$19 in Assets, $575 in Price: The Structural Flaws Exposed by the VCX Pre-IPO Asset Premium Frenzy

- Core Viewpoint: Using the extreme premium and subsequent crash of the Fundrise Innovation Fund (VCX) as an example, the article reveals the structural contradictions in the current Pre-IPO asset market: the massive demand from retail investors for top-tier unlisted assets versus the fundamental flaws in existing compliant and crypto solutions (such as closed-end funds, SPV tokens, synthetic derivatives) regarding access rights, pricing power, and redemption risks.

- Key Elements:

- After VCX's listing, its share price reached a nearly 30x premium compared to its Net Asset Value (NAV) of approximately $19. The core drivers were scarce circulating supply (just over 10%), AI narrative frenzy, and unequal access rights between institutions and retail investors.

- Compared to similar products, DXYZ's premium has significantly narrowed from its peak, while RVI, which lacks an AI narrative, has performed flatly. This indicates that such premiums are highly dependent on narratives and sentiment and are difficult to sustain long-term.

- The essence of VCX is selling "access qualification" rather than asset returns. Its premium faces immense pressure to rapidly converge to zero once the underlying companies complete their IPOs, which fundamentally differs from MicroStrategy's capital operation model.

- While solutions from the crypto market (such as Ventuals perpetual contracts, SPV tokenization platforms) attempt to bypass access barriers, they introduce new risks like diluted rights chains, opposition from target companies, and regulatory uncertainty.

- The fundamental contradiction lies in the fact that all existing solutions are constructed under circumstances where the underlying companies are passive or even opposed. Market maturity requires target companies to actively participate in designing pre-listing participation mechanisms.

The market demand for Pre-IPO assets is real and substantial, but all existing supply-side solutions—whether closed-end funds, SPV tokens, or synthetic perpetual contracts—have structural flaws that cannot be ignored.

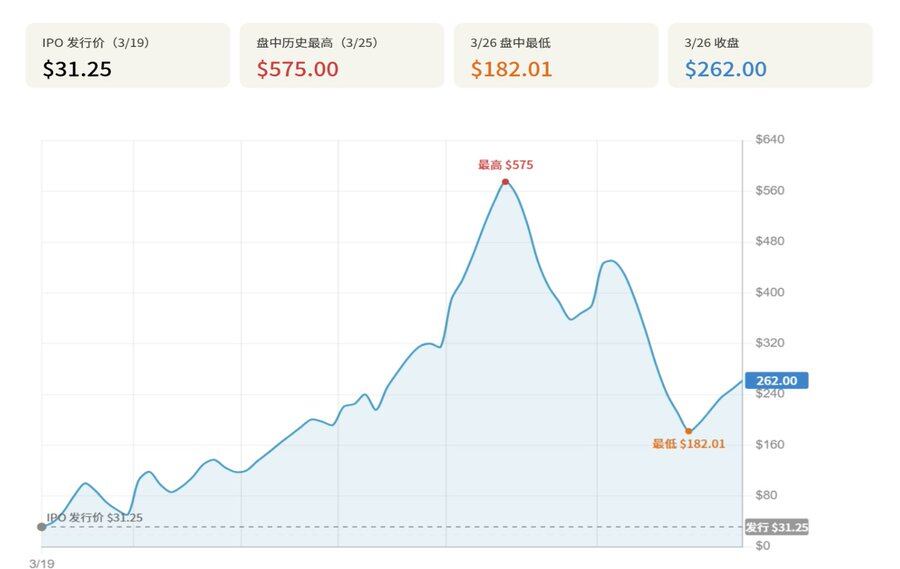

On March 19, 2026, the @fundrise Innovation Fund (NYSE: VCX) listed on the New York Stock Exchange at an issue price of $31.25. Within seven trading days, its stock price surged to a high of $575, marking a 1,740% increase from the issue price, while its Net Asset Value (NAV) per share remained around $19, with a peak premium approaching 30 times. On March 26, short-selling firm Citron Research published a short report and sent a letter to the SEC, causing the stock price to plummet by approximately 40% that day.

This article uses the $VCX event as a core case study, analyzing it from six dimensions: portfolio structure, comparison with similar products, causes of the premium, product nature, rights structure risks, and parallel pathways in the crypto market.

The research suggests that VCX's extreme premium did not stem from expectations of excess returns on the underlying assets but from the superposition of three structural factors: extreme scarcity of circulating shares (non-locked shares barely exceeding 10%), high-intensity endorsement from the AI sector narrative, and institutional channels creating a systemic access disparity for retail investors. In terms of product nature, VCX is essentially a financial instrument selling access rights under a compliant shell. Its premium logic fundamentally differs from the @MicroStrategy flywheel mechanism and faces pressure for its access premium to rapidly approach zero once the underlying companies complete their IPOs.

1. Event Overview: The Surge and Plunge Within Seven Days

On March 19, 2026, the Fundrise Innovation Fund (NYSE: VCX) officially listed on the New York Stock Exchange with an issue price set at $31.25 per share. The core selling point of this closed-end fund was straightforward: packaging equity in Silicon Valley's most elite private tech companies like Anthropic, OpenAI, and SpaceX into a financial product that ordinary investors could freely trade on the secondary market.

However, what happened after the listing was likely unexpected even by the issuer itself. The stock closed up 63% on the first day and continued to climb over the next four trading sessions. By March 25, it hit an intraday all-time high of $575, a 1,739% increase from the $31.25 issue price. According to Bloomberg, as of the close on March 24, VCX traded at $314.99, while its underlying assets' Net Asset Value (NAV) per share was only about $18.97, representing a premium multiple of approximately 16.6 times. At the peak of $575, the market premium approached 30 times the value of the underlying assets.

VCX Price Chart Over 7 Days of Listing (March 19 - March 26)

On March 26, the well-known short-selling firm Citron Research announced it was shorting VCX and publicly stated that the fund was trading severely unanchored, with a stock price above $400 while its asset value was around $19. Citron also sent a letter to the SEC requesting an investigation into whether Fundrise continuously employed social media influencers, YouTube creators, and content publishers for paid promotion of VCX—citing that Fundrise Advisors LLC had already been formally penalized by the SEC in 2023 for paying approximately $8 million to over 200 influencers for promotional activities without proper disclosure. That day, VCX's stock price plummeted by about 40%, falling from a previous close of $380 to around $226, with an intraday low of $182.01.

Key Price Milestones for VCX Since Listing (Data Source: Bloomberg, CNBC, investing.com, data as of March 26, 2026, compiled by Go2Mars)

2. Portfolio Structure: What Exactly Is Being Bought

VCX disclosed its top ten holdings as of February 15, 2026, in its prospectus and on the fund's official website. The portfolio's narrative logic is very clear: Anthropic (20.7%) as the largest position, supplemented by Databricks (17.7%) and OpenAI (9.9%), and rounded out with high-profile star projects like Anduril, SpaceX, and Epic Games.

However, the issues with the portfolio structure itself are precisely the most direct irony of this premium. Using VCX's NAV of approximately $19 as a baseline, and calculating based on the peak market price of $575 on March 25, the market was willing to pay a premium of about 30 times for this batch of Pre-IPO equity. In other words, the price paid by investors buying VCX that day, when translated to Anthropic, implied a valuation premium far exceeding its private financing valuation—and this occurred within the structure of a closed-end fund with extremely low liquidity and holdings that cannot be directly redeemed.

VCX Top Ten Holdings (as of February 15, 2026)

3. Comparison with Similar Products: Similar Logic, Different Fates

VCX is not an isolated case. In fact, between 2024 and 2026, at least three closed-end funds or similar products in the US with core strategies of holding private tech company equity have listed, showing vastly different market reactions.

DXYZ (Destiny Tech100) is the closest reference point to VCX. This fund listed on the NYSE in March 2024 and initially also experienced a retail frenzy, with its price surging intraday to over $100 while its NAV was only about $5, representing a premium close to 2,000%. However, its subsequent trajectory has proven that such a premium cannot be sustained long-term: as of March 26, 2026, DXYZ closed around $29.8, with its latest publicly disclosed NAV at $19.97 (as of December 31, 2025), a premium of about 50%, significantly narrowed from its peak. Its 52-week high was $50.50, still down about 33% from the initial peak.

Comparison of Pre-IPO Closed-End Funds (as of 2026-03-26)

RVI (Robinhood Ventures Fund I) represents another fate. Also in March 2026, Robinhood launched its own closed-end fund product with an IPO price of $25 and a size of approximately $658 million. However, RVI broke its issue price on the first day of trading, closing at $21, down 16%. The market's冷淡态度 formed a stark contrast to VCX's狂欢. As of March 26, 2026, RVI traded around $32, a premium of about 28% from the issue price, but negligible compared to VCX's premium.

The significance of this对比 lies in: for closed-end funds holding Pre-IPO equity, the degree of endorsement from the AI sector narrative directly determines the intensity of market speculation.

- In VCX's portfolio, AI-related holdings (Anthropic, OpenAI, Databricks) account for nearly 50% combined, which is the core reason for its extreme追捧 during the current AI boom.

- RVI's portfolio leans more towards fintech and platform-type holdings like Revolut and Databricks, with relatively sparse AI concepts, leaving retail sentiment with little to leverage.

Citron Research provided a concise estimation framework for this: if VCX's premium eventually compresses to DXYZ's current level of about 35%, the corresponding reasonable price for VCX would be around $26, representing a drop of over 93% from the peak of $575. This prediction does not represent an inevitable outcome, but it accurately describes the path risk of a closed-end fund's premium mean-reverting from extreme highs towards its NAV.

4. Causes of the Premium: Scarcity of Shares, Narrative, and Systemic Disparity

The extreme premium exhibited by VCX after listing cannot be explained by a single emotional factor; it is the叠加作用 of three layers of structural causes.

The first layer is the extreme scarcity of shares. Fundrise's official information shows that VCX had accumulated approximately 100,000 existing investors before listing, whose shares were subject to a six-month lock-up period from the listing date and could not be sold. According to public statements by a fund spokesperson, non-locked shares仅略超 10% of the total. This means that in the face of extremely active buying pressure, the truly tradable circulating shares in the market were极为有限, and any marginal buying would have an放大效应 on the price, pushing the stock price far beyond its NAV. This is the天然放大器 of the closed-end fund structure under special supply-demand conditions.

The second layer is the high-intensity endorsement from the AI narrative. In early 2026, competition in the large model赛道 remained白热化, with Anthropic launching its new Claude agent capable of controlling user computers, OpenAI's valuation持续攀升, and the entire AI industry's high关注度构成 a backdrop of持续输出情绪热度. VCX恰好 completed its listing at this juncture, with Anthropic as its largest holding and OpenAI as its third-largest, effectively becoming an极罕见通道 for retail investors to directly participate in top-tier AI private assets. This scarcity was priced by the market with an extreme premium rate.

The third layer, and the most fundamental one, is a systemic disparity issue, namely: those with the right to enter the private equity market are selling access at a markup to those who cannot enter. VCX's underlying assets were acquired by Fundrise through institutional channels in the primary market or private secondary markets—a domain traditionally accessible only to top-tier VCs or qualified institutional investors. After these assets were packaged into a fund and listed, retail investors were not buying at the primary market price but were taking over at a secondary market price that already carried a significant premium, on top of which they paid an additional NAV premium ranging from 16 to 30 times. This is a systemically完全合法的 information and channel disparity—institutions with原始资产获取权 packaged them into a product tradable on public markets and sold it to retail investors lacking pricing power at the highest price the market sentiment was willing to pay.

5. Product Essence: Selling Access Rights Under a Compliant Shell

The above analysis reveals a core conclusion: VCX did not receive a premium because of outstanding asset selection or higher return expectations, but because it was selling the通道 itself. This leads to a question: What kind of product is VCX?

From a legal form perspective, it is a closed-end基金 registered with the SEC, with transparent holdings and a compliant structure, not本质上 different from any ordinary equity ETF on the market.但从实际功能看, what it sells is not the traditional "investment return expectation" but an asset-side准入资格—previously accessible only to top VC institutions and qualified investors—and this资格 is packaged into units of shares tradable on the NYSE.

Therefore, the market's willingness to pay a 16 to 30 times NAV premium is essentially pricing this access right, not assessing the future收益 of the underlying assets.

From this perspective, the comparison between VCX and MicroStrategy (MSTR) is quite illustrative. Superficially, both are doing similar things: packaging稀缺资产 that are difficult to obtain directly (Bitcoin/top Pre-IPO equity) into securities tradable on the secondary market, exhibiting premiums far exceeding the value of the underlying assets. However, their capital operation logics are fundamentally different:

- MSTR continuously raises funds by issuing convertible bonds and preferred shares, then uses the proceeds to purchase additional Bitcoin. This mechanism赋予 it the ability for dynamic balance sheet expansion and持续增持, giving its stock price premium a certain endogenous维持基础.

- VCX, however, is constrained by the structure of a closed-end基金: its asset size is基本锁定 after issuance, unable to持续买入新资产 through refinancing, and the liquidity of its holdings高度依赖 the IPO or M&A exit of the underlying companies. Once retail sentiment recedes, or after the six-month lock-up period expires and circulating shares increase, the pressure for its premium to narrow will be far greater than that for MSTR.

VCX vs. MSTR (Strategy) Model Comparison

In other words, MSTR's premium is supported by a持续运转的资本机制, while VCX's premium primarily stems from share scarcity +情绪驱动. This product logic itself is not inherently right or wrong, but the risks it蕴含 are more difficult for the market to correctly price than those of ordinary closed-end funds:

Once retail investors buy at a price far exceeding NAV, what they are actually paying for is not the value of the asset itself, but the premium for this access right—and this premium will face pressure to rapidly approach zero once the underlying companies complete their IPOs and direct trading channels form in the public market.

6. Beyond the Premium: Access Barriers and Structured Exits

The problem with this structure extends beyond the premium itself; deeper risks lie in two points.

- First, the attractiveness of Pre-IPO assets高度依赖于 their "not-yet-listed" status, not the intrinsic value of the assets themselves. Once underlying companies like Anthropic and OpenAI complete their formal IPOs and enter the public market, the渠道稀缺性溢价 attached to existing closed-end funds will be迅速抹除—at that point, the pricing of products like VCX will converge towards the public market stock prices. The drawdown risk borne by investors holding positions at premiums of over ten times NAV aligns closely with the historical trajectory of DXYZ.

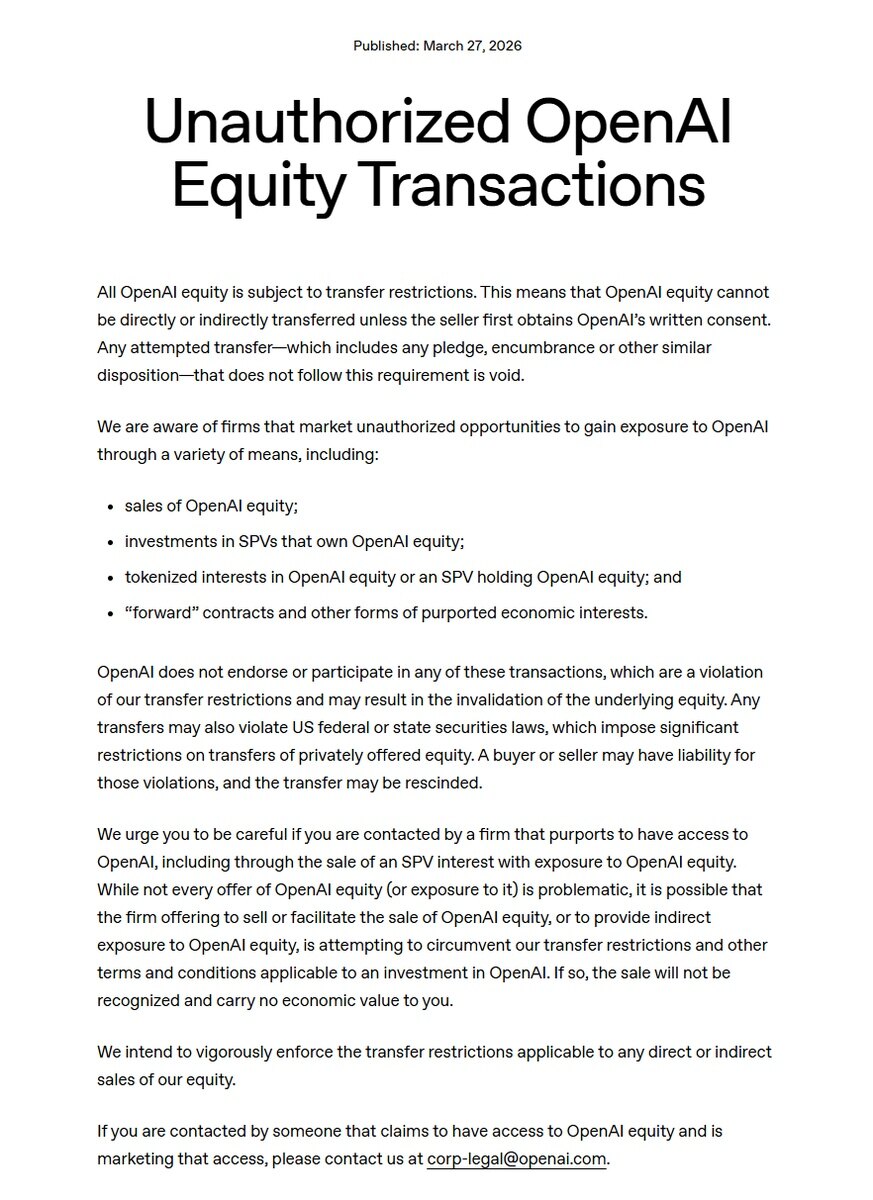

- Second, a more severe issue lies in the uncertainty of underlying rights. As shown in the figure below: Companies like OpenAI and Stripe have already issued严厉警告,明确指出 that holding their equity through SPV structures violates transfer restriction clauses in shareholder agreements, and声明 that corresponding token or certificate holders are not recognized as registered shareholders of the company. If underlying companies refuse to convert shares for related SPVs or refuse to acknowledge their shareholder status during a future formal IPO, secondary market investors who entered at high premiums will ultimately hold仅是对某个离岸 SPV 的合同性权益, not company equity in any sense. The fragility of this rights chain is a structural risk严重低估 by current market sentiment.

OpenAI Official Website Statement Prohibiting Equity Transfers (https://openai.com/policies/unauthorized-openai-equity-transactions/)

Through the above phenomena, two key industry observation perspectives can be extracted:

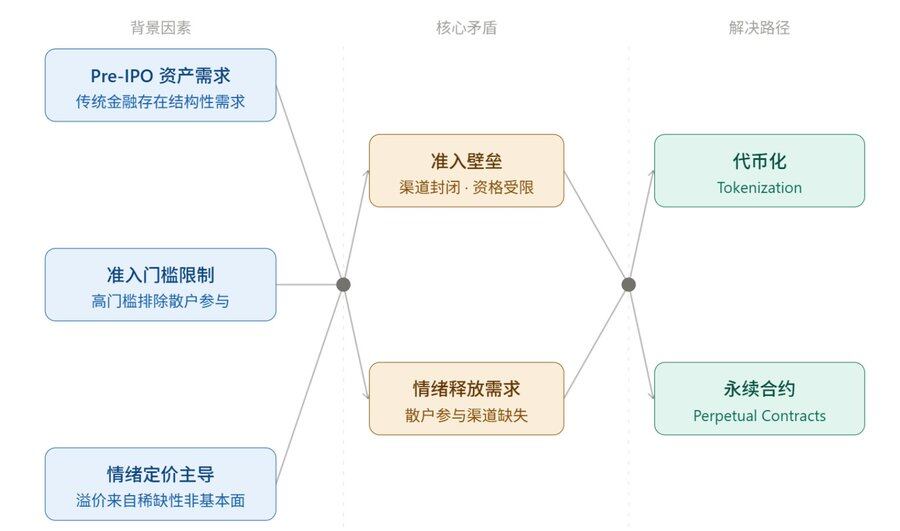

- First, there is indeed庞大真实需求 for early-stage high-growth assets within the traditional financial system, but constrained by existing合规框架 and结构化困境, this demand cannot be met efficiently and fairly.

- Simultaneously, the狂热定价 of Pre-IPO assets by the market is more about paying for their pre-IPO准入壁垒 and流动性溢价, rather than being based solely on the financial fundamentals of the assets.

Structural Contradictions in the Pre-IPO Market and Crypto Mechanism Solution Pathways

Against the backdrop where traditional financial channels struggle to resolve this供需矛盾 and合规摩擦, the tokenization mechanisms in the crypto asset space demonstrate突出的释放潜力: through tokenization + perpetual contract-ization, they can最大程度跳过准入门槛 and结构化困境, completing the release of retail sentiment.

Returning to the Crypto Perspective: From Perpetual Contracts to SPV Tokenization

The VCX case demonstrates the structural limitations of traditional financial channels in resolving the供需矛盾 and合规摩擦 of Pre-IPO assets, while the tokenization and perpetual contract mechanisms in the crypto asset space展示出了 the possibility of skipping access barriers and releasing retail sentiment.

Ventuals: Perpetual Contracts for Valuation Exposure

@ventuals is built on Hyperliquid's HIP-3 standard, allowing users to trade long or short on the valuations of private companies like OpenAI (vOAI), SpaceX (vSPACE), and Anthropic (vANTHRPC), with up to 20x leverage, settled in USDH, a stablecoin pegged to the US dollar. Its pricing method directly maps valuation to contract price, with the计价单位 being company valuation divided by one billion. For example, if OpenAI's current valuation is $350 billion, then 1 vOAI is approximately $350. What users hold is not any form of equity—the platform explicitly states that Ventuals contract holders do not own any form of economic interest in the underlying companies; it is purely speculative exposure to valuation changes.

In terms of scale, Ventuals has grown relatively quickly since its launch in October