AI PC大戰:不要押陣營,要押收費站

- 核心觀點:AI PC競爭的本質並非x86與Arm的架構之爭,而是產業鏈中「收費站」邏輯的確定;優先布局先進製程、算力平台等能持續獲得現金流的環節,而非押注某一陣營。

- 關鍵要素:

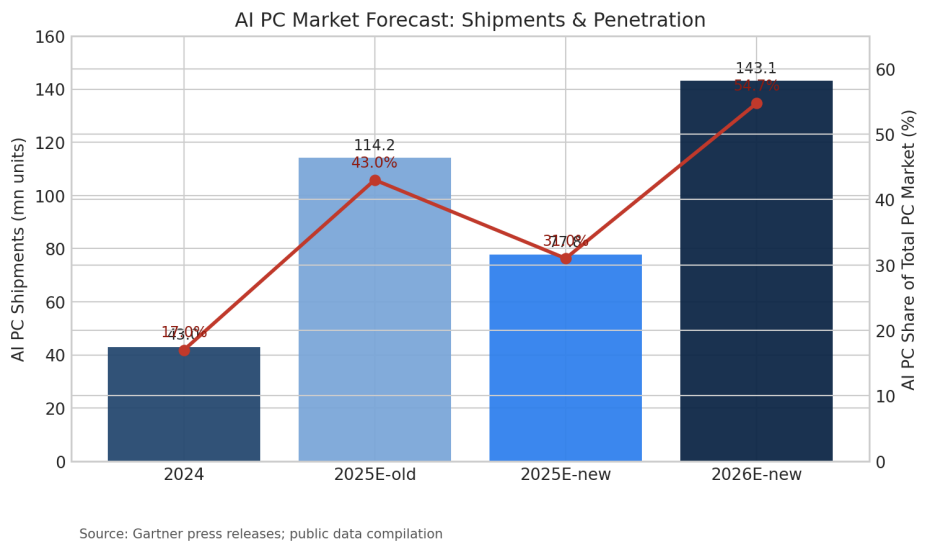

- Gartner預計2026年AI PC滲透率達54.7%,短期受關稅擾動,但長期標準配備化方向不變。

- 用戶換機動力取決於本地AI應用(如企業級隱私計算)能否超越「會議紀錄」等基礎體驗。

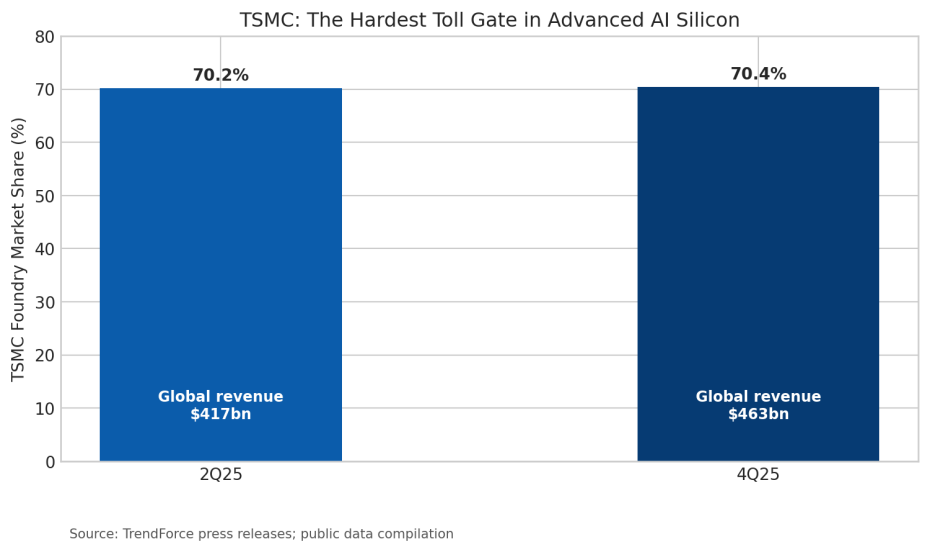

- 台積電(TSMC)作為先進製程「收費站」,2025年Q4全球晶圓代工市佔率約70.4%,受益於所有玩家競爭。

- 輝達與聯發科進場,使Windows終端AI生態從單點試水進入多玩家格局,加劇競爭。

- 投資標的分層:台積電為底倉,AMD與輝達提供進攻彈性,ARM和英特爾屬於高風險的困境反轉機會。

Original Author: Roger Lee, BIT US Stock Market Special Analyst

With 21 years of experience in investment banking, asset management, and financial institutions, specializing in AI industry chain, macro liquidity of US stocks, and options strategy research.

Report Date: June 4, 2026

Investment Summary

My core conclusion is simple: In the AI PC battle, don't bet on camps; bet on toll booths. Make TSMC your foundation, AMD your offensive play, ARM a small position for volatility, Intel only a lottery ticket, wait for Qualcomm to be re-priced, and don't chase NVIDIA after the FOMO triggered by news impulses.

NVIDIA and MediaTek's entry into AI PC appears on the surface as a new chipset combination for consumer PCs, but the essence is a shift in the Windows on-device AI ecosystem from initial trials to multi-player competition. My assessment is that this war should not be simplified into a "x86 vs. Arm" tribal standoff. What truly deserves study is who can survive replacement cycles, consistently secure gross margins, cash flow, and pricing power within the industry chain.

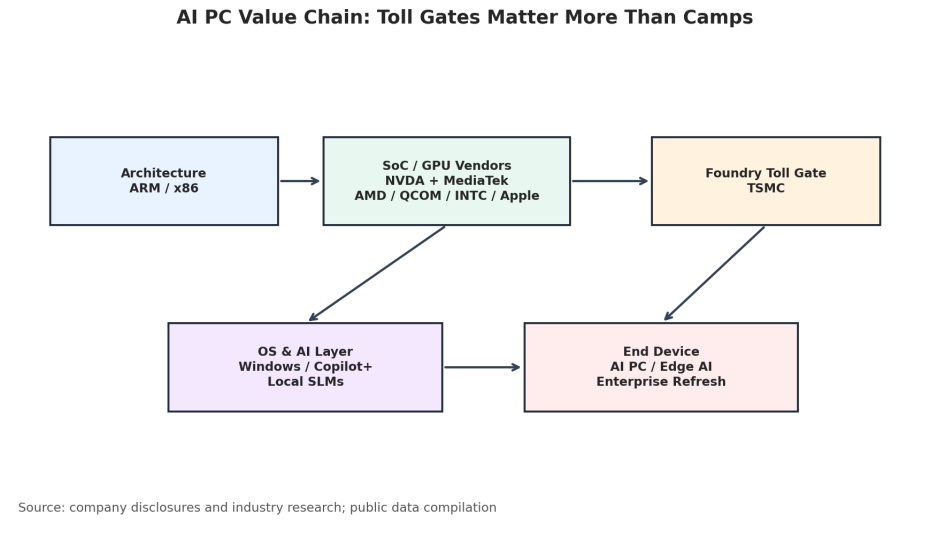

I view AI PC as a three-tier opportunity. The first tier is the advanced process toll booth – no matter who wins, TSMC is most likely to collect the toll. The second tier is computing power and platform spillover, where AMD and NVDA represent x86 offense and GPU software stack extension, respectively. The third tier is architecture diffusion and turnaround potential – both ARM and INTC have upside, but position discipline must be stricter.

I. Industry Assessment: AI PC Moves from Concept to Shipment Validation

In 2024, Gartner projected AI PC shipments would reach 114.225 million units in 2025, accounting for 43% of the PC market. After an update in 2025, affected by tariff and procurement rhythm disruptions, the forecast was revised down to 77.792 million units (31% share), but 2026 shipments are still estimated at 143.113 million units, with a penetration rate of 54.7%. The insight this data provides me is not that "AI PC demand is falsified," but that short-term rhythms may fluctuate, but the long-term trend of standardization remains unchanged.

From an investment perspective, the real challenge for AI PC is not whether it has an NPU, but whether users are willing to upgrade their devices for on-device AI experiences. If application layers remain limited to meeting minutes, image generation, and simple assistants, upgrade elasticity will be lower than the market's most optimistic expectations. However, if enterprise users start adopting privacy computing, low-latency inference, and local knowledge base deployment as standard configurations, AI PC will transform from a consumer electronics story into an enterprise IT upgrade narrative.

From an investment perspective, the real challenge for AI PC is not whether it has an NPU, but whether users are willing to upgrade their devices for on-device AI experiences. If application layers remain limited to meeting minutes, image generation, and simple assistants, upgrade elasticity will be lower than the market's most optimistic expectations. However, if enterprise users start adopting privacy computing, low-latency inference, and local knowledge base deployment as standard configurations, AI PC will transform from a consumer electronics story into an enterprise IT upgrade narrative.

II. Competitive Landscape: Chip Manufacturers Battle, TSMC Collects Toll Fees

The surface narrative of AI PC is Arm challenging x86, but I care more about where the profit pool shifts. NVIDIA excels in GPU and AI software stacks, AMD in x86 CPU and GPU combinations, Qualcomm in low power consumption and connectivity, and Intel in legacy ecosystem and enterprise channels. Each has its advantages, but a commonality is also clear: High-end chips cannot bypass advanced manufacturing processes.

TrendForce revealed that global foundry revenue in Q2 2025 was approximately $41.7 billion, with TSMC holding a 70.2% share. By Q4 2025, global foundry revenue reached about $46.3 billion, with TSMC's share around 70.4%. This means that as long as AI PCs, AI servers, mobile APs, and edge AI chips continue to compete for advanced nodes, TSMC is not simply a cyclical stock but more akin to the tollgate for the entire AI hardware era.

I don't believe every new product launch warrants a chase, but I do believe that with each instance of intensified industry chain competition, one should conversely ask: If the winner is uncertain, who can charge all potential winners? In the AI PC line, my answer remains advanced processes, packaging, key IP, and platform software, rather than simply betting on a single architectural slogan.

III. Stock Ranking: Core Position in TSM, Offensive in AMD, Upside Optionality in Intel/ARM

Over the past year, semiconductor stocks have already priced in expectations for AI PC, on-device AI, and computing power spillover. According to Yahoo Finance daily prices, within the sample period, AMD, Intel, ARM, and TSM all showed significant volatility, but they represent different risk-return profiles. My approach is not to buy all AI PC-related stocks together, but to layer them based on certainty, valuation discipline, and industry chain position.

My core conclusion is simple: This is not a war where you only buy the winner; it's a war where you should buy toll booths, platforms, and companies generating certain cash flows. If the market fully prices in sentiment on the day of a news release, I would rather wait. If a correction brings the risk-reward profile of good companies back into a reasonable range, I will prioritize TSM and AMD, followed by the option-like upside in ARM and Intel.

IV. Risk Disclaimers

The risks of this theme cannot be ignored. First, AI PC applications may underperform expectations, leading to a weaker-than-expected upgrade cycle. Second, if the compatibility improvement of Windows on Arm is too slow, the narratives of Qualcomm and new entrants will be suppressed. Third, tariffs, corporate purchasing pauses, and macroeconomic uncertainty could dampen PC demand. Fourth, if there is a temporary mismatch in advanced process supply and demand, TSMC could also face valuation pullbacks. Fifth, the entire AI chain is trading at high valuations; once US stock risk appetite declines, the most volatile stocks often see the fastest pullbacks as well.

Therefore, I prefer to view AI PC as a long-term industrial migration rather than a short-term news trade. The truly professional approach is not to buy slogans on the day of a launch event, but to wait for the tide of emotion to recede and then buy into ecosystems, toll booths, and companies that can consistently deliver cash flow.

V. Data Source Explanation

Data References

This report was prepared by a special analyst. The views expressed in this report are solely those of the author and do not represent the views of the BIT platform. This material is for reference only and does not constitute investment advice.