6月CPI落地:雷沒爆,但倒車還沒停

- 核心觀點:5月CPI拆除了「核心通膨失控、6月立即升息」的尾部風險,但名目CPI處於高檔以及「更久更高」的利率預期仍壓抑市場,目前處於分批布局窗口開啟期,而非全倉追反彈的時機。

- 關鍵要素:

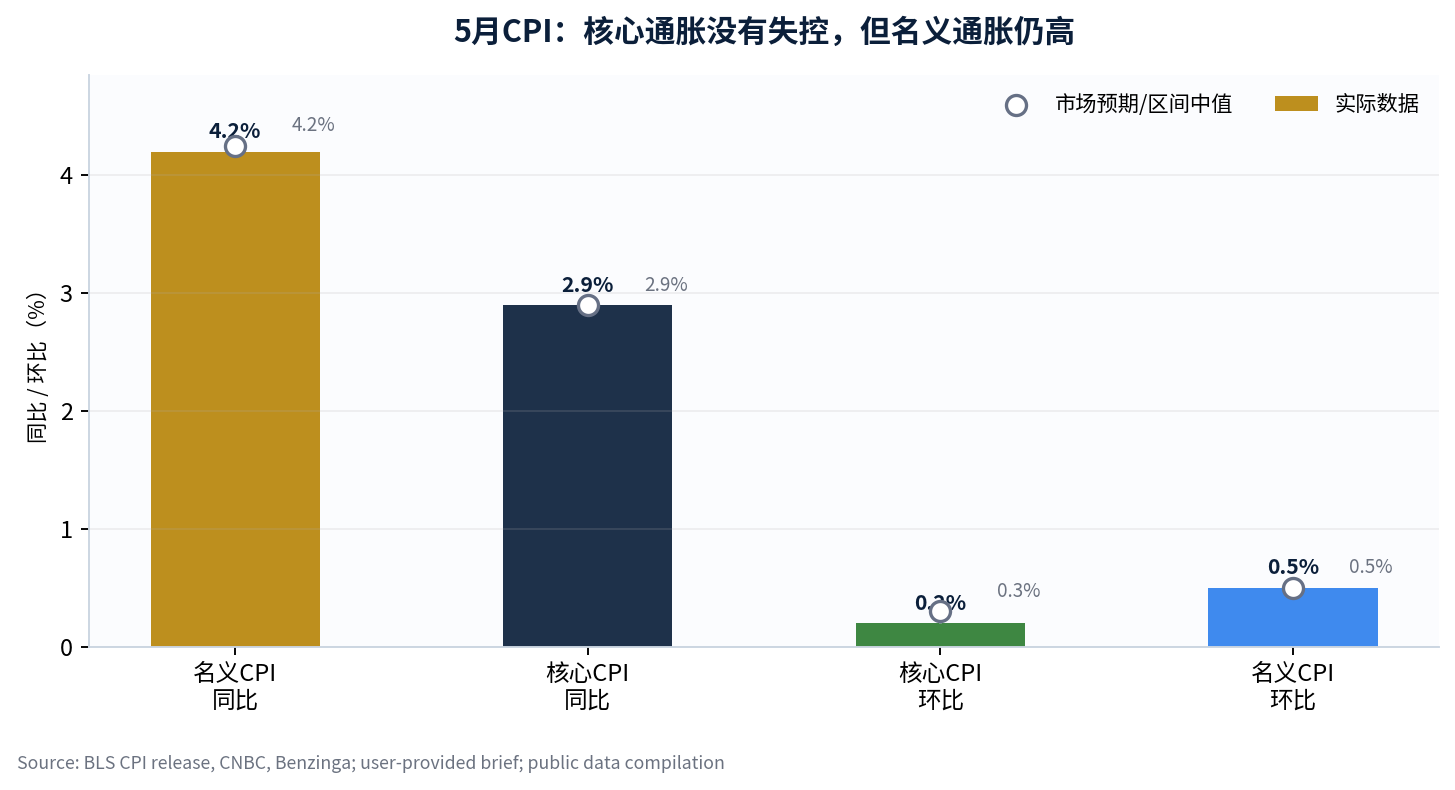

- 美國5月核心CPI月增率僅0.2%,低於預期,排除了「通膨二次失控」和6月立即升息的極端情境。

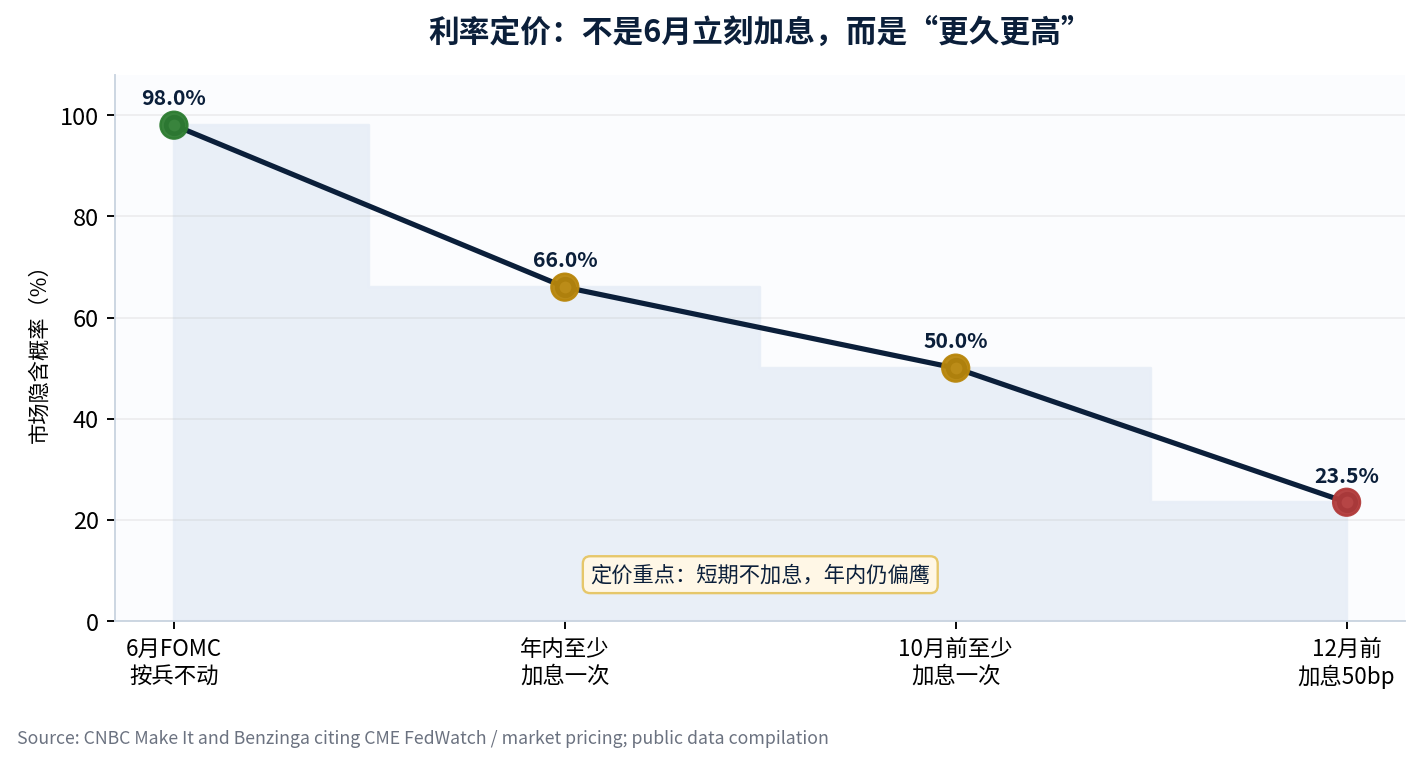

- 名目CPI年增率4.2%創三年新高,能源價格與地緣衝突使債市維持鷹派立場,年內再升息一次的機率約為66%,形成「短期不升、長期更高」的定價分裂。

- 半導體板塊去槓桿程度較深,SMH、MU自高點回撤約10.5%和17.4%,而VIX收在22.22並未突破恐慌閾值,顯示非系統性崩盤,但擁擠的倉位尚未完全出清。

- SOXS資金流入以及SMH賣權成交量放大,顯示機構藉由CPI利好的反彈來鎖定下行風險,而非全面買進。

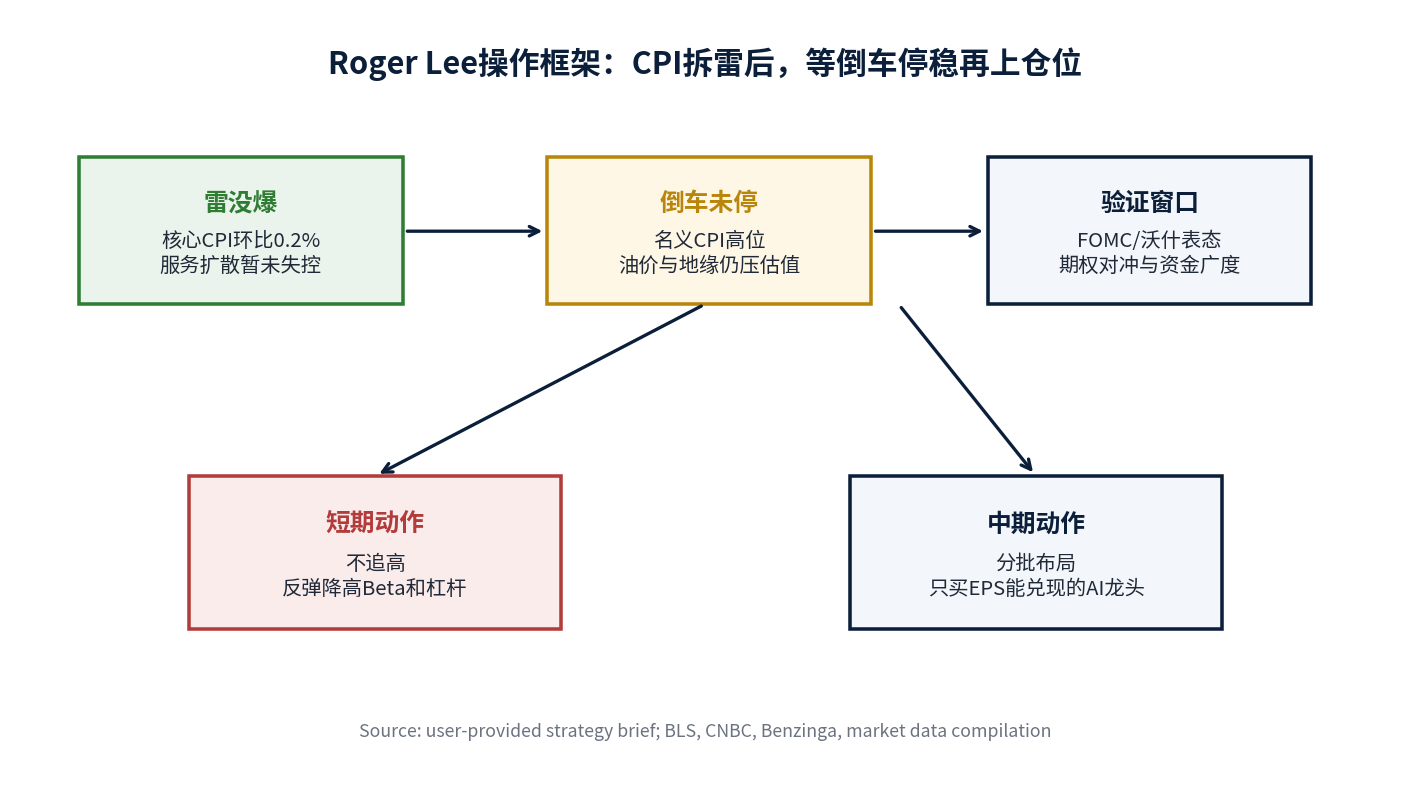

- 策略建議在FOMC會議前降低高Beta與純敘事型品種的倉位,會議後僅分批布局有EPS證據的AI龍頭股,尤其是直接受惠於雲端資本支出的環節。

Roger Lee | BIT US Stock Special Analyst

With 21 years of experience in investment banking, asset management, and financial institutions, he has long focused on AI industry chain, US stock macro liquidity, and options strategy research.

Investment Summary

My conclusion is straightforward: The May CPI dismantled the "core inflation is out of control, immediate rate hike in June" bomb, but it didn't completely stop the US stock market's reversal; now is not the time to go all-in on the rebound, but rather to patiently wait for the FOMC decision with phased deployment and strengthening positions while cutting weak ones.

This sentence is the core of how I view last night's market reaction. The US May headline CPI was 4.2% year-over-year, core CPI was 2.9% year-over-year, and core CPI month-over-month was only 0.2%. The data itself did not confirm a "secondary inflation loss of control"; however, the headline CPI still hit a three-year high, and energy items and geopolitical conflicts continued to push the bond market in a hawkish direction. Therefore, the market did not directly translate the positive CPI data into a stock market surge. [1] [2]

I believe the current market is not about "blindly buying after bad news is fully priced in," but rather "extreme tail risk has decreased, but crowded trades are still actively reducing risk." SMH has retraced approximately 10.5% from its recent high, MU approximately 17.4%, MTUM approximately 7.5%, and VIX closed at 22.22, not yet breaking above the panic threshold of 25. This indicates the market is not experiencing a systemic collapse, but rather semiconductors and high-beta sectors are still undergoing deleveraging. [5]

1. Factual Judgment: CPI Didn't Explode, So Why Didn't the Market Rise?

The key to the US May CPI lies not in the headline YoY figure itself, but in whether core inflation is broadly spreading to the services sector. The user's original text mentioned headline CPI YoY at 4.2%, core CPI YoY at 2.9%, core CPI MoM at 0.2%, and headline CPI MoM at 0.5%. Public reports and official data口径 show that energy prices were one of the core drivers of headline inflation, and the core CPI MoM being lower than the market expectation of 0.3% means the worst-case scenario of "the oil price shock is fully spreading to the services sector" has temporarily been avoided. [1] [3]

The market didn't surge because stocks and bonds were looking at different things. Stocks saw that core inflation was not out of control, and the AI earnings narrative had not been falsified by macroeconomic data in the short term; bonds saw that headline inflation remains high, oil prices and geopolitical conflicts are uncertain, and the probability of another rate hike within the year has risen again. CNBC and Benzinga's coverage of the CME FedWatch and market pricing shows that the probability of the FOMC holding steady in June is close to 98%, but the probability of at least one rate hike within the year is about 66%. This is precisely the pricing split of "no hike in the short term, but higher for longer." [2] [4]

2. Bond-Stock Split: The Real Pressure Comes from "Higher for Longer"

The implication of this CPI report is not "an immediate rate hike," but rather "the imagination of rate cuts continues to be suppressed." If the core CPI MoM had been significantly higher than expected, the market would have directly priced in a rate hike in June or July. Now that this extreme scenario has been ruled out, the high headline CPI, oil price shock, and resilient employment data still prevent the bond market from prematurely betting on easing. The damage to tech stocks is not an immediate falsification at the fundamental level, but a discount rate constraint on the valuation side.

My judgment is that the bond-stock split will not end in a single day. Stocks can rebound because core CPI came in lower than expected, but if the 10-year Treasury yield continues to rise, or if Fed communication shifts "another rate hike" from a risk scenario to a baseline scenario, high-valuation tech stocks will continue to face valuation compression. Therefore, before the FOMC, the positive CPI should not be interpreted as "an immediate signal to go all-in on chasing highs."

3. Semiconductor Hedging: Surging Hedging Demand Indicates the Reversal Hasn't Stopped

The user's original text mentioned that SOXS fund inflows and the surge in SMH put option volumes are the most important micro-signals in the post-CPI market. My understanding is that institutions are not selling off all AI assets, but are using the rebound to lock in downside risk. In other words, they acknowledge that the CPI has defused one bomb, but they do not believe the crowded semiconductor positions have been fully cleaned out.

Based on captured market data, as of June 10, SMH had retraced approximately 10.5% from its recent high, MU approximately 17.4%, MTUM approximately 7.5%, QQQ approximately 7.0%, SPY approximately 4.5%, and VIX closed at 22.22. [5] This set of data illustrates two things. First, the deleveraging within the semiconductor sector is significantly deeper than the broader market; second, VIX has not broken through 25, indicating that the market has not yet entered a phase of indiscriminate panic selling. For me, this is not a "total wreck," but it is also not yet a "safely parked car."

4. Operational Framework: Don't Chase Short-Term Highs, Buy EPS Phased in Medium-Term

I divide the next two weeks into two phases. Phase one is before the FOMC meeting; the core tasks are capital preservation and noise reduction. Since market breadth hasn't significantly improved and VIX hasn't hit panic extremes, I won't directly add leverage just because CPI was slightly better than expected. I will reduce exposure to pure narrative, high-beta, high-leverage semiconductor and concept tech stocks on the bounce, especially those lacking orders, gross margin support, and relying solely on valuation expansion.

Phase two is after the FOMC and Walsh's comments; the core task is phased deployment. The user's original text mentioned that if investors can tolerate a 3%-4% pullback in the market, the current market has gradually entered a range for phased deployment. I agree with this judgment, but the premise is to only buy AI leaders with EPS evidence, not all tech stocks that have fallen. The previous report already emphasized that the real terminator for the tech rally is industry involution and EPS falsification, not the Fed raising rates by another 25bp; this framework hasn't changed after this CPI release. [6]

5. My Investment Interpretation: The Bomb is Defused, But Don't Deploy Cash Too Quickly

My operational strategy is very clear: CPI gave the market a breather, but I won't misinterpret this single breath as a sign that the trend has re-accelerated. For core AI assets I already hold, I won't easily exit due to post-CPI volatility; but for new positions, I will deploy in phases, with limit orders, and wait for confirmation. Priority for new positions will go to AI infrastructure stocks with high order visibility, stable gross margins, and good cash flow, especially those directly benefiting from cloud capital expenditure.

For high-beta and pure narrative names, I will continue to reduce positions on bounces. Quantum, aerospace, and small-cap chip stocks lacking a clear path to profitability will find it difficult to continue expanding valuations based on stories alone in a "higher rates for longer" environment. Once the market shifts from "discussing long-term potential" back to "looking at current quarter EPS," these targets will be the first to be sold.

6. Conclusion: The Car Isn't Safely Parked Yet, Don't Unfasten Your Seatbelt Too Early

The final conclusion circles back to the first sentence: The May CPI dismantled the "immediate rate hike" bomb, but did not dismantle the "higher for longer" valuation pressure; currently, the window for phased deployment is beginning to open, it's not the starting gun for going all-in. If Walsh's comments on June 18 are merely verbally hawkish, core inflation remains controllable, and AI EPS and orders are not revised downward, I will view this pullback as a medium-term deployment opportunity. Conversely, if oil prices continue to rise, the dot plot becomes more hawkish, and semiconductor hedging demand increases instead of decreasing, I will continue to keep positions within a tolerable volatility range.

One-sentence summary: CPI gave the market a breather, but the car isn't safely parked yet. Don't rush to go all-in. Deploy in phases, and keep sufficient cash reserves to cope with potential 3%-4% volatility. That is the key to survival in the current environment.

Risk Disclosure

This report is for research and discussion purposes only and does not constitute any promise of returns or individual stock buy/sell recommendations. The key risks to monitor moving forward are threefold: First, if oil prices and geopolitical conflicts continue to push up headline inflation, US Treasury yields may rise again, thereby suppressing high-valuation tech stocks; Second, if the FOMC dot plot and official statements turn significantly more hawkish, the market's discounting of "higher for longer" will deepen; Third, if the AI supply chain shows signs of slowing orders, declining gross margins, or stalling EPS upgrades, the semiconductor rebound will shift from valuation recovery to fundamental verification failure.

References

1. U.S. Bureau of Labor Statistics, *Consumer Price Index — May 2026*. https://www.bls.gov/news.release/cpi.htm

2. CNBC, *CPI inflation report May 2026*, June 10, 2026. https://www.cnbc.com/2026/06/10/cpi-inflation-report-may-2026.html

3. Morningstar, *May CPI Forecasts Show Continued Lofty Inflation*. https://www.morningstar.com/economy/may-cpi-forecasts-show-continued-lofty-inflation

4. CNBC Make It, *Rate hikes are back on the table amid rising prices*, June 10, 2026. https://www.cnbc.com/2026/06/10/interest-rates-may-stay-higherwhat-it-means-for-your-money.html

5. Yahoo Finance Chart API, daily prices for SMH, MTUM, MU, QQQ, SPY and ^VIX, retrieved June 11, 2026. https://finance.yahoo.com/

6. Roger Lee Research, *The interest rate hike is not the tech killer, EPS is: The strategy of strengthening positions while cutting weak ones after the AI market's major decline*, June 8, 2026.

7. Benzinga, *Hottest Inflation In Over 3 Years: Is The Fed Ready To Hike Interest Rates?*, June 10, 2026. https://www.benzinga.com/markets/economic-data/26/06/53128579/may-cpi-reactions-fed-hold-inflation-4-2

8. Reuters, *Gold inches higher as oil falls, US rate-hike fears cap gains*, June 9, 2026. https://www.reuters.com/world/india/gold-extends-falls-rising-treasury-yields-2026-06-09/

This report is prepared by a special analyst. The views expressed in the report represent only the personal stance of the author and do not represent the views of the BIT platform. This material is for reference only and does not constitute investment advice.