When Nvidia on Bitget Starts Paying Dividends, the Stock Market Enters Its 'Reality' Moment

- Core Viewpoint: The tokenized stock track is evolving from "shadow tokens without real asset backing" towards financial products with real custody, complete rights, and cross-asset portfolio capabilities. By building its own Reality platform, Bitget has achieved features such as underlying 1:1 real stock custody, dividend distribution, and usability as collateral, aiming to construct a "panoramic exchange" covering crypto, US stocks, gold, forex, and other assets.

- Key Elements:

- Bitget's stock perpetual contract market share has reached 22.61% (second globally), with its tokenized stock trading volume accounting for approximately 89% of the Ondo platform. Cumulative trading volume for stock futures has exceeded $10 billion.

- Its self-built Reality platform, through licensed broker Alpaca, achieves 1:1 underlying stock custody. It undergoes independent audits by The Network Firm and publishes real-time reserve proof via on-chain dashboards, ensuring asset authenticity.

- rTokens (such as rNVDA) already possess dividend rights, with dividends distributed in USDT or token form. Additionally, they can be integrated into Bitget's unified account and used as collateral for cross-asset trading (e.g., using Nvidia stock to open BTC contracts).

- Bitget has launched the IPO Prime product, allowing users to subscribe for equity in unlisted companies (such as SpaceX, OpenAI) via an SPV structure. The two rounds attracted nearly $300 million in subscriptions from nearly 20,000 participants.

- The platform has listed CFD products covering 79 varieties (forex, gold, etc.), with daily trading volume peaking at over $8 billion. The range of assets far exceeds the scope of traditional crypto exchanges.

Author: David, Chaoxiang Research

Tokenized US stocks are one of the fastest-growing sectors in the crypto industry over the past two years, and also one of the most criticized.

What’s the criticism? That it’s an empty shell.

For example, you spend 100 USDT to buy a token called NVDA, thinking you own a small piece of an NVIDIA stock. In reality, you’re likely just getting a shadow that tracks the stock price. There are no real underlying stocks, no dividends, and none of the rights a stock should have.

Yet, this criticized sector has become the inevitable trend in the current version of the crypto industry.

And within it, one exchange has produced a set of figures that are hard to ignore.

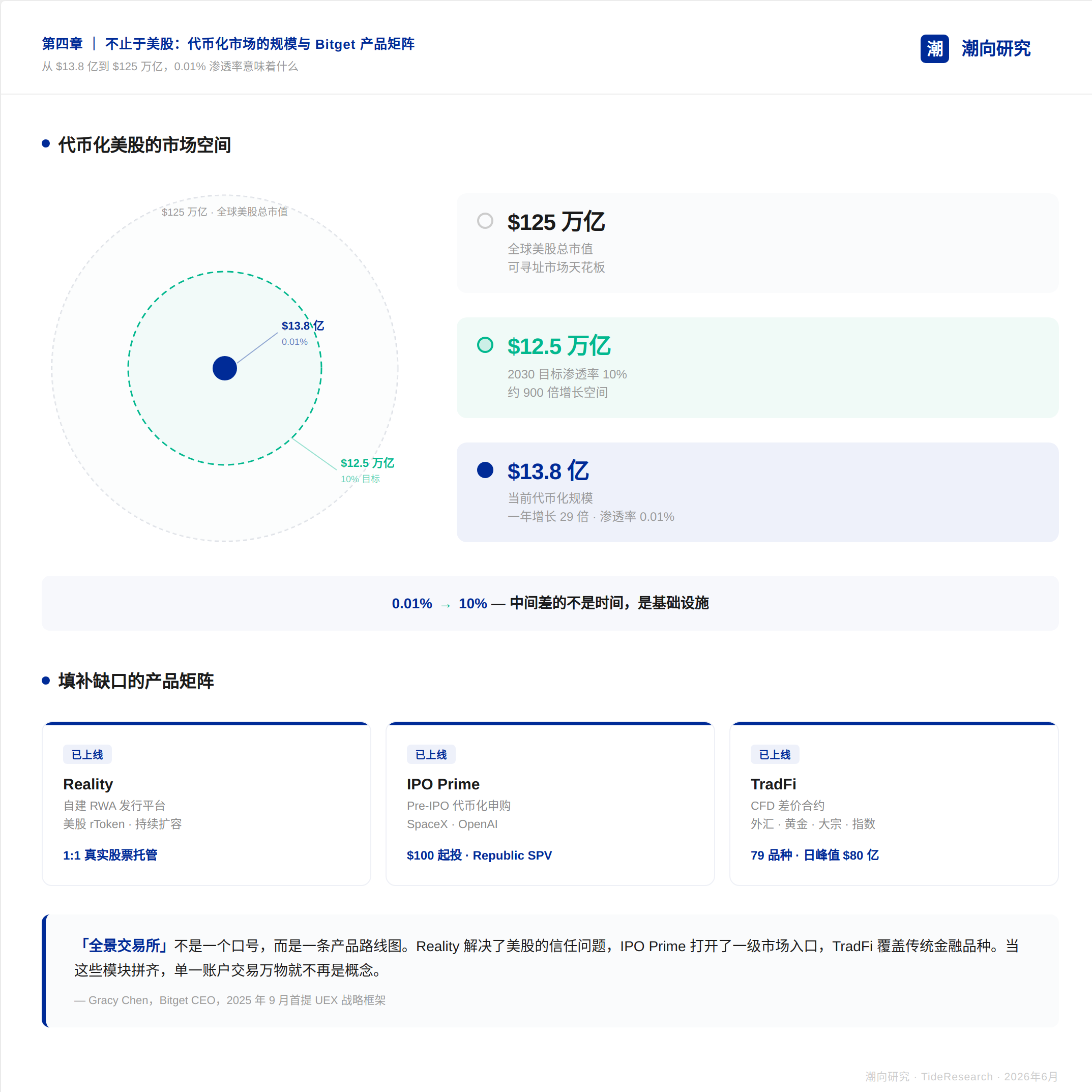

According to Bitget's Q1 2026 Transparency Report, the peak trading volume of non-crypto assets now accounts for 40% of the platform's total. Stocks, gold, and forex—assets that should normally appear in a brokerage app—are now being traded in significant volume on a crypto exchange.

TokenInsight's Q1 contract market report provides another reference point. Bitget's stock perpetual contracts ranked second globally, with a market share of 22.61%.

Additionally, within the tokenized stocks issued by Ondo, Bitget alone consumed approximately 89% of the trading volume. The cumulative trading volume of stock futures has exceeded $10 billion, and spot volume has surpassed $1 billion.

Now, look at the user side.

According to Bitget's user asset allocation report published in May this year, 52% of users' portfolios already include both cryptocurrencies and US stocks. Half of the users are no longer just buying coins; their accounts now house assets from two worlds.

A year ago, all these figures were zero.

The numbers are impressive, and the demand is real. But from our perspective, a sharper question lies behind the numbers:

With these on-chain US stocks, what exactly are you buying? Or, are you spending real money only to buy a sophisticated price shadow?

Bitget took nine months to answer this question.

Stones from Other Hills, Applied to US Stocks

In Q3 last year, Bitget started stocking US stocks on its shelves, using the concept of "stones from other hills."

Tokenized stocks issued by third parties like Ondo and xStocks were listed and traded on Bitget. Concurrently, they launched the industry's first US stock index perpetual contract, offering up to 100x leverage and 24/7 trading.

This model ran for a few months. By the end of December last year, the contract volume reached $10 billion, a substantial scale. The demand was clear: users wanted to trade US stocks on a crypto exchange. However, the product itself had issues.

Stones from other hills can polish jade, but if the stone itself is too coarse, a smooth experience cannot be built. As volume grew, problems followed.

For example, you search for NVIDIA and buy 100 USDT of the on-chain NVDA token. The price does track the Nasdaq. But then what?

First, the liquidity depth is at a DEX level; even moderately large orders suffer noticeable slippage. Second, regarding shareholder rights, if NVIDIA pays quarterly dividends, you receive nothing. When a stock split occurs, your position might take days to update.

For on-chain US stocks, you essentially buy a price first, and receive nothing else.

In fact, these three issues are not unique to Bitget; they are common ailments across the entire tokenized US stock sector. Third-party issuers control the underlying assets and product logic, making the exchange merely a shelf for display. You have no control over liquidity, dividends, or asset usability.

The ceiling of the distribution model is the ceiling of someone else's product.

For Bitget and other exchanges, two paths lay ahead at this point. One was to continue patching up someone else's infrastructure. The other was to build their own ship. They chose the heavier path.

Self-Polishing: When Stocks on Bitget Start Paying Dividends

Recently, NVIDIA just announced it would raise its quarterly dividend from $0.01 per share to $0.25, with the next payment date on June 26. If you hold rNVDA on Bitget, your account might soon see a cash dividend converted into USDT, and your cost basis will update automatically.

In the on-chain US stock sector, "real equity" is likely a first. This corresponding right exists because the underlying on-chain US stocks have undergone a new evolution on Bitget.

In June this year, Bitget launched a platform called Reality. The name literally translates to 'reality.' In a crypto-US stock sector full of shadow stock assets, the name itself reads more like a manifesto:

When tokenized stocks become the mainstream of the future, they will shed the prefix "tokenized" and become the default stock in people's minds. What people trade today will instead be prefixed and called "traditional stocks."

This might sound like science fiction, but Reality's goal is to turn it into reality.

What the platform does is not complicated. Instead of sourcing from Ondo or xStocks, it issues its own tokenized US stocks through Reality. Issuance is handled by Reality, custody is entrusted to licensed broker Alpaca, and audits are independently executed by The Network Firm. Each party handles its respective role.

The stock tokens issued by the platform are called rTokens. The US stock tickers you now buy on Bitget will appear with an 'r' prefix.

What’s the difference in experience between rTokens and the third-party tokens from six months ago?

The most direct difference is that you can finally figure out if there's something real behind them. In the 1.0 era of tokenized US stocks, the underlying custody chain was essentially a black box for users. You never knew if the NVDA you bought was actually backed by an NVIDIA share.

Reality lays this chain bare. rToken-style tokenized US stocks have a direct mapping to underlying real-world assets.

For example, when you buy $100 worth of rNVDA on Bitget, Reality, through Alpaca, purchases an equivalent amount of real NVIDIA shares on the US stock market and deposits them into an Alpaca custody account. Whatever you buy, it buys, in a 1:1 ratio.

Public information shows Alpaca is a licensed self-clearing broker in the United States, registered with the Financial Industry Regulatory Authority (FINRA) and protected by the Securities Investor Protection Corporation (SIPC).

SIPC is a federal-level investor insurance mechanism in the US, meaning even if the broker itself fails, the securities assets in the custody account have a safety net, up to $500,000. Alpaca is currently one of the most widely used custodians in the tokenized securities space, serving clients including Binance, Ondo, and xStocks.

Independent audits are conducted by The Network Firm, which produces CPA-level reports confirming reserve ratios of over 100%. Bitget also provides a separate on-chain proof-of-reserves dashboard, updated in real-time and publicly accessible.

You buy an asset, and you know it's real. This is the perceived change at the user level.

Following this experience, you can see the design philosophy behind Reality's entire architecture. Bitget deconstructed tokenized US stocks into three layers for rebuilding:

The first layer is securing the foundation. The aforementioned Alpaca custody, 1:1 purchasing, and on-chain proof-of-reserves address the fundamental trust issue: "Is there really something behind what I'm buying?"

The second layer is completing the rights. Stock dividends are issued 1:1 as tokens to your account, cash dividends are converted to USDT and deposited directly, and stock splits and reverse splits are mapped onto the chain in real-time. For the past two years, if you bought tokenized NVIDIA elsewhere, you watched real shareholders collect dividends quarterly while your account remained unchanged. This time, it's the rToken holders' turn.

The third layer is asset activation.

rTokens are integrated into Bitget's unified account system. Your rNVDA holdings can be used directly as margin. You can use an NVIDIA position to open a BTC contract, using a US stock to leverage a crypto position. In traditional brokerages, cross-asset margin is typically reserved for institutions; in previous on-chain US stocks, it was unthinkable. Now, an ordinary user can achieve a similar effect on Bitget.

So, with this self-built infrastructure, what's the cost of buying stocks?

Based on publicly disclosed fee schedules from various platforms, for buying $1,000 worth of US stocks, Bitget charges approximately $0.40, while traditional online brokerages typically charge around $2.

Looking at these three layers together, the tokenized US stock category has undergone a qualitative change at Bitget: from being a shadow token that merely tracks the price, to a financial product with real custody, complete rights, and the ability to be used interchangeably with crypto assets.

Two years ago, brokerages wouldn't have done this, and exchanges couldn't.

Some might ask, since the goal is to trade US stocks, why not take an easier route, like simply connecting to a broker's channel and building a front-end?

Bitget's choice was the opposite. Instead of being an adjunct to traditional finance, they chose to rebuild the entire chain using crypto and on-chain methods. Reality is fully self-controlled from custody to distribution to on-chain mapping. rTokens are inherently on-chain assets, capable of being deposited, withdrawn, and composed – things that a simple broker connection cannot achieve.

Writing this, I was reminded of a famous line from the Chinese drama *The Knockout*: "The bigger the waves, the more valuable the fish."

But to navigate the sudden shifts in the market environment and catch more fish, you need a reliable boat. Renting someone else's boat might work, but with a boat you build yourself, you set the waterline. This is likely the unspoken but evident ambition behind Bitget's Reality platform, despite its various public communications.

And clearly, Bitget doesn't intend to use this boat just for US stocks.

Beyond US Stocks: The Blueprint for a Panoramic Exchange

The first cargo loaded onto the newly built boat wasn't just publicly traded company shares.

In April this year, Bitget launched a product called IPO Prime, allowing ordinary users to subscribe to shares of companies not yet public. The first offering was SpaceX, with a subscription price of $650 per unit and a total pool of approximately $61 million. The result: $177 million poured in, with 14,435 people competing.

The second offering switched to OpenAI, with a subscription price of $725 per unit and a pool of about $21 million. Actual subscriptions reached $120 million, with 5,448 participants, oversubscribed by nearly six times.

Combined, the two rounds saw nearly $300 million in subscriptions from almost 20,000 participants.

The common characteristic of these two companies is that, in the world of traditional finance, ordinary people have no channel to gain equity exposure before their IPOs. Behind IPO Prime is an SPV structure in partnership with Republic, anchored by real equity.

Beyond Pre-IPO, Bitget also launched TradFi late last year, a USDT-denominated CFD product covering 79 instruments including forex, gold, commodities, and stock indices, with a peak daily trading volume exceeding $8 billion.

Combined with the growing suite of US stock rTokens from Reality, the types of assets accessible from a single Bitget account now far exceed the traditional definition of a "crypto exchange."

Bitget internally refers to this direction as UEX, or "Unified/Ultimate Exchange" – the Panoramic Exchange.

When CEO Gracy Chen first publicly mentioned this concept last September, the goal was straightforward: to cover crypto, US stocks, gold, ETFs, and forex, allowing one-stop trading of global quality assets through a single account.

To support this framework, the team is also expanding.

Public information shows that Bitget has intensively recruited a group of versatile talents with backgrounds in both traditional finance and internet growth over the past six months. New hires come from companies like Futu (Fubao), LongBridge, Robinhood, and eToro, bringing cross-market experience spanning the US, Hong Kong, Singapore, and Australia, and maintaining cooperative ties with traditional financial institutions like Nasdaq.

Judging by the recruitment direction, this isn't a crypto exchange playing catch-up; it looks more like a new species building its skeleton.

What I find interesting is Bitget's attitude towards this endeavor. There's a lighter path to trading US stocks: connecting to a broker's channel, slapping a front-end on it, and letting users buy and sell. Many platforms take this route. Bitget, however, chose the heaviest one: building its own issuance platform, constructing its own custody chain, with rTokens being deposit-able, withdrawable, and composable on-chain.

Why?

From a product perspective, Bitget's stance is clear. A broker-direct connection scheme is essentially just a front-end for traditional finance. The stocks users buy live within the broker's system. They can't be deposited on-chain, withdrawn to a wallet, and certainly can't be used to leverage a BTC position.

The rTokens built on Reality are born as on-chain assets, capable of far more than a broker channel. Choosing