In-depth analysis of the truth behind xUSD's de-pegging: The domino crisis triggered by the October 11 crash.

- 核心观点:Stream Finance因策略失败致xUSD脱锚巨亏。

- 关键要素:

- 链下交易爆仓致9300万美元损失。

- 采用高杠杆递归循环放大风险。

- 缺乏透明度与真实Delta中性策略。

- 市场影响:引发DeFi领域信任危机与监管关注。

- 时效性标注:短期影响

Original author: Trading Strategy

Compiled by Odaily Planet Daily ( @OdailyChina )

Translator | Wenser ( @wenser2010 )

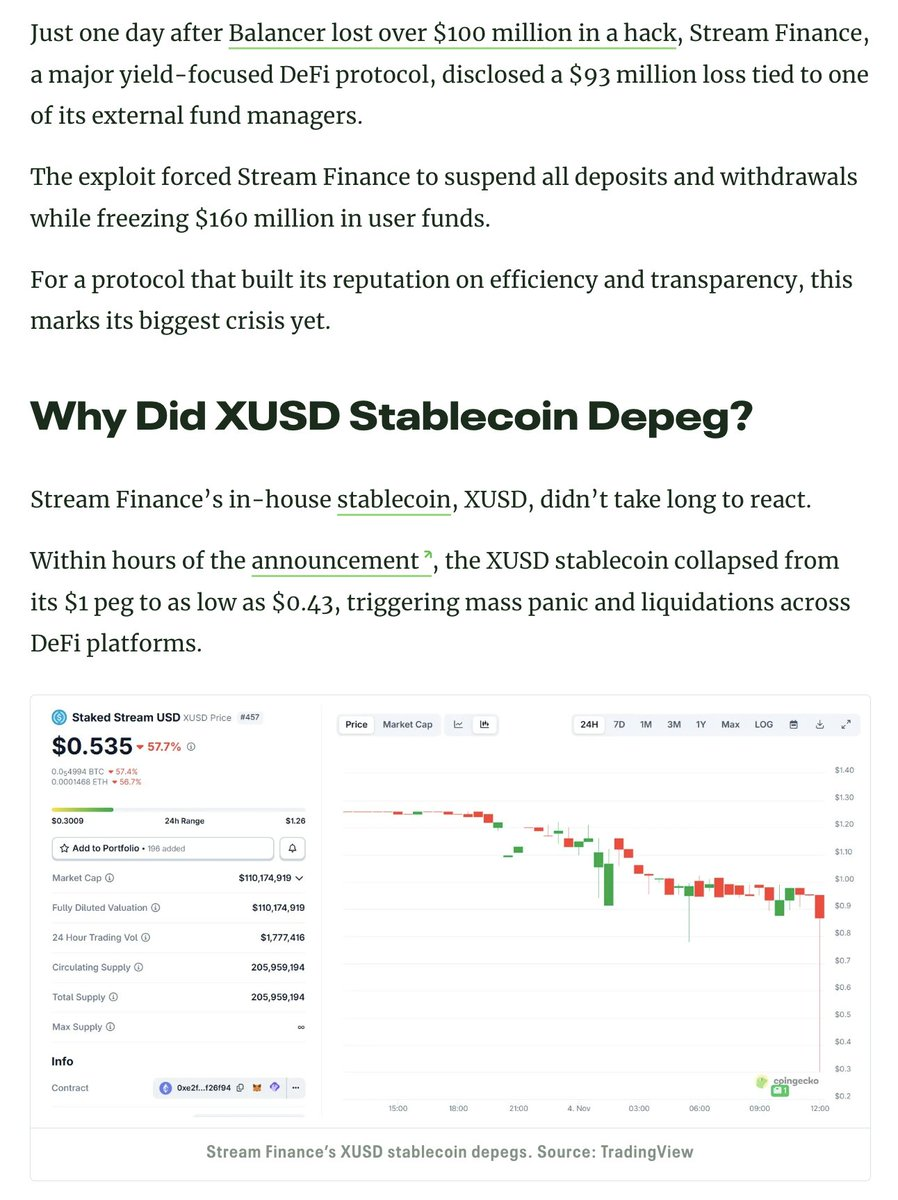

Editor's Note: Twenty-four days later, the xUSD de-pegging crisis has once again exposed Stream Finance's massive losses to the public. On November 4th, Stream Finance officially acknowledged that external fund managers disclosed losses of approximately $93 million in their funds, and that they had hired lawyers from Perkins Coie LLP to conduct a full investigation. As of this writing, the xUSD price has de-pegged to around $0.14, a drop of approximately 87%. More worryingly, the market has little hope for a return to peg, and this may just be one link in a domino effect crisis triggered by the "October 11th crash." To uncover the truth behind the xUSD de-pegging and Stream Finance's massive losses, Odaily has compiled the following investigative report from Trading Strategy for readers' reference.

The xUSD de-anchoring collapse: When a DeFi Curator gets shot in the forehead

Based on available information, xUSD issued by Stream Finance is a "tokenized hedge fund" disguised as a DeFi stablecoin, with its official claim being that it operates a delta-neutral strategy for investment. Now, Stream is embroiled in a public relations crisis.

Over the past five years, numerous crypto projects have followed this script: attempting to leverage revenue generated from delta-neutral investments to fuel their token growth. Some successful examples include MakerDAO, Frax, Ohm, Aave, and Ethena.

Unlike many DeFi competitors who actually execute this strategy, Stream Finance lacks transparency regarding its strategies and positions. Of its claimed "up to $500 million TVL," only $150 million in assets are visible on-chain (e.g., verifiable via @DeBankDeFi ). Now, the truth has been revealed: Stream invested a portion of the funds in off-chain trading strategies run by independent traders, some of whom suffered margin calls, leaving behind a nominal loss of $100 million.

Initially, @CCNDotComNews used the "xUSD de-anchoring incident" as a starting point to report on the event in detail .

It should be emphasized that the Balancer hack incident is merely an introduction and is unrelated to this matter.

According to rumors (which we cannot confirm as Stream has not officially disclosed), off-chain trading strategies involving "selling volatility" are also implicated. In quantitative finance, "selling volatility" (also known as "short volatility") refers to a trading strategy that profits when market volatility decreases, remains stable, or when actual volatility is lower than the implied volatility priced in the financial instrument. If the price of the underlying asset does not change significantly (i.e., low volatility), the option may expire worthless, allowing the seller to retain the premium as profit. However, this approach carries significant risk, as a sudden surge in volatility can lead to substantial losses—this strategy is often described as "picking up pennies in front of a steamroller." More information on selling volatility can be found here .

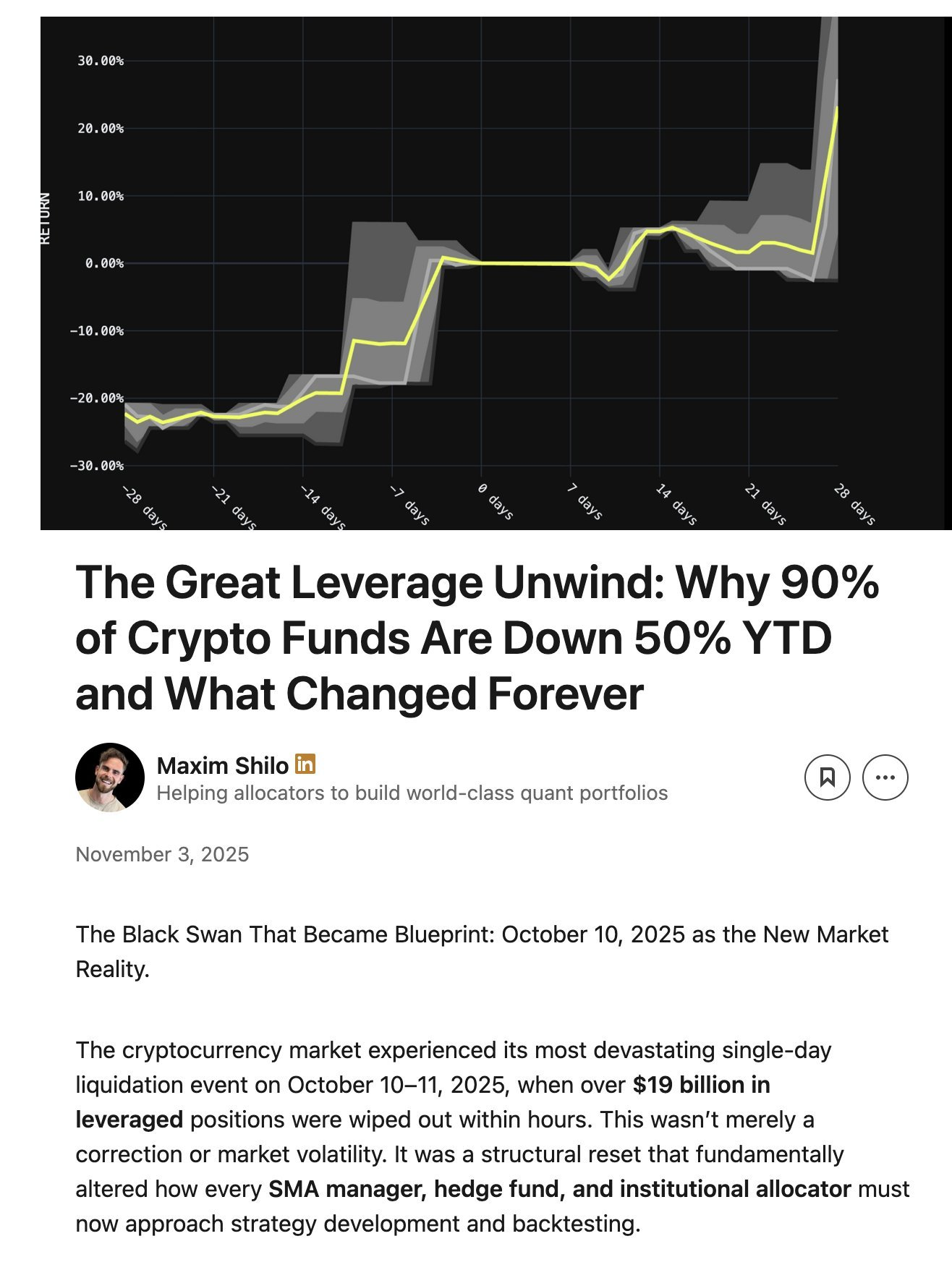

The cryptocurrency market experienced a similar surge in volatility during last month's "Red Friday" (Odaily Planet Daily note: the massive crash on October 11th Beijing time). Over time, fueled by Trump's aggressive policies this year, the cryptocurrency market accumulated significant systemic leverage risk. When Trump announced new tariffs on Friday afternoon, October 10th (early morning of October 11th Beijing time), all capital markets panicked, and this panic quickly spread to the cryptocurrency market. In such extreme panic, it's understandable that those who panicked first would sell off their leveraged assets; and it was this sell-off that led to the subsequent secondary liquidations.

Due to the long-term accumulation of leverage risk, systemic leverage rose to a high level, and the perpetual futures market lacked sufficient depth to smoothly close out all leveraged positions. In this situation, the Automated Liquidation (ADL) system came into play, leading to amplified losses for market participants with some profit margins. This further squeezed the already frenzied crypto market. For an introduction to Automated Liquidation (ADL), please see here .

The market volatility caused by this event is a once-in-a-decade occurrence in the cryptocurrency market. While not widely known, a similar crash occurred in the early cryptocurrency market back in 2016. Unfortunately, we lack complete data from that era, so most quantitative traders' strategies are based on recent "volatility smoothing" data. In other words, because we haven't experienced such a volatility surge in recent years, even leveraged positions of only 2x were liquidated in this crash.

Maxim Shilo previously detailed in an article what this event means for quantitative traders and what permanent changes cryptocurrency trading might undergo after "Red Friday."

Now, we are seeing the first bodies to surface from the “Red Friday” incident, and Stream is one of them.

A requirement for Delta-neutral funds is that you cannot lose money. If you lose money, by definition, you are not a Delta-neutral strategy. Stream promises to remain delta-neutral, but behind the allocation of funds, they invest in proprietary, opaque off-chain trading strategies. Delta-neutral strategies are not always black and white, and it's easy to judge in hindsight. Many experts might argue that these off-chain trading strategies are too risky to be considered true Delta-neutral because they could backfire, and reality has proven this point.

When Stream loses its principal in these bad trades, the end result is insolvency.

Undoubtedly, DeFi is not without risk, and partial losses are permissible. You can still recover your assets to 100%, and if you can achieve a 10% annualized return, a one-time 15% drawdown is not devastating.

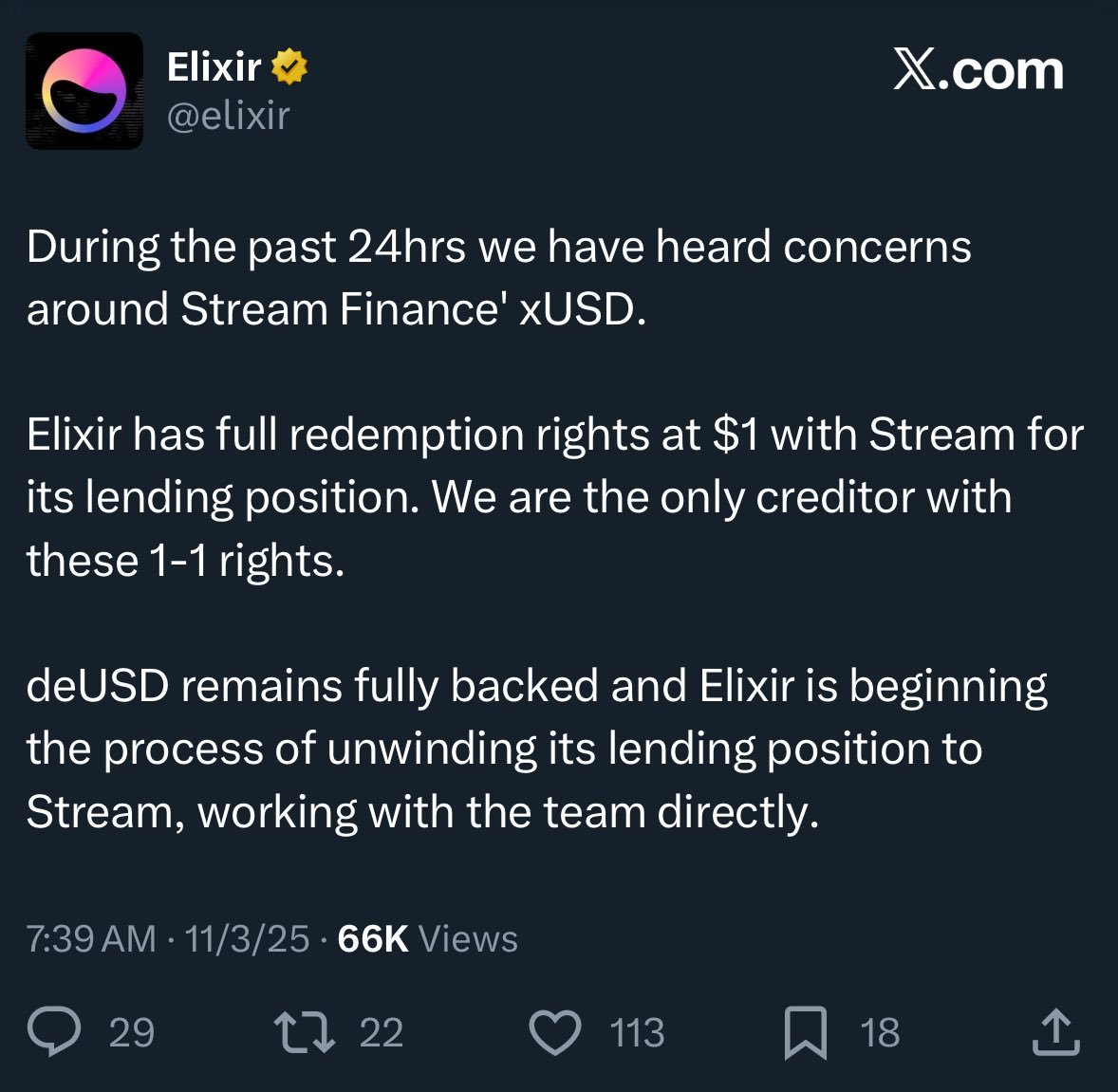

However, faced with this loss situation, Stream also made full use of its funds by implementing a "recursive loop" lending strategy using another stablecoin, Elixir. An introduction to recursive loops can be found here . This resulted in increased leverage. (For details on how Stream leveraged and how much leveraged its positions were, please refer to this article ).

To make matters worse, Elixir claims that the "cooperative assets" are generated based on an off-chain protocol between the two parties so that their principal can be recovered in the event of Stream's bankruptcy. This means that Elixir will receive more compensation, while other DeFi investors in Stream will receive less (or none at all).

Due to a lack of transparency, recursive loops, and proprietary strategies, we are not actually aware of the losses suffered by Stream platform users. The Stream xUSD stablecoin is currently trading at $0.60 (around 4 AM on November 5th).

Because Stream did not disclose this information to these DeFi users, many users are now very angry with Stream and Elixir: they not only have to bear the loss of their assets, but also have an uncertain amount of the remaining funds confiscated to ensure that wealthy Americans from Wall Street hold onto their profits.

This incident also impacted other lending protocols and their Curators (DeFi curators). As Rob from @infiniFi stated, " Those who think they are 'lending with collateral' on Euler are actually 'indirectly participating in uncollateralized lending.' " (Odaily Planet Daily note: This means you think your funds are being lent to a collateralized lender, but in reality, your money is being borrowed by an uncollateralized lender.)

Furthermore, due to Stream's lack of transparency regarding its positions and profit/loss, or the absence of on-chain data, these events have led users to suspect that Stream's management team fraudulently misappropriated user investment profits. Stream xUSD stakers rely on "oracles" reported by Stream's official channels to obtain "paper" profits, and third parties cannot verify the accuracy or fairness of any profit/loss calculations.

How can this problem be solved?

Events like Stream could actually be avoided, especially in emerging industries like DeFi.

The rule of "high risk, high reward" always applies. However, to profit from this rule, you must first understand the risks: not all risks are created equal, and some risks may be unnecessary. Several reputable liquidity mining, lending, and stablecoin tokenization hedge fund protocols offer transparent information on their risks, strategies, and positions.

For example, @StaniKulechov, the founder of @aave, recently published an article discussing DeFi planners and when high-risk events might occur. He also mentioned recent DeFi risk events.

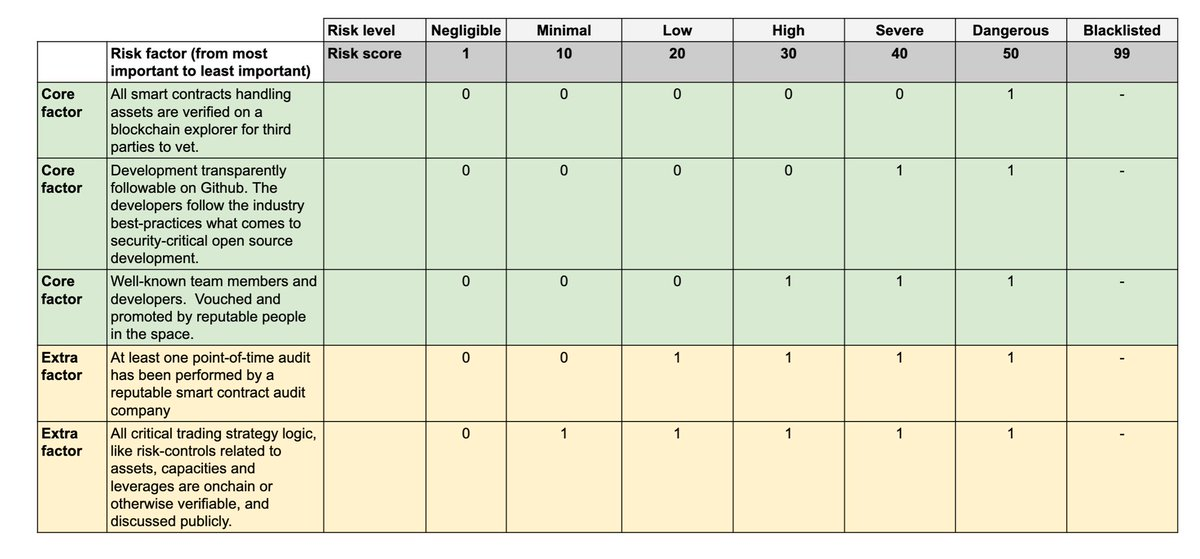

To make the distinction between "good vaults" and "bad vaults" clearer, we have started publishing vault technology risk assessment scores in our DeFi Vault Report, which can be found here .

Technical risk, viewed from several different dimensions, refers to the possibility of losing funds invested in DeFi vaults due to poor technical execution. The vault technical risk framework provides a simple analytical tool primarily used to categorize DeFi vaults into high-risk and low-risk categories. It's important to emphasize that technical risk scoring does not eliminate market risks such as bad trades and risk contagion; its value lies in allowing third parties to assess these risks (to decide whether to invest).

As DeFi users gain access to more comprehensive and complete information, fund allocation will shift towards projects that comply with rules and operate transparently, and future collapses like Stream will not cause such severe losses and impacts again.

Another good suggestion for solving the vault management problem is to increase the funds that DeFi curators invest in the vault. Many traditional financial copy trading services typically display the amount of capital (such as USD value and percentage) that traders invest in their trading strategies.

Finally, a serious reminder and warning: Vaults holding Stream xUSD leverage are currently offering huge APYs above 50%; however, the vaults are operating at 100% capacity, meaning that funds are locked in lending positions and cannot be closed because the protocol has either suspended operations or the lending positions are underwater with insufficient funds for withdrawal. If you deposit funds into these vaults, you will most likely suffer financial losses; please do not risk it.