It wasn't carry trade unwinding that saved the Nikkei: Yen short positions remain crowded, and AI-driven foreign capital is the real driver of new highs

- Core Viewpoint: Although the yen is currently at a low level, short positions are crowded, and Japan's Ministry of Finance has conducted its largest-ever intervention, the Nikkei 225's new highs are primarily driven by foreign capital chasing AI themes. This mechanism is entirely different from the market decline triggered by carry trade unwinding in August 2024. Market narratives need to be dissected more carefully.

- Key Factors:

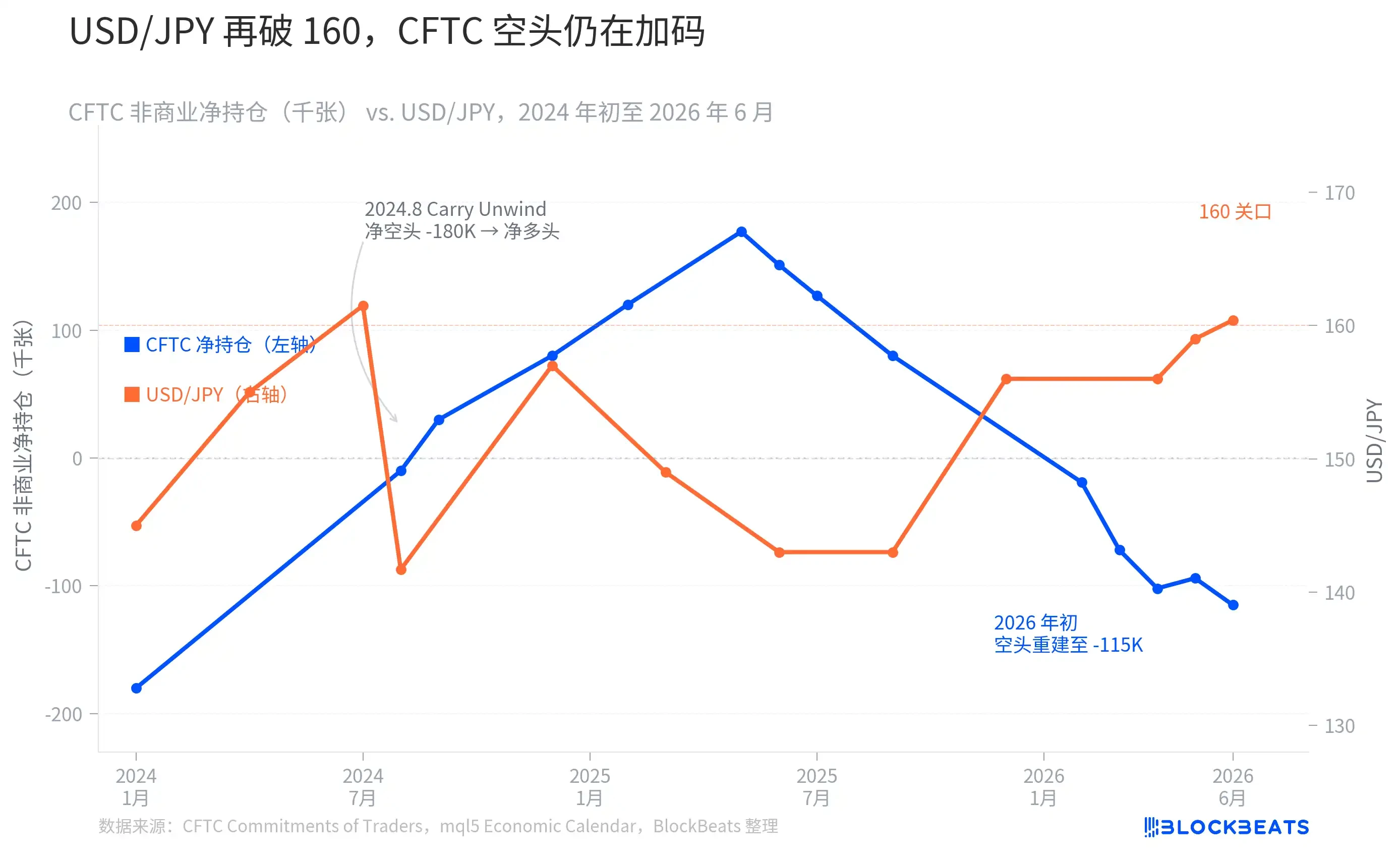

- As of May 26, CFTC data shows net short positions in yen futures stood at 114,667 contracts, an increase of 27,152 contracts from the previous week, indicating speculative funds are increasing their yen short bets, not withdrawing.

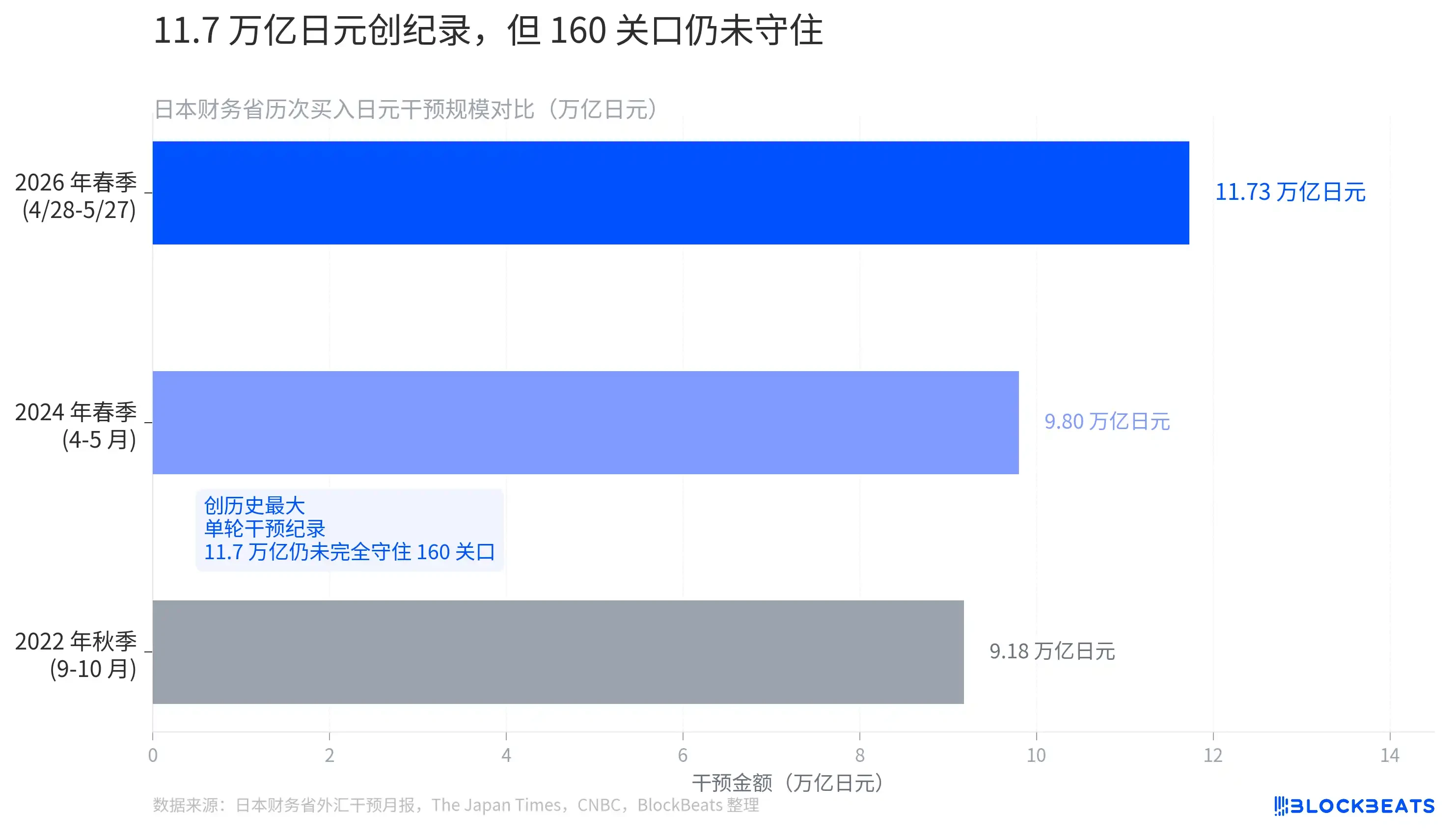

- Between April 28 and May 27, Japan's Ministry of Finance implemented a record single-round yen-buying intervention totaling 11.7349 trillion yen (approximately $73.6 billion), but failed to effectively defend the 160 threshold, showing limited intervention effectiveness.

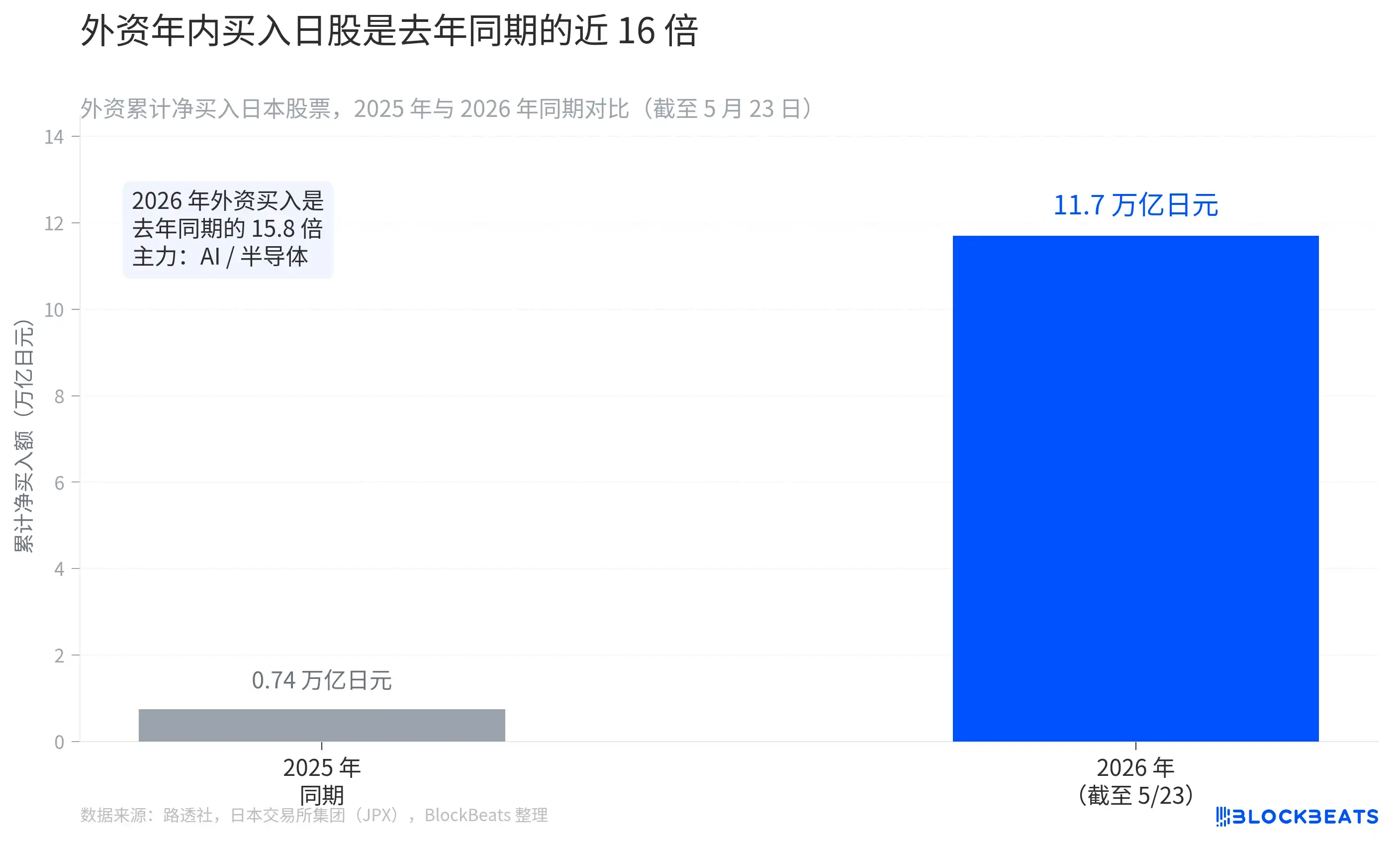

- In the week ending May 23, overseas investors were net buyers of Japanese stocks for the 8th consecutive week, with cumulative net purchases for the year reaching approximately 11.7 trillion yen, 15.8 times the amount in the same period of 2025. The buying logic was driven by AI demand boosted by Nvidia's earnings.

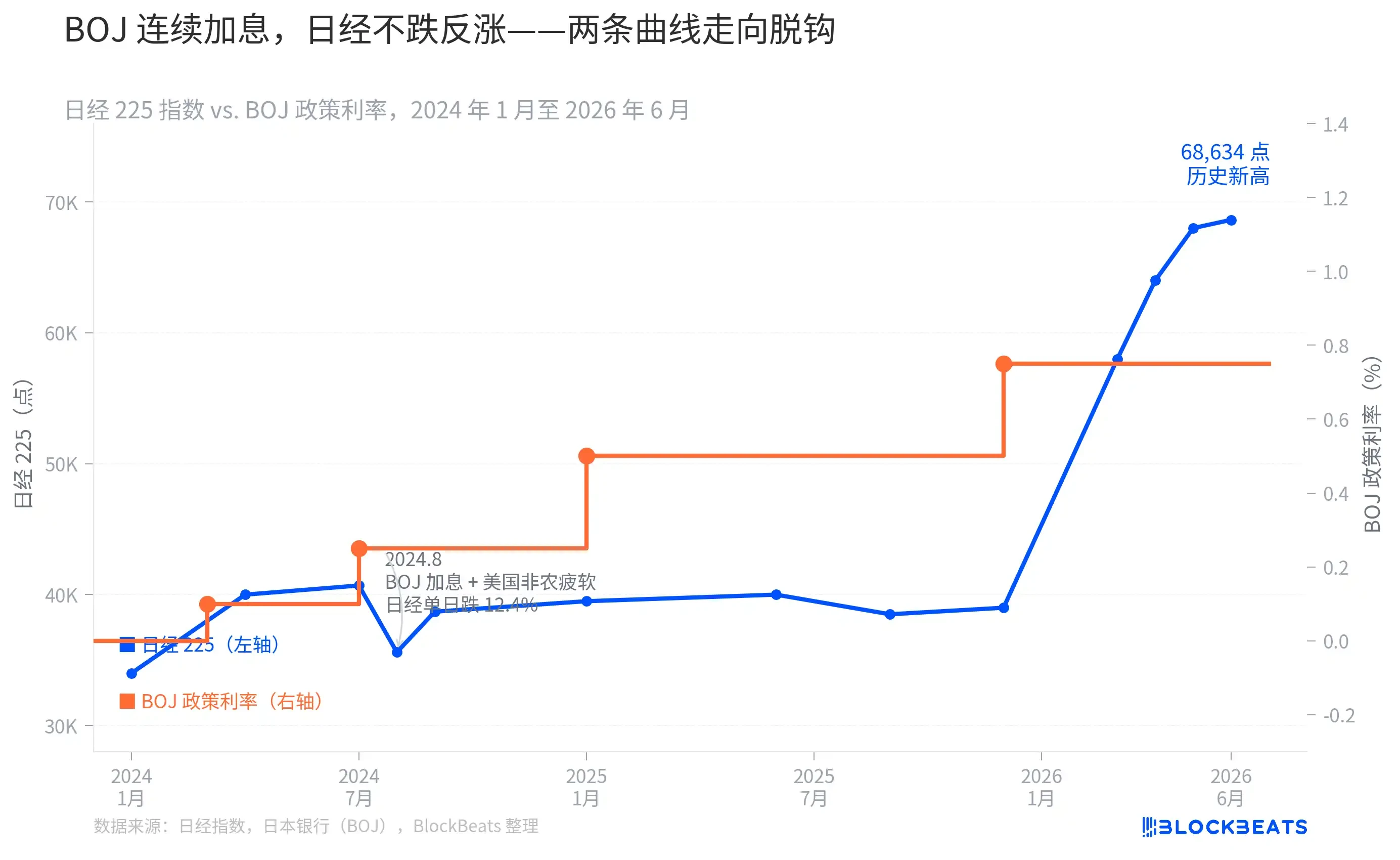

- The correlation between the Bank of Japan's interest rate hike path and the Nikkei 225's trajectory has changed: the July 2024 rate hike triggered a crash, but the rate hikes in January and December 2025 were accompanied by stock market gains, as AI capital is less sensitive to yen interest rates.

- If the BOJ raises rates to 1.0% at its July meeting while the U.S. dollar weakens, the currently crowded yen short positions (approximately 114,667 net shorts) could face passive unwinding pressure similar to August 2024.

6 月 3 日,美元兌日圓盤中觸及 160.44,是 2024 年 7 月以來的新高。同日,日經 225 指數首次突破 68,000 點,最高漲至 68,634.74 點。兩個數字疊在一起,市場上立刻出現了一套熟悉的敘事:「carry trade 要崩了,2024 年 8 月要重演」。

這套敘事有一半是對的。另一半,數據說的是完全相反的故事。

空頭沒有撤,反而在加碼

衡量日圓套利交易擁擠程度最直接的指標,是美國商品期貨交易委員會(CFTC)每週發布的非商業持倉報告。它記錄了投機性交易者在日圓期貨市場上的淨多頭或淨空頭倉位。

據 CFTC 持倉報告,截至 5 月 26 日當週,非商業帳戶日圓期貨淨空頭達到 114,667 張合約——多頭 112,993 張,空頭 227,660 張。較前一週淨空頭倉位進一步增加了 27,152 張。

從圖中可以看到一條有點反直覺的走勢。2024 年 7 月,USD/JPY 觸及 161 附近的高點,彼時 CFTC 淨空頭約在 -180,000 張的歷史極值區間。隨後 8 月初,日本央行(BOJ)意外加息疊加美國非農數據大幅低於預期,日圓空頭在短短幾週內被強制平倉,淨空頭從約 -180,000 張驟然收縮,到 2025 年第二季更反轉為超過 +177,000 張的淨多頭——carry trade 在那段時間確實出現了系統性擠倉。

但隨後的走向與「擠倉敘事」完全相反。從 2025 年底開始,日圓淨空頭倉位重新累積,2026 年 2 月翻負,4 月快速擴大至 -102,000 張。到 5 月 26 日,淨空頭已經達到 -114,667 張。USD/JPY 重返 160 附近時,全球投機資金不是在跑,而是在繼續加碼。

這意味著,如果 BOJ 在 7 月會議上發出更鷹派的訊號,或者美國經濟數據再次超預期走弱,這批 -114,667 張的淨空頭將面臨與 2024 年 8 月高度類似的被動平倉壓力。日本財務省也意識到了這一點——4 月 28 日至 5 月 27 日,財務省動用了創紀錄的 11.7349 兆日圓買入日圓、賣出外匯,試圖壓制空頭。

最大單輪干預,沒能守住 160

日本財務省在外匯干預方面的歷史可以追溯到 1998 年。2022 年秋季,日圓跌至 152 附近時,財務省首次自 1998 年以來動用「買入日圓」操作:9 月砸了 2.84 兆,10 月又追加了 6.34 兆,合計約 9.18 兆日圓。那輪干預短暫將 USD/JPY 從 152 壓回至 127 附近,但效果只維持了數月。

2024 年春季,USD/JPY 再度逼近 160 並一度突破,財務省出手約 9.80 兆日圓,是當時 2022 年以來的最大單輪操作,也是「自 2022 年以來首次確認買入干預」。

據日本財務省 2026 年 5 月 29 日公布的月度干預數據,此次 4 月 28 日至 5 月 27 日的操作規模為 11.7349 兆日圓(約合 736 億美元),是有記錄以來的最大單輪干預,超過 2022 年全年的干預總量,也比 2024 年春季足足多出近 2 兆日圓。

然而,就在財務省披露數字後不到一週,USD/JPY 仍然重新漲破了 160 關口。最大規模的干預,沒能完全守住這道心理關口。

外資買日股,追的是 AI,不是 carry 平倉帶來的避險資金

如果 carry trade 仍然擁擠,日經 225 為何還在創新高?

據路透社援引日本交易所集團(JPX)數據,截至 5 月 23 日當週,海外投資者已連續第 8 週淨買入日本股票,單週淨買入達 1.08 兆日圓。年內累計淨買入金額接近 11.7 兆日圓。

2025 年同期,外資累計淨買入不過 7421 億日圓。2026 年這個數字是它的 15.8 倍。

這筆資金的去向非常集中。同期漲幅靠前的個股中,AI 投資平台軟銀集團單週上漲 17.62%,晶片設計商 Socionext 上漲 12.26%。路透社的報導直接說明了買入動力:輝達(Nvidia)的業績展望提振了 AI 和半導體需求前景,外資藉日本市場追捧這條主線。

這與 2024 年 8 月「carry unwind 引發拋售」的邏輯截然相反。那次是被迫減倉、無差別拋售,資金從日本市場撤出。而 2026 年的外資淨買入,是主動選擇進入日本市場追逐 AI 再通膨行情。兩者的驅動機制不同,對日經指數的含義也不同。

加息不壓股市,但這對關係正在變得更脆弱

日經 225 的另一個反直覺之處,是它在 BOJ 連續加息的背景下持續上漲。

據日本銀行(BOJ)歷次政策決議公告,過去兩年的加息路徑如下:2024 年 3 月結束負利率政策,將政策利率從 -0.1% 上調至 0.1%;2024 年 7 月再度加息至 0.25%;2025 年 1 月加息至 0.5%;2025 年 12 月加息至 0.75%,這也是 1995 年以來的最高水準。2026 年 4 月會議維持 0.75% 不變,但以 6 比 3 的投票通過——三名委員(高田肇、田村直樹、中川純子)明確主張加息至 1.0%。

從圖中可以清晰看到:加息節點與日股走勢之間的相關性,在不同階段是完全不同的。2024 年 7 月那次加息,觸發了日經 225 單日跌幅 12.4% 的歷史性暴跌——那是因為 BOJ 加息和美國非農數據同時疊加,直接引爆了 carry unwind。但 2025 年 1 月和 12 月的兩次加息,伴隨的是日經 225 從 40,000 點附近一路爬升至如今的 68,634 點新高。

這背後的原因並不複雜:當外資買入的邏輯是追 AI 再通膨,而不是依賴日圓低利率融資成本時,BOJ 小幅加息對這部分資金的影響相當有限。當然,這對關係並非不變——如果 BOJ 7 月會議真的把利率推至 1.0%,同時美元因其他因素走弱,carry trade 的融資成本急劇上升,屆時兩條曲線的走向就可能重新耦合。

三張圖放在一起,可以得到一個相對完整的認知框架:日圓空頭仍然擁擠,財務省的歷史最大干預沒能守住 160,但日股新高的驅動是 AI 外資行情——這三件事同時為真,彼此並不矛盾,也沒有一件單獨能預測接下來會發生什麼。