware. Earlier, in April 2024, io.net partnered with the AI creative platform KREA, whose enterprise client list includes Nike, Apple, FC Barcelona, Publicis Group, and Meta. io.net provides KREA with NVIDIA A100-80GB GPU clusters at roughly a third of the market average price.

Around the same time, Aethir's over 150 paying enterprise clients are distributed across AI, Web3, and gaming. In Q3 2025, its single-quarter revenue reached $39.8 million, with an annualized revenue exceeding $147 million, covering scenarios like AI inference, model training, and Agent platforms.

On the Akash front, Venice.ai (a private, uncensored generative AI application) uses Akash GPUs for inference requests, and FLock.io (a federated learning platform) allows operators to deploy validation nodes on Akash. Both integrations were completed in 2024.

The common characteristic of the above cases is that non-crypto-native enterprises are beginning to incorporate decentralized computing power into actual procurement and technical integration, moving beyond just the narrative level. While the number of cases is not massive, they represent a substantial breakthrough in market entry pathways.

Chart 4: Changes in Key Indicators of the DePIN Computing Sector (2024 - 2026)

Source: BlockEden - Decentralized GPU Networks 2026 & DePIN Revenue Inflection; Yellow.com (May 2026); Messari project report series; CoinGecko - Top Bittensor Subnets (April 2026).

However, it must also be acknowledged: the decentralized computing power sector still faces significant unresolved core obstacles.

First, while raw GPU quotes are indeed cheaper (offering discounts of 45-60%), the variance in reliability often forces users to over-provision computing power, significantly eating into the nominal cost savings.

Second, enterprise adoption of decentralized computing still faces difficulties, such as: orchestration challenges, difficulty debugging distributed failures, and a lack of enforceable SLA (Service Level Agreement) guarantees.

Third, the DePIN tech stack is highly fragmented—computing, storage, verification, and data are dispersed across different protocols. Developers must piece together multiple systems for production-grade deployment, significantly increasing engineering costs.

A noteworthy exception regarding enterprise-side issues is Aethir. Aethir maintains a 99.31% uptime across over 435,000 GPU containers and offers enforceable enterprise-grade SLAs. It is one of the few projects in the decentralized computing space capable of meeting enterprise contract-level service requirements.

Of course, these issues represent both current constraints and tangible gaps that projects can specifically address.

5. Lessons for Ecosystem Participants' Development Paths

For ecosystem participants entering this sector in 2026, the aforementioned data points to several specific judgments:

First, avoid redundant construction of a basic aggregation layer. io.net, Akash, and Aethir have established sizable GPU aggregation networks across different price tiers. A new project entering solely with a general-purpose GPU aggregation approach, without significant differentiation—whether in geographic coverage, compliance qualifications, specialized hardware types, or vertical industry certifications—will find it difficult to build a sustainable advantage. Projects like Render, which expanded from rendering to AI computing, or Aethir, which moved from cloud gaming to enterprise AI inference, which have accumulated specific scenario resources, are more likely to secure initial users and differentiated pricing power than purely general-purpose aggregation networks.

Second, the tooling layer and middleware layer represent more realistic entry points. Each of the previously mentioned unresolved issues—reliability management, distributed debugging, SLA guarantees, cross-chain settlement, and Agent-level compute procurement and reconciliation—corresponds to a viable independent tool-type project.

- Gensyn's Verde is an early example. It is a verification protocol specifically designed for machine learning in decentralized environments. Its core is a lightweight dispute arbitration system that can precisely locate the first step where the training party and the verification party disagree in the training computation graph. This allows re-computation of only that single operation, rather than rerunning the entire task, significantly reducing verification overhead.

- Another idea, proposed by io.net, is to leverage the MCP protocol to allow AI Agents to directly purchase and schedule computing resources without the need for manual KYC or enterprise accounts, thus bypassing the unfriendly onboarding barriers of traditional cloud services for autonomous Agents.

Toolchains built around these underlying protocols offer clearer differentiation space than building another GPU marketplace.

Third, opportunities in the vertical application layer are diverging. Specific scenarios like AI biopharmaceuticals, AI image/video generation, continuous AI Agent operation, on-chain data analysis and backtesting, and privacy computing (combined with TEE) have different requirements for cost sensitivity, latency tolerance, and reliability. Cases like the Templar subnet training the 72B parameter Covenant model on Bittensor demonstrate that small-scale, specific-task training is feasible on decentralized networks. However, the subsequent team exit incident in the same project also highlights that the governance and team stability of vertical application projects are deeply intertwined with the market performance of their tokens.

Fourth, tokenomics design becomes a core barrier. Token models like BME and IDE, which are linked to real business volume, have become de facto standards for the new generation of DePIN computing projects. The earlier approach of releasing tokens first, attracting hardware to the network, and then marketing the market cap to attract users has been proven unsustainable in the market environment of 2026. The token model design of new projects must answer from day one: where does the demand side for the token come from?

Fifth, and a crucial point: the integration of decentralized GPU networks with the AI Agent economy has only just begun in 2026. When the number of AI Agents experiences an order-of-magnitude increase in the next 12-18 months, the demand for decentralized