告别传统牛熊,市场进入泡沫轮动时代

- 核心观点:当前金融市场已从过去缓慢、持续的牛市熊市周期,转变为由一系列快速轮动、相互关联的热点板块构成的“链式风暴”行情。投资者需跳出对单一热点趋势的执念,从更高维度识别结构性变化和循环逻辑。

- 关键要素:

- 市场结构根本性转变:与过去几十年相比,投机群体全民化、永续买盘形成、被动投资崛起、多策略基金和高频交易主导等八大变革,共同塑造了当前市场环境,且趋势不可逆转。

- 行情形成模式:市场热点如同夏季雷暴,由特定触发点启动,经历“蛰伏-启动-叙事-分化-破裂”等阶段。资金从消退热点流出,如同冷空气楔子,点燃相邻领域的新一轮行情。

- 关键结构性因素:低交易成本、被动指数投资对价格不敏感、多策略基金风控趋同导致市场脆弱性集中,信息传播零延迟加剧了情绪和趋势的放大。

- 投资者群体分化:市场主要利好两类投资者:深入理解技术壁垒与盈利逻辑的行业专家,以及能洞察主流资金行为模式和市场情绪的趋势观察者。

- 未来题材持续丰富:AI基础设施、机器人、加密货币、核聚变、量子技术等多个领域的上下线环节将持续成为潜在热点,为轮动提供充足燃料。

Original Author: Smac, Partner at Compound VC

Original Translation: Saoirse, Foresight News

Editor's Note: As market hotspots emerge one after another, the AI craze is sweeping the scene, leading some to question whether it will repeat the fate of the metaverse hype cycle. Amidst the market noise, people are easily swept away by the immediate trends, losing sight of long-term trajectories. To make rational judgments, one must learn to elevate their perspective. In this article, Compound VC partner Smac uses a meteorological analogy to deconstruct the market logic behind the successive bubbles.

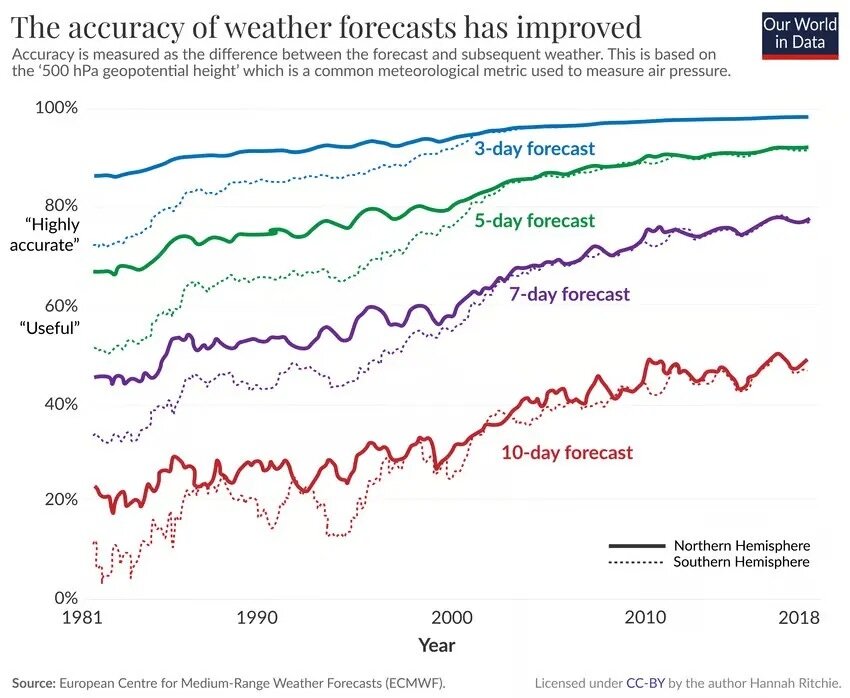

Meteorology is a fascinating field. Over the past fifty years, various weather forecasting tools have been iteratively improved, enhancing the accuracy of weather predictions. Today's five-day forecast is as precise as a single-day forecast was thirty years ago.

Most people perceive weather as a single, coherent moving system: clouds roll in, rain falls, it stops, and the sky clears. Imagine a winter front approaching; the image that likely comes to mind is a vast expanse of grey clouds covering hundreds of miles, dumping heavy snow. Meteorologists call this type of weather stratiform clouds. Simply put, it's like a layered cake; any area within the cloud cover experiences the same weather changes.

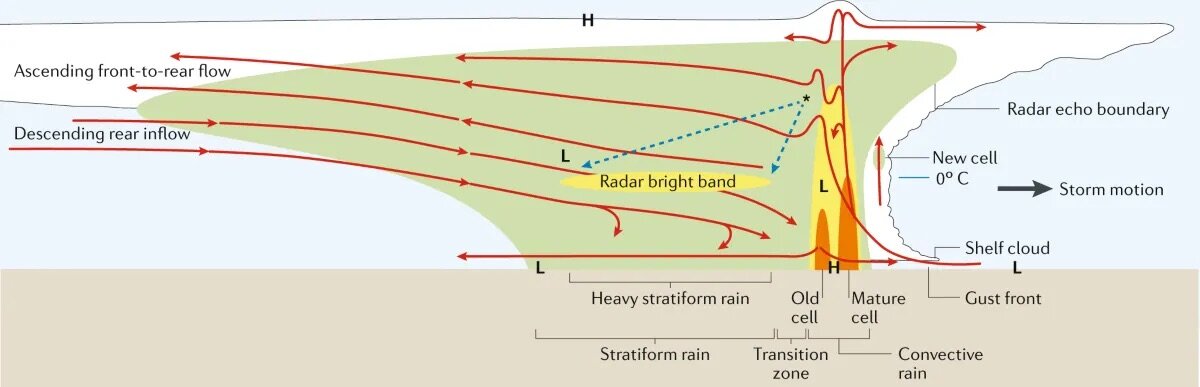

But weather isn't always like this. If you've ever witnessed a summer thunderstorm over the plains, you know it operates quite differently. First, a single convective cloud forms: warm, moist air near the surface rises, meets colder air aloft, the water vapor condenses, and a towering, localized cumulonimbus cloud develops. Within an hour, hail, lightning, and torrential rain arrive, reducing visibility to less than a hundred meters.

The cloud cluster peaks, unleashing its energy completely, and then gradually dissipates. The storm's downdraft of cold air spreads outwards at speeds up to 40 miles per hour. When this cold air collides with the surrounding warm, moist air that hasn't yet formed a storm, it acts like a wedge, forcing the warm air upwards again.

As long as sufficient instability exists in the atmosphere, this "cold air wedge" spawns a new convective cloud cluster about a dozen miles away from the original storm.

This new cluster couldn't form on its own. The energy was already stored in the atmosphere, lacking a trigger, which the dissipating storm provided. The new cluster then repeats the evolution process of the previous storm.

When multiple convective clusters form in succession, they create a mesoscale convective system. For someone on the ground, they experience each storm individually, with each storm feeling like the entirety of the weather system. On one side, it's calm, with no sign of the impending storm; on the other, the sun is already out after the rain. But from a satellite perspective, you see a line of independent clusters, each at a different stage of development, moving forward until they exhaust the warm, moist air along their path.

Supercell thunderstorm near Amistad, New Mexico at sunset

This system of sequential storms is fundamentally different from the conditions that create a single frontal system. It relies on a specific atmospheric environment:

- Warm, moist air near the surface, acting as "fuel" for the storms;

- Dry, cold air aloft, causing the warm air to rise continuously, creating atmospheric instability;

- Winds blowing from different directions at various altitudes, causing storms to rotate and move laterally, known as wind shear.

When all three conditions are met, storms will erupt one after another.

Enough about meteorology, let's get to the point: The meteorological phenomenon described above is almost identical to the state of today's financial markets.

Markets of the past were like stratiform weather systems: a bull market, then a bear market, alternating, with sector themes rotating slowly, each lasting for years. The period from 1982 to 2000 was a long bull market, followed by the dot-com bubble, and then the real estate and credit cycle from 2003 to 2007. These cycles were long and clear. Even if an investor was a few years off in their timing, understanding the major trend was enough to profit in the end.

But today's market is no longer the same. We are in an era of convective storm chains: individual hot sectors hit like successive storms, and anyone in the middle of one feels that this particular trend is unstoppable and all-encompassing.

Capital flows out of a fading theme and into a neighboring sector, igniting a new wave. The pace of market theme rotation has accelerated dramatically. AI infrastructure, GLP-1s (a class of diabetes drugs popularized by their weight loss effects, now a hot investment track in capital markets), stablecoins, quantum technology, nuclear power, distributed autonomous technology, robotics, aerospace... Each track goes through a complete cycle of hype, attracts a faithful following, completes a full narrative arc, and inevitably sees its heat dissipate. The "cold air" spreading from the dissipation of the previous wave then ignites the next hotspot in a new area.

Refusing to admit that the market has fundamentally changed is self-deception. People love to joke about "this time is different," but willfully ignoring the permanent transformation of the financial market environment is either intellectual laziness or stubbornly clinging to a fantasy of the old market.

A Market Landscape Unlike Any Other

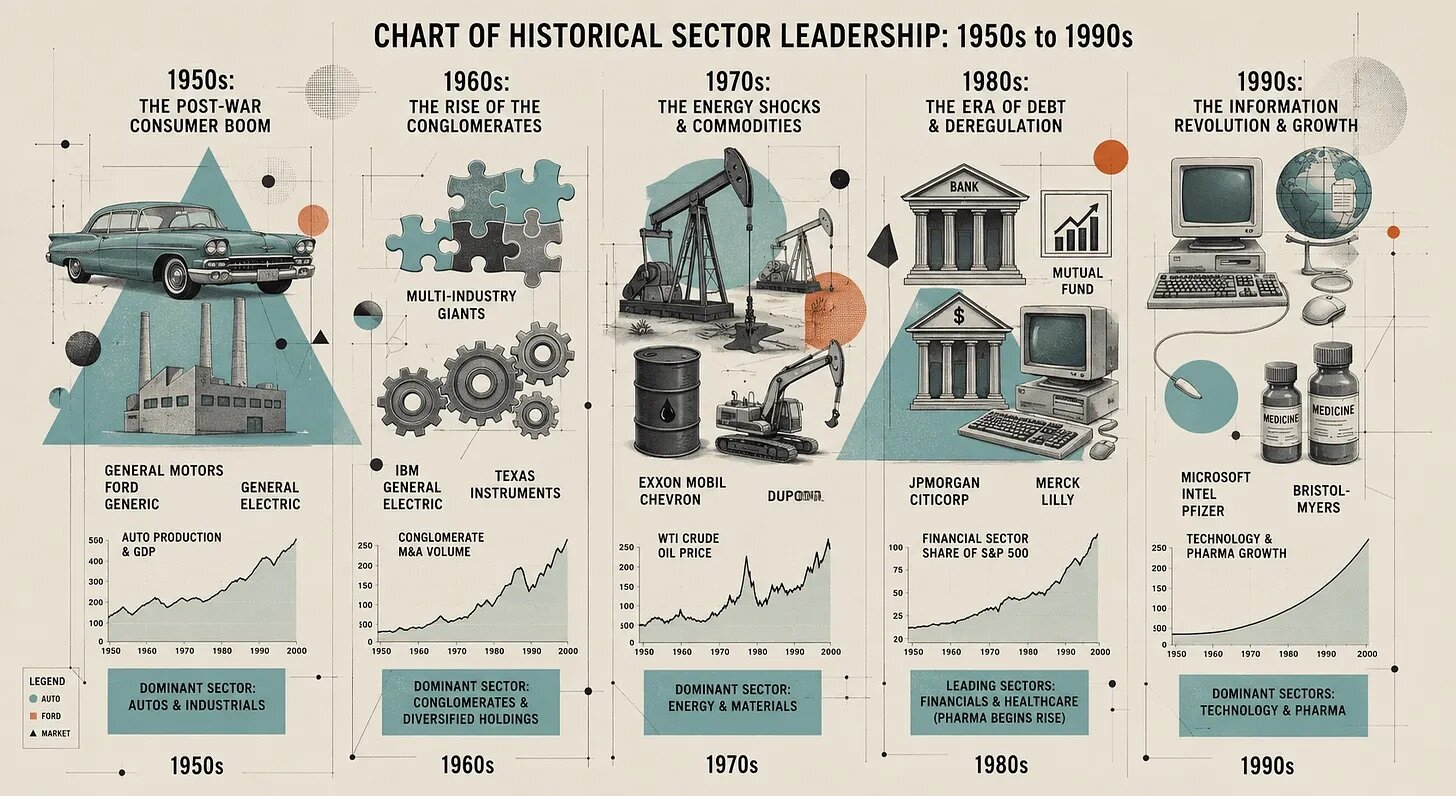

For a long time after World War II, the rhythm of financial markets resembled slow-moving weather systems. A bull market could last ten, fifteen, or even twenty years, with sector rotation always revolving around long-term megatrends.

Approximate timeline of industry themes and leading sectors

Back then, sector rotations occurred within a unified macro environment. The entire market landscape would only be overturned at landmark epochal turning points, such as the collapse of the Bretton Woods system, Volcker's anti-inflation policies, the peak of the dot-com bubble, and the global financial crisis.

This market form was shaped by numerous structural factors: high transaction costs in the past meant very low retail participation, forcing a long-term holding habit; pensions were the primary vehicle for retirement assets; the S&P 500 was heavily weighted toward manufacturing, energy, banking, and retail companies, whose earnings growth largely tracked the overall economy, making their trajectories stable and predictable. Simultaneously, information spread slowly; after a company's annual report was released, most investors often wouldn't see its contents for weeks.

Volatility in the past was also relatively balanced. Bull markets were followed by deep corrections, leverage was gradually flushed out, and adjustment cycles were long; rebounds in bear markets were similarly gradual. The market would linger in different sentiment zones for extended periods, with overall landscape shifts occurring over quarters or years.

Returning to the meteorological analogy: the old market had moderate fuel, high atmospheric stability, and weak wind shear, leading to long, stable trends where investors could plan calmly. Today, all environmental conditions have changed, some completely reversed, leading to a fundamental transformation of the market structure.

Where Does the Change Come From?

Many changes are intertwined, amplifying each other. Any one of these changes would be enough to reshape the market on its own. In summary, there are eight core transformations:

- Democratization of the Speculative Class

- Formation of Perpetual Buying Pressure

- Passive Investment Creates Inelastic Counterparties

- Rise of Multi-Strategy Funds and HFT, Disappearance of Market Intermediaries

- Volatility Artificially Suppressed

- Fundamental Shift in Index Composition

- Complete Elimination of Information Lag

- Shift in Fiscal and Monetary Environment

Democratization of the Speculative Class

The participants in today's market have visibly changed. In the 1990s, retail trading volume accounted for only about 10% of total U.S. stock market turnover. Due to high commissions, retail investors predominantly held stocks long-term, with very little active speculation.

Robinhood pioneered zero-commission trading and created the payment for order flow model; in the fall of 2019, Schwab followed suit by eliminating trading commissions, with Fidelity, TD Ameritrade, E*Trade, and other brokers quickly joining, completely rewriting the industry rules.

The COVID-19 pandemic further accelerated this trend: fiscal stimulus checks distributed, people stuck at home, and mobile trading apps deliberately gamifying the experience. From 2020 to 2021, retail trading volume share surged to 25%. Many thought this was a temporary phenomenon, but the high level of retail participation has persisted. On April 29, 2025, amid market volatility triggered by tariff policies, JPMorgan data showed retail order flow reached a record high of 48% of total volume. On normal trading days, retail volume is more than double pre-pandemic levels; during significant market swings, this proportion can reach up to 35%.

A deeper change lies in what retail investors are trading. Single-stock options have become a mainstream choice for retail, and the expansion of 0DTE (zero days to expiration) options has been explosive. New participants are primarily young, hold highly concentrated portfolios, and trade based on market themes. Crucially, these investors often use special methods to leverage their bets (leverage that doesn't appear in standard margin data), making trading decisions more based on price action than company fundamentals, and they are highly susceptible to following others.

In meteorological terms: the "warm, moist air" near the surface of the market is more abundant than ever, with pent-up potential energy reaching historic highs.

Formation of Perpetual Buying Pressure

I have analyzed this point in previous articles. Simply put, the U.S. retirement security system has shifted from defined-benefit pensions to defined-contribution plans. Now, individuals must manage their own retirement finances. Reflected in the market, this means a massive, price-insensitive wave of passive money buying stocks every pay cycle, creating automated, perpetual buying pressure.

The operational logic of traditional pensions was completely different: defined-benefit plans needed to match liabilities and manage duration risk. Managers would actively judge market valuations; if they thought stocks were too expensive, they would adjust asset allocation and increase bond holdings. Even if rebalancing was slow, it was far more active than today's purely passive perpetual buy orders.

This is crucial: the marginal trading capital in the market has far more power to influence prices than ever before.

Passive Investment Creates Inelastic Counterparties

The essence of passive index investing is to buy and sell strictly according to the weight of constituent stocks, regardless of price. The higher a stock's market cap, the more passive money flows into it, and vice versa. This mechanism naturally embeds momentum into the market's underlying logic: stronger-performing assets attract more passive capital, which is a significant reason for the strong performance of the "Magnificent Seven" mega-cap tech stocks.

For years, articles have analyzed the concentration of index weight toward top companies. Of course, these top companies are not undeserving; their profitability and growth are robust. But the core issue is that passive capital has no built-in "take-profit switch."

Rise of Multi-Strategy Funds and HFT, Disappearance of Market Intermediaries

Concurrently with the emergence of perpetual passive buying, the active trading landscape has also undergone a dramatic shift, marked by the rise of multi-strategy portfolio trading firms. Institutions like Citadel, Millennium, Point72, and Balyasny aggregate hundreds of independent portfolio managers, each running a specialized trading strategy, all under strict risk controls. The assets under management of these firms have exploded, with capital concentrating at the top, mirroring the concentration trend in stock index constituents.

At the same time, high-frequency trading (HFT) now accounts for 50% to 60% of U.S. stock market volume and up to 75% in futures markets. This combination creates an extremely fragile market environment: these trading firms are each other's counterparties, and the price discovery function of the market is weakened. A large portion of the volume on the tape is just capital circulating within the market itself.

Under normal conditions, bid-ask spreads are very tight, which is beneficial. However, when a theme narrative breaks, market positioning becomes extremely imbalanced, or the risk limits of multiple firms are triggered simultaneously, the market microstructure can instantly break down. The risk exposures of all portfolio managers are highly correlated, and their stop-loss rules are largely similar. When one firm is forced to reduce positions, the rest follow suit. The market crashes of February 2018, August 2019, March 2020, and August 2024 are classic examples. The market structure that fosters such events is now deeply entrenched and will recur.

Traditional fundamental long-short hedge funds are being squeezed out: these funds relied on deep research for stock selection, holding 20-40 stocks with investment horizons spanning several quarters. Nowadays, these firms are either being absorbed by large asset management platforms or migrating to private markets, family offices, or single-strategy funds. In my view, significant alpha can still be found by understanding the logic of theme rotation and maintaining patience amidst the flow of short-term capital.

Volatility Artificially Suppressed

Combining the above four points, the current volatility dynamics are easy to understand. Data shows that since 1990, the VIX (fear index) has closed below 20 on two-thirds of trading days; the daily correlation of volatility is as high as 85%, meaning the day's volatility level essentially carries over from the previous day.

But the pattern of volatility shifts has become extreme and unbalanced: extensive research shows that once suppressed volatility crosses a threshold, it explodes violently within a few days; the process of volatility declining, however, is very slow, often taking weeks.

There are multiple structural reasons behind this: a massive "short volatility" industry has emerged. The proliferation of 0DTE options further suppresses intraday volatility through market makers' hedging activities. The market remains in a calm, low-volatility state for extended periods, accumulating risk; when tail risk materializes, all participants rush for the exits simultaneously.

In short, the distribution of volatility in today's market is increasingly skewed: long periods of low volatility building up energy, ultimately leading to more violent risk releases.

Fundamental Shift in Index Composition

The sixth change is the very composition of the stock indices themselves. In 1980, the S&P 500 was dominated by manufacturing companies. Industrial, materials, energy, financials, and consumer staples were the leading sectors. The earnings growth of these companies largely tracked GDP, with smooth growth curves, and valuation multiples would mean-revert around a reasonable central value. Even forecasting earnings for a company like Procter & Gamble five years out wouldn't yield massive errors.

The situation is completely different now. Information technology, communication services, plus tech-leaning consumer discretionary names like Amazon and Tesla, collectively account for over 40% of the S&P 500's weight. The earnings models of these companies are no longer linear: the marginal cost of distributing software is essentially zero; and the AI track is full of uncertainty – will AI labs be the core infrastructure of the next half-century or a bottomless pit of capital expenditure? Market opinions are polarized.

For these types of companies, forecasting short-term earnings is difficult enough, and long-term value is highly variable, leading to significant fluctuations in valuation. Valuations are no longer solely based on financial statements; market narratives become a core influencing factor. For investors who can anticipate the direction of frontier technology, understand competitive moats, and identify future emerging markets, there is substantial alpha opportunity here.

Traditional manufacturing companies expanded capacity gradually, with relatively stable results from discounted cash flow models, making valuation multiples more likely to revert to reasonable levels. Today, a company's valuation is largely determined by the market's acceptance of its development story. I am not suggesting traditional valuation frameworks are obsolete; this is merely the objective reality of today's new economy companies.

Today's major indices are filled with these long-duration, narrative-driven companies. The steeper the temperature gradient in the atmosphere, the more energy is stored. Similarly, the more of these companies exist, the greater the latent kinetic energy in the market; once a trigger appears, market volatility will be more intense.

Complete Elimination of Information Lag

Everyone can see this intuitively, but its impact is often underestimated. For most of financial history, the spread of market-related information was constrained by distribution channels. Now, information propagates with virtually zero delay.

This is especially true for portfolio holdings information, which spreads much faster than before. Investors can see in real-time how well-known figures react to news, and more and more people proactively disclose their holdings. This constant stream of real-time information fuels a culture of comparison. Screenshots of profits are everywhere, stories of turning a small principal into millions go viral, and the fear of missing out (FOMO) continuously intensifies.

Shift in Fiscal and Monetary Environment

This point needs little elaboration; the key summaries are:

- U.S. monetary policy has been persistently accommodative for a long time, with low real interest rates;

- Quantitative easing has continuously expanded the Federal Reserve's balance