孙宇晨看好的核能赛道,悄悄开启上市潮

- ประเด็นหลัก: ความกังวลเรื่องความต้องการไฟฟ้าที่เพิ่มขึ้นจากการขยายตัวของพลังประมวลผล AI กำลังผลักดันให้เงินทุนเข้าสู่ "แหล่งพลังงานระยะยาว" เช่น พลังงานนิวเคลียร์และนิวเคลียร์ฟิวชันล่วงหน้า ซึ่งคุณค่าของมันไม่ได้มาจากความก้าวหน้าทางเทคโนโลยีอีกต่อไป แต่มาจากความสามารถในการผูกขาดเชิงกลยุทธ์ในการมอบ "สิทธิ์ในการขยายพลังประมวลผล" ให้กับศูนย์ข้อมูลในอนาคต

- องค์ประกอบสำคัญ:

- ไฟฟ้ากลายเป็นคอขวดของ AI: ศูนย์ข้อมูลขาดแคลนไฟฟ้า พลังงานลมและแสงอาทิตย์ไม่เสถียร โรงไฟฟ้านิวเคลียร์แบบดั้งเดิมใช้เวลาก่อสร้างนานเกินไป บริษัทเทคโนโลยียักษ์ใหญ่ (เช่น Amazon) เริ่มจองกำลังการผลิตของเครื่องปฏิกรณ์นิวเคลียร์แบบโมดูลาร์ขนาดเล็ก (SMR) ล่วงหน้าด้วยการทำข้อตกลงจัดหาพลังงานระยะยาว

- เงินทุนเดิมพันระยะยาว: หุ้น General Fusion ปิดตัววันแรกพุ่ง 38% วางแผนสร้างเครื่องปฏิกรณ์ภายในปี 2035; X-energy เปิดตัวขาดทุนแต่มูลค่าตลาด 9.1 พันล้านดอลลาร์ ต้องขอบคุณคำสั่งซื้อจาก Amazon ตลาดกำลังซื้อขาย "ใบจอง" ไม่ใช่สถานีไฟฟ้าที่ผลิตไฟฟ้าได้แล้ว

- ผลกระทบต่อห่วงโซ่อุปทาน: ความกังวลเรื่องการใช้ไฟฟ้าของ AI ส่งผ่านจากผู้พัฒนาเครื่องปฏิกรณ์ไปยังผู้ผลิตเชื้อเพลิง TRISO (เช่น Standard Nuclear), ผู้ผลิตยูเรเนียมสมรรถนะสูงเสริมสมรรถนะต่ำ (เช่น Centrus) และบริษัทเหมืองยูเรเนียม (เช่น Eagle Energy Metals) ทำให้ห่วงโซ่อุปทานต้นน้ำของนิวเคลียร์ทั้งหมดได้รับความสนใจ

- นิวเคลียร์เชื่อมโยงกับ AI: ในอดีต พลังงานนิวเคลียร์ขายเรื่องคาร์บอนต่ำและความปลอดภัย ปัจจุบันขายเรื่อง "สิทธิ์ในการขยายพลังประมวลผล" ผู้มีชื่อเสียงอย่างซุน อี้เชียน และซุน จิ้งจี ต่างชี้ว่าปลายทางของพลังงาน AI คือนิวเคลียร์ฟิวชัน ซึ่งเป็นสัญญาณของการเปลี่ยนผ่านในบริบทของอุตสาหกรรม

- เปรียบเทียบกับวิกฤติน้ำมัน: ความต้องการไฟฟ้าของ AI กำลังเปลี่ยนไฟฟ้าจากสินค้าโภคภัณฑ์ที่ "เสียบปลั๊กก็ใช้ได้" ไปเป็นทรัพยากรเชิงกลยุทธ์ที่ต้องวางแผนล่วงหน้าหลายปี คล้ายกับการเปลี่ยนแปลงบทบาทของน้ำมันหลังปี 1973

For a period last year, the market was buzzing with rumors that Justin Sun had bought a power plant in Norway.

To understand his logic, I dug through his old YouTube videos and found him saying, "If you missed out on Nvidia, you can look further down the line, like electricity, like nuclear fusion." He later put it even more bluntly: the endgame of AI is energy, and nuclear fusion is a long-term trend worth watching in the AI era.

Back then, the term "nuclear fusion" felt too distant, and the AI hype was nowhere near as intense as it is now, so the market largely ignored it.

On July 14th, Asia's richest man, Masayoshi Son, talked about AI. He didn't start with chips. He also talked about nuclear fusion.

The SoftBank founder said that within fifteen years, nuclear fusion could power AI data centers, gradually replacing natural gas. As usual, he dismissed the "AI bubble" and urged Japan not to sit on the sidelines of this wave.

Two individuals, from vastly different businesses and contexts, operating from perspectives few can grasp, both fixed their sights on the same machine that doesn't yet exist.

Data centers are running out of power.

Fusion Isn't Generating Power Yet, but General Fusion Has Already Rallied

On July 13th, Canadian fusion company General Fusion listed on the Nasdaq via a merger with a SPAC, under the ticker GFUZ. It became the world's first publicly traded pure-play fusion energy company.

On its first day of trading, the stock price surged, closing up about 38%.

General Fusion holds roughly $150 million in cash, which the company expects will fund operations until 2028. They hope to build their first commercial fusion reactor around 2035.

In other words, what the market traded that day wasn't a power plant already generating electricity.

It was a ticket for nine years from now.

The fusion business has a cruel aspect. Scientific experiments can be measured in seconds of plasma stability, a single materials test, or a device parameter; capital markets lack that patience. They always ask, when will the electricity be sold, who will buy it, and will the numbers add up?

In the past, fusion companies gave grand answers.

Clean energy. Artificial suns. Infinite fuel. Humanity's ultimate energy source.

These words are all correct, but they are far from a balance sheet.

Now, someone has added a more down-to-earth line.

AI companies need electricity.

Suddenly, a company planning to build a commercial reactor by 2035 has a tangible future customer profile. Not some vague utility company, but rows of AI data centers, already burning cash to build up, waiting to be connected to the grid.

The attitude of money changes fast.

According to the latest statistics from the Fusion Industry Association, global investment in the fusion industry over the past year reached a record $4.48 billion. This figure is based on the industry body's own methodology and isn't definitive proof that fusion has won.

But it at least shows one thing.

The number of people willing to pay a deposit for "electricity far in the future" has suddenly increased.

When X-energy Went Public, the Market Had Already Changed Its Algorithm

General Fusion is just the furthest-out ticket.

A closer ticket is X-energy.

This advanced nuclear energy company attempted to go public via a SPAC in 2023 but didn't succeed. Back then, people looked at it much like someone claiming they were building a rocket. The project was huge, the timeline long, but the financial statements were on the table, impossible to ignore.

Three years later, X-energy returned with an IPO.

In April this year, the company raised approximately $10.2 billion, with an issue valuation of around $9.1 billion. It closed up about 27% on its first day of trading. Its 2025 revenue was roughly $109 million, with a net loss of about $390 million.

Looking at these numbers alone, it doesn't look great.

But it also has Amazon.

Amazon's collaboration with X-energy aims to help deploy up to 5GW of small modular reactor capacity by 2039.

It's not just Amazon. Google has also partnered with Kairos Power to reserve a spot for nuclear power.

These partnerships are still far from actual power plants being built. Approvals can be delayed, projects can change, and options don't equal revenue. Treating them directly as future income is like mistaking a reservation order for an invoice.

But in the capital market, a reservation has its own value.

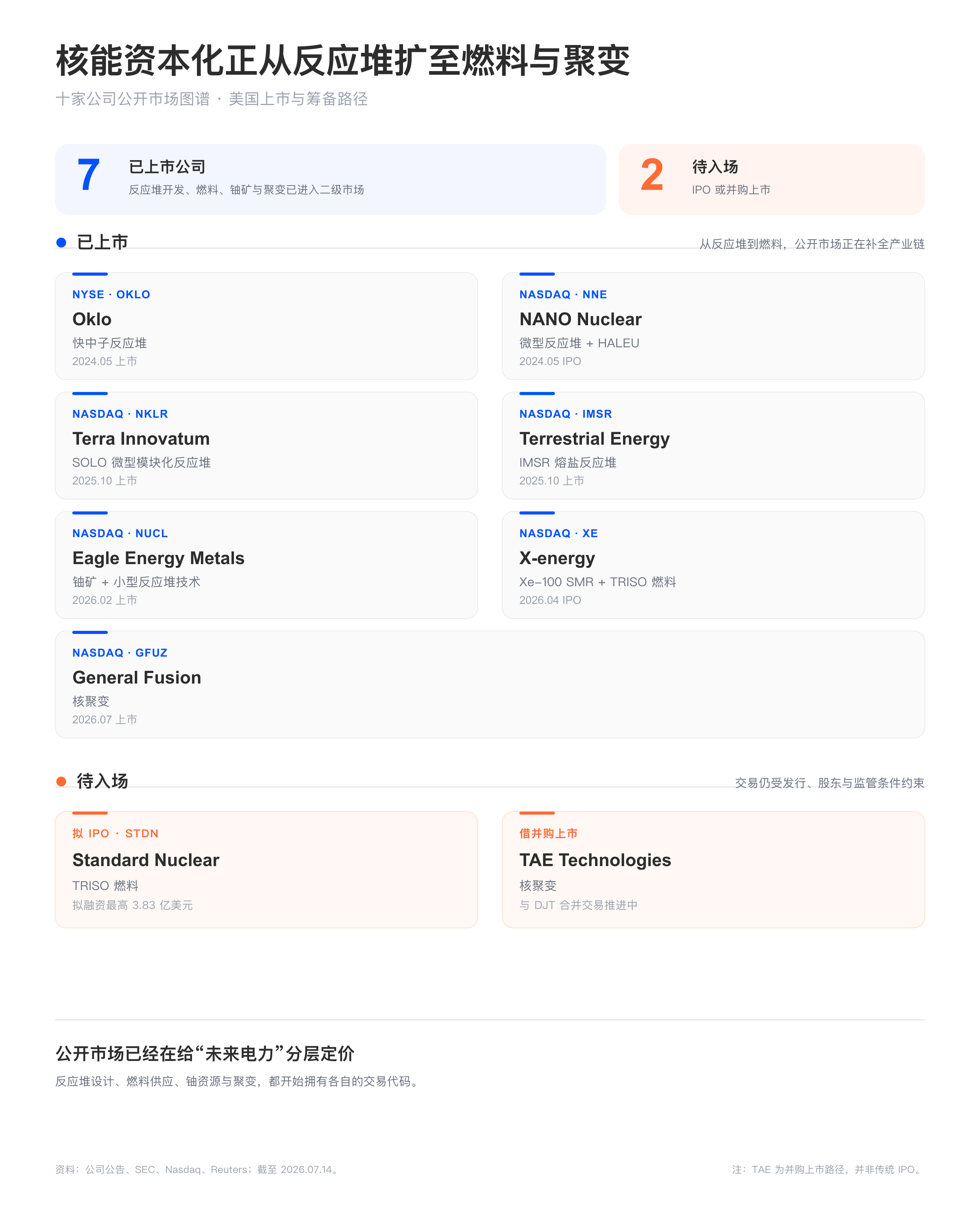

Looking at the timeline, you'll see that the nuclear energy sector has seen a wave of listings in a short time. Oklo, Terra Innovatum, Terrestrial Energy, and X-energy have brought reactor developers to exchanges; Eagle Energy Metals has capitalized on both uranium mining and small reactor technology; Standard Nuclear has led the market all the way to TRISO fuel. General Fusion and TAE have brought even the most distant fusion stories to the doorstep of public markets.

In the past, nuclear energy companies sold low carbon, stability, and energy security.

Today, they are selling something else.

The right to expand computing power.

Secure the Power First, Then Keep Stacking Chips in the Data Center

Why would data centers push such a slow technology to the forefront?

Because even if chips are expensive, you can order them.

Electricity is different.

Servers can be purchased in advance, shipped to a construction site, and stored in a warehouse. If GPUs are scarce, Nvidia can ramp up production, AMD can follow, and customers can upgrade. Electricity doesn't work that way. It requires power generation first, then transmission, then substations, then nods of approval from local governments, regulators, grid companies, and communities.

The biggest fear for AI companies isn't the price of electricity.

It's building the server room and not being able to connect to the grid.

A large data center园区 runs 24/7, machines generate heat, and cooling systems generate heat too. When training models, thousands of chips work simultaneously. You can't tell a client, "The wind is low today, the model will answer your questions tomorrow."

Wind and solar are certainly important, but they depend on the weather. Gas turbines are flexible enough but come with old problems of fuel, emissions, and supply. Large traditional nuclear plants are stable, but their construction timelines can try the patience of any internet company.

SMRs, or Small Modular Reactors, fit right in the middle.

They promise to make nuclear plants smaller, more standardized, deployable in parts, and scalable over time. This promise hasn't yet been tested by large-scale commercial operation, but it suits the temperament of data centers perfectly.

They don't want to wait for a giant power plant to be built.

They are willing to take a number and wait their turn.

The long-term procurement arrangements signed by tech giants like Amazon and Google are, in essence, ways to queue up for future power capacity. They aren't just buying a unit of electricity; they are reserving a plug-in for their own future expansion.

This brings something far more valuable to nuclear energy companies than a technical white paper.

Data Centers Trail the Problem All the Way to the Mine

When the "need for power" first surfaced, capital initially saw reactors.

Companies like Oklo, X-energy, Terrestrial Energy, and Terra Innovatum were thus pushed to the front. They all sell next-generation reactors that are still under development. Some work on fast neutron reactors, some on molten salt reactors, some on SMRs.

SMRs are Small Modular Reactors. They break down large nuclear plants, traditionally built on a city scale, into smaller pieces, aiming for repeatable manufacturing and phased deployment. Data centers like this because they also don't want to wait for a mega reactor to slowly come online.

But once reactors are actually penciled into project plans, problems cascade down the line.

What fuel does this machine consume?

X-energy's Xe-100 needs TRISO fuel. TRISO sounds like a lab acronym, but it can be understood as a tiny nuclear fuel kernel encased in several layers of ceramic material. It must withstand high temperatures and last long enough in the reactor. No matter how beautiful the reactor design diagram is, without this fuel, it remains stuck on a computer. This is exactly what Standard Nuclear does.

So Standard Nuclear's IPO preparation is no longer just a story about a fuel company.

What it sells is quite unassuming. There are no lights from a reactor launch party, no massive data center orders, no grand fifteen-year predictions from Masayoshi Son. But when the market starts believing that advanced reactors will be built, people will eventually ask who can deliver the fuel to their doorstep on time.

Going further back, the fuel itself becomes a bottleneck.

Some advanced reactors require HALEU, or High-Assay Low-Enriched Uranium. Its enrichment level is higher than the fuel commonly used in traditional nuclear plants but far below weapons-grade material. The name is long, but the logic is simple. New machines need a different grade of fuel, which isn't available in old stockpiles, and there aren't many facilities to produce it.

Companies like Centrus are therefore being re-evaluated.

The questions don't stop there.

Where does HALEU come from? Where does the uranium come from? This is how companies like Eagle Energy Metals, which hold both uranium mining assets and small reactor technology, can enter the public market along the same line. The mines, once furthest removed from AI, are now illuminated by the data center's hunger for power.

This wave of listings isn't due to the nuclear industry suddenly falling in love with Wall Street.

It's more like data centers laid a power order on the table, then traced back along that order. First, check who can build the reactor. Once built, check who has the fuel. If fuel is insufficient, check who can enrich uranium, and who owns the mines.

Every step up the supply chain runs into a bottleneck that can't be solved with overtime work.

Approvals can be expedited. Models can be iterated. Servers can be reordered. Fuel production lines and uranium mines don't care about any of this.

So now, the market is no longer just asking which company has a good reactor design. They start asking which link in the chain will cause the reactor to generate power a year late.

After 1973, Oil Was No Longer Just Oil

Before the 1973 oil crisis, oil was already crucial.

Cars ran on it, factories relied on it, airplanes used it. But what suddenly made governments across the world nervous wasn't the discovery that oil could burn, but the realization that they had little control over a long, fragile supply chain.

Oil wells were far away. Oil tankers were at sea. Pipelines crossed borders. Prices were set by others.

From then on, oil was no longer just a commodity. It became entangled with diplomacy, strategic reserves, warfare, and industrial policy.

AI is making electricity travel a similar path.

Electricity was once too ordinary. Plug it in, the lights turn on, the computer runs. Because it was so ordinary, few people ever seriously thought about where it came from.

Until a group of companies started planning to multiply their computing power tenfold, a hundredfold.

That's when they discovered that electricity also has a geographic location, a queue to get in, and a construction cycle. It's not just a hole in the wall, but a path that needs to be booked many years in advance.

Masayoshi Son talks about fifteen years, Justin Sun says nuclear fusion is the next stop, General Fusion surged on its first trading day, and X-energy presents both its losses and high valuation to the market.

Put together, these events don't prove that fusion has arrived.

They only prove that a growing number of people are starting to worry that, by the time it does arrive, they might have missed their spot in line.