OKX Ventures Research Report: Understanding the Landscape of the "Prediction Market"

- 核心观点:预测市场正从边缘实验走向主流金融工具。

- 关键要素:

- 监管清晰与机构资金加速流入。

- Polymarket与Kalshi形成双寡头格局。

- 周交易额突破25亿美元创新高。

- 市场影响:重塑全球信息聚合与价格发现体系。

- 时效性标注:中期影响

In 2025, with increasingly clear regulations and accelerated inflows of institutional funds, the crypto prediction market is evolving from a fringe experiment into a crucial tool for information pricing—reflecting the real-time game and risk management of future uncertainties through collective on-chain intelligence. From macroeconomic indicators to technological innovations, probability judgments that previously relied on single channels can now be rapidly and accurately repriced by on-chain funds. This shift is impacting how we understand information and market signals.

In layman's terms, prediction markets in the crypto industry are platforms where you bet on future events using cryptocurrencies, such as predicting whether a coin's price will rise or fall, or predicting who will win a competition. If you guess correctly, you make money; if you guess incorrectly, you lose money.

OKX Ventures will continue to monitor this sector and analyze the overall landscape of the "prediction market". Our research reports are for learning and communication purposes only and do not constitute investment advice.

I. Predicting the Origin and Development of the Market

Prediction markets, as information mechanisms that aggregate "collective wisdom," are entering a new phase driven by Web3 technology. Since 2000, this industry has been evolving through academic innovation, compliance competition, and technological paradigm shifts, and by 2025, it will present a new landscape of rapid growth and structural transformation.

The modern model of prediction markets originated from the Iowa Electronic Market (IEM) in 1988, which first proposed the concept of "price as probability," aggregating participants' differing judgments on the outcome of events through the trading of financial contracts. In the 1988 US presidential election, the IEM achieved accurate predictions with small-scale operations. Subsequent research showed that the IEM's election prediction accuracy between 1988 and 2004 was higher than 74% of opinion polls, and it demonstrated a predictive advantage up to 100 days before elections. In 1993, the CFTC's exemption of the IEM established the policy foundation for event-driven contract markets, allowing academic experiments to be tested in commercial applications.

Since the 2000s, the commercialization of prediction markets has surged, but it has faced multiple challenges from gambling and financial regulations. Representative platforms such as Betfair and Intrade grew rapidly, but were also restricted or even shut down due to their gambling nature and compliance difficulties. PredictIt, despite initially receiving a "no-action letter," had it subsequently withdrawn and became embroiled in litigation, highlighting the extreme difficulty of institutionalizing external compliance markets. In contrast, internal prediction markets like Inkling have circumvented regulation and become important tools for corporate decision-making.

The 2020s witnessed two major structural transformations in the industry. First, Kalshi received CFTC approval to become a compliant "event-based contract" exchange, marking formal regulatory recognition. However, the 2023 election market case highlighted the continued sensitivity of themes and the limitations of regulation. Second, the introduction of Web3 technology enabled prediction markets to achieve trustless clearing and settlement through blockchain smart contracts, significantly improving censorship resistance and lowering the threshold for compliant operation. In October 2025, ICE, the parent company of the NYSE, planned to invest approximately $2 billion in the decentralized platform Polymarket. This move was seen by the industry as recognition of the Web3 model by top-tier financial infrastructure, foreshadowing a paradigm shift across the entire industry.

Prediction markets (information markets, decision-making markets, event derivatives) allow participants to place bets, with market prices directly mapping to the probability of events occurring. Their theoretical foundations include the efficient market hypothesis and the principle of collective intelligence: the former posits that market prices can be approximated as probabilities, while the latter emphasizes that collective market decision-making is superior to individual decision-making under diverse, independent, and decentralized participation mechanisms.

Taking the probability of interest rate cuts as an example, let's compare professional data and market forecasts.

Tools like CME FedWatch deduce probabilities from derivative prices, representing institutional expectations, but are affected by tool design and funding structures. In contrast, open prediction markets like Polymarket and Kalshi directly determine probabilities through bets placed by all participants, theoretically offering greater transparency and democracy. Higher platform activity reflects more comprehensive information.

In summary, since the Iowa Electronic Market (IEM) validated price as probability in 1988, prediction markets have undergone a long period of regulatory turmoil. Until 2020, with the introduction of Kalshi compliance and Web3 technology, and finally marked by ICE investment intentions, a paradigm shift of institutionalization and decentralization was initiated. Driven by the synergy between Web3 and traditional financial institutions, prediction markets are currently in a window of opportunity for industry explosion and mechanism evolution. The parallel development of decentralization and institutionalization will reshape the global financial information aggregation and price discovery system.

II. Market Growth and Platform Strategy Analysis

(I) Macro Market Overview: Dual-Top Pattern and Capital Inflow

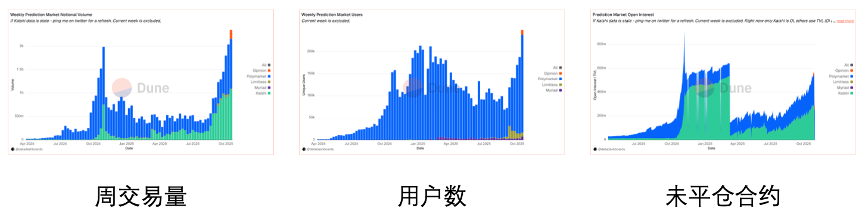

Fueled by the 2024 US presidential election and the influx of institutional capital, the prediction market experienced a structural boom in 2025. The market shifted from being driven by a single event to a sustained financial trading activity, with both capital depth and user base reaching record highs.

Trading Volume Peak Evolution: The market experienced two significant peaks. The first was driven by the US presidential election in October-November 2024, with weekly trading volume approaching $2 billion. The second surge began in July 2025 and reached an all-time high in October 2025, with weekly trading volume exceeding $2.5 billion, surpassing the peak during the election period.

User growth: Market activity is highly positively correlated with transaction volume. In October 2025, the number of weekly active users across the entire market exceeded 225,000, indicating a continuous and genuine influx of new users.

Open Interest ( OI): OI represents the actual capital locked in the market. During the 2024 election, total market OI peaked at nearly $800 million before declining due to settlement. In the second half of 2025, total market OI steadily recovered and stabilized in the $500 million to $600 million range. This indicates that the market has moved beyond simple short-term speculation and established a funding base comprised of institutional and long-term participants.

Competitive Landscape: The market exhibits a duopoly between Polymarket and Kalshi. In 2024, Polymarket held an absolute dominant share of approximately 90%. However, by October 2025, the compliant platform Kalshi's market share had climbed to nearly 60%, surpassing Polymarket in total volume. Despite this concentration at the top, second-tier platforms such as Opinion, Limitless, and Myriad still carved out the remaining market share and secured stable liquidity during specific time windows (such as token issuance periods).

(II) Data Decomposition of Leading Platforms

1. Polymarket: From election bonuses to multi-category retention.

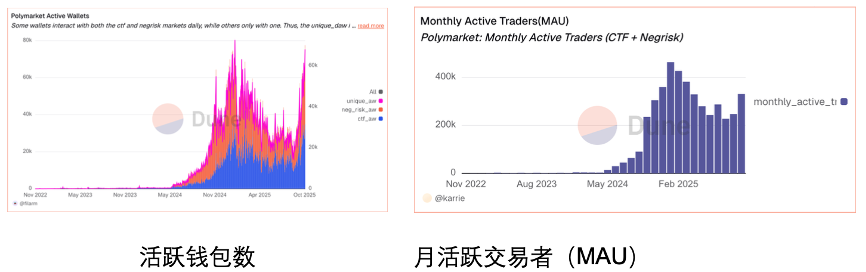

As a leader in the decentralized prediction market, Polymarket's data exhibits strong "event explosiveness" and maintained high user retention after the election by expanding its product categories.

In terms of user data, active wallets reached an all-time high of nearly 80,000 at the end of 2024. Although the number declined after the election, it remained stable at over 60,000 by October 2025, a significant improvement over the beginning of 2024. Monthly active traders (MAU) peaked at 450,000 in January 2025, and maintained over 260,000 active users even after the election hype subsided, demonstrating strong long-tail stickiness of the platform. Daily active users (DAU) reached a single-day peak of 58,000 on October 19, 2025, growing from 10,000 to 58,000, an increase of nearly six times.

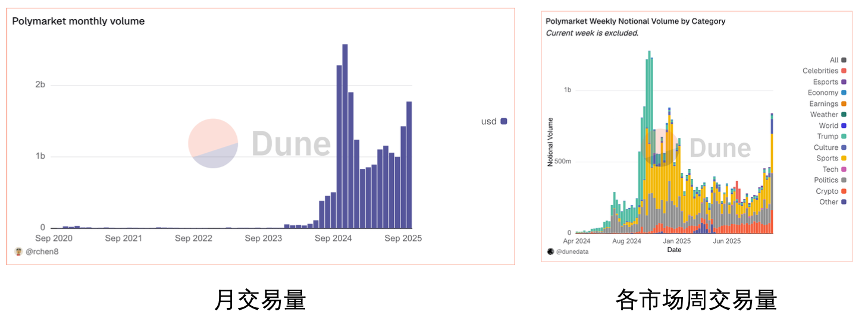

In terms of transaction volume, the historical cumulative transaction volume has exceeded US$18.1 billion, with the monthly peak occurring during the November 2024 election, reaching US$2.63 billion, an increase of approximately 1,000 times compared to earlier data in December 2020. After the election, the monthly transaction volume dropped to approximately US$1.9 billion, a decrease of about 30%-40%, but still far higher than the level in 2023. In terms of growth rate, the year-on-year growth rate reached 5,270% in July 2024, and as high as 26,000% in October 2025, mainly due to the low base effect of the same period of the previous year; on a month-on-month basis, the transaction volume from October to November 2024 also achieved an explosive growth of approximately 750%.

In terms of market structure and categories, during the peak of the 2024 election, "political/economic" transactions accounted for over 60%, with weekly trading volume exceeding $1 billion at one point. By 2025, the focus of trading gradually shifted to "sports" and "crypto assets," with Super Bowl-related contracts reaching approximately $1.1 billion in trading volume, and Bitcoin prediction markets, such as "2025 Bitcoin Price," exceeding $15.5 million in trading volume. Simultaneously, market supply also expanded, with over 7,000 new prediction markets established in April 2025 alone, setting a new record.

2. Kalshi: Exponential growth driven by compliant channels

Kalshi demonstrated its strongest growth momentum in 2025, leveraging its compliance advantages to open up Web2 channels, with all of its core metrics achieving several-fold growth.

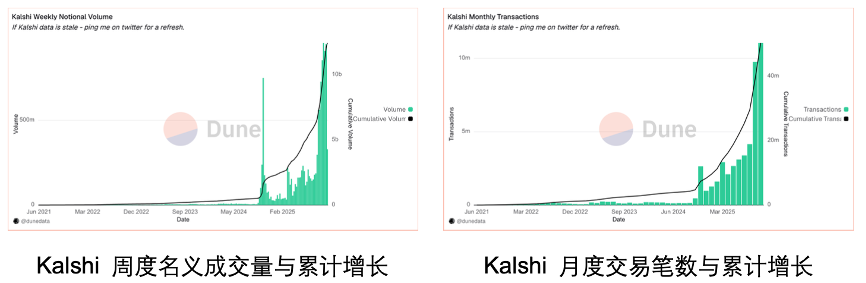

In terms of transaction volume and scale, Kalshi experienced explosive growth in both transaction volume and number of transactions from the end of 2024 to the beginning of 2025, with cumulative transaction value exceeding $10 billion and cumulative transaction volume surpassing 40 million. The average order value was approximately $250–$300 per transaction, demonstrating a clear retail user characteristic. In terms of weekly performance, weekly nominal transaction value jumped from $150 million to $200 million in the fourth quarter of 2024 to over $850 million in the second and third quarters of 2025.

In terms of market share and ranking, as of October 2025, Kalshi's weekly trading volume accounted for 55%–60% of the entire market, officially replacing Polymarket as the most liquid prediction market platform. Regarding total contribution, from September to October 2025, the industry's weekly trading volume exceeded $1.5 billion, with Kalshi contributing $800 million to $900 million in a single week, representing a more than five-fold increase compared to 2024.

In terms of open interest and user structure, open interest surged from less than $50 million at the end of 2024 to over $200 million in the third quarter of 2025; monthly active users (MAU) also expanded from 80,000-100,000 at the end of 2024 to over 400,000 in the mid-to-late 2025. The market structure is highly concentrated, with sports accounting for approximately 45% and politics for approximately 30%, these two sectors contributing over 75% of the open interest, while economics accounts for approximately 10%. On the supply side, the number of effective markets expanded from approximately 300 to over 1,200 by October 2025.

(III) Data Performance of Emerging/Vertical Platforms

Besides the two giants, platforms such as Opinion Lab, Myriad, and Limitless have also generated noteworthy data in specific incentive or vertical scenarios.

1. Opinion Lab: Mainnet Launch Boom

Opinion's daily transaction fees surged on October 25th, exceeding $200,000 in a single day and rapidly pushing cumulative transaction fees from near zero to approximately $320,000. By November, cumulative transaction fees had surpassed $600,000. On its launch day (October 25th, the mainnet incentive launch day), notional trading volume, number of transactions, and number of users all reached their daily peaks. On that day, Opinion accounted for approximately 15%–20% of the total notional trading volume in the market. In terms of funds, the platform's total value locked (TVL) reached a peak of $50 million on October 30th, indicating that large amounts of capital remained temporarily after the incentive campaign.

2. Myriad: Media Traffic Conversion and Retention

In terms of user conversion, it has over 513,000 registered users, but only 30,000 active trading users (USDC traders), resulting in a registered-to-trading user ratio of approximately 17:1. This reflects the conversion funnel from content readers to financial traders, with approximately 30,000 cumulative active wallets. Regarding trading volume, cumulative trading volume reached $12 million (USDC). During the peak period of September-October 2025, daily trading volume approached $2 million, with weekly peaks exceeding $6 million. In terms of fund retention, total value locked (TVL) approached $800,000 in mid-October, representing an overall increase of approximately 300% since August. Open interest (OI) peaked at $500,000 in early October, a month-on-month increase of approximately 2.5 times. In terms of revenue generation, cumulative fee income reached approximately $400,000, with a peak daily fee income of approximately $6,000.

3. Limitless: Data fluctuations under high-frequency excitation

In terms of trading volume, a surge occurred from August to September 2025, with trading volume increasing approximately 25 times. By mid-October, trading volume exceeded $100 million in just half a month, bringing the cumulative total to over $500 million. The first season of the incentive program attracted approximately 34,000 active traders, completing 750,000 trades. Despite the cumulative trading volume reaching $500 million, the peak total value locked (TVL) was only slightly above $1 million, and the extremely low TVL/Volume ratio indicates that users were primarily engaged in ultra-short-term high-frequency trading. After the airdrop ended, the 24-hour trading volume quickly dropped by 34.7% to $7.56 million, and the data gradually returned to normal.

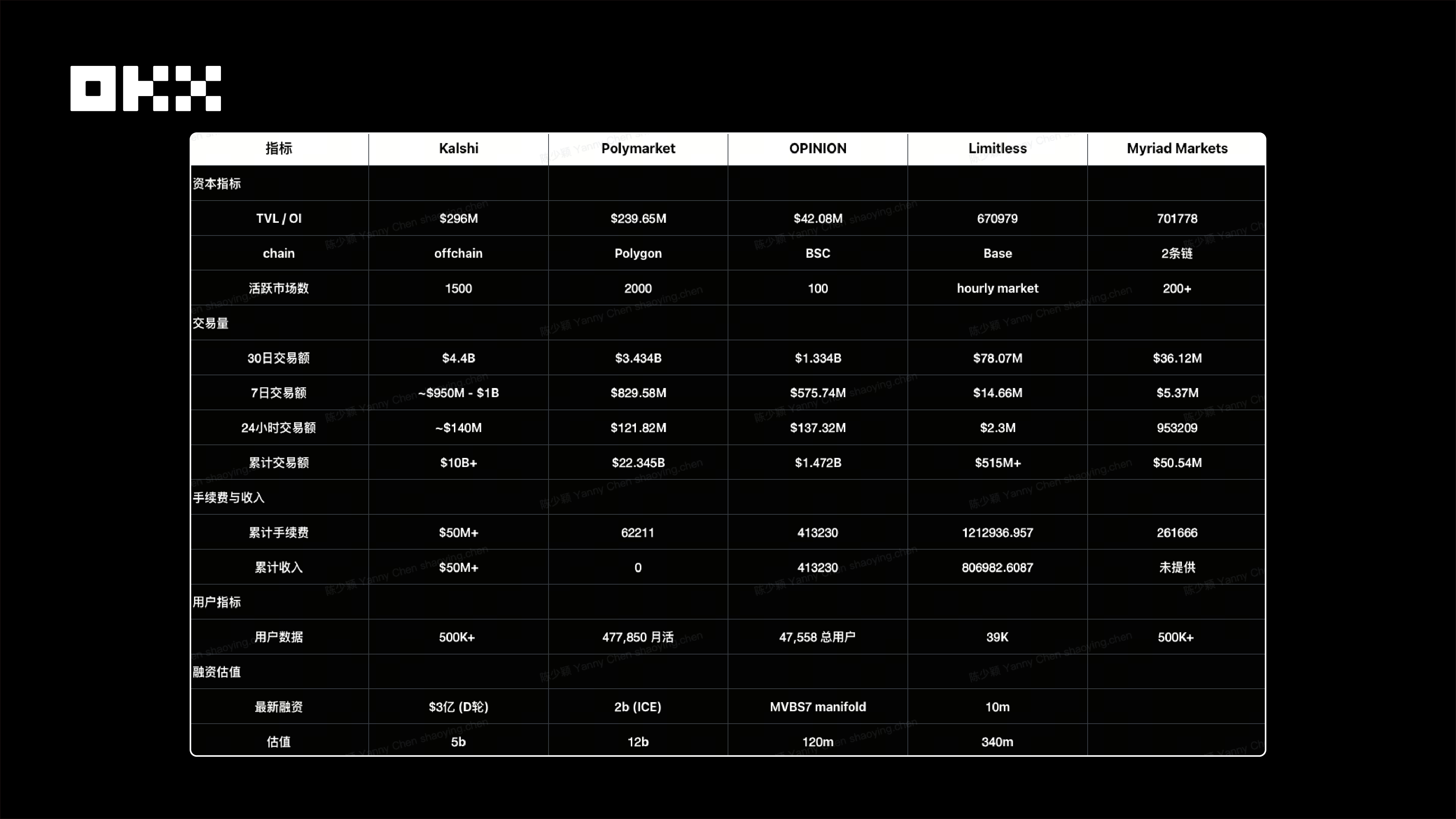

(iv) Horizontal Comparison Table of Core Data

From different indicators

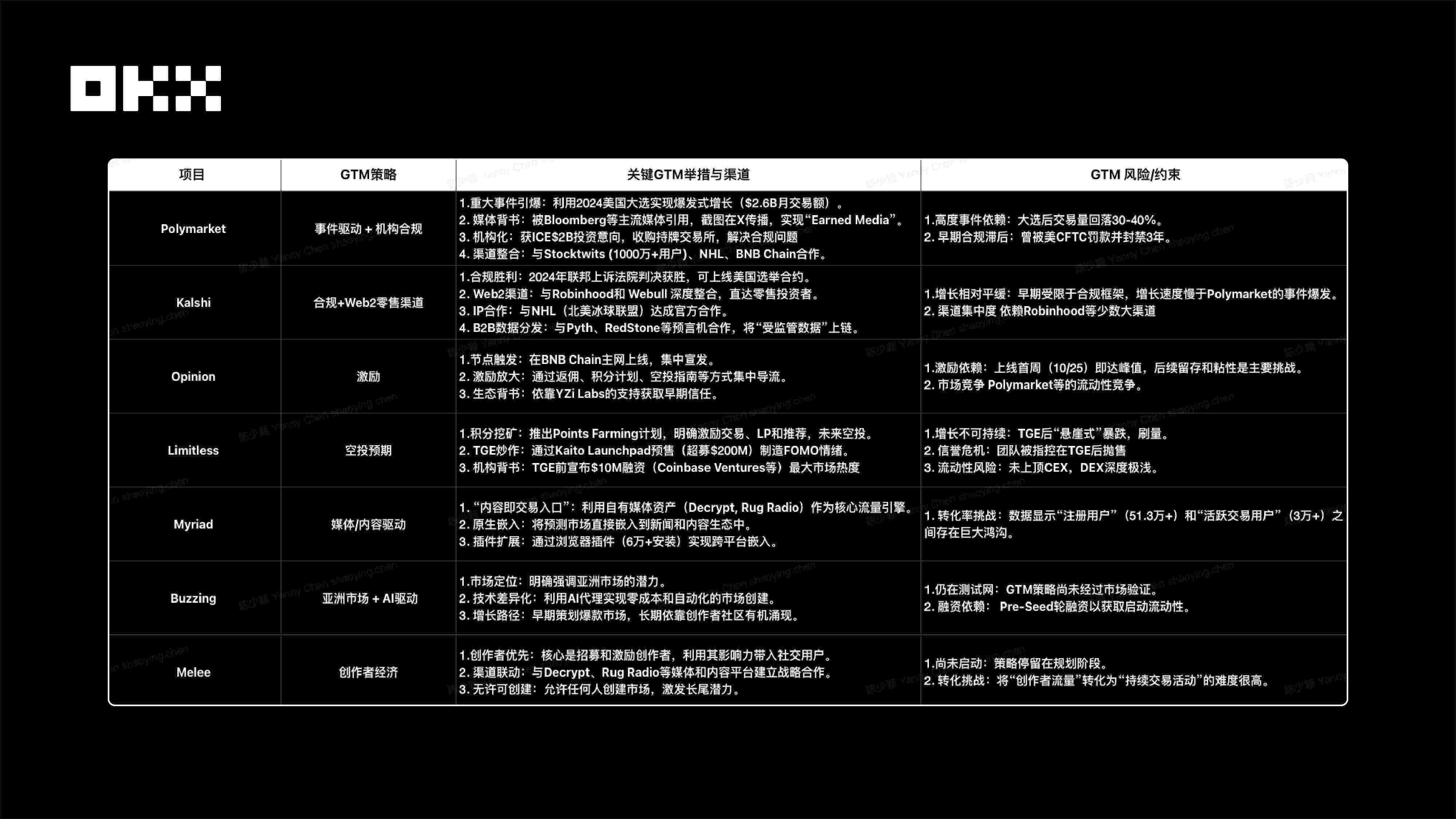

From GTM's perspective

The growth quality brought about by the GTM strategy shows a clear hierarchy : structural growth quality brought about by channel integration (such as Kalshi) is the highest; followed by cyclical bursts brought about by event-driven (such as Polymarket); then high-friction growth brought about by content conversion (such as Myriad); while the growth driven by airdrop expectations through boosting traffic declines relatively quickly.

Compliance is the "underlying anchor" of growth: Polymarket's evolution (event-driven → compliance pains → institutional compliance) proves this point. Despite its explosive growth fueled by the 2024 election (450,000 MAU), its early lack of compliance caused it to miss out on the US market for three years. The 2025 investment offer from ICE and the acquisition of a licensed exchange signify that even leading players must ultimately return to the path of "compliance."

III. Industry Structure Analysis

(a) Track Mapping

1. Infrastructure is gradually becoming modularized, and integrated platforms (such as the early Augur) are evolving into "combinable Lego modules":

Infrastructure protocols such as Azuro, UMA, and Gnosis Omen significantly lower the technical barriers to new projects, supporting multi-chain deployment and pluggable front-ends, enriching the general track, providing entrepreneurs with a plug-and-play product foundation, and fostering more long-tail innovation scenarios, such as AI-driven and community-based gameplay. Gnosis (Omen) / CTF provides an industry-standard asset issuance framework, while Azuro Protocol offers plug-and-play betting middleware, allowing new projects to focus on front-end experience without needing to build their own liquidity pools and odds engines.

This modularity greatly lowers the barrier to entry for new applications, driving the prosperity of many niche sectors, including sports and gamification, and bringing more innovative and diversified development possibilities to the entire prediction market ecosystem.

2. Numerous opportunities in vertical sectors: Sports and the creator economy are becoming growth drivers.

Beyond general-purpose and leading platforms, projects in various sectors, including sports, music, pre-IPO, knowledge verification, social games, AI prediction, and Telegram bots, are rapidly emerging. Viral growth mechanisms such as social media/UGC, creator revenue sharing, and community interaction are becoming common features of these new projects, increasing user engagement and dissemination speed.

The window of opportunity for general-purpose platforms is closing, and opportunities for new projects are increasingly concentrating on vertical markets. Data shows that sports betting and the creator/social economy are currently the two fastest-growing vertical sectors. Sports betting, as a separate sector, has spawned dedicated public chains (such as SX Network), middleware (Azuro), proprietary protocols (Overtime), and even the phenomenal application Football.fun, which reached a TVL of $10 million in just two weeks.

In the creator and social economy sectors, the project model is no longer about "creating your own market," but rather about driving growth by "empowering KOLs." Platforms like Melee offer a 20% revenue share to creators, and Index.fun offers 30% of creator earnings. These platforms are transforming prediction markets from simple information tools into tools for creators and opinion leaders to monetize their influence, further expanding the diversity of the ecosystem and its application scenarios.

3. AI is a standard feature of new projects: automating creation and settlement.

AI has demonstrated enormous potential in scenarios such as market generation, event analysis, content production, settlement, gambling, and risk control. Combined with AI agents or Copilot, it can assist in information archiving, automated market setup, and even predictive analysis, thereby improving user experience and operational efficiency. Artificial intelligence is transitioning from an auxiliary tool to a core product positioning for some new platforms, addressing the fundamental pain points of traditional prediction markets in terms of cost and efficiency. For example, OpinionLabs and BuzzingApp both use "AI agents" as their core, achieving zero-cost creation, unlimited supply, and automated settlement through AI. This represents a fundamental technological disruption to Polymarket, which relies on UMA, and Kalshi, which relies on human compliance.

4. Interaction Layer Restructuring: "Bot" and "Aggregator" Become Key Entry Points

Front-end tools and Telegram bots are significantly reducing user experience friction at the underlying protocol level, thereby creating new opportunities for interaction layers. For example, bots like Flipr and Noise simplify complex predictive trading operations from cumbersome web interfaces to one-click order placement within tweets or group chats, becoming a key GTM strategy for reaching socially driven markets. Meanwhile, aggregators like Flipr and XO Market have solved the liquidity fragmentation problem of leading platforms (Polymarket, Kalshi) and added enhanced features such as leverage, stop-loss and take-profit orders, etc., which are not available on native platforms, precisely meeting the needs of professional traders.

5. Prediction markets become part of the DeFi Lego: composable infrastructure

Prediction markets are gradually evolving from isolated platforms into true "DeFi Lego." On the one hand, some projects (such as Index.fun) are starting to package different prediction results (based on the Gnosis CTF standard) into tradable "creator indices." On the other hand, this data (such as Kalshi's integration with Pyth) is provided to other DeFi protocols (such as Gondor) through oracles, becoming a new source of data for on-chain derivatives, insurance, or lending protocols.

6. Prediction markets can be viewed as financial derivatives: a convergence from "event prediction" to "high-frequency trading".

Product design is rapidly converging from "event prediction" to "financial derivatives." For example, Limitless's 30-minute ultra-high frequency contracts are used as volatility trading tools, Flipr's 5x leverage transforms them into futures, and Touchmarket's price range prediction has evolved into structured options. This indicates that the entire sector is rapidly evolving from its initial purpose of information aggregation into a new branch of high-frequency DeFi derivatives trading.

7. Opportunities in middleware are worth noting, such as data processing and cross-chain functionality.

Middleware and data tools are forming a complete prediction market infrastructure, significantly improving trading efficiency and user experience. For example, Polysights provides a service similar to a "prediction market Bloomberg terminal," aggregating decentralized data from platforms such as Polymarket, Kalshi, and Limitless to track smart money movements and generate advanced arbitrage signals. In the betting and sports sectors, Azuro has demonstrated the opportunity of "backend as a service," with its protocol packaging liquidity pools, odds engines, and sports data oracles (Chainlink), allowing new projects to focus on user experience and GTM promotion.

Meanwhile, cross-chain liquidity and order aggregation become key, with markets distributed across Base (Limitless), Polygon (Polymarket), and Solana (Melee). Flipr aggregates order flows, routes odds, and resolves cross-chain settlements, playing the role of "1 inch in the prediction market." In addition, the opportunity for GTM and interaction layer middleware lies in embedded tools, such as Flipr and Noise, which inject trading functions (such as one-click ordering and leverage) into Telegram Bots, X platform tweets, or content wallets, directly capturing traffic and trading behavior the moment a user generates trading intent.

(II) Comparison of Leading Projects

(III) Regional Analysis of Track Investment

1. North American Market: Compliance and Data-Driven

- Kalshi: Kalshi dominates the US compliant market with its CFTC license, monopolizing the trading of regulated macroeconomic data such as economic indicators and Federal Reserve interest rate decisions. Its market share once surpassed Polymarket by 60%.

- Political and Event Separation (Dual Monopoly): High-profile political events are dominated by Polymarket (global funds) and Kalshi (US compliant funds), forming a clear distinction based on region and funding attributes.

- Avoid platform competition (GTM extremely high): The barriers to entry for leading platforms are already in place. Blindly establishing a new compliant exchange is too costly and risky. The idea of directly challenging Kalshi/Polymarket should be abandoned.

- Mining the “support layer” (tool opportunities): The real opportunity lies in serving giants, such as developing front-end analytics tools for Robinhood/Kalshi channels (Polysights model), or becoming an institutional compliance data distributor.

2. Global/Offshore Market: Essential Need for Sports Products and Product Shortage

- Sports is a basic necessity (the largest vertical category): Sports is the most certain growth track globally. 92% of Kalshi's recent growth comes from sports. The high TVL of on-chain protocols such as Azuro/Overtime verifies its offshore basic necessity attribute.

- Middleware strategy (shovel business): Investing in liquidity and odds middleware like Azuro is the best strategy, as they provide the underlying infrastructure for all front-end sports betting apps, enabling "plug and play".

- Solving the "Missing Piece" Pain Point: Leading platforms lack the "Parlay" function due to compliance and risk avoidance. Platforms that can implement this function in a decentralized manner will have a huge siphon effect on highly engaged gaming users.

- Crypto-native Limitless Short-Term Trading: High-frequency crypto price fluctuation prediction for DeFi traders (such as Limitless mode) is another niche market with strong demand, satisfying the needs of short-term speculation.

3. Asian Market: Social Sharing and Long Tail Micro-Markets

- Mobile-first and social-driven (market characteristics): The Asian market is an untapped blind spot, with users preferring mobile operation, social sharing and high-frequency interaction, which is very different from the institutionalized style in Europe and the United States.

- Abandon grand political narratives (localization): Asian users have little interest in and are sensitive to macro-political issues in Europe and America, so the strategy of copying Polymarket's political betting should be completely abandoned.

- Telegram Bots are King (Best Entry Point): Building a lightweight entry point by leveraging Telegram bots (such as Flipr and okbet) greatly lowers the barrier to entry and perfectly matches the social and payment habits of Asian users.

- Micro-entertainment topic selection (long-tail strategy): Focusing on long-tail micro-events such as e-sports, KOL gossip, and meme pricing, and utilizing Melee-style "creator revenue sharing" mechanism to stimulate KOLs' self-promotion and viral growth.

IV. Analysis of the Current Status of Regulatory Agencies

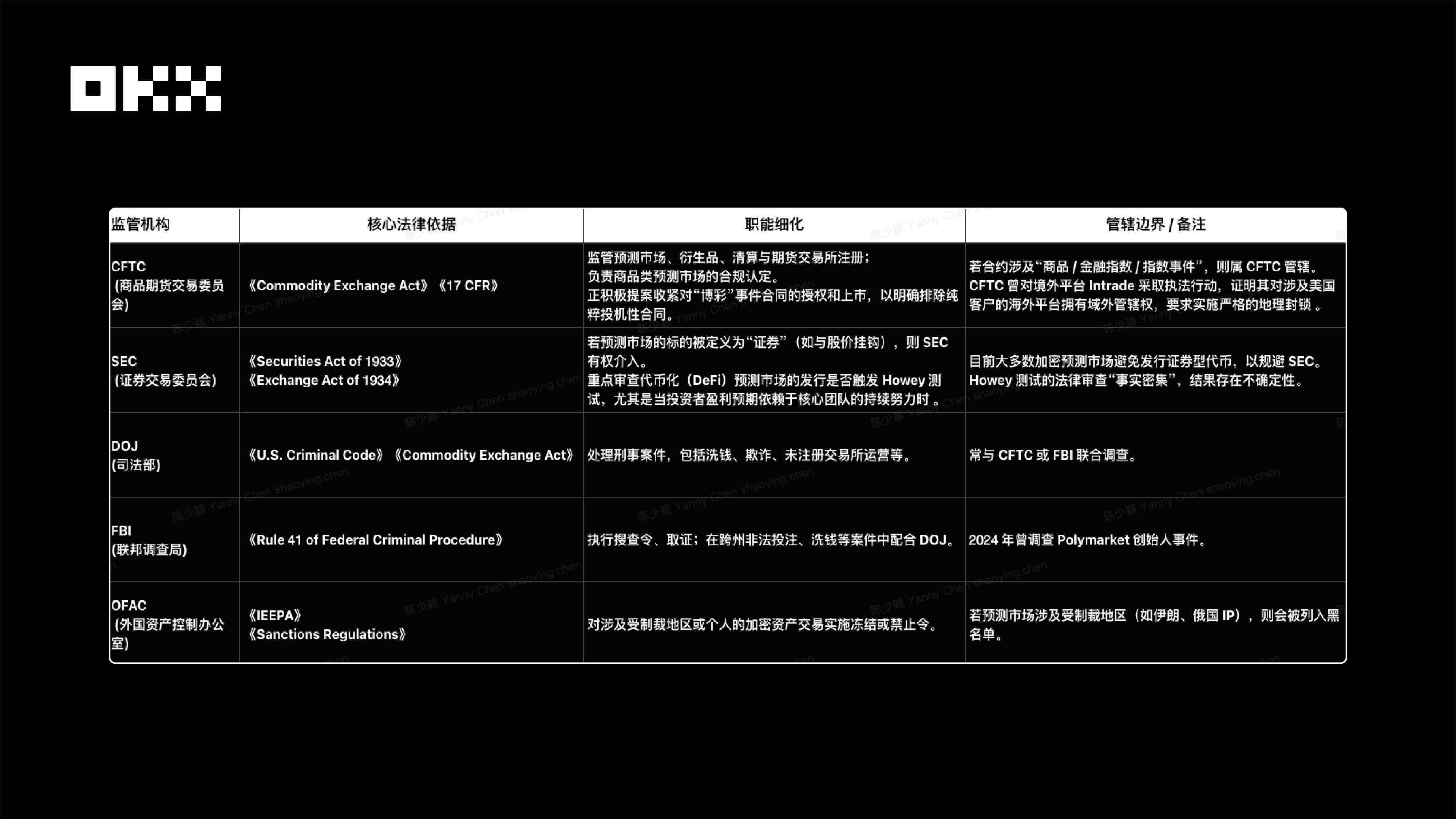

(I) Current Status of the U.S. Regulatory System

The current state of federal regulation can be seen in the following diagram.

State-level and local regulatory status

1. The most intense battleground in the US "federal vs. state" jurisdictional struggle, the outcome of which will have a decisive impact on the industry.

Kalshi and the CFTC argue that the Commodity Exchange Act has exclusive federal jurisdiction, claiming that their "event contracts" are financial derivatives and should take precedence over state law. However, gaming commissions in at least eight states, including New York, argue that this is merely regulatory arbitrage, a "backdoor" to circumvent state-level gaming licenses and taxes. This controversy is not only a debate over the interpretation of legal provisions but also a struggle between regulatory power and fiscal interests. The Kalshi case will be a watershed moment: a victory for Kalshi would clear the biggest obstacle to federal financial regulation; a defeat could force all prediction markets to accept fragmented gaming regulation dominated by 51 states, with unimaginably high compliance costs.

2. Case Study: Kalshi vs. NYGC Litigation

The conflict between Kalshi and the New York State Gaming Commission stems from a core legal contradiction between the Commodity Exchange Act (a federal law) and state gambling laws. The incident began when the New York State Gaming Commission issued a cease and desist letter to Kalshi, accusing it of offering unlicensed sports betting. Kalshi subsequently filed a lawsuit in federal court, arguing that federal law has exclusive jurisdiction over its event contracts and emphasizing that federal jurisdiction should take precedence over state gambling laws to avoid regulatory confusion arising from "51 different and conflicting state laws." The case became further complicated by tribal litigation, which involved Kalshi's partner Robinhood. California tribes also filed a lawsuit, citing the Indian Gaming Regulation Act (IGRA), expanding the jurisdictional issue to a federal, state, and tribal level, significantly increasing the legal and regulatory uncertainty of the case.

Current status of regulation in various countries

The "borderless" or "decentralized" nature upon which prediction markets (especially DeFi platforms) rely is seen as ineffective by regulators. Regulatory bodies in various countries are actively using geo-blocking, payment channel blocking, and ISP bans to enforce their domestic jurisdiction.

The global (non-US) regulatory trend toward prediction markets is clearly tightening . Regulators are not turning a blind eye because of their "innovation," but are instead rapidly integrating them into the two existing regulatory frameworks ( finance or gaming ), and are firmly rejecting overseas operators who attempt to circumvent domestic licenses.

Frankly speaking, the current regulatory landscape is extremely chaotic, and unification is virtually impossible in the short term. Different classifications will lead to drastically different compliance requirements and legal consequences. First, if classified as a commodity or derivative, the regulatory body is the federal-level CFTC (Commodity Futures Trading Commission). The logic is that the market is used to hedge against the risks of future events (such as interest rates and political events), functioning similarly to futures, serving price discovery and risk management. The Kalshi platform is striving to develop along this path and has already obtained authorization from the CFTC.

Secondly, if it is classified as gambling or betting, the regulatory agencies include state betting commissions (such as the New York State Betting Commission) and international betting organizations (such as ANJ in France and UKGC in the UK). The logic is that the market is used to "bet" on the outcome of future events, and the main purpose is entertainment rather than economic risk management. Real-world examples include New York State's accusation that Kalshi offered unlicensed sports betting, and Belgium and other countries directly banning Polymarket.

Finally, if classified as a security, the regulatory body is the federal-level SEC (Securities and Exchange Commission), which primarily targets DeFi platforms. When a platform's profit expectations depend on the continuous efforts of its core team or the underlying asset is linked to a stock price, it may trigger a Howey Test and be considered an investment contract. Real-world evidence is that the SEC continues to focus on scrutinizing token issuances in DeFi prediction markets.

(II) Mechanism Analysis: Business Model, Transaction Mechanism, and Oracles

1. Business Model Analysis

Prediction markets are evolving from simply monetizing B2C transaction fees to a B2B DaaS model that mines data value, and will eventually move towards a hybrid model embedded in the media and creator ecosystem to minimize customer acquisition costs.

- Kalshi's compliant revenue strategy: The platform relies on its regulatory license as a moat and adopts a high-fee centralized model to directly capture B2C transaction revenue, aiming to dominate the compliant financial market trusted by institutions and conservative traders.

- Polymarket's market share priority strategy: Projects use capital support to maintain extremely low rates in order to prioritize market share and data assets, build barriers through network effects, and are committed to mining the long-term data value of B2B DaaS.

- Limitless's protocol value strategy: The platform adopts a DeFi native model, using an economic flywheel of fee-based token buybacks to directly empower the protocol token with platform value, relying on token incentive mechanisms to compete for high-frequency liquidity in the crypto space.

- Cultivate Labs’ robust B2B strategy: This model avoids speculative markets and focuses on providing SaaS solutions that support decision-making for large enterprises and governments, locking in predictable recurring revenue through strong customer relationships.

- Potential and challenges of hybrid models: Embedded models, represented by Melee and Myriad, have the largest potential market size by reaching a broad range of internet users, but the challenge of transforming entertainment-oriented forecasts into sustainable economic models still needs to be addressed.

2. Analysis of Trading Mechanisms: Liquidity, Matching, and Capital Efficiency

From theoretical models (CLOB, LMSR) to specific platform implementations (Polymarket, Kalshi, etc.), this paper systematically compares their differences in matching mechanisms, architecture, position sizing mechanisms, capital efficiency, and risk characteristics.

- How to trade off between "efficiency" and "decentralization"

- Capital efficiency (a strength of CEXs): Models like CLOB (Order Book) are highly capital efficient, offering low slippage and deep liquidity. This is essential for attracting professional traders and high trading volumes.

- Decentralization (the soul of DeFi): Models like AMMs are permissionless and censorship-resistant. This is the core value of prediction markets as a "global information market."

- None of today's market leaders can perfectly achieve both. They have all made compromises:

- Kalshi: 100% efficient, 0% decentralized. (Fully embraces regulation and centralization)

- Gnosis/Omen: 100% decentralized, 0% inefficient. (LMSR is too inefficient, nobody uses it.)

- Polymarket: A hybrid compromise. (It trades efficiency for off-chain matching, but sacrifices some decentralization and introduces regulatory risks.)

- Limitless: Technical compromise. (Attempting to force on-chain CLOB implementation using L2 speeds, but still relying on professional market makers.)

- The industry's holy grail is to find a model that combines the efficiency of CLOB with the passivity and decentralization of AMM.

- The "clumsiness" of the old AMM lies in its uniform distribution of liquidity across the entire range of 0% to 100%, resulting in 90% of the funds being "dormant" in a 50/50 market, which is extremely inefficient.

- "Centralized liquidity" (the core concept of Uni v3) is the holy grail for resolving this contradiction, allowing liquidity providers (LPs) to "smartly" concentrate 100% of their funds in high-probability trading ranges such as 40%-60%.

- This new model perfectly combines two major advantages: it achieves the capital efficiency and low slippage of CLOB while retaining the decentralized spirit of AMM, which is permissionless and passively "sets up and forgets".

- Therefore, the future of the market is a "smart AMM" specifically designed for prediction markets, with "centralized liquidity" at its core, and may use Uni v4's "Hooks" to add advanced features such as dynamic fees.

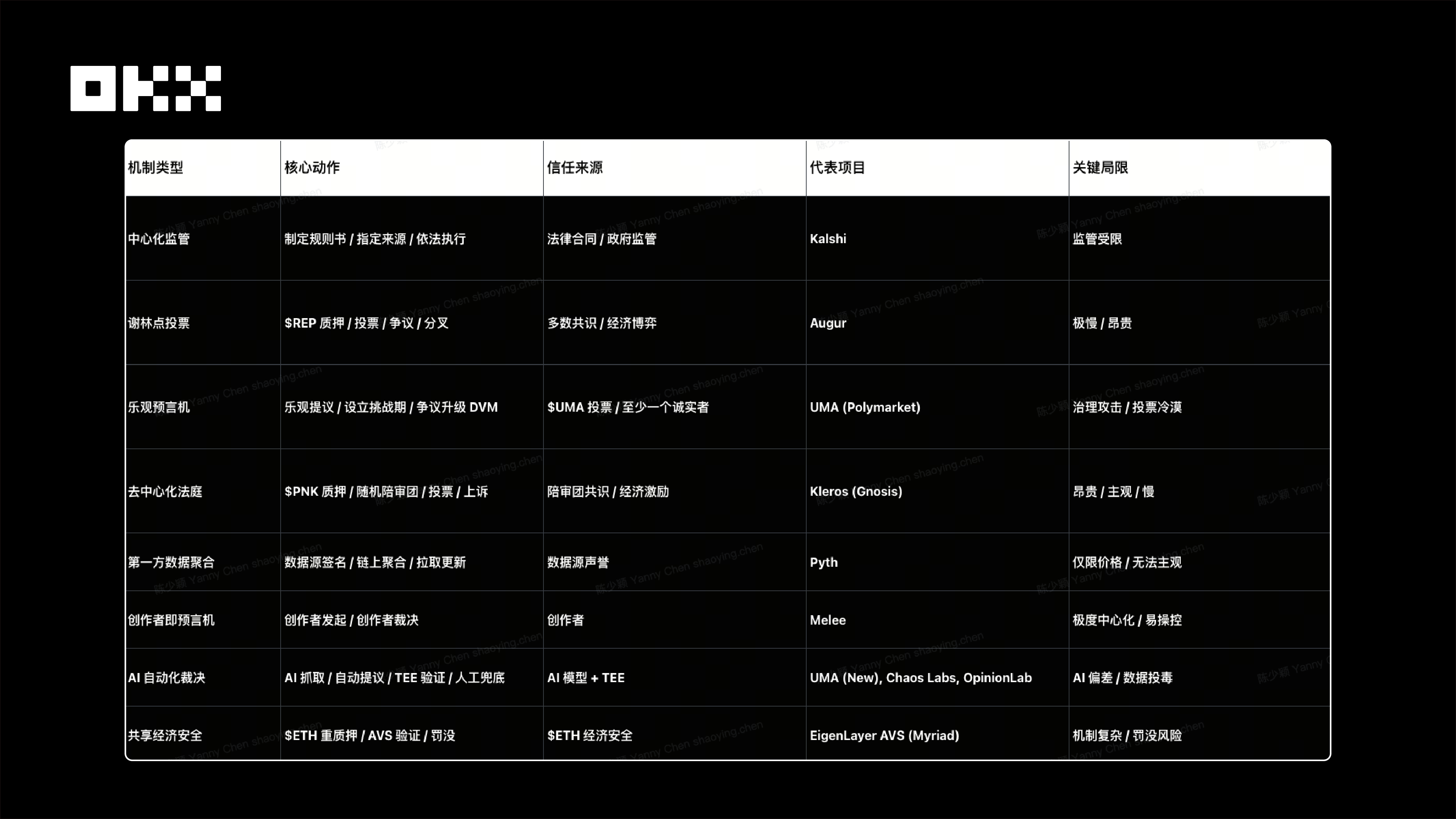

3. Oracle Mechanism: Trust, Security, and Settlement Efficiency in Result Adjudication

- Authoritarian Epistemology: A Centralized Regulatory Model (Kalshi)

- Mechanism: Based on the legal rules, the platform designates a single authoritative data source (such as a Department of Labor report) to make the ruling.

- Sources of trust: legal contracts and CFTC regulation.

- Advantages: High legal certainty, suitable for institutions.

- Limitations: The scope of the ruling is limited by regulatory approvals (such as the previous ban on political predictions).

- Consensus Epistemology: Decentralized Schelling Point Model (Augur, UMA)

- Mechanism: Utilizing the Schelling point principle, token holders are incentivized to vote on the outcome.

- Augur: REP token holders vote, triggering a fork in case of disputes (extremely slow and expensive).

- UMA (Polymarket): Optimistic Oracle Mode. Passes by default if uncontested; if contested, it escalates to a DVM vote.

- Security assumption: Cost of corruption (CoC) > Benefit of corruption (PfC).

- Limitations: Risk of governance attacks. The 2025 UMA incident in the Ukrainian market, where it was manipulated by whales, demonstrates that token voting is vulnerable to attacks when participation is low.

- Judicial Epistemology: Decentralized Arbitration Tribunals (Kleros)

- Mechanism: Randomly selected jurors adjudicate complex/subjective disputes, similar to an on-chain court.

- Advantages: Highly expressive and capable of handling ambiguous/unstructured disputes.

- Limitations: High cost and slow speed.

- Evolution of emerging mechanisms

- Pyth Network (Pull Model): Top-level institutions directly sign on the blockchain, high frequency, low cost, suitable for objective price data (such as Limitless).

- AI + TEE (Opinion/Buzzing): AI Agent automatically captures and adjudicates data, TEE hardware ensures the reliability of the process, and the community provides a safety net. This addresses the adjudication costs in the long-tail market.

- AVS Shared Security (EigenLayer): Provides economic security by leveraging heavily staked ETH, addressing the risk of attacks caused by insufficient market capitalization of a single oracle token.

- Melee (Creator as Oracle): Allows creators to customize rules and make decisions, adapting to the social/entertainment long-tail market.

- For protocol developers: Reject "omnipotent oracles" and embrace specialization.

- Financial/Price Markets: Choose first-party data source models such as Pyth or Chainlink, pursuing ultimate performance and fidelity. Avoid using voting mechanisms to determine high-frequency prices.

- Objective/Binary Events: An optimistic model based on EigenLayer AVS is adopted to ensure that the "cost of corruption" is always higher than the "benefits of corruption".

- Subjective/ambiguous events: Integrate decentralized arbitration systems such as Kleros, or accept Kalshi's centralized "rulebook" model.

- Long Tail/Social Market: Adopt Melee's "Creator as Oracle" model and clearly position it as a social entertainment product.

- For bettors and investors, oracle risk should be taken into full consideration.

- Primary risk control: Before trading, you must read and fully understand the market's decision-making mechanism.

- Define your bet: Ask yourself, "Am I betting on the outcome of the event, or on the voting behavior of a group of anonymous token holders?" The 2025 Polymarket attack proved that the two can be completely opposite.

- Risk pricing: For markets that rely on cryptoeconomic consensus, the risk of oracles being manipulated must be factored into one's odds and position models as a core element.

- From "truth machines" to "verifiable automation"

- The development of market oracles is a history of moving from idealism to pragmatism, and then towards specialization and modularization.

- The earliest "truth machines" (such as Augur) failed due to their complexity and inefficiency.

- More pragmatic "optimistic models" (such as UMA) have been broken down due to their fatal flaws in isolated economic security.

- Regulated "authoritative models" (such as Kalshi) are technically robust, but their application is severely limited.

- The future will be neither completely centralized nor purely decentralized, but rather a combination of hybrid and specialized approaches.

- Hybrid: Integrating AI automation (improving efficiency), human supervision (ensuring security), and the security of the sharing economy (addressing economic vulnerabilities) to form a composite system of "human-machine loop".

- Specialized: Embrace specialized models like Pyth (specializing in price) and Melee (specializing in social), which achieve their core value by sacrificing universality.

Ultimately, the "oracle problem" will not be "solved" by a single mechanism, but rather "managed" by an evolving ecosystem comprised of multiple mechanisms. This ecosystem will provide different trade-offs for different types of "truth" based on four dimensions: security, speed, cost, and expressibility.

V. Compliance is the anchor of growth

2025 marks a paradigm shift in prediction markets from fringe experimentation to financial infrastructure. Catalyzed by both capital and regulation, the sector has formed a duopoly of Kalshi (compliant finance) and Polymarket (offshore DeFi), and the business logic is shifting from single transaction fees to B2B data distribution and embedded traffic monetization.

Compliance has become the anchor of growth, and regulatory characterization will determine the market ceiling. The industry is gradually differentiating into institutionalized paths based on licenses and censorship-resistant paths based on code. Infrastructure is also developing professionally, with matching mechanisms evolving from AMM to CLOB to improve capital efficiency. Oracles are upgrading from simple token voting to a hybrid defense system of "AI automation + AVS shared security" to deal with governance attack risks.

Looking ahead, the window of opportunity for general-purpose platforms has closed, and growth will break through to the two ends of verticalization and socialization. One end is the deep institutionalization of sports and macro derivatives, and the other end is the "financialization of attention" combined with the creator economy. The final outcome of the race will be a coexistence of high-frequency compliant data flow and long-tail social game.

Disclaimer

This article is for informational purposes only. The views expressed are solely those of the author and do not represent the position of OKX. This article is not intended to provide (i) investment advice or recommendations; (ii) an offer or solicitation to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. We do not guarantee the accuracy, completeness, or usefulness of such information. Holding digital assets (including stablecoins and NFTs) involves high risk and may result in significant volatility. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For your specific circumstances, please consult your legal/tax/investment professional. You are solely responsible for understanding and complying with applicable local laws and regulations.