Crypto Agent Commercialization Infrastructure Deep Dive: A Core Analysis of Stablecoin-Based "Native Currency Layer" and Settlement Networks

- Core Thesis: The primary obstacle preventing AI Agents from becoming true economic entities is that traditional payment systems cannot support their autonomous receipts and payments. Stablecoins, represented by USDC, combined with dedicated infrastructure launched by companies like Coinbase, Circle, and Stripe, are constructing a native, programmable, 24/7, high-frequency micro-payment "money layer" for AI Agents, fostering a program-driven on-chain micro-economy.

- Key Elements:

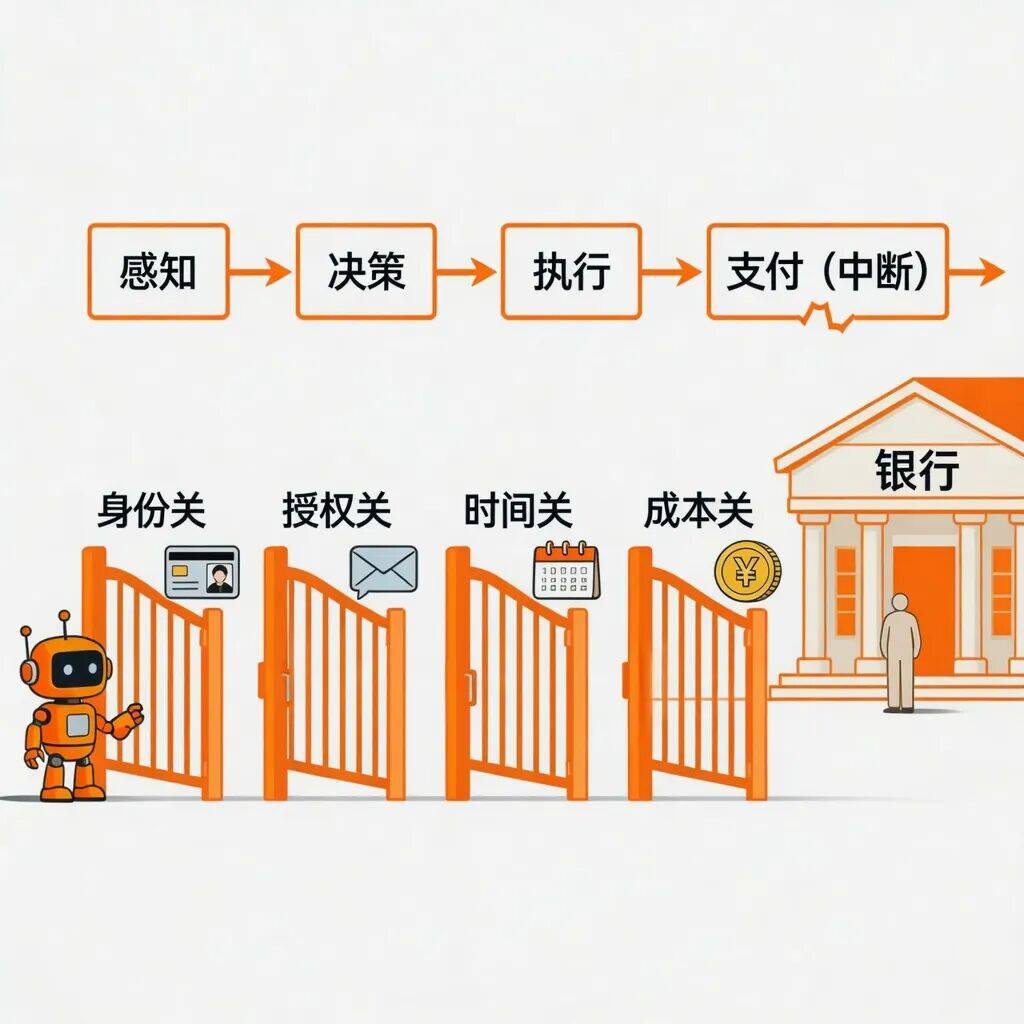

- Four Major Barriers of Traditional Payments: Agents cannot pass identity verification (lacking ID), authorization checks (requiring verification codes), time constraints (not 24/7), and cost hurdles (high fixed fees), preventing them from conducting high-frequency micro-transactions.

- Stablecoin Native Advantages: Programmable (code for automated execution), permissionless (generate wallets independently), 24/7 operation, transparent accounting, and stable value, perfectly matching Agent payment requirements.

- Leading Company Implementations: Coinbase launched AgentKit and the x402 protocol (processing over 50 million transactions); Circle introduced the CCTP cross-chain protocol and AgentStack; Stripe rolled out stablecoin APIs and supports USDC subscription payments.

- Typical Use Case 1 (Nano-payments): The x402 protocol and Circle's Gateway Nanopayments enable micro-payments at the $0.000001 level, unlocking long-tail economies for pay-per-use scenarios like API calls and data access.

- Typical Use Case 2 (Automated Yield Generation): AI Agents can achieve "self-sustainability" through yield-bearing stablecoins (e.g., aUSDC), using interest to cover operating costs. Platforms like Ymax can achieve annualized stablecoin yields of 8-12%.

- Challenges for Mass Adoption: Private key management is vulnerable to attacks (e.g., the Owockibot incident); there are compliance gaps (Agents lack legal person status); and inaccurate AI intent could lead to irreversible financial losses.

For AI Agents to become true economic entities, the first step is not to become smarter, but to have their own wallets.

Generative AI is evolving from "chatbots" into autonomous agents (AI Agents) capable of performing tasks independently. A practical problem has emerged: How do these silicon-based "employees" get paid and make payments? The traditional banking system—with its real-name authentication, manual authorization, and corporate accounts—is fundamentally incompatible with AI Agents.

A rapidly forming answer is to build a native "money layer" for AI using stablecoins (USDC, USDT, and yield-bearing stablecoins). This article will break down the implementation strategies of leading companies like Coinbase, Circle, and Stripe in this space, while also discussing compliance and security risks.

The technical infrastructure is ready, but finding the drive for implementation remains a significant challenge.

1. The "Payment Gap" in AI Agent Commercialization

AI Agents today are already quite capable: booking flights, writing code, calling APIs... but they hit a wall when it comes to "paying." Traditional payment systems are designed for humans—you need an ID, an SMS code to confirm, you must operate during business hours, and each transaction incurs a non-negligible fee. These are all obstacles for an Agent.

Specifically, the traditional payment system presents four key barriers for Agents:

- Identity Barrier: Opening a bank account or credit card requires an ID, facial recognition, and even bank statements—things an Agent cannot provide.

- Authorization Barrier: Payments often require SMS verification codes, manual confirmation, or 3D Secure authentication. Agents can't receive texts or click buttons.

- Time Barrier: Banks process transfers only during business hours on weekdays, while Agents need to operate 24/7.

- Cost Barrier: Fixed transaction fees (e.g., starting at $0.30 for credit cards) make micro-payments like $0.001 per transaction economically unviable. However, Agents' economic activities precisely require such small, high-frequency payments (e.g., pay-per-API-call, usage-based billing).

A more fundamental issue is that the entire payment system was never designed for "program-to-program" direct transfers. Even between two tech companies, the process often involves: Agent generates an order → sends an email to a human → human approves → human logs into online banking to transfer → counterparty's finance reconciles. The Agent handles only the first two and the last steps; the core movement of money from A to B must be done manually.

Existing Attempts: Mimicking Humans, Not Creating New Accounts for Agents

The industry has made numerous attempts, but they essentially force Agents to "pretend to be human":

- Virtual Credit Cards + APIs: Agents use Stripe-like interfaces to make payments, but the underlying card and identity are still linked to a human. When risk control detects anomalies (fast transactions, unusual amounts), it triggers manual verification.

- Robotic Process Automation (RPA): Agents click through banking websites like a human. If the bank's website changes, the CAPTCHA evolves from numbers to sliders, or an extra verification step is added, the script breaks.

- Delegated Payment: A human pre-approves a spending limit for the Agent. However, granting limits, renewals, and auditing expenses still require human intervention.

The common flaw in these solutions: Agents lack their own accounts and can only "exist by proxy." Their autonomy can be revoked by a bank or platform at any time.

Why Stablecoins Are a Better Solution: Providing Agents with a Native "Money Bag"

For Agents to truly manage their own money, they need a monetary system that is programmable, does not require a human identity, operates 24/7, has transparent and auditable ledgers, and maintains relatively stable value. Stablecoins precisely offer these features:

- Programmability: Logic can be written directly into code, enabling automatic payment upon condition fulfillment without human button-pressing.

- Permissionless: Agents can generate their own wallet addresses without queuing up at a bank.

- 24/7 Operation: No weekends, holidays, or after-hours downtime.

- Transparent Ledgers: Every transaction is on-chain, accessible to all for auditing purposes.

- Value Stability: Unlike the volatile prices of Bitcoin or Ethereum, stablecoins are suitable for pricing and long-term settlement.

Stablecoins are not risk-free. Fiat-collateralized ones like USDC and USDT rely on centralized custody and audits, and have experienced brief de-pegs historically; pure algorithmic stablecoins have proven unviable. When referring to stablecoins, this article primarily means regulated mainstream fiat-collateralized stablecoins.

2. Who is Building the Infrastructure for Payment Agents?

The direction is clear, so who is paving the way? Over the past year and a half, leading companies like Coinbase, Circle, and Stripe have moved beyond concepts to launch usable tools and protocols. Each has chosen a specific angle: some focus on Agent wallets and payment rails, others solve cross-chain settlement, and some bridge fiat and stablecoins.

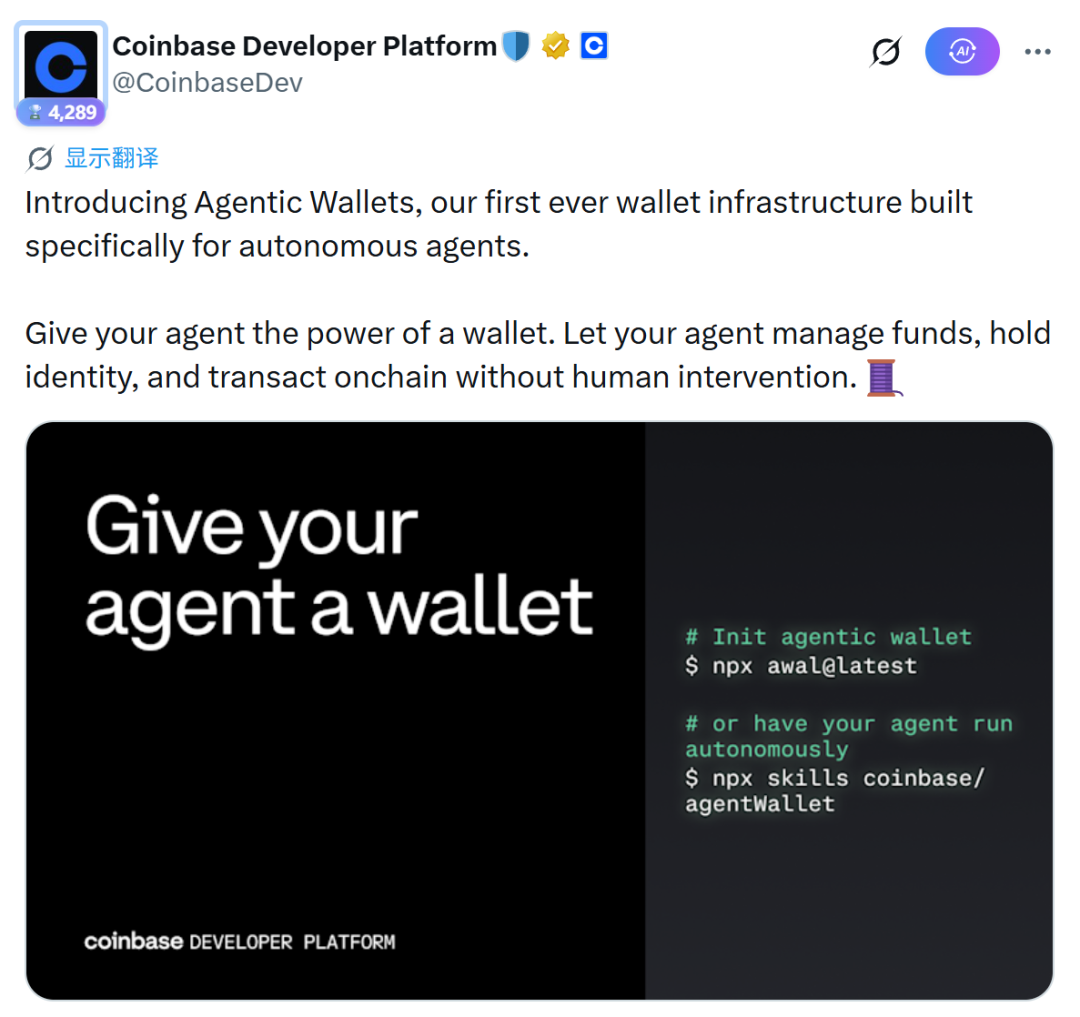

Coinbase: Base Chain + AgentKit Toolkit

Coinbase launched AgentKit, a development toolkit enabling developers to equip AI Agents with on-chain wallets and payment capabilities. In February 2026, they released Agentic Wallets, built-in with five core functions: identity authentication, saving, payment, trading, and yield generation. It uses the x402 protocol co-developed with Cloudflare, specifically designed for machine-to-machine payments.

By early 2026, this protocol had processed over 50 million transactions. In terms of security, Agentic Wallets supports setting limits like "maximum spend per session" or "maximum spend per transaction."

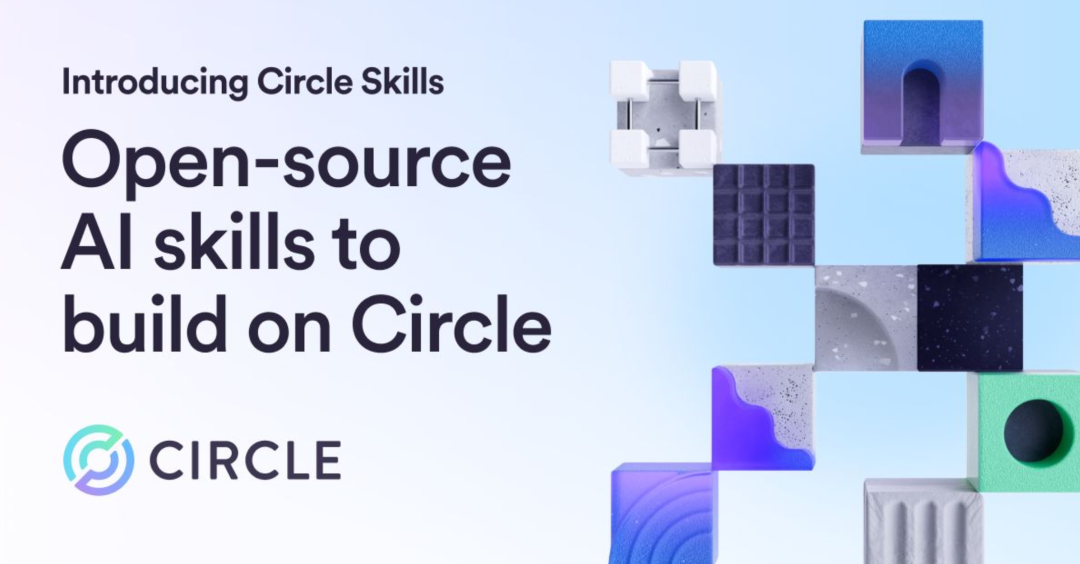

Circle: CCTP Cross-Chain Protocol + AgentStack

Circle's Cross-Chain Transfer Protocol (CCTP) addresses the secure movement of USDC between different blockchains. Using a "burn and mint" mechanism, it doesn't rely on third-party bridges, making it inherently more secure and compliant. Building on this, Circle launched AgentStack in 2025, comprising: Agent Wallets (supporting gasless transactions), CCTP, Gateway Nano Payments (down to $0.000001), and an Agent service marketplace.

CCTP added "Hooks" functionality, allowing AI Agents to attach business data during cross-chain transfers, enabling a single operation like "automatically deposit or invest upon receiving a cross-chain transfer."

In March 2026, Circle launched the Circle Skills open-source library, enabling AI Agents (like Claude) to autonomously decide when to use CCTP or Gateway Nano Payments.

Stripe: Stablecoin API, Bridging Traditional Commerce and the On-Chain World

Stripe officially launched its Stablecoin API in 2025 and, by acquiring stablecoin infrastructure company Bridge, built a compliant bridge from traditional business to the on-chain ecosystem. In October of that year, Stripe launched stablecoin subscription payments, initially supporting USDC subscriptions on Base and Polygon. They also wrote smart contracts to solve the hassle of signing every payment—users can save wallets as payment methods, authorizing recurring automatic debits.

On the backend, Stripe uses its own ledger and KYC/AML compliance monitoring, abstracting away the complexities of blockchain underlying technology like private key management and gas fees. When an AI Agent needs to transact with a traditional merchant, Stripe provides a legally compliant USD conversion and settlement channel.

Beyond these three major players, some traditional leading internet companies have also begun to layout in this area:

- AWS + Stripe + Coinbase (May 2026): Jointly launched USDC-based payment infrastructure, allowing AI Agents to pay for digital services like cloud computing and API calls themselves. Amazon Bedrock's AgentCore Payments serves as the payment layer, settling on Base chain in about 200 milliseconds with a per-transaction cost under $0.01. Stripe implemented its MPP (Machine Payment Protocol), supporting "streaming payments"—real-time charging based on computing power or token consumption per second. On the same day, Stripe and Tempo released the MPP open standard, with Visa also announcing its support.

- Google + Coinbase (September 2025): Launched the Agent Payments Protocol (AP2) jointly, combining Google's Agent-to-Agent communication framework (A2A) with Coinbase's x402 payment rails. This allows Agents to complete the entire process of "negotiating price → paying → issuing receipt." Initial partners include ServiceNow, Salesforce, PwC, Shopee, Worldpay, etc.

- VirtualsProtocol + Ethereum Foundation (March 2026): Proposed ERC-8183 (Agentic Commerce), an on-chain commerce settlement standard specifically for AI Agents. The core concept is "Job": a three-party (client, provider, arbiter) smart contract locks funds and settles according to a state machine of "Create → Fund → Deliver → Complete/Dispute/Expire."

3. Typical Application Scenarios for a Silicon-Based Economy

With the infrastructure in place, if AI Agents truly have their own stablecoin wallets enabling them to receive, pay, transact cross-chain, and earn yield, they will cease to be isolated tools and can form self-operating micro-economies. Here, we analyze application scenarios that have seen partial real-world implementation and show the most promise for realizing the value of a silicon-based economy in the near term.

Scenario 1: DeFi Yield Optimization—Letting Agents Make Money Work

In traditional finance, idle cash in a checking account generates virtually no yield. However, in the DeFi world, stablecoin holders can deposit funds into lending protocols (e.g., Aave, Morpho, Compound) to earn interest. The challenge is that interest rates across different protocols and chains fluctuate constantly, making it difficult to monitor and rebalance frequently. This is where AI Agents excel.

Take the Walbi platform, for example: it processed 187,000 transactions initiated autonomously by AI Agents over 14 weeks, involving 9,500 distinct Agents—all without human intervention. Agents automatically scan lending rates across chains, calculate net yield after accounting for gas fees, and move funds from lower-yielding to higher-yielding pools. Consider ZENITH's approach: deploying independent AI Agents on major public chains like Ethereum, Arbitrum, Optimism, and Base. Each Agent is responsible for its chain's DeFi protocols (Aave, Morpho, Compound, etc.). When an Agent discovers a rate differential on another chain sufficient to cover the cross-chain cost, it uses a protocol like CCTP to transfer funds.

Why are Agents essential for this task? Manual operation faces three hurdles: first, it's impossible to simultaneously track rate changes across multiple lending protocols due to data overload; second, cross-chain operations are cumbersome, requiring manual signing each time; third, the fees and time costs of frequent rebalancing are prohibitive. An AI Agent paired with stablecoins can offer 24/7 monitoring, millisecond-level response, automated execution, with every transaction traceable and auditable.

Scenario 2: Micropayments—Unlocking a Long-Tail "Per-Use" Economy

Traditional payment systems impose fixed transaction fees (e.g., $0.30 minimum for credit cards), making micropayments (like $0.001) economically unfeasible. Yet, for AI services billed per API call, per image generated, or per query, micropayments are the most natural pricing model. The low fees and support for minuscule units make stablecoins a viable foundation for micropayments again.

The x402 protocol co-developed by Coinbase and Cloudflare embeds payment directly into HTTP requests. When a client accesses a protected API, the server returns a 402 status code (Payment Required) along with a payment request (e.g., "Please pay 0.001 USDC"). The client automatically pays via its built-in Agent wallet to access the data or service. By early 2026, this protocol had processed over 50 million transactions. Typical use cases: API paywalls, pay-per-access to valuable datasets, real-time market data subscriptions.

Circle's Gateway Nanopayments goes even further, designed for high-frequency, ultra-small transactions, supporting USDC transfers down to $0.000001 without charging the recipient gas fees. The underlying principle is "batch settlement + state channels": multiple micropayments are aggregated off-chain, with only the net amount settled on-chain once. This allows Agents to pay for each API call, each megabyte of storage, or each second of computing time in real-time, with near-zero fees. Without micropayments, AI Agent commercialization would rely on old models like bundled subscriptions or prepaid credits. With them, Agents can be billed with the precision of a utility meter, and inter-Agent collaboration (e.g., Agent A paying Agent B a few cents for a model inference call) can occur with extremely low friction.

Scenario 3: From "Idle Funds" to "Auto-Yield"—An Advanced Use Case for Yield-Bearing Stablecoins

In traditional finance, corporate checking account balances typically earn minimal interest. Investing requires researching products, signing agreements, and manual transfers, a process too cumbersome and time-sensitive for many small and medium enterprises, which often just give up. Stablecoins combined with AI Agents completely overturn this logic.

When an Agent holds yield-bearing stablecoins (like aUSDC, sDAI, eUSD), its wallet balance automatically accrues yield. These stablecoins are essentially deposit receipts for DeFi protocols, with interest reflected in an appreciating exchange rate against the underlying asset. The Agent can "earn yield by doing nothing." More critically, a well-designed yield management Agent can automatically switch between different yield-bearing assets, achieving the goal of "earning yield while maintaining payment capability."

Ymax's yield orchestration platform launched in February 2026 is a prime example: with a single user authorization signature, an Agent automatically distributes funds across multiple vaults (Morpho, Aave, Compound, etc.), and automatically rebalances based on real-time interest rates—all without user intervention, with yield accruing every second. Another company, aarnaFinance, offers AI-managed vaults aggregating over twenty on-chain yield sources (lending, staking, vault strategies). The Agent dynamically constructs an investment portfolio, achieving stablecoin-denominated annualized yields of 8-12%. For comparison, traditional bank savings accounts typically offer below 0.5%, and USD money market funds around 4-5% APY.

For AI Agents, the ability to earn yield is not just a nice-to-have; it could change the underlying economic logic: a yield-earning Agent can use its interest to cover operating costs (gas fees, API calls), or even accumulate more capital for complex tasks. An Agent can transition from a "money-burning" cost center to a "self-sustaining" micro-economy. When billions of such Agents operate simultaneously, they will birth a new, entirely program-driven financial sub-market.

4. Necessary Challenges for Large-Scale Adoption

The infrastructure is in place, and scenarios are proven, but don't celebrate yet—without overcoming the following hurdles, large-scale commercial use remains a distant prospect.

Private Key Management and Security

A major design flaw in many current AI Agent wallets is directly handing the private key or API credentials to the Agent. If subjected to a "prompt injection attack" (e.g., a malicious actor induces the Agent to perform harmful actions via input), the private key can be leaked. Auditing firm Sherlock identifies "malicious third-party skills," "indirect prompt injection," "credential exposure," and "improper wallet permission design" as the top Web3 Agent security risks for 2026. On-chain transactions are irreversible, a single mistaken signature can lead to permanent loss.

A real-world lesson: In the Owockibot incident of February 2026, an autonomous AI Agent leaked its hot wallet's private key in multiple places, forcing the project team to cut off the Agent's internet and encryption operation capabilities. The project founder admitted: "I severely underestimated the security difficulty of this project; it must be re-architected from a security-first perspective."

Currently explored solutions include:

- Isolated Signing Layer: The Agent can propose "I want to pay X amount to Y," but the actual signing occurs in an independent hardware security module or custody layer.

- MetaMask Smart Account Solution: The Agent can initiate transactions but never possesses the private key. Fine-grained permission control is achieved through ERC-4337 smart accounts and ERC-7710 delegation signatures.

Compliance and Regulatory Gaps

Traditional KYC needs to evolve into "Know Your Agent" (KYA), but this legal category doesn't exist yet. An Agent is not a legal entity; it cannot own assets, sign contracts, or bear liability for breaches. If an Agent pays the wrong party, or gets hacked and transfers funds,