After the Bubble, Where to Go: 2026 Digital Asset Market Analysis Report

- Core Thesis: The crypto market is currently in an adjustment phase following a bubble burst, highly resembling the historical cycle of the internet bubble (2000-2002). It is not "dead," but rather undergoing value regression and infrastructure reshaping, laying the foundation for the next growth cycle.

- Key Elements:

- Historical Cycle Patterns: Major tech bubbles like railways, radio, and the internet all experienced a four-stage cycle: "Emergence - Mania - Crash - Adjustment." The adjustment phase is characterized by capital concentration towards leading entities, improved regulatory frameworks, and a business model shift from "storytelling" to "profitability."

- Crypto Market Status: As of March 2026, the total market cap stands at approximately $2.5 trillion. BTC is consolidating in a $65,000 - $76,000 range, with BTC dominance stabilizing at 58-60%. Market characteristics are similar to the post-internet bubble adjustment period (e.g., 2002-2004).

- Institutionalization Progress: Since its approval in 2024, the U.S. spot BTC ETF has seen cumulative net inflows exceeding $53 billion, with institutional investors accounting for over 30%. This indicates BTC is transitioning from a speculative asset to an institutional-grade allocation target.

- Regulatory Framework Implementation: In March 2026, the SEC and CFTC jointly released a digital asset classification framework, categorizing 16 assets as digital commodities. This ends a prolonged period of regulatory uncertainty, providing an institutional framework for market entry.

- Capital Concentration and Project Shakeout: Crypto VC funding increased by ~50% year-on-year in 2025, but deal count dropped by 46%, with capital highly concentrated in later-stage projects. Over 70% of DeFi and Meme projects have experienced TVL declines exceeding 90%, indicating liquidity drain.

- Strategic Recommendations: Projects should focus on stablecoin payments and RWA tokenization. VCs should pivot to hybrid equity + token investments. Investors should prioritize BTC allocation, remain cautious towards altcoins, and focus on verifiable revenue sources.

Preface: The Certainty and Uncertainty of Crypto

At the start of 2026, amidst a new bull-to-bear transition, the market is gripped by anxiety. Following the 1011 incident, market liquidity began to dry up. Going forward, aside from a handful of leading projects and companies still standing, most teams have chosen to shut down or pivot.

With the sudden emergence of Openclaw, a new wave of technological disruption has compounded the panic with immense uncertainty. As market liquidity contracts, countless crypto workers are pivoting to AI. Media outlets once solely focused on crypto have somehow found room for AI reports on their front pages. Even some OGs who have navigated the space for over a decade are now declaring "crypto is dead."

Has the crypto bubble truly burst? Is crypto really dead?

Tossing this question to AI yields a myriad of answers. DeepSeek will tell you the dividends of the crypto market have dissipated, making it a domain for professional, compliant players with no opportunities left for retail. Ask Grok, and it'll say this is just a bull-bear transition that will weed out some participants while steering crypto in a better direction. Consult Gemini, and it will argue that AI's development will drive crypto's growth in tandem.

The noise is deafening. So, we aim to find our own answer. There is nothing new under the sun. We have vague memories that when the internet bubble burst in 2001, the market said the same things. In fact, this narrative accompanies almost every bubble.

This time, we choose to study bubbles.

Even if our answer might be wrong, it represents a certainty that is uniquely ours.

I. Exploring the Historical Cycle: From Railways to the Internet, How Tech Bubbles Recur Through History

The Glory of Railways and Radio: Bubbles of the Industrial Revolution

On September 27, 1825, the world's first railway built in England, the Stockton and Darlington Railway, officially opened. Three years earlier, despite opposition from feudal aristocrats and the church, capitalists, seeing the future value of the steel behemoth, chose to bet on it and ultimately succeeded in its construction. They believed this technology would bring them returns, but they did not realize the impact it would have on the entire era.

Although the first railway was built merely as a branch line for the canal transport system, its convenience and cost-effectiveness spurred rapid industry-wide growth, attracting investors. Towards the end of the South American mining speculation bubble of 1824-1825, these risk-takers began shifting their investments to railway companies. During 1836-1837, as the overall stock market strengthened, railway stock prices doubled. Seeing an opportunity, the British Parliament approved 44 new companies in that very year, whose total fundraising easily surpassed all previous capital raised in the industry.

Bubble Formation, Dissipation, and Reformation

Like countless bubbles that followed, when a new technology gains market acceptance, it rapidly develops, forms a bubble, and quickly bursts. Then, as infrastructure gradually improves, a new, stronger bubble may form before finally settling onto a stable trajectory.

After the establishment of these 44 companies, due to the lack of a comprehensive railway network, rail transport didn't seem as convenient as traditional waterway transport. The railway stock index started to decline. By the early 1840s, however, valuations began to rebound, nearing previous peaks. Before 1843, average annual investment in railway companies was about £1 million (~$3.5 billion today). In 1844, it reached £20 million (20x), approaching £60 million in 1845 (60x). By 1846, it had ballooned to £132 million (~$120 billion today). That same year, a record 4,538 miles of new railway were built. Everything seemed prosperous.

Bubble Burst and Value Regression

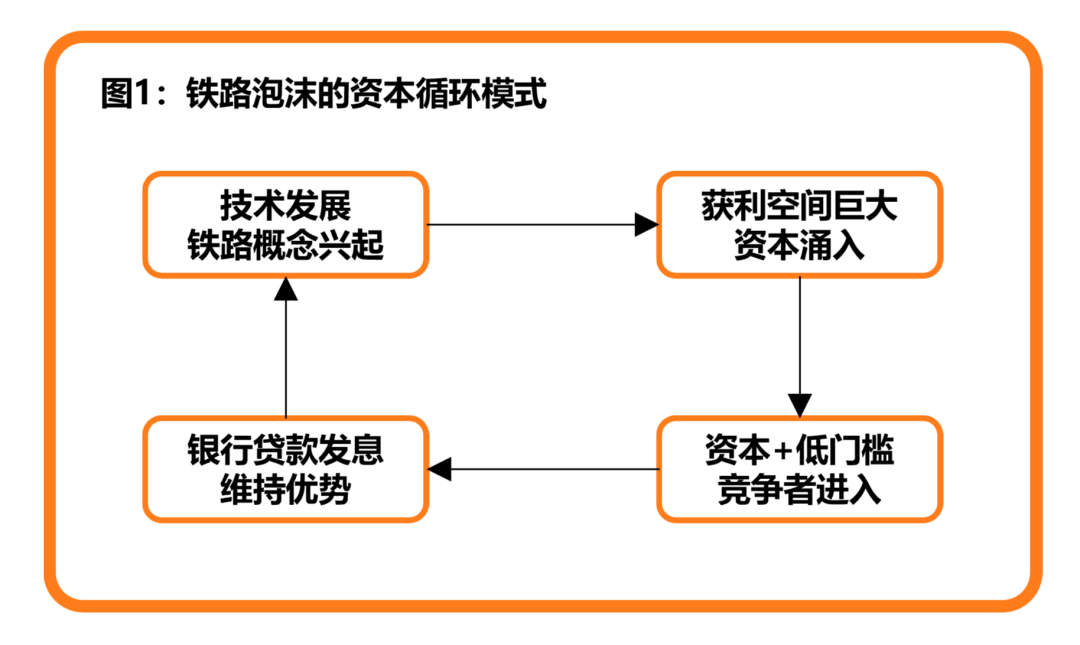

Undeniably, early railways were successful commercial projects. However, investor optimism quickly drove stock prices far beyond any rationally justified valuation for railway stocks. The first railways enjoyed first-mover advantages, but without barriers to entry, these advantages vanished. Ample market capital combined with low technological/market barriers presented a golden opportunity for subsequent competitors, continuously compressing the profit margins of existing firms, creating an environment of diminishing industry-wide returns, commonly known as "involution."

For market investors, the first sign that the boom was ending was the disappearance of huge premiums on new stock issuances. Only companies perceived as higher quality could maintain their stock prices. For surviving railway firms, expanding and securing prime locations was the best way to maintain valuation and competitive advantage. Leveraging bank loans accelerated this advantage. Worse still, being in a nascent industry, most railway companies systematically underestimated construction difficulties. Consequently, actual costs far exceeded initial estimates in their prospectuses. Over time, these stocks became a pure financial game: railway dividends no longer came from profits but from capital funds and bank loans.

In this vicious cycle, bank interest rates kept rising. At a certain tipping point, railway companies could no longer sustain the capital loop. The financial luster of technology suddenly vanished. Overnight, countless investors were bankrupted, and public praise for railway companies turned into criticism.

Facing this situation, the British government passed an act of parliament allowing industry consolidation and abandoning nearly 20% of approved new railway construction. As surviving firms regained profitability, a wave of mergers and acquisitions began. Thereafter, the glory of British railways was no longer a glaring spectacle but more like the gentle, slow light of the morning sun warming the land. While the frenzied speculative capital was unlikely to return, the railways truly nourished the growth of the Industrial Revolution.

Ultimately, the same story played out again, slightly later, on the American continent.

Marconi and Radio

As a footnote to the era, the railway story pauses. With continuous improvements in transportation, distances between regions shrank. People could travel further using these vehicles or, staying home, transmit information via wired telephones and telegraphs.

Of course, the speed limit of information transmission was likely higher.

In 1865, after Scottish physicist James Clerk Maxwell systematically proposed electromagnetic theory, inventors began experimenting with radio waves. Eventually, in 1895, luck favored the Italian inventor Guglielmo Marconi. After successfully making a bell ring on a receiver 10 yards away using his self-built signal transmitter, he believed this distance could be extended.

Marconi keenly saw the technology's future commercial value. He filed a patent in 1896 and began marketing his technology to government agencies. Soon after, he founded the Wireless Telegraph and Signal Company to develop and sell wireless telegraph equipment. In exchange for assigning his patent rights, Marconi received £15,000 (~$6 million today) in cash and £60,000 (~$28 million today) in shares, freeing him from financial worries. That year, Marconi was just 22 years old.

From Warfare to the Marketplace

As a rising star, Marconi quickly attracted public attention. Early in the company's history, he recognized the communication needs of the British Navy, which had a global presence. In 1899, he began providing radio equipment sales and consulting services to both the British and Italian navies. The first contract was worth £6,000 (~$2.5 million today), with subsequent annual revenues exceeding £3,000 (~$1.25 million today).

Despite securing national-level endorsements, the market remained skeptical about the technology's conventional commercial viability. After several years of trial and error, Marconi adjusted his model, shifting from direct sales to leasing. The key characteristic of this strategy, compared to traditional paths, was ecosystem building. Through these partnerships, any product or enterprise could use radio equipment after paying a rental fee, with the sole restriction that customers could only communicate with other Marconi clients.

This strategy led to the birth of countless radio stations and similar competitors.

The Birth of Radio Concept Stocks

With Marconi and other competitors entering the fray, the radio industry flourished, attracting massive capital. In its early days, despite reported losses, Marconi's company didn't deter investor enthusiasm: the technology and business model were still in early development, making losses acceptable. Later, Marconi's company was renamed RCA. The technical advantages and business networks built in the US began to pay off. RCA pooled patents from AT&T, GE, RCA itself, and Westinghouse, creating a formidable commercial fortress, leading to explosive growth in sales and profits.

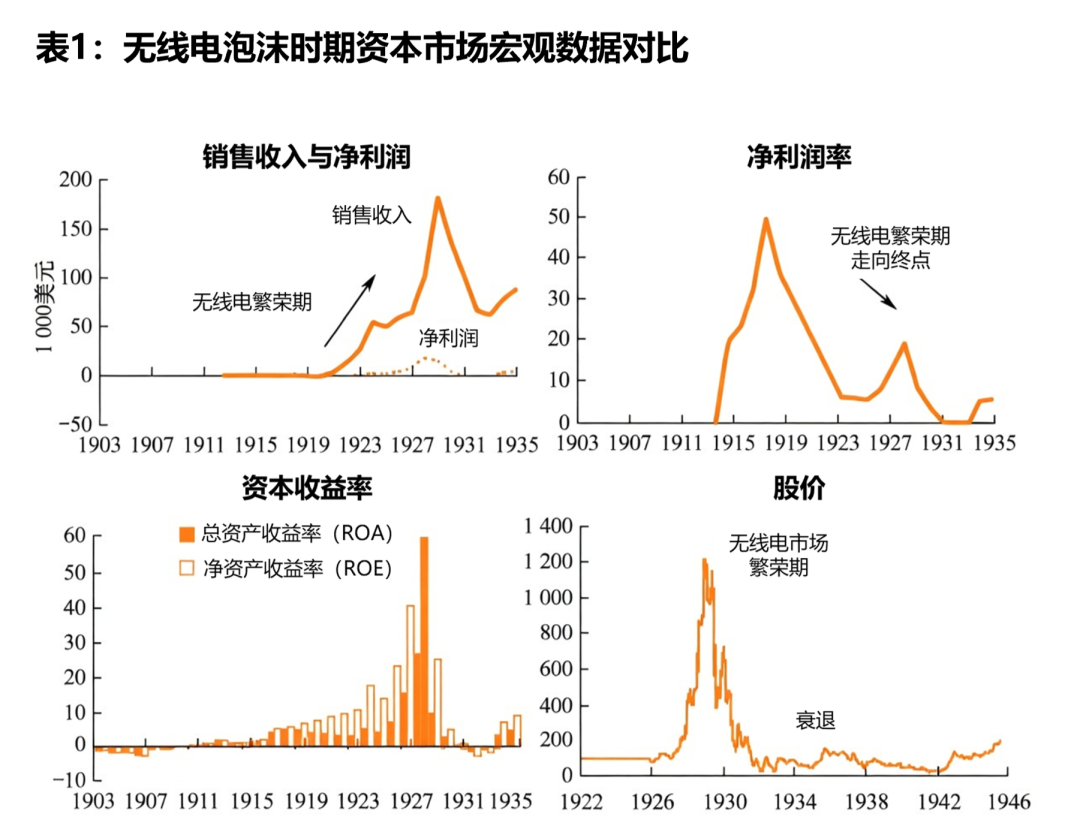

When one person gets promoted, even one's chickens and dogs ascend to heaven. Upstream and downstream companies related to RCA also enjoyed this technological dividend. At the market's peak, some people could simply register a company related to "radio" and easily raise funds and list their stocks. The subsequent story mirrored the railway dividend: capital and companies flooded in; as dividends faded, bank loans replaced earnings for dividend payouts, eventually leading to market collapse and the evaporation of prosperity. Yet, unlike railways, the commercial value of radio was so epoch-defining that this boom lasted nearly two decades. With radio infrastructure complete, the imagination spanned from radios and broadcast stations to televisions and radio media, large enough to sustain long-term market prosperity.

Eventually, the Great Depression arrived. The capital game could no longer be sustained, forcing a return to seeking harder but more practical ways to improve actual sales revenue and net profit for companies and products.

At the Peak of the Internet Wave: A New Technological Social Experiment

After IBM ventured into personal computers and Apple propelled them forward, PC penetration in the mass market reached new heights. This meant certain technologies previously confined to research labs began to emerge – namely, the Internet.

From the Ivory Tower to the Commercial Arena

The origin and birth of the Internet is a well-worn topic, not to be repeated here. More instructive is the path of its commercialization.

A decisive factor in this transition was the US National Science Foundation's (NSF) decision to relinquish control of the National Research and Education Network (NREN) and move towards privatization and self-sustaining operations. During this process, numerous key elements emerged, enabling widespread Internet application: Apple PCs provided the hardware foundation, the World Wide Web provided the framework, and Mosaic provided the entry point. Coupled with NREN's commercialization, a giant industry began its magnificent journey.

In the early days of commercial open-source development, not everyone saw the opportunity. Many related companies adopted conservative approaches. On one hand, their knowledge and insight didn't let them recognize the Internet's potential. On the other hand, in the prevailing business environment, industry giants generated revenue through land-grabbing and building proprietary ecosystems, making them naturally averse to this extremely open new environment. Nevertheless, this wasn't entirely bad for industry development: the resistance of giants created ample market space and opportunities for new entrants.

Netscape: The First to Catch the Big Fish

As one of the earliest pioneers to capitalize, Netscape's peak electrified the entire market. In late 1994, Mosaic Communications faced a legal dispute over its name with Mosaic and subsequently renamed itself Netscape Communications Corporation.

Despite having $12 million in the bank, the company was burning $1 million monthly, forcing Netscape to consider a business model pivot. After some maneuvering, it changed its service model, offering a 30-day free trial followed by a $49 service fee. Combined with the overwhelming performance advantage of its product, it rapidly captured a large market share. The initial goal was merely to boost valuation at IPO, but the strategy worked spectacularly. In its August 1995 IPO, Netscape raised $140 million, catapulting it to its zenith.

However, the success of this sales strategy led to complacency. Basking in the glory of the IPO, Netscape didn't consider building its moat. It neither acquired companies to solidify its upstream/downstream position nor deepened its product to make it better. It even disdained industry partnerships, opting instead for the foolish strategy of inaction.

The outcome was predictable. When the market discovered the huge potential validated by Netscape, a flood of competitors rushed in. Ultimately, Netscape was acquired by AOL.

One Whale Falls, Myriad Things Thrive

Netscape's story is regrettable, but broadly, it was beneficial for market development. Countless profit-seekers and innovators joined the adventure, spawning a dizzying array of projects. Almost in the same year Netscape succeeded, Jerry Yang and David Filo spent significant time studying browser needs, eventually creating a highly efficient information indexing system they named "Yahoo." Meanwhile, at Stanford University, Sergey Brin and Larry Page explored information search engines, aiming to find desired content faster on the Internet. Inspired by these ideas crossing the ocean, Jack Ma in China began preparing to develop "China Pages."

The Pinnacle of Conceptual Bubbles

Compared to past railway and radio technologies, the entry barrier for Internet technology was significantly lower. It didn't require hiring workers to build railways or laying cables, nor obtaining specific permits from the government. Anyone with relevant Internet knowledge could do anything they wanted. The powerful wealth effect, combined with low barriers to entry, ignited a capital market frenzy.

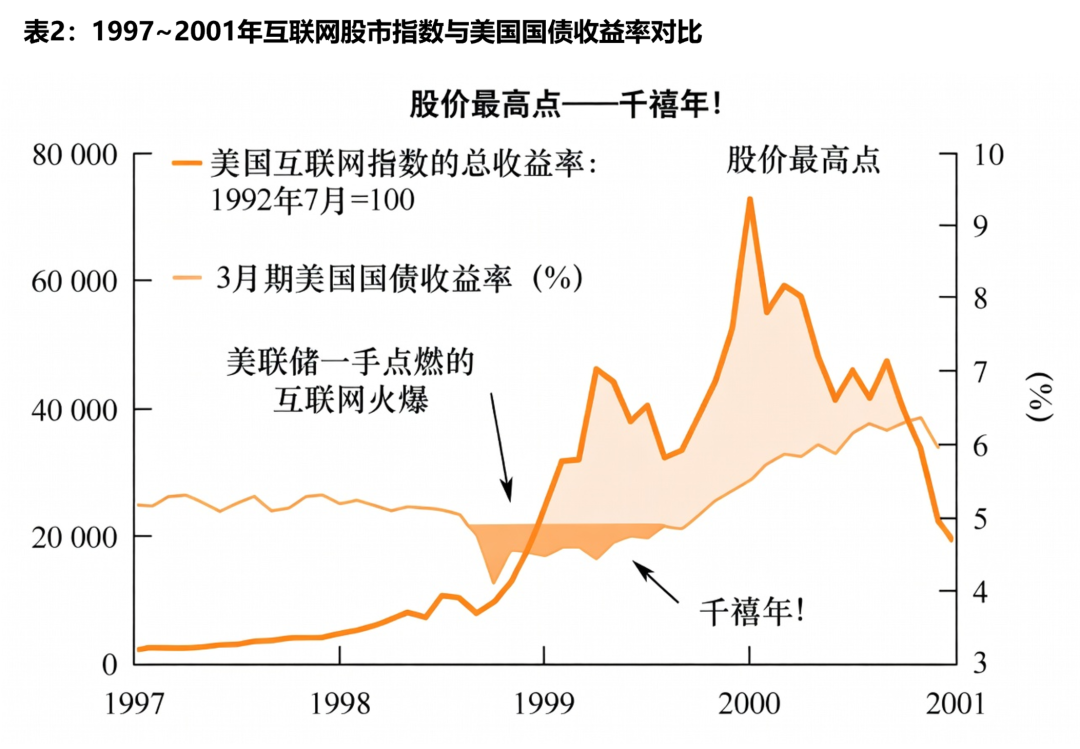

At the bubble's onset, the capital market maintained some caution. However, when they saw crude products born in "garages" like Yahoo and Google also making fortunes through innovative business models, they realized the old market valuation logic seemed obsolete. With Internet tech stocks surging, investors threw their earlier skepticism overboard. Eventually, for fundamental investors, valuations in the TMT sector were artificially inflated without restraint or discrimination, and almost everyone thought this was fine.

As valuations became audacious, professional analysis standards deformed. Typically, the higher the stock price, the higher the valuation an analyst focused on the income statement would tend to assign. To justify valuations when profit anchors could no longer support current prices, the valuation basis gradually shifted from profitability to revenue, and then further dissected into concepts like "click-through rates" and "retention rates" to analyze a company's prospects. This logic chain seemed reasonable, but the fatal flaw was ensuring the validity of business model analysis without historical precedent. The only preliminary method was to listen to the founding team's analysis, i.e., "storytelling."

Ultimately, people no longer paid for technological utility but for stories – whoever had a more compelling business story and broader prospects could raise more funds. A true FOMO (Fear Of Missing Out) began. Initially, people still seriously designed their businesses, but as the market grew more frenzied, some realized that even companies initially unrelated to the Internet could be classified as TMT and enjoy market dividends just by registering a website. Admittedly, some highly forward-looking projects emerged during this storytelling competition, like online shopping, food delivery, and even online pet care. However, the problem was that without adequate infrastructure, stories remained just stories.

Ultimately, the same ending unfolded again. Among the companies on the stock market, few truly adapted to the era and survived. Most relied on bank loans to sustain the false prosperity until interest rates reached a critical point, causing the market to collapse.

Data-Driven Bubble Indicators: How Internet Valuations Failed

We've briefly recounted historical stories. To discover more valuable information, we need to translate these narratives into quantifiable, comparable macro-financial indicators and find patterns. This section uses the Internet bubble (1995–2002) as a core sample, supplemented by historical data from the Great Depression era around 1929, to systematically present the evolutionary path of macro data across the bubble lifecycle from four dimensions: valuation indicators, monetary environment, capital flows, and the real economy. These regular trends will provide a solid "invariant" benchmark for the cyclical analysis of the Crypto market in subsequent chapters.