Một bài đọc hiểu: Tất cả các mắt xích truyền dẫn và cổ phiếu ngành liên quan đến tình trạng thiếu khí đốt tự nhiên toàn cầu

- Quan điểm cốt lõi: Cuộc xung đột quân sự ở Trung Đông vào cuối tháng 2 năm 2026, thông qua bốn chuỗi truyền dẫn chính là khí đốt tự nhiên - phân bón - heli - chip, đã biến cú sốc năng lượng cục bộ thành một bài kiểm tra áp lực có hệ thống đối với chuỗi công nghiệp toàn cầu, cuối cùng thúc đẩy sự phân hóa giá trị giữa chip AI và điện tử tiêu dùng trong nội bộ cổ phiếu công nghệ.

- Các yếu tố then chốt:

- Khoảng 17% công suất LNG của Qatar bị ảnh hưởng, với sản lượng 12,8 triệu tấn hàng năm bị ngừng sản xuất, chu kỳ khôi phục từ 3-5 năm, kết hợp với việc eo biển Hormuz bị tắc nghẽn, giá giao ngay LNG châu Á đã tăng từ 10 USD/triệu đơn vị nhiệt Anh lên hơn 25 USD.

- Khí đốt tự nhiên là nguyên liệu đầu vào cho amoniac tổng hợp và urê; xung đột đã khiến nhà máy sản xuất 5,6 triệu tấn urê của QAFCO phải ngừng hoạt động. Khoảng 30% thương mại phân bón toàn cầu vào năm 2024 được vận chuyển qua eo biển Hormuz.

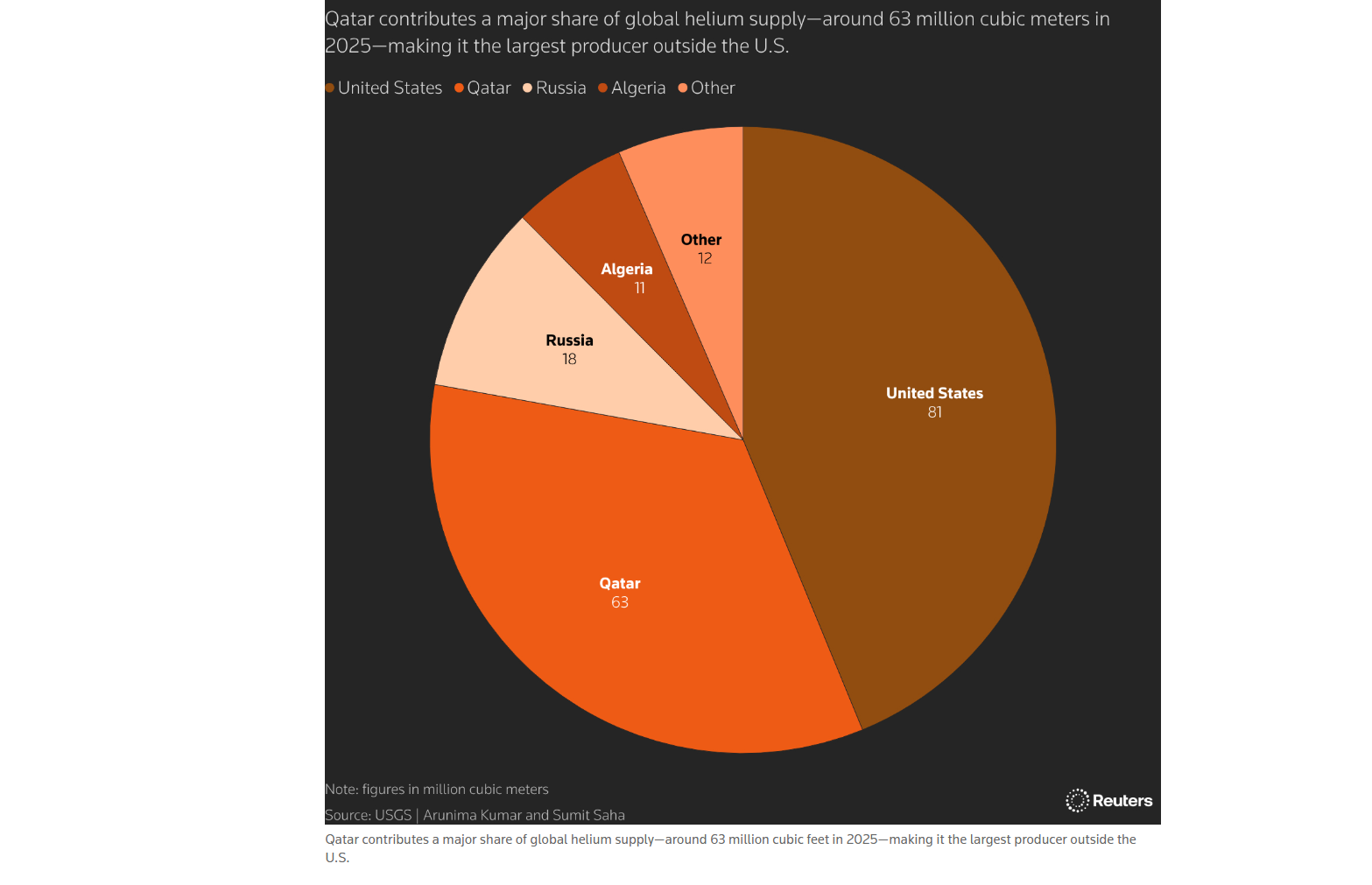

- Qatar cung cấm gần một phần ba nguồn heli toàn cầu, một vật liệu quan trọng cho hệ thống làm mát wafer và chân không trong sản xuất chất bán dẫn. Sự gián đoạn nguồn cung sẽ tác động mang tính cấu trúc đến công suất sản xuất chip tiên tiến.

- Trong bối cảnh công suất hạn chế, các nhà sản xuất ưu tiên đảm bảo các đơn hàng chip AI có biên lợi nhuận cao. Cuộc đua sức mạnh tính toán của các nhà cung cấp dịch vụ đám mây vẫn không đổi, trong khi điện tử tiêu dùng (PC, điện thoại) phải chịu chi phí tăng và áp lực công suất.

- Sau khi xung đột kéo dài đến tháng 5, các chuỗi năng lượng, phân bón và chip sẽ chuyển từ tác động về giá sang các ràng buộc công suất thực tế, kích hoạt sự tái cân bằng chuỗi công nghiệp toàn cầu.

Original author: Frank, Meitong MSX

Many people did not expect that a military conflict in the Middle East would ultimately cascade through multiple links such as natural gas, fertilizers, helium, semiconductors, and consumer electronics, turning into a systemic stress test spanning dozens of industries.

At the end of February 2026, the US and Israel launched military strikes against Iran, which subsequently restricted passage through the Strait of Hormuz, forcing one of the most critical global energy transport chokepoints into a semi-frozen state. Shortly after, Qatar's largest natural gas facility, Ras Laffan Industrial City, was repeatedly attacked, shutting down one of the world's most important LNG production and export hubs.

According to Reuters, approximately 17% of Qatar's LNG export capacity was damaged, leading to an annual stoppage of 12.8 million tons of LNG production, with repair times for some facilities potentially taking 3 to 5 years.

Superficially, this appears to be an energy event of "rising natural gas prices."

But what truly deserves attention is that natural gas is not just fuel for power generation and heating. It is also the upstream input for several key industrial products, including ammonia, urea, methanol, hydrogen, and helium. Once this input path is blocked, the transmission chain spreads from the energy market to agriculture, food inflation, semiconductor manufacturing, and finally culminates in the valuation divergence of tech stocks.

This is the core logic this article aims to deconstruct layer by layer: this crisis is not a single-point impact but a continuous transmission across four chains — Natural gas prices → Energy sector; Natural gas → Ammonia → Fertilizer & Agriculture; Helium supply disruption → Chip manufacturing; AI chips vs. Consumer electronics → Tech stock divergence.

I. Natural Gas Prices: The 'First Shockwave' for the Energy Sector

The first sector to be breached was the global natural gas market.

The combination of Qatar's LNG production halt and the restricted Strait of Hormuz effectively pulled two fuses simultaneously from the global natural gas supply side. On one hand, Qatar is one of the most important exporters in the global LNG supply system. On the other hand, the Strait of Hormuz is a key passage for its LNG exports. With both production and transport restricted simultaneously, a sharp spike in natural gas prices was almost inevitable.

From a market performance perspective, Asian LNG spot prices rapidly surged from above ~$10/MMBtu before the conflict to over $25/MMBtu. Although they have since retreated somewhat, they remain significantly above pre-war levels. European TTF prices were also impacted, with Goldman Sachs maintaining its Q2 TTF forecast around €63/MWh, noting that if Qatari supply cannot be restored by early May, prices may need to rise further to suppress demand.

The beneficiaries of this chain are very direct. Non-Middle East LNG exporters, primarily the US, and energy companies with stable production capacity and export capabilities will undoubtedly be the biggest winners from replacement supply. For instance, MSX has listed OXY.M, XOM.M, CVX.M, corresponding respectively to Occidental Petroleum (a long-term Buffett holding), ExxonMobil (the global integrated oil & gas leader), and Chevron (with both US shale gas and global LNG export capabilities).

However, the losers are equally clear. Asian economies heavily reliant on LNG imports are the first to be affected, especially South Korea, Japan, Singapore, Taiwan, and some South Asian countries. This explains why rising energy prices won't just stop at the profit statements of oil and gas companies.

For importing countries, higher LNG prices mean higher power generation costs, higher industrial production costs, and increased pressure on residential electricity prices. This ultimately extends the tail of inflation. For capital markets, this compresses rate cut expectations and puts higher discount rate pressure on high-valuation growth sectors.

In other words, natural gas is the first shockwave, but it is never the final link.

II. Natural Gas → Ammonia → Fertilizer: The Overlooked Agricultural Chain

The second transmission chain is more subtle but hits closer to home, directly affecting the "rice bowls" of 8 billion people globally.

Why does rising natural gas prices affect food? The logic is not complicated: Natural gas is a crucial raw material for ammonia production; ammonia is the basis for urea and nitrogen fertilizers; nitrogen fertilizers directly impact global crop planting costs. Therefore, when natural gas supply tightens and prices rise, fertilizer production costs rise concurrently. And when the Strait of Hormuz is blocked, fertilizer exports from the Middle East face further logistical constraints.

This has been starkly evident in the current conflict. CRU Group pointed out that Middle East tensions have exacerbated uncertainty in urea supply. After QatarEnergy stopped LNG and related product production in early March, QAFCO's 5.6 million tons/year urea plant in Mesaieed was also affected, becoming the first confirmed fertilizer production casualty of this conflict.

Data from IFPRI further illustrates the severity: in 2024, up to ~30% of global fertilizer trade needed to pass through the Strait of Hormuz. Simultaneously, about 20% of LNG and 27% of globally traded crude oil also transit this strait. This means Hormuz is not just an oil and gas passage; it's also a critical corridor for global agricultural inputs.

The danger of this chain lies in its close coupling with the agricultural season. While energy prices can react quickly in futures markets, the impact of fertilizer shortages on crops has a specific window. It's crucial to remember that once the critical fertilization stage is missed during the Northern Hemisphere spring planting season, even if supply recovers later, it's very difficult to fully compensate for the earlier losses. This implies that the impact of this crisis on food prices might not be fully reflected in the current month's CPI but will be released gradually over several months through crop yields, agricultural product prices, and food processing costs.

However, the difficulty with the fertilizer chain is that a single fertilizer company often struggles to fully cover the complex transmission pathway between natural gas, ammonia, urea, agricultural products, and basic materials. Therefore, ETF tokens are better suited to capture these medium-to-long-term logics. For example, MSX has listed FTAG.M, MOO.M, XLB.M, corresponding to the global agricultural industry chain, global agricultural leaders, and the US basic materials sector respectively:

•FTAG.M leans towards a "basket of agricultural inputs" tool, covering fertilizers, pesticides, seeds, and machinery.

•MOO.M focuses more on global agricultural production, processing, and equipment leaders, suitable for observing the transmission of rising planting costs to agricultural product prices.

•XLB.M covers basic industrial sectors like chemicals, materials, metals, and construction, including companies like Linde and Sherwin-Williams that are significantly impacted by inflation and industrial costs.

In other words, if fertilizer price increases form a long chain from energy to food, these ETF tokens offer not a bet on a single company, but a portfolio approach to capture the re-pricing opportunity across the entire agricultural inputs chain.

III. Helium: The Systemic Risk Most Overlooked

This is the most underestimated link in the entire transmission chain, but potentially the one with the most profound impact.

If the fertilizer chain connects to food, the helium chain connects to chips.

Many might wonder: why does a natural gas plant shutdown affect semiconductors? The answer lies in the fact that helium is a vital byproduct of natural gas processing and cannot be produced on a large scale through chemical synthesis. Qatar has long been a major global source of helium supply. Reuters, citing the US Geological Survey, notes that Qatar produces nearly one-third of the world's helium supply. Following the current Middle East conflict, tightening helium supply has already begun to impact the global tech industry chain.

Helium is nearly irreplaceable in semiconductor manufacturing. It is used for wafer cooling, vacuum system leak detection, inert atmosphere control, and some precision manufacturing steps. For advanced process nodes, temperature stability, cleanliness, and process consistency are paramount, and helium is one of the fundamental materials supporting these conditions.

Once supply becomes unstable, chip fabs can buffer for a short time using inventories and recycling systems. However, if the shortage persists for months, production line scheduling, material prioritization, and customer delivery schedules will be forced to adjust.

More concerningly, helium is not as easily stockpiled on a large scale as crude oil. It is one of the smallest monatomic gases, difficult to store and transport. Liquid helium transport relies on specialized cryogenic equipment. This explains why this crisis's impact on semiconductors is not a simple "bearish for chip stocks" scenario but a more nuanced structural shock.

Among these, MSX has listed DRAM.M, TSM.M, and MU.M, which correspond to several key observation points along this chain:

•DRAM.M is the world's first pure-play memory ETF token, covering memory leaders like Samsung, SK Hynix, and Micron. It can be used to observe supply-demand dynamics for segments like HBM, DRAM, and NAND in the AI era.

•TSM.M (TSMC) corresponds to TSMC, the core node for global advanced process foundry and a key manufacturer for end-user chips like NVIDIA, AMD, and Apple.

•MU.M (Micron Technology) corresponds to US memory chip leader Micron, with exposure across DRAM, NAND, and HBM. It also benefits more from the restructuring of the US domestic supply chain compared to Korean players.

Ultimately, the helium shortage truly triggers a larger proposition: the global semiconductor supply chain depends not only on EUV, EDA, advanced packaging, and high-end equipment but also on industrial gases, chemicals, transport tanks, and regional energy security – factors often overlooked by capital markets.

This is precisely what is most easily underestimated about this crisis. It serves as a reminder not just that "chips are important," but that the construction of AI-era computing power rests upon an extremely long, extremely fragile, and highly globalized physical supply chain.

IV. AI Chips vs. Consumer Electronics: The Real Divergence Begins

When helium shortages, energy price hikes, and material transport delays cascade down to the semiconductor manufacturing end, the easiest mistake the market can make is to paint all tech assets with the same brush.

Reality, however, is quite the opposite. This shock will not cause the tech sector to simply decline collectively; it will drive further divergence within tech stocks.

AI chips will certainly face pressure in the short term, as advanced process manufacturing heavily relies on a stable supply of high-purity gases, lithography materials, packaging capacity, and energy. The supply chain requirements for HBM, GPUs, and AI servers are significantly more complex. Once upstream materials become tight, AI chip delivery cycles may lengthen, potentially causing temporary hiccups in the capital expenditure pace of some cloud vendors and server manufacturers.

But from a demand perspective, the rigidity of demand for AI chips is significantly stronger than for consumer electronics. The computing power race among cloud vendors, model companies, and enterprise clients is far from over. AI infrastructure remains one of the most certain directions for tech capital expenditure. Therefore, in a scenario of limited capacity, the manufacturing side is more likely to prioritize high-margin, high-strategic-value AI chip orders over low-profit, price-sensitive consumer electronics orders.

The ones truly under pressure might instead be end-market consumer electronics like PCs, phones, and tablets. This means the core contradiction in this tech chain is not "will AI continue to grow," but "who gets priority allocation for limited advanced capacity, memory capacity, and critical materials":

•NVDA.M (NVIDIA) remains the absolute AI chip leader; AMD.M (Advanced Micro Devices) is the second-largest AI chip designer; AVGO.M (Broadcom) spans both AI ASICs and networking chips.

•MSFT.M (Microsoft), GOOGL.M (Google), and AMZN.M (Amazon) correspond to AI infrastructure and cloud computing demand, representing three paths: Azure + OpenAI, TPU self-development + Cloud, and AWS global cloud services.

•In contrast, AAPL.M (Apple) and DELL.M (Dell Technologies) are more susceptible to fluctuations in consumer electronics, PCs, server hardware costs, and end-market demand, with a clearer pressure logic.

•As for 3x leveraged semiconductor ETF tokens like SOXL.M and SOXS.M, they are better suited for expressing short-term sentiment and sector volatility rather than long-term allocation logic.

In other words, even within the same "tech assets" category, the risk-reward structures of AI chips, cloud infrastructure, consumer electronics, and leveraged ETF tokens are completely different. The true test of this crisis is whether investors can look beyond the broad "tech" label and dissect the more granular industrial chain positions.

For investors, what's truly worth capturing is not simply betting for or against tech stocks, but re-identifying *within* tech stocks who holds pricing power, who has supply priority, and who can only passively bear the burden of rising costs.

Final Thoughts

Returning to the core thesis at the beginning of this article, this roughly 60-day Middle East crisis has cascaded from natural gas all the way to AI chips. The transmission chain is far longer and more complex than it appears on the surface.

After all, the foundation of the global supply chain is not abstract financial models but energy, shipping lanes, minerals, gases, chemicals, equipment, and transport capacity. In recent years, the market has grown accustomed to understanding the tech cycle through grand concepts like "AI," "computing power," and "globalization." However, this crisis reminds us that