The Federal Reserve cuts interest rates, and the stablecoin business is not so good

- 核心观点:美联储降息终结稳定币利差盈利模式。

- 关键要素:

- Tether年收入或降9.53亿美元。

- Circle可能从盈利滑向亏损。

- 派息稳定币兴起压缩利润空间。

- 市场影响:行业加速转型,洗牌在即。

- 时效性标注:中期影响。

Original author: Sleepy.txt

Original editor: Kaori

Original source: Beating

On September 18, 2025, the Federal Reserve announced a 25 basis point cut in the federal funds rate to 4.00%-4.25%. This was a signal of easing for most industries, meaning lower financing costs and more abundant liquidity.

But for the issuers of stablecoins, this cut means that the countdown to the model of making easy money on interest rate differentials has officially begun.

The turning point of the high-interest rate era has arrived. Since March 2022, the Federal Reserve has raised interest rates 11 times in a row, pushing them to a high of 5.25% to 5.50%. This period of high interest rates has opened an unprecedented profit window for stablecoin issuers.

Today, with inflation falling, growth sluggish, and monetary policy shifting, the golden age of the stablecoin industry has come to an end.

Countdown to the end of the interest rate differential model

The core profit logic of stablecoins is extremely simple and direct. Users exchange US dollars for tokens of equivalent value, and the issuer invests the money in short-term US Treasury bonds or money market funds, making money from the interest rate differential.

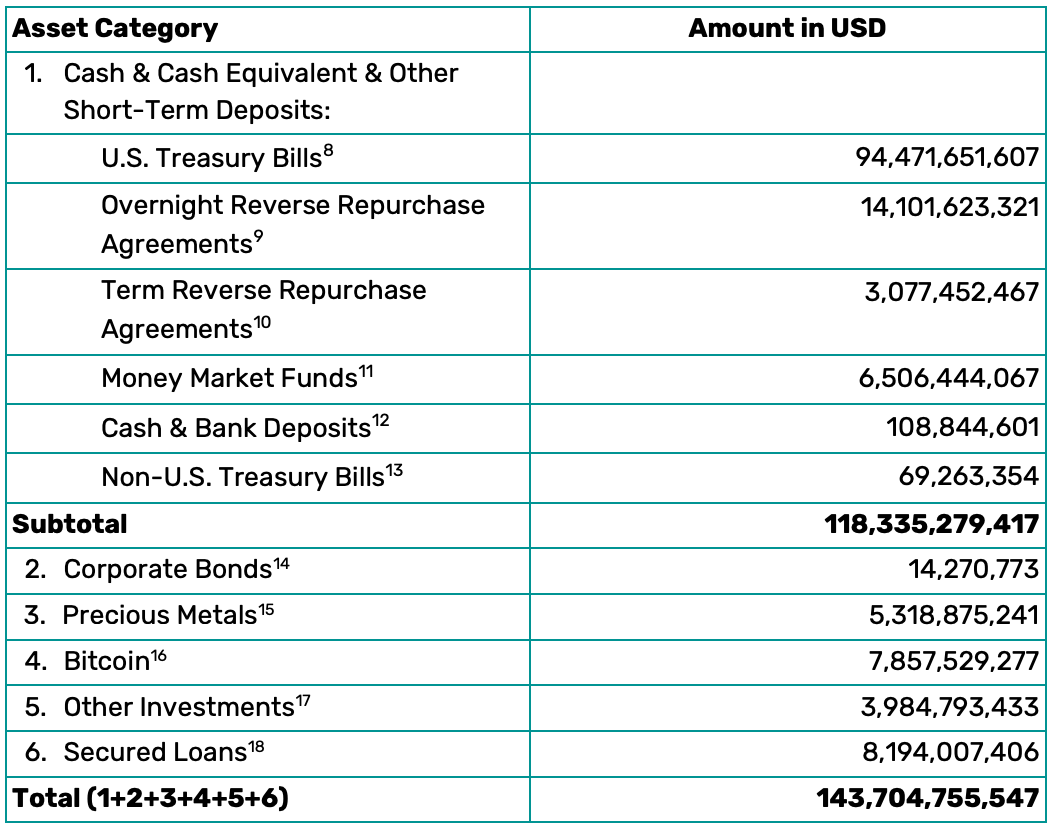

During high-interest rate cycles, this model delivers astonishing returns. Tether is the most striking example. Its reserve verification report for the fourth quarter of 2024 shows that the company's annual profit reached $13 billion, of which approximately $7 billion came from interest on Treasury bonds and repurchase agreements, accounting for more than half of the total profit. Its holdings of U.S. Treasury bonds totaled $90.87 billion, representing 82.5% of its total reserves.

Details of the reserves supporting the fiat-denominated Tether tokens in circulation | Source: Tether official website forensic opinion and comprehensive reserve report

The same is true for Circle, another major stablecoin issuer. While Circle doesn't disclose its full profit breakdown, its reserve disclosures indicate that it allocates approximately a quarter of its funds to short-term US Treasury bonds, with the remainder primarily held in money market funds managed by BlackRock. This, too, is a stable cash machine when interest rates remain high.

However, when interest rates are cut, this profit margin will be the first to be cut.

Let's do some simple math. Take Tether, for example. According to its Q2 2025 attestation report, the company's exposure to US Treasury bonds reached $127 billion. Every 25 basis point drop in interest rates would reduce its annualized interest income by approximately $318 million.

If, as generally expected by the market, the Federal Reserve cuts interest rates 2-3 more times in the future, for a total of 75 basis points, Tether's annual revenue will be reduced by approximately US$953 million.

Circle is in a similarly delicate position. Its Q2 2025 financial report shows an average USDC circulation of $61 billion and reserve income of $634 million. Approximately 80% of this amount is allocated to short-term US Treasury bonds. A 25 basis point interest rate cut would mean a reduction in annual revenue of approximately $122 million; a cumulative 75 basis point rate cut would see revenue decline by $366 million.

The problem is that Circle only generated $126 million in adjusted EBITDA for the quarter, and if its interest margins shrink, it could easily slide from profitability to losses.

More importantly, there is no symmetrical relationship between the loss of interest rate spread and scale expansion.

In theory, interest rate cuts will increase market risk appetite, boost trading activity, and potentially expand the circulation of stablecoins. However, this growth is far from enough to fill the interest rate gap.

For example, at Circle's current fund size, a 25 basis point interest rate cut would reduce revenue by approximately $122 million. To offset this loss, assets under management would have to increase by 6%, equivalent to an additional $3.7 billion. If the cumulative rate cuts reached 75 basis points, Circle would need to expand by 21%, or $12.6 billion, to maintain its current return.

This asymmetry reveals the fundamental fragility of the interest rate differential model. Once the high interest rate environment subsides, the dividend cycle of this track will come to an end.

Greater pressure comes from the rise of dividend-paying stablecoins. More and more institutions are launching products that can distribute dividends to users, cutting off part of the interest rate spread that originally belonged to the issuer.

This trend directly squeezes the profit margins of traditional stablecoins and forces issuers to speed up their search for new business models.

From a quasi-money fund to a global financial services provider

As the interest rate spread model reaches its end, stablecoin issuers must undergo a fundamental transformation, transitioning from quasi-money market funds to global financial service providers. The core idea is to shift the revenue focus from a single interest rate spread to a broader, more sustainable financial service offering.

Several giants have already begun taking action, each with its own keen sense of smell, and each has explored different paths. These attempts reveal three distinct transformation directions.

Circle: The Didi of the Financial World

Circle is attempting a radical transformation, and its goal can be understood with an intuitive analogy: Didi.

Didi does not own cars, but it can match drivers and passengers; the Circle Payment Network (CPN) built by Circle also does not directly handle funds, but hopes to weave together banks and financial institutions around the world.

Traditional cross-border payments are like the ride-hailing market without Didi. You have to hail a car on the street, unsure when the driver will show up, how much it will cost, or what problems you might encounter along the way. CPN aims to provide a real-time dispatching system for global capital flows.

Circle co-founder Jeremy Allaire said in an interview that they are "building one of the largest financial networks in history." Although this statement sounds a bit exaggerated, it also reflects Circle's ambition.

The CPN's design also has its ingenuity. Since it doesn't directly hold funds, it doesn't need to apply for a money transmission license in every country. As a technology service provider, it can invest more resources in product innovation rather than being bogged down by compliance costs. Circle's asset-light approach and focus on its network have enabled rapid expansion.

However, the core of the financial industry is trust. To win the approval of traditional institutions, Circle invited four major global banks—Santander, Deutsche Bank, Societe Generale, and Standard Chartered—to serve as advisors. For CPN, these names are a testament to its credibility.

From a profit model perspective, Circle is shifting from profit margins to a revenue-generating model. Circle collects network fees for every transaction that passes through the CPN. This aligns revenue with transaction volume, rather than interest rates. Even in a zero-interest rate environment, as long as there's money flowing, there's profit.

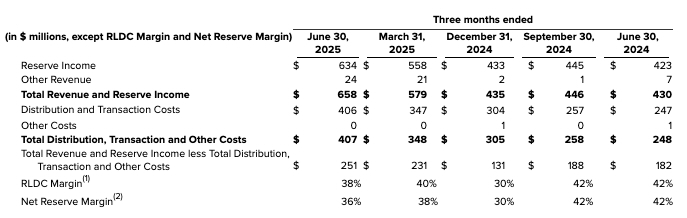

However, this transformation story is still in its very early stages. CPN only officially launched in May of this year and currently has only four active payment channels. Despite over 100 financial institutions lining up for integration, revenue has so far been limited. According to Circle's second-quarter 2025 financial report, the company's total revenue was $658 million, of which $634 million came from reserve interest. Other revenue (including CPN) accounted for only $24 million, or approximately 3.6%.

Source: Circle 2025 Q2 Financial Report

In other words, while Circle's "toll" strategy is clear, it will take time for its valuation and stock price to truly support its growth. Even optimistically, it could take another three to five years for CPN to begin contributing revenue at scale. Until then, Circle remains heavily reliant on interest rate differentials, and the impact of interest rate cuts remains an unavoidable challenge.

In the longer term, Circle is attempting to build a complete digital financial infrastructure. In addition to the CPN, it is also developing API services for programmatic payments, digital identity, and foreign exchange settlement. According to market analysis, if Circle can attract 10,000 medium and large enterprise customers through these API services, each contributing $50,000 to $150,000 annually, this could generate $500 million to $1.5 billion in annual revenue for Circle.

Currently, over 30 fintech companies worldwide have joined the network, ranging from Coins.ph in the Philippines to Flutterwave in Africa, and from OpenPayd in Europe to dLocal in Latin America. With each additional node, the value of the entire network grows exponentially.

This is the charm of the platform economy. The initial investment is huge, but once a network effect is formed, a moat can be built.

Circle's transformation strategy reflects a profound business insight: in the digital age, the most scarce resource is not capital itself, but connections.

Tether: The Berkshire Hathaway of the Crypto World

If Buffett built his investment empire with insurance company float, Tether is using the cash flow generated by stablecoins to lay out a cross-industry investment portfolio and has begun its "de-spreading" layout early on.

Tether’s strategy can be summed up in one word – reverse thinking.

Actively searching for new profit engines puts Tether in a different position before the interest rate cut cycle arrives.

Tether's investments span a wide range of sectors, encompassing nearly every imaginable sector. Energy is a key sector, and the company is betting heavily on Bitcoin mining globally, aiming to create a closed-loop system. Bitcoin production requires mining, while transactions require USDT. The issuance of USDT generates new cash flow for Tether.

Gold is another core configuration of Tether. The company holds $8.7 billion worth of physical gold in its reserves and has invested more than $200 million in Canadian gold mining companies. Tether CEO Paolo Ardoino even called gold "natural Bitcoin."

In traditional financial theory, the price of the US dollar and gold tends to rise and fall in symbiotic relationships. By holding both types of assets, Tether effectively creates a natural hedge. Regardless of the strength or weakness of the US dollar, at least some of its assets maintain their value.

What surprised the outside world most was Tether's involvement in commodity trade financing. This kind of business, which sounds quite "old-fashioned", has brought considerable returns to the company.

Tether leverages its abundant cash flow to provide short-term loans for the transportation of raw materials. According to people familiar with the matter, this business has reached billions of dollars. Because traditional banks are generally cautious or even shy away from this market, Tether fills the gap and earns a stable interest rate spread.

From the perspective of portfolio theory, Tether's strategy coincides with the modern portfolio theory proposed by Harry Markowitz - don't put all your eggs in one basket.

By diversifying its investments across different assets and industries, such as energy, gold, and commodity financing, Tether has significantly reduced its reliance on a single business. As a result, in the second quarter of 2025, the company achieved a net profit of $4.9 billion, a significant portion of which came from contributions from these diversified investments.

However, this strategy also makes Tether increasingly complex, making it difficult for the outside world to fully understand its operating logic.

Unlike Circle's emphasis on transparent operations, Tether's disclosures are often limited, which deepens market concerns about the security of its assets.

The deeper issue is that the core value of stablecoins lies in stability and transparency. When issuers are overly diversified, will systemic risks be introduced? If a major loss occurs in an investment, will the stability of USDT be affected? These questions remain unresolved.

Even so, Tether's strategy still demonstrates a realistic judgment. In an industry full of uncertainty, early planning and risk diversification are themselves a kind of survival wisdom.

Paxos: The Foxconn of the Stablecoin World

If Circle aspires to be the Didi of the financial world, and Tether is building the Berkshire Hathaway of the crypto world, then Paxos is more like the Foxconn of the stablecoin world. Foxconn doesn't sell its own brand of phones, but instead manufactures for giants like Apple and Huawei. Similarly, Paxos doesn't prioritize its own brand, but instead provides a comprehensive suite of stablecoin issuance services to financial institutions.

This positioning actually demonstrates resilience during a period of interest rate cuts. While Circle and Tether worry about shrinking interest rate spreads, Paxos has long been accustomed to sharing profits with its customers. This seemingly disadvantageous arrangement actually provides a buffer for the company.

Paxos' business philosophy can be summarized in one sentence: let professionals do professional things.

PayPal has 430 million users but lacks blockchain technology expertise; Standard Chartered Bank boasts a global network but lacks stablecoin experience; Kraken understands cryptocurrencies but needs a compliant stablecoin product. Paxos aims to become the technical brains behind these giants.

In the traditional model, stablecoin issuers bear all technical, market, and regulatory risks and costs. Paxos's OEM model leaves market and brand risks to its clients, while keeping technical and compliance risks within its own hands.

PayPal's PYUSD is a prime example. Building their own team could have taken years, invested hundreds of millions of dollars, and faced complex approval processes. However, with Paxos, PayPal was able to launch the product in just months, freeing up its resources to focus on user education and expanding its application scenarios.

What’s even more interesting is that Paxos is building a “stablecoin federation”.

In November 2024, Paxos launched the Global Dollar Network, whose core product is the USDG stablecoin. This network is backed by many well-known institutions, including Kraken, Robinhood, and Galaxy Digital.

Standard Chartered Bank will become a reserve management partner, responsible for cash and custody. The idea of this "federation" is that stablecoins of different brands share the same infrastructure and achieve interoperability, just like different brands of Android phones can run the same application.

Behind this approach lies the evolution of our business model. Paxos doesn't pursue scale alone, but rather focuses on efficiency and ecosystem collaboration. Its core competitiveness lies not in how many users it has, but in how much value it can create for its partners.

Its revenue structure also reflects this philosophy: technology licensing fees, compliance service fees, operating management fees, and reserve income share form a diversified source of income. This allows it to maintain a stable cash flow even in an interest rate cut environment.

Looking deeper, Paxos attempts to redefine "infrastructure."

Traditional financial infrastructure is a pipeline, solely responsible for the flow of funds; the platform built by Paxos simultaneously creates and distributes value. This shift from pipeline to platform may become the prototype of the future stablecoin industry.

Of course, this model has its weaknesses. As a behind-the-scenes player, Paxos struggles to build direct user recognition and brand recognition. However, in an era that emphasizes division of labor, this invisibility can be an advantage: it can provide services to any potential customer without being perceived as a competitor.

The future of stablecoin businesses

The attempts of several stablecoin giants have outlined the possible direction of the industry. Stablecoins are shifting from a single value storage tool to a broader financial infrastructure.

The first direction is the payment network.

Stablecoins are gradually becoming a new generation of clearing channels, rivaling traditional networks like SWIFT and Visa. Compared to traditional systems, stablecoin-based payment networks can achieve 24/7 global fund settlement, becoming the underlying infrastructure for cross-border payments.

Traditional cross-border payments require layers of intermediaries, each adding time and cost. Stablecoin payment networks, on the other hand, allow suppliers and demanders of funds to connect directly. Circle's CPN epitomizes this trend, aiming to create a global, real-time settlement system that allows financial institutions to bypass the correspondent banking model.

Building on this foundation, stablecoin companies are expanding into a wider range of financial services. They are beginning to resemble banking services, offering lending, custody, and clearing services, using stablecoins as a gateway to traditional finance. Leveraging smart contracts, these services can reduce operating costs and enhance transparency and automation.

More importantly, stablecoins are entering corporate treasury and trade scenarios, providing multinational corporations with treasury management, supply chain finance, and international settlement solutions. Stablecoins are thus evolving from a transaction medium for retail users to an enterprise-level payment and financing tool.

Asset management is another direction.

In the past, reserves were almost entirely invested in U.S. Treasuries, offering security but limited returns. In an environment of falling interest rates, issuers are beginning to explore more diversified allocations, hoping to strike a balance between transparency and returns. Tether's investments in gold and commodities exemplify this exploration. By diversifying their reserve portfolios, issuers are attempting to ensure stability while making their reserves themselves a new profit engine.

This means that stablecoin companies are no longer content with playing a marginal role in the financial system. Their goal is to become the core infrastructure of a new financial system. However, whether this ambition can be realized depends on finding a sound balance between technological innovation, regulatory compliance, and business models.

A reshuffle is imminent, and only the fittest will survive

The implementation of interest rate cuts has fully exposed the fragility of the interest rate differential model. Profit models relying on interest rate differentials are becoming ineffective, and the stablecoin industry is facing a reshuffle. Whether a company can survive depends on the speed of its business model upgrades and the thoroughness of its transformation.

For publishers, transformation often means making unpleasant decisions in the short term, but it is crucial for their long-term survival. This requires both courage and the ability to discern future trends.

The focus of competition may shift from issuance size to service capabilities. Whoever can truly transform a stablecoin into a financial services platform, rather than simply issuing tokens, will be more likely to gain a firm foothold in the new landscape.

From this perspective, the Fed's interest rate cut isn't just a monetary policy adjustment; it also serves as a stress test for the stablecoin industry. Those companies that can weather this crisis will occupy a more prominent position in the future financial landscape; those that still rely on a single interest rate differential model may find themselves facing difficulties.