Người muốn mua đã mua xong: Cơn sốt nhà đầu tư nhỏ lẻ của SpaceX hạ nhiệt, áp lực bán thực sự còn đến vào tháng 8

- Quan điểm chính: SpaceX (SPCX) sau khi niêm yết đã trải qua một đợt tăng giá chớp nhoáng do giới đầu tư nhỏ lẻ thúc đẩy, nhưng đà tăng nhanh chóng suy yếu. Dưới áp lực bán tháo và kỳ vọng cổ phiếu nội bộ hết hạn phong tỏa, giá cổ phiếu giảm ba ngày liên tiếp, xóa sạch toàn bộ mức tăng và quay về gần giá mở cửa. Thị trường cho rằng "những người muốn mua đã mua xong".

- Các yếu tố chính:

- Giá mở cửa của SpaceX trong ngày đầu niêm yết là 150 USD, sau đó tăng lên mức cao nhất mọi thời đại 225 USD trong vòng sáu ngày, vốn hóa thị trường một thời vượt qua Microsoft, nhưng dòng vốn hàng ngày của nhà đầu tư nhỏ lẻ đã sụp đổ sau khi đạt đỉnh vào ngày 16 tháng 6.

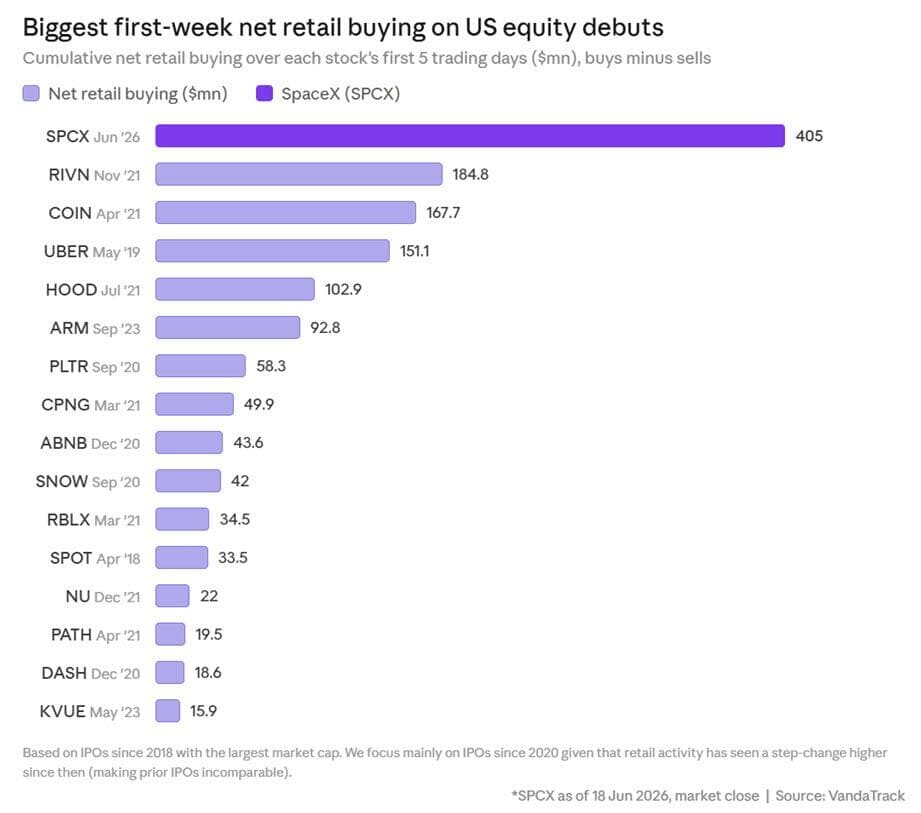

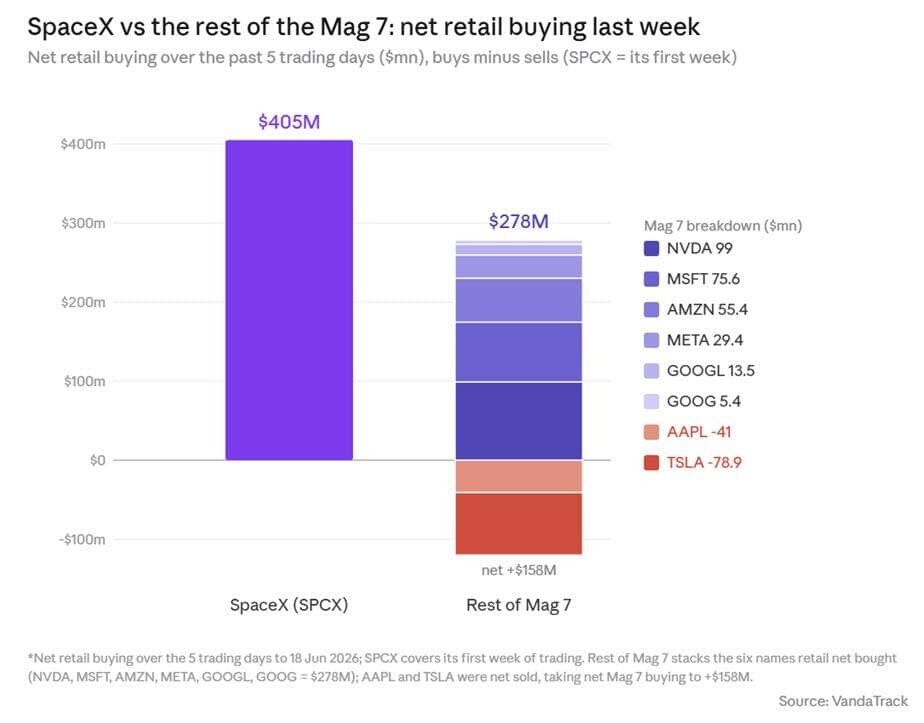

- Trong tuần đầu niêm yết, nhà đầu tư nhỏ lẻ đã mua ròng 405 triệu USD cổ phiếu SPCX, vượt qua tổng lượng mua ròng của nhà đầu tư nhỏ lẻ đối với tất cả các cổ phiếu thuộc nhóm Mag 7 (tổng cộng 278 triệu USD) và các ETF SPY và QQQ trong cùng kỳ.

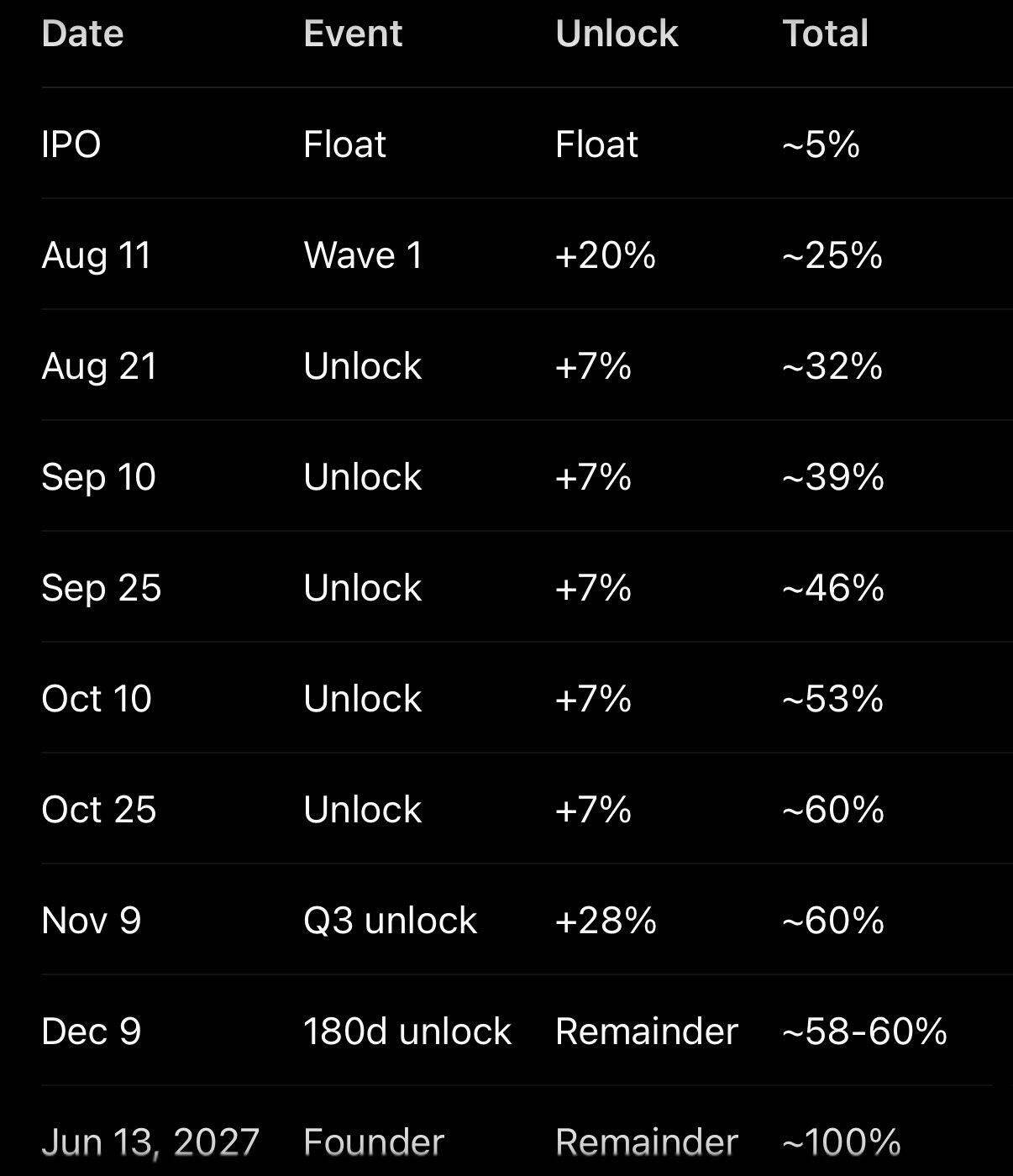

- Hiện tại chỉ có 5% lượng cổ phiếu lưu hành có thể giao dịch, nhưng cổ phần của nội bộ sẽ dần được mở khóa từ tháng 8 đến tháng 9. Đợt đầu tiên 20% được giải phóng sau báo cáo tài chính, và đến đầu tháng 9, có thể bán tối đa 44% cổ phần, mở rộng lượng cổ phiếu lưu hành thêm khoảng 900%.

- Dòng vốn nhà đầu tư nhỏ lẻ nhanh chóng đổ vào các sản phẩm đòn bẩy, như ETF 2x Long SPCX đã thu hút 65,8 triệu USD trong vài ngày đầu, nhưng nhu cầu sau đó thấp hơn nhiều so với mức điển hình của một cơn sốt.

- Sau khi đạt đỉnh vào ngày 16 tháng 6, giá cổ phiếu giảm ba ngày liên tiếp. Vào thứ Hai, giá đã giảm mạnh 16,4%, xóa sạch 600 tỷ USD vốn hóa thị trường. Sau giờ giao dịch, giá chạm mức mở cửa 150 USD, đe dọa tất cả những người mua ở thị trường thứ cấp.

- Các nhà phân tích cảnh báo rằng đà tăng hiện tại của thị trường chứng khoán Mỹ (đặc biệt là cổ phiếu công nghệ) phụ thuộc vào cơn sốt và đà tăng của nhà đầu tư nhỏ lẻ. Một khi nhà đầu tư nhỏ lẻ rút lui, áp lực bán tháo có thể lan sang các lĩnh vực lưu trữ và bán dẫn.

Original Author: Tyler Durden (ZeroHedge Anonymous Alias)

Original Translation: Source: ZeroHedge

Overview: SpaceX has fallen for three consecutive days, plunging 16.4% on Monday alone, wiping out $600 billion in market cap and sliding back to its $150 opening price. This analysis is straightforward: the people who wanted to buy have already bought, and more importantly, the real selling pressure hasn't arrived yet. This pump-and-dump scheme only utilized 5% of the circulating supply, with insiders potentially able to dump up to 44% of shares by early September.

It started with a bang. SpaceX went public on June 12, opening at $150 per share, well above its $135 IPO price. Within two days, aggressive traders began frenetically buying $380 call options expiring in two days, aiming to drive the stock price to the moon and create a gamma squeeze (where market makers are forced to buy the stock to hedge options, pushing the price higher).

@zerohedge tweeted: They're really going for it this time.

In a report this morning, Canaccord described the "new wave of optimism" accompanying the SpaceX IPO as follows:

"SPCX's order book shows the market has entered a new level of frenzy. Before this historic IPO, we thought AI optimism was already quite robust, sometimes even excessive, but buying was primarily from rational (albeit exuberant) institutions—large, well-capitalized public companies and PE investors. In our view, SPCX has opened a new chapter with a massive surge in retail participation, pushing the stock into the global top six by market cap, adding the equivalent of half a META in its first week of trading. Its market cap now far exceeds that of its sister company TSLA, while its revenue is only about 20% of TSLA's. Don't let the name SpaceX fool you; revenue is skewed towards its connectivity business—Starlink contributed $11.39 billion, launch services only $4.1 billion, and AI computing revenue was $3.2 billion in 2025."

VandaTrack was even more emphatic. In a review earlier Monday, it stated: "SpaceX's first week of trading was record-breaking. Retail investors net purchased $405 million in SPCX over the first five trading days, the strongest retail participation in an IPO in recent years. Buying was extremely aggressive in the first few days before cooling off later in the week. The flow increasingly looks like position-building for the long term, not chasing a short-term meme stock."

Chart: Retail Capital Flow for SPCX During the First Five Trading Days

Source: VandaTrack

The scale of retail buying for SPCX becomes even more staggering in context. Last week, retail purchases of SPCX exceeded their combined purchases of all other Magnificent 7 stocks—NVDA, MSFT, AMZN, META, GOOGL, and GOOG only saw $278 million in total retail inflows over those five days. SPCX's retail buying also surpassed the combined retail inflows for the SPY and QQQ ETFs during the same period ($352 million). A stock that just began trading last week is already competing with the market's largest individual stocks and ETFs for retail money.

Chart: SPCX Retail Buying vs. Mag 7 Individual Stock Retail Buying

Source: VandaTrack

The old playbook is playing out again. While individual stocks were being bought up, retail investors quickly surged into various SpaceX leveraged products, with demand equally strong. In the first few trading days, retail investors purchased $65.8 million in the Leverage Shares 2x Long SPCX Daily ETF – a significant number, but still far below typical levels seen during extreme speculative retail frenzies. Even so, it dwarfed recent thematic new issues: Roundhill's storage ETF (ticker DRAM) only attracted $5.6 million in its first four trading days, and it took DRAM 22 trading days for cumulative retail buying to match what the SpaceX leveraged ETF absorbed.

Chart: Retail Capital Flow Comparison: SPCX Leveraged ETF vs. Thematic ETFs

Source: VandaTrack

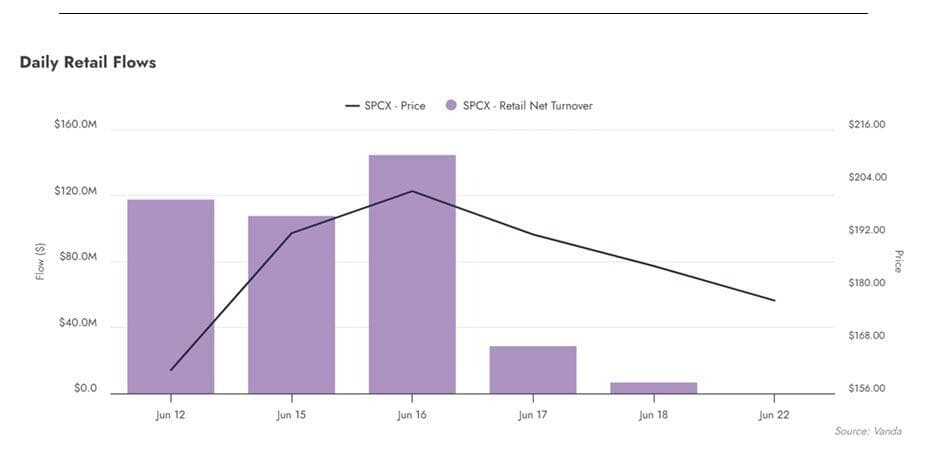

After the initial burst, momentum quickly faded, along with the fantasy of "riding a reusable rocket all the way into orbit via a gamma squeeze." June 16 was the peak, with SPCX hitting an all-time high of $225, briefly surpassing Microsoft in market cap. Since then, daily retail capital flows have collapsed, and retail turnover has nearly vanished.

Chart: SPCX Retail Daily Capital Flow – Cliff-like Decline After June 16 Peak

Source: VandaTrack

This brings us back to Canaccord's point. Based on SpaceX's early trajectory, the investment bank judged that "tech stocks can likely sustain momentum in the near term," but it also warned: "There is now a more dangerous vacuum beneath these stocks."

Sure enough, once momentum dissipated, coupled with the market realizing trillions of shares were about to unlock, the stock fell for three consecutive days, culminating in a crash on Monday. That day, as SpaceX attempted to issue over $20 billion in investment-grade bonds for the first time—taking advantage of the still-exuberant bond market before the issuance window closed, aiming to refinance a much higher-interest bridge loan—SPCX plummeted 16.4%, wiping out a record $600 billion in market cap in a single day. Adding the 5% drop on Wednesday and 3.5% drop on Thursday, the stock is now only slightly above its $150 opening price from two weeks ago.

Chart: SPCX Price Action Since Listing – Falling Back Near $150 from $225 High

Source: ZeroHedge

Worse still, SPCX touched its $150 IPO opening price in after-hours trading. If it breaks below that level at the open tomorrow, everyone who bought and held in the secondary market will be underwater.

Chart: SPCX Drops Near $150 IPO Opening Price in After-Hours Trading

Source: ZeroHedge

What's particularly noteworthy is that this pump-and-dump occurred with only 5% of the float available for trading – 95% of the stock is still locked up. But this is about to change.

Chart: SPCX Lockup Structure – Only 5% Currently in Float, 95% Locked

Source: ZeroHedge

Jeff Jacobson, a strategist at 22V Research, stated that after SpaceX reports earnings between early and mid-August, 20% of insider shares will unlock. Additionally, if the stock price is 30% above the IPO price, it triggers another 10% unlock. There are also 7% unlocks around August 21 and September 10.

Chart: SPCX Lockup Expiration Schedule

Source: 22V Research

Jacobson said insiders could potentially sell up to 44% of their SpaceX shares by early September, expanding the current float by approximately 900%.

In other words, it will only get harder to push the stock price up from here. Meanwhile, Michael O'Rourke, Chief Market Strategist at JonesTrading, said "the sellers have regained control," adding: "Everyone in the world who wanted to buy has already bought."

Commenting on today's decline, Bloomberg wrote that SpaceX's drop "dragged most of the market down with it."

Whether that's entirely true remains debatable. But in this market—which has risen from the March lows almost entirely propped up by retail frenzy and momentum chasing—if retail investors truly get spooked, first SpaceX, then the storage bubble, and finally the semiconductor stocks that have feasted on the AI trade...

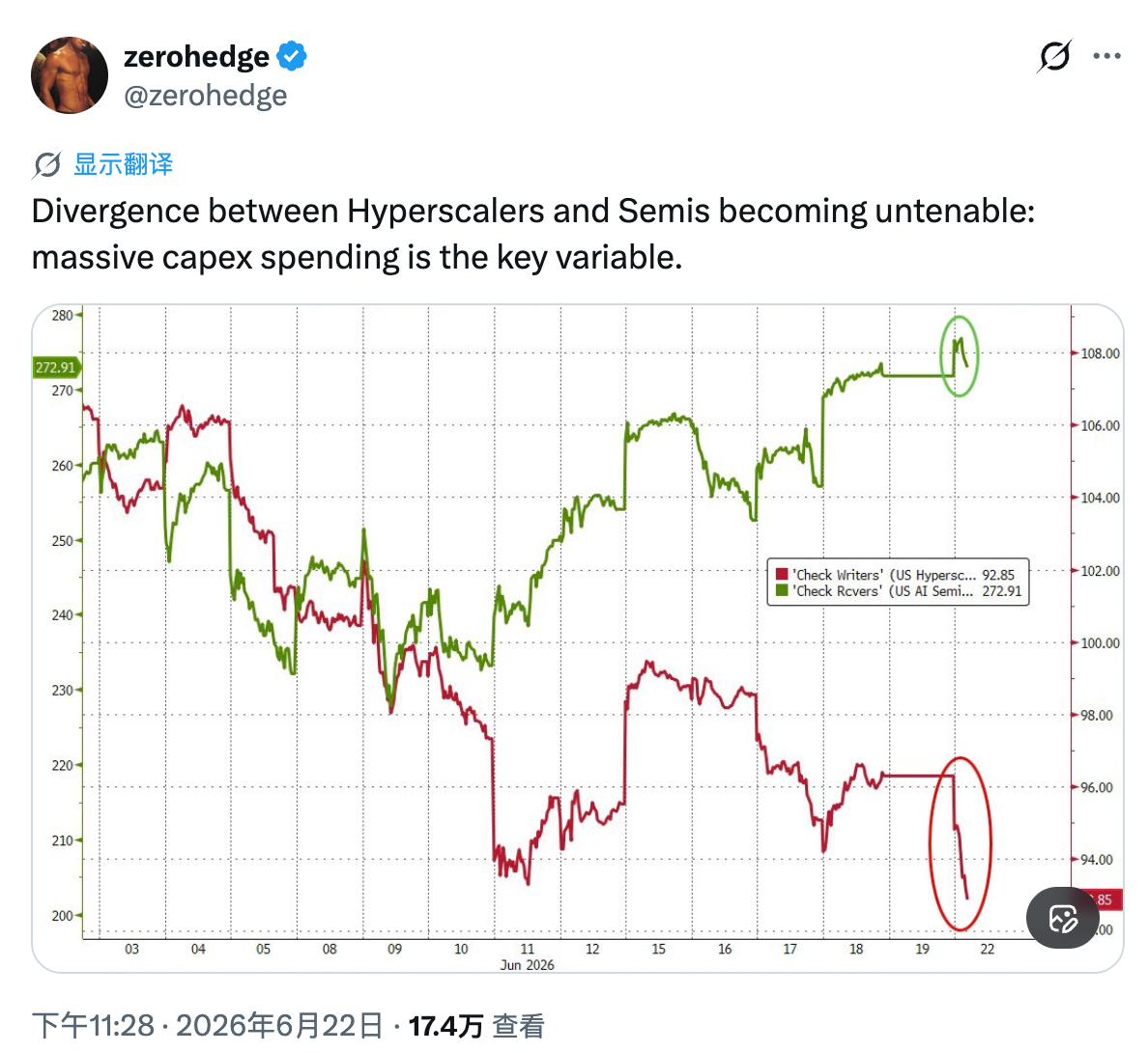

@zerohedge tweeted: The divergence between hyperscalers and semiconductors is unsustainable: massive CapEx is the key variable.

...then, it will be time to invert T.S. Eliot's line: This is not how the sell-off ends, but with a bang.