Could it be removed from the index? Strategy is mired in a "quadruple strangulation" crisis.

- 核心观点:微策略面临多重压力,市场信心受考验。

- 关键要素:

- mNAV溢价大幅收缩至1.2。

- 股价负溢价,年内跌幅40.9%。

- 高管减持与增持比特币放缓。

- 市场影响:引发DAT行业信任危机与资金流出担忧。

- 时效性标注:短期影响。

Original author: Nancy, PANews

The crypto market is in turmoil, with Bitcoin's weakness dragging down the overall market and accelerating the bursting of the bubble, leaving investors feeling extremely cautious. As one of the important crypto bellwethers, leading DAT (crypto treasury) company Strategy is facing multiple pressures, including a significant narrowing of the mNAV premium, reduced coin hoarding, executive stock sales, and the risk of being delisted from the index, severely testing market confidence.

Strategy faces a crisis of confidence and may be removed from the index.

The DAT (Digital Amount and Data) sector is currently facing its darkest hour. With the continued decline in Bitcoin prices, the premiums of many DAT companies have plummeted, their stock prices are under constant pressure, and buying activity has slowed or even stopped, putting their business models at risk of survival. Strategy has not been spared either, facing a crisis of confidence.

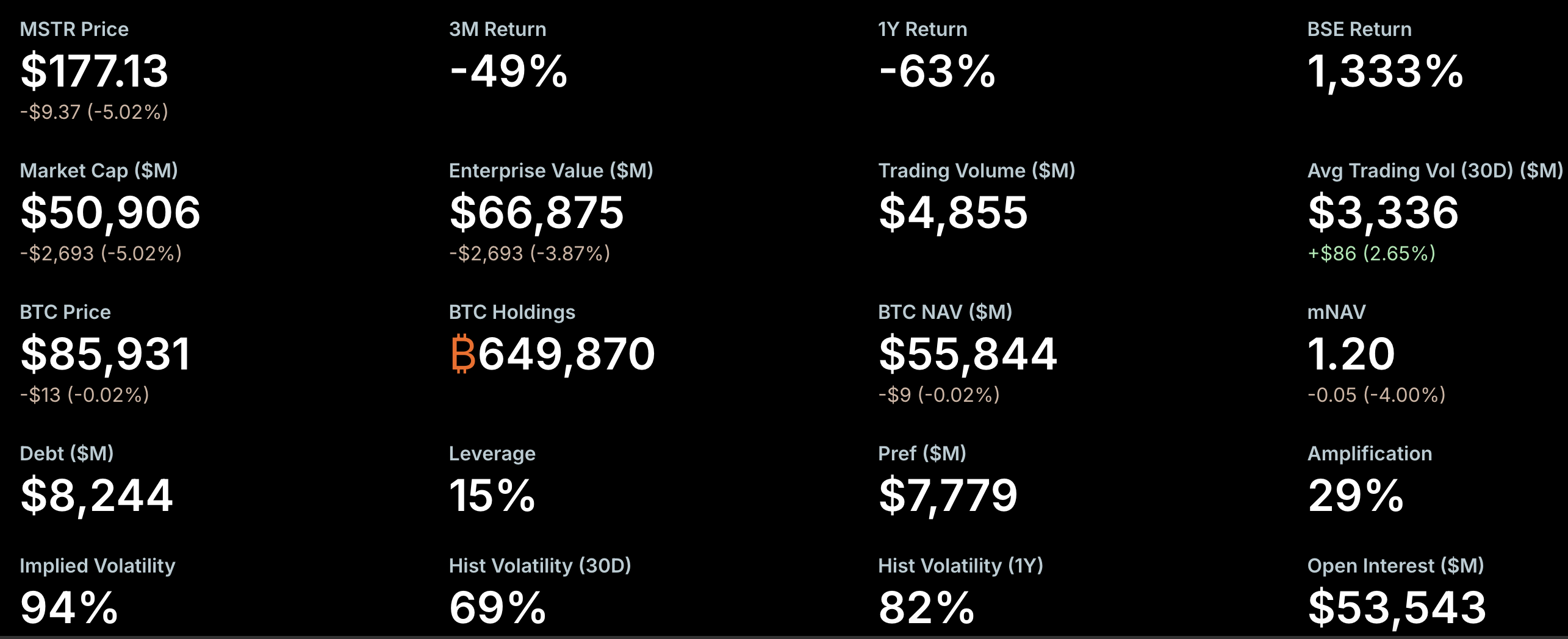

mNAV (market capitalization multiple) is a key indicator of market sentiment. Recently, Strategy's mNAV premium has contracted rapidly, nearing the critical threshold. StrategyTracker data shows that as of November 21, Strategy's mNAV was 1.2, having previously fallen below 1, representing a drop of approximately 54.9% from its historical high of 2.66. As the largest and most influential DAT company, Strategy's failure to maintain its premium has triggered market panic. The underlying reason is that the decline in mNAV weakens its financing capabilities, forcing the company to issue new shares to dilute existing shareholders' equity, putting pressure on the share price, and thus further reducing mNAV, creating a vicious cycle.

However, Greg Cipolaro, Global Head of Research at NYDIG, points out that mNAV has limitations as a metric for evaluating DAT companies and should even be removed from industry reports. He believes that mNAV can be misleading because its calculation does not take into account the company's operating business or other potential assets and liabilities, and is usually based on an assumed number of outstanding shares, excluding convertible debt that has not yet been converted.

The poor stock performance has also sparked market concerns. StrategyTracker data shows that as of November 21, Strategy's MSTR stock had a total market capitalization of approximately $50.9 billion, lower than the $66.87 billion market capitalization of its nearly 650,000 Bitcoins (with an average holding cost of $74,433). This means the company's stock price is trading at a "negative premium." Since the beginning of the year, MSTR's stock price has fallen by 40.9%.

This situation has sparked market concerns about Strategy's removal from indices such as the Nasdaq 100 and MSCI U.S. JPMorgan Chase predicts that if MSCI removes Strategy from its stock indices, related capital outflows could reach as high as $2.8 billion; if other exchanges and index compilers follow suit, the total outflow could reach $11.6 billion. MSCI is currently evaluating a proposal to exclude companies whose primary business is holding Bitcoin or other crypto assets, and which hold more than 50% of their balance sheets, and will make a final decision by January 15, 2026.

However, the risk of Strategy being removed from the index is relatively small at present. For example, the Nasdaq 100 index undergoes a market capitalization adjustment on the second Friday of December each year. The top 100 are retained, those ranked 101-125 must have been in the top 100 the previous year to be retained, and those above 125 are unconditionally removed. Strategy remains in a safe range, with its market capitalization ranking within the top 100, and recent financial reports show solid fundamentals. In addition, several institutional investors, including the Arizona Pension Plan Investment Board, Renaissance Technologies, the Florida Pension Plan Investment Board, the Canada Pension Plan Investment Board, Swedbank, and the Swiss National Bank, disclosed holdings of MSTR stock in their third-quarter reports, which also supports market confidence to some extent.

Strategy's recent pace of accumulation has slowed significantly, interpreted by the market as a lack of "ammunition," especially given its Q3 financial report showing cash and cash equivalents of only $54.3 million. Since the beginning of November, Strategy has added a total of 9,062 Bitcoins, far less than the 79,000 Bitcoins added during the same period last year, which is also influenced by the rising price of Bitcoin. This month's increase mainly came from last week's latest purchase of 8,178 BTC, with other transactions mostly involving hundreds of Bitcoins.

To replenish its capital, Strategy has begun seeking international market financing and launched a new financing instrument, perpetual preferred stock (which requires high dividends of 8-10%). Recently, the company raised approximately $710 million through the issuance of its first euro-denominated perpetual preferred stock, STRE, to support its strategic development and Bitcoin reserve plan. It is worth noting that the company currently has six outstanding convertible bonds, with maturities between September 2027 and June 2032.

Furthermore, the movements of senior executives have also increased market attention. Strategy disclosed in its financial report that Executive Vice President Shao Weiming will leave the company on December 31, 2025, and that he has sold $19.69 million worth of MSTR stock in five transactions since September of this year. However, these sales were conducted according to a pre-arranged 10b5-1 trading plan. Under U.S. SEC rules, a 10b5-1 trading plan allows company insiders to trade stocks with pre-defined buying and selling rules (specifying quantity, price, or timetable), thereby reducing the legal risks of insider trading.

Multiple analyses suggest that debt risks have been exaggerated, putting significant pressure on investors who paid high premiums.

In response to the gloomy sentiment in the crypto market and multiple concerns about the DAT business model, Strategy founder Michael Saylor reiterated the "HODL" philosophy in an article, expressing optimism about the recent decline in Bitcoin prices and remaining bullish on the future. He even emphasized that Strategy's holdings would not be sold unless Bitcoin fell below $10,000, in an effort to boost market confidence.

Meanwhile, the market has also analyzed Strategy from multiple perspectives. Matrixport points out that Strategy remains one of the most representative beneficiaries of this Bitcoin bull market. The market had previously worried that the company might be forced to sell its Bitcoin holdings to repay debts. However, based on its current balance sheet structure and debt maturity distribution, it judges that the probability of being "forced to sell Bitcoin to repay debts" is low in the short term and is not the main source of risk. Currently, the biggest pressure comes from investors who bought at high premiums. Most of Strategy's financing occurred when its stock price was near its historical high of $474 and its net asset value per share (NAV) was at its peak. As NAV gradually declined and the premium compressed, the stock price also fell from $474 to $207, resulting in significant unrealized losses for investors who entered at the high premium range. Using the recent Bitcoin price increase as a reference, Strategy's current stock price has clearly corrected from its previous high, making its valuation relatively more attractive, and the expectation of its inclusion in the S&P 500 index in December remains.

Crypto analyst Willy Woo further analyzed Strategy's debt risks, expressing "high skepticism" about a potential liquidation during a bear market. In a tweet, he stated that Strategy's current debt primarily consists of convertible senior notes, which can be repaid with cash, common stock, or a combination of both upon maturity. Of this, approximately $1.01 billion in debt will mature on September 15, 2027. Woo estimates that to avoid needing to sell Bitcoin to repay the debt, Strategy's stock price at that time must be above $183.19, roughly equivalent to a Bitcoin price of around $91,502.

CryptoQuant founder and CEO Ki Young Ju also believes that the probability of Strategy going bankrupt is extremely low. He stated bluntly, "MSTR would only go bankrupt if an asteroid hits Earth. Saylor will never sell Bitcoin unless shareholders demand it, a point he has repeatedly emphasized publicly."

Ki Young Ju points out that even if Saylor sells just one Bitcoin, it would shake MSTR's core identity as a "Bitcoin vault company," triggering a double death spiral for both Bitcoin and MSTR's stock price. Therefore, MSTR's shareholders not only want Bitcoin's value to remain strong, but also expect Saylor to continue using various liquidity strategies to ensure that MSTR's price rises in tandem with Bitcoin's.

Addressing market concerns about debt risk, he further explained that the majority of Strategy's debt is in the form of convertible bonds, and failing to reach the conversion price does not imply liquidation risk. It simply means the bonds need to be repaid in cash, and MSTR has multiple ways to handle maturing debt, including refinancing, issuing new bonds, obtaining secured loans, or using operating cash flow. Failure to convert does not trigger bankruptcy; it's simply a normal occurrence due to debt maturities and is unrelated to liquidation. While this doesn't mean MSTR's stock price will remain high indefinitely, the idea that they would sell Bitcoin to inflate the price or go bankrupt is utterly absurd. Even if Bitcoin falls to $10,000, Strategy will not go bankrupt; the worst-case scenario is simply debt restructuring. Furthermore, MSTR could also choose to raise cash using Bitcoin as collateral, although this carries potential liquidation risk and will therefore be a last resort.