Powell Bows Out But Stays On, Trump’s Rate Cut Hopes May Be Dashed

- Core Insight: In a rare 8-to-4 split vote, the Federal Reserve kept interest rates unchanged at its April 30 FOMC meeting. The internal division reflects ongoing concerns over inflationary pressures, while outgoing Chair Powell will remain as a governor to defend the Fed’s independence, breaking expectations that new Chair Warsh might come under political pressure to cut rates.

- Key Elements:

- The committee voted 8-4 to hold the federal funds rate steady at 3.5%-3.75%, marking the most dissenting votes since 1992 and signaling a deepening hawkish stance.

- Three of the four dissenting votes opposed the "dovish lean" in the statement's language, with hawkish officials worried that the US-Iran conflict could keep oil prices elevated long-term, upgrading inflation from "somewhat elevated" to "elevated."

- Powell announced he will remain on the Fed’s Board of Governors after his term as Chair ends (May 15), breaking with tradition to counterbalance Trump's political pressure on the central bank.

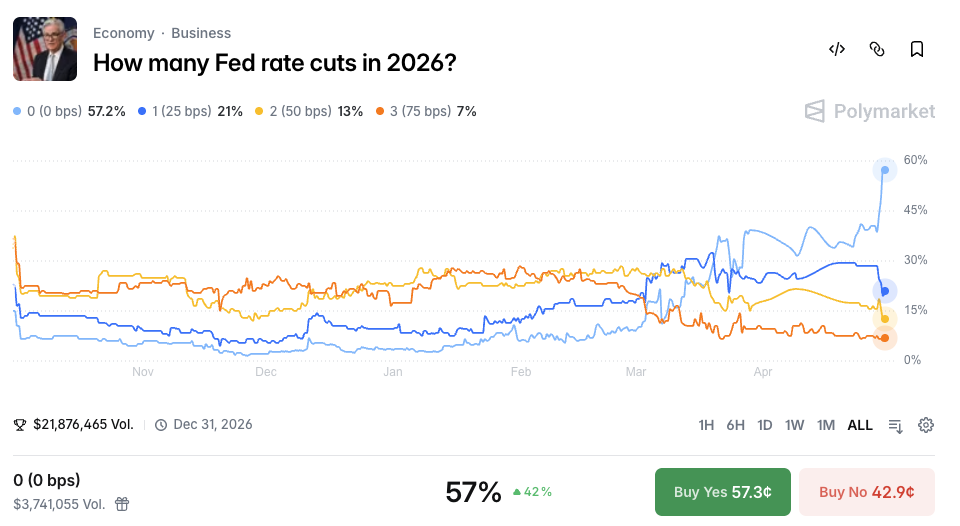

- Prediction market Polymarket shows the probability of "no rate cut in 2026" rising from 38% to 57%, indicating further cooling of rate cut expectations.

- Trump’s preferred new Chair, Warsh, has advanced in nominations, but Powell’s continued presence limits Trump’s ability to install allies on the Board, leaving Warsh to face resistance from a hawkish committee.

Original by Odaily (@OdailyChina)

Author: Golem (@web3_golem)

At 2:00 AM Beijing time on April 30, the Federal Open Market Committee announced its latest interest rate decision, deciding to keep the federal funds rate target range unchanged at 3.5%-3.75%. As expected, the Fed held rates steady, but what unsettled the market was the rare split vote. Of the 12 voting members, the decision passed with an 8-to-4 vote, marking the most dissenting votes against a Fed interest rate decision and policy statement since October 1992.

Meanwhile, at the press conference following the rate decision, current Fed Chair Jerome Powell stated that this would be his last conference as Chair. However, after his term as Chair ends (May 15), he will remain a Fed Governor for an unspecified duration. (Odaily note: Powell's term as a Fed Governor runs until January 2028.)

The implications of this FOMC meeting are significant. On one hand, the rare four dissenting votes indicate a deepening hawkishness at the Fed. On the other hand, Powell's break with tradition—as previous Fed Chairs have resigned their governor positions upon the end of their chairmanship—serves as a setback for Trump, thwarting his plan to use political pressure to force the Fed into cutting rates.

Deepening Hawkish Stance at the Fed

According to the FOMC statement, among the four dissenting votes on the rate decision, Fed Governor Christopher Waller voted against maintaining the rate, as before, favoring a 25 basis point cut. However, the other three dissenting votes—from Cleveland Fed President Beth Hammack, Minneapolis Fed President Neel Kashkari, and Dallas Fed President Lorie Logan—opposed the inclusion of language in the monetary policy statement with an "easing bias." In short, they more clearly opposed signaling future rate cuts.

This rare internal division stems from the US-Iran conflict, which has led to a contraction in global oil supply, and the sustained surge in crude oil prices threatens to exacerbate the already high inflation in the US. Powell acknowledged in the press conference that there was a heated debate within the committee, noting that "the number of officials supporting a shift to a neutral bias has increased, and perhaps the next meeting will consider changing the current easing bias." He also emphasized that the market was overreacting to the dissenting votes. He stated that opposing the language maintaining an easing stance does not mean officials favor rate hikes, saying, "People aren't saying we need to hike now. It's more about discussing whether the Fed should maintain a neutral stance on the policy outlook."

However, the market generally believes that the publicizing of this internal division indicates a deepening hawkishness at the Fed. Previously, the Fed tended to view price increases triggered by geopolitical events as "temporary shocks." For instance, when Trump's tariff policies in 2025 impacted goods trade and caused price increases, the Fed judged it a "one-time price level adjustment" which didn't ultimately prevent the final rate cut decision.

Now, the Fed's attitude towards the oil price surge caused by the US-Iran conflict is changing. The US-Iran conflict has been ongoing for about two months, but so far, peace negotiations have made no substantive progress. The Strait of Hormuz remains under control, and crude oil prices stay high. In this situation, more officials within the Fed believe the high oil prices have transitioned from a short-term impact to a long-term persistent pressure, leading these officials to adopt a more cautious policy stance.

In this FOMC statement, the Fed also changed its description of inflation from "somewhat elevated" to "elevated," indicating growing concern among Fed officials about the potential pass-through effects of oil prices and the general price level. While these statements and leanings are not yet enough for the Fed to decide on a rate hike at the next meeting, they signal to the market that the likelihood of a rate cut is also decreasing. According to monitoring by the Odaily Seer Channel, the probability on Polymarket that "the Fed will not cut rates in 2026" rose from 38% to 57%, an increase of 19%.

However, some believe the four dissenting votes at this FOMC meeting may have been intentional—a warning to incoming Fed Chair Kevin Warsh to maintain the Fed's independence and not blindly follow Trump's orders to cut rates, or face dissenting votes.

Trump's Plan for Political Pressure to Cut Rates Falls Flat

Just hours before this deeply divided FOMC meeting, the Senate Banking Committee advanced Warsh's nomination for Fed Chair. Last Sunday, after the Justice Department concluded its investigation into Powell, Senator Thom Tillis also switched his support to Warsh. Ultimately, the Senate Banking Committee voted along party lines 13-11 to send Warsh's nomination for Fed Chair to the full Senate.

With the key obstacle of Republican Senator Thom Tillis removed, Warsh is highly likely to be confirmed by the Senate before Powell's term as Chair ends. The official 2026 Senate calendar shows a recess from May 4 to May 8, so the earliest possible window for a full Senate vote would be the week of May 11, after the recess returns. Under a Republican-controlled Senate, as long as it gets scheduled, Warsh's nomination could be confirmed between May 11 and May 15.

Although, even after confirmation, Warsh would still need to be appointed by the President (Odaily note: Warsh is not a Fed Governor; he would first need to take Waller's governor seat) and be formally sworn in before officially taking charge of the Fed, he could still potentially chair the June FOMC meeting rather than Powell acting as interim chair. (Odaily note: In 2018, Powell was sworn in 13 days after confirmation, and his second term from Senate confirmation to formal swearing-in took 11 days.)

Consequently, Trump happily reiterated today that it is a good time to lower interest rates, as his chosen new Fed Chair is poised to take over before the next FOMC meeting. Warsh has also made several dovish statements in the past. However, what Trump didn't anticipate is that even as an outgoing Chair, the deeply responsible Powell would find ways to thwart his plans.

Powell stated at the FOMC press conference that he would not act as a shadow chair and would give Warsh ample room to govern. Powell's reason for staying on as a Fed Governor is to defend the Fed's independence. He stated, "What has happened over the past three months [Trump's legal actions against Powell] leaves me with no choice but to remain."

Powell had previously argued that Trump's investigation into the cost of the Fed building renovation was an attempt to apply political pressure for rate cuts from the Fed under his leadership, but Powell ultimately did not let Trump succeed. Now, with Warsh as Trump's chosen new Fed Chair, and given their personal relationship, Powell believes Warsh might ignore objective facts and follow Trump's directives to cut rates upon taking office. Therefore, Powell staying on the Board is precisely to prevent Trump from gaining complete control of the Fed.

Powell's continued presence on the Board limits Trump's ability to appoint allies to the Board from a personnel perspective. Including the incoming Warsh, three of the seven Fed Board members would be Trump nominees, the other two being Michelle Bowman and Christopher Waller. If Powell had followed tradition and resigned from the Board upon leaving the Chairmanship, Trump would have gained another opportunity to appoint a governor, potentially giving him four personally appointed members on the seven-person Board.

Given the Fed's overall demonstrated hawkish stance (coincidentally, the three FOMC members opposing the easing stance are all regional Fed presidents, not Board governors), even the dovish Warsh will face a policy committee extremely resistant to rate cuts upon taking office.

Therefore, Trump's sustained political pressure on Powell and the Fed has, so far, not only failed to achieve its effect but has actually intensified the Fed's resistance. Given the current situation, the best course of action for Trump might be to quickly end the US-Iran conflict or reopen the Strait of Hormuz to lower crude oil prices, thereby providing Warsh with proper justification to persuade other Fed officials to support rate cuts.