Goldman Sachs Calls for $610: Microsoft's AI Story Rests Entirely on Azure's Performance

- Core Thesis: Goldman Sachs maintains a Buy rating and a $610 price target ahead of Microsoft's earnings, viewing Azure growth and returns on AI investment as the market's focal points. Against a backdrop of rising capital expenditure, investors need to verify whether higher spending can convert into actual revenue and profit, rather than just weighing on cash flow.

- Key Elements:

- Azure Growth Remains the Main Theme: Goldman Sachs expects Azure to grow 40%-41% on a constant currency basis in Q4, slightly above the company's guidance. The market already anticipates strong growth, so attention will be on whether the actual figures can beat expectations.

- Significant Capital Expenditure Increase: Microsoft's Q4 CapEx is projected to exceed $40 billion, with spending around $190 billion for the 2026 calendar year. Goldman Sachs has raised its CapEx estimates for 2028-2030 by approximately 10%, reflecting that investment in AI computing power has not cooled down.

- Copilot Commercialization Yet to Be Verified: M365 Copilot has surpassed 20 million paid seats, but the market's focus is on user engagement, renewal rates, and enterprise spending expansion, which will determine if it can become a sustainable profit source.

- In-House Maia Chip Maturity Insufficient: Maia is still in a catching-up phase and relies on AMD as a second source and supply chain improvements to reduce dependency on GPUs, thereby affecting the unit economics of AI investment.

- Xbox Restructuring Impact Limited: The Xbox layoff of approximately 4,800 employees is a business structure adjustment. Goldman Sachs values it at around $30 billion, but it cannot replace Azure and the AI narrative as the short-term driver of the stock price in the near term.

TL;DR

- Goldman Sachs maintains a Buy rating on Microsoft with a $610 price target, implying approximately 59% upside based on the stock price as of July 9.

- Azure growth remains the key theme of the earnings report, with Goldman Sachs expecting Q4 growth of 40%-41%, higher than the company's previous guidance.

- Higher capital expenditure will amplify the debate on returns, with Copilot monetization, Maia chips, and new capacity deployment yet to materialize.

Goldman Sachs maintained its Buy rating on Microsoft ahead of its Q4 fiscal year-end earnings report on July 29, setting a 12-month price target of $610 while raising its medium-to-long-term capital expenditure expectations. For investors, the earnings focus is not whether Microsoft is an AI winner, but whether Azure can sustain high growth while increasing computing power, and translate higher spending on data centers, chips, and energy into revenue, rather than dragging down free cash flow and margins.

$610 Price Target Rests on Azure Continuing to Exceed Expectations

Market data shows that as of July 9 UTC, Microsoft's stock price was approximately $383.34. Based on this price, the $610 target implies a potential upside of about 59.1%.

This valuation is based on several conditions: sustained high growth in cloud demand, new data center capacity coming online as planned, no internal cannibalization of computing resources between Microsoft's internal AI development and external customer needs, and AI products like Copilot beginning to contribute clearer revenue and profits.

Azure remains the first metric scrutinized in the earnings report.

Microsoft's FY26 Q3 official earnings call showed Azure and other cloud services revenue grew 40% year-over-year, or 39% in constant currency. The company provided Q4 FY26 guidance of 39%-40% constant currency growth, stating that customer demand still exceeds available capacity.

Goldman Sachs' report indicates that Azure's constant currency growth in Q4 could reach 40%-41% year-over-year, with next quarter's guidance potentially remaining in the 40%-41% range. This forecast is slightly above the company's previous guidance, but market expectations are already high. If Microsoft merely delivers cloud growth in line with these high expectations, the stock price may not continue to reward higher AI spending.

Microsoft will also need to explain where the growth is coming from. It could be from new data center capacity coming online, continued expansion of enterprise AI demand, or smoother allocation of computing resources between internal applications and external customers.

In recent quarters, the constraint on Microsoft's AI business has not been a lack of demand, but supply tightness. Azure must serve both external customers like OpenAI and support Microsoft's internal Copilot, MAI model development, and first-party applications. When computing resources are tight, cloud growth is limited by delivery capacity. When capacity deployment is too slow, capital expenditure is first reflected in cash flow and depreciation pressure.

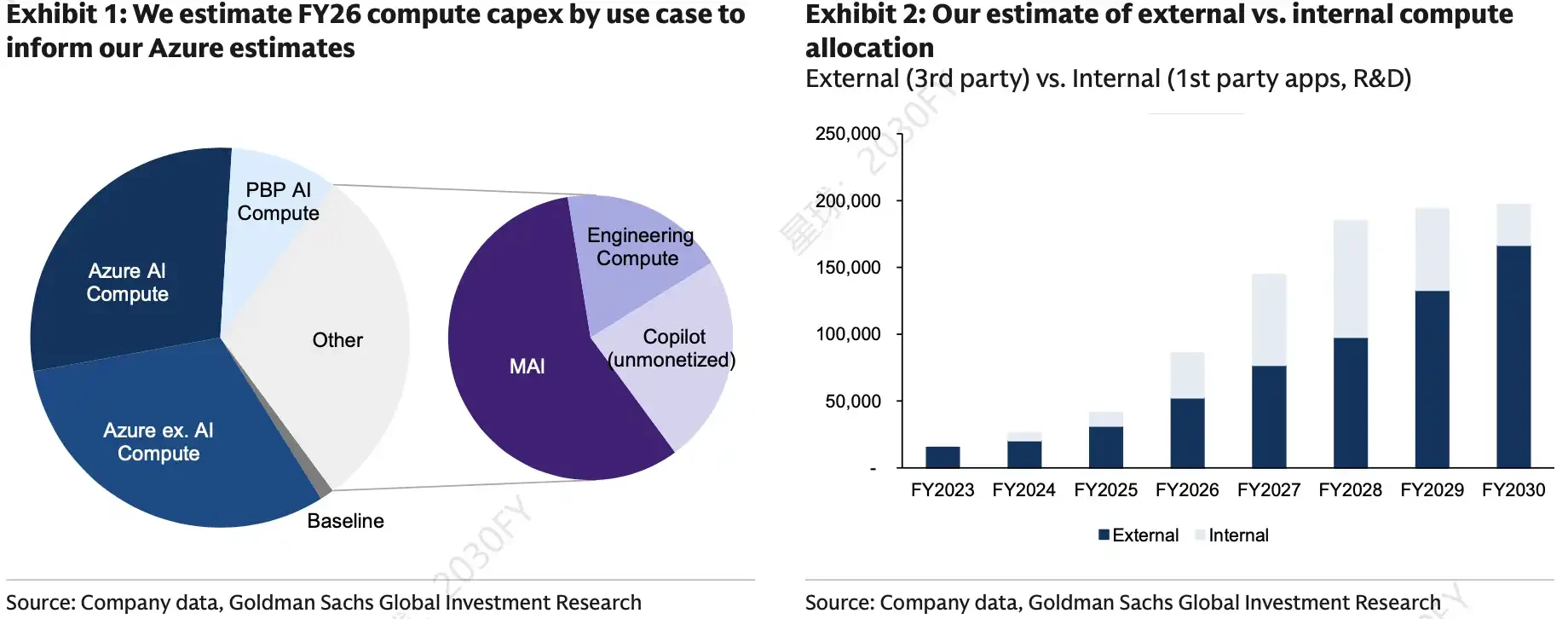

Microsoft FY26 computing capacity spending breakdown by use case and external/internal computing resource allocation. AI computing, MAI, Copilot, etc. account for a high proportion. Internal computing investment has stabilized after rising over the past 12 months, which is key to judging whether Azure can simultaneously support customer demand and internal AI R&D.

Capital Expenditure Continues to Rise, AI Computing Race Hasn't Cooled

Microsoft has already signaled higher spending. FY26 Q3 capital expenditure was $31.9 billion. The company guided Q4 capital expenditure to exceed $40 billion and expects calendar year 2026 capital expenditure to be approximately $190 billion, with about $25 billion stemming from higher component prices.

Goldman Sachs' report states that Microsoft's capital expenditure expectations for fiscal years 2028-2030 have been raised by approximately 10%. According to the report's estimates, the adjusted annual capital expenditure assumptions for certain years are higher than market consensus, reflecting a more aggressive view on Microsoft's future computing power investments.

This is not a choice unique to Microsoft. Guidance from chipmakers like Nvidia, Broadcom, and AMD, as well as capital moves from cloud and internet giants like Google and Meta, indicate that demand for AI computing power has not significantly cooled. Hyperscale cloud vendors are still preparing for years of expansion in data centers, chips, and energy resources.

For Microsoft, high spending has two sides.

On one hand, the Azure and AI product cycle remains a valuation support. Goldman Sachs' report suggests Microsoft's computing capacity could potentially expand to about 40GW by mid-2030. On the other hand, the higher the capital expenditure, the more investors will question whether the new computing power can translate into cloud revenue, AI subscriptions, and higher-margin businesses, rather than just heavier depreciation and cash flow pressure.

Goldman Sachs' report also estimates Microsoft's FY26 revenue at $329.4 billion with EPS of $16.75, and FY27 revenue at $387.1 billion with EPS of $19.32. This forecast implies an assumption that AI investment can both drive revenue and not continuously suppress the pace of profit realization.

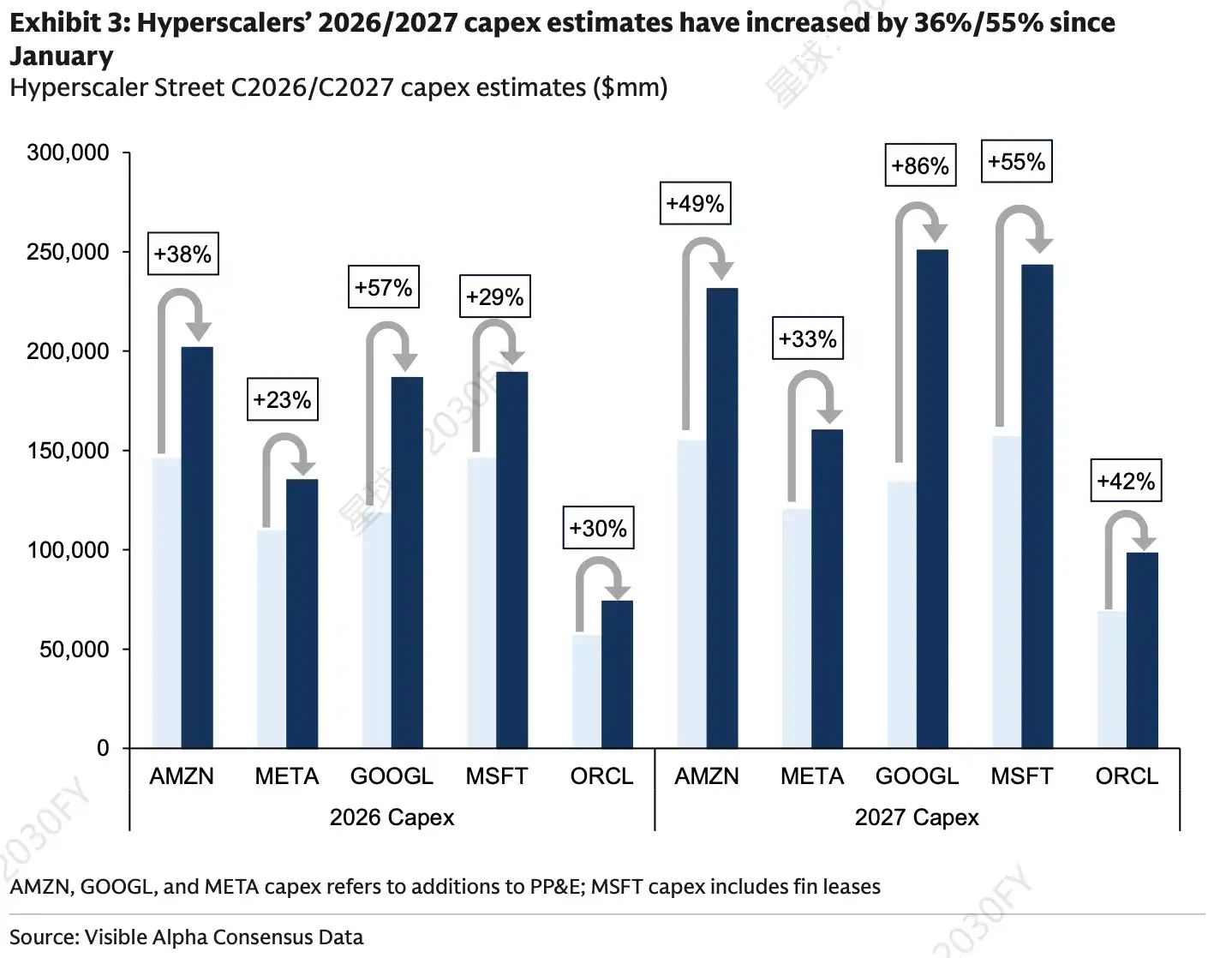

Street expectations for hyperscale cloud vendor capital expenditure in 2026/2027. Since January, capital expenditure expectations for AMZN, META, GOOGL, MSFT, and ORCL have all been significantly raised, with MSFT's 2027 expectation increasing by 55%.

Copilot Monetization and Maia Chip Aim to Reduce GPU Dependency

The success of Microsoft's AI investment ultimately hinges on two key drivers: the commercialization of Copilot and the maturity of its self-developed and alternative chip supply.

Copilot's logic is relatively clear. Increased usage is beneficial for software revenue expansion in the long term and offers opportunities to improve profit structure. However, the short-term issue is that usage volume itself does not equal revenue realization.

Microsoft's FY26 Q3 disclosure showed M365 Copilot paid seats exceeded 20 million. GitHub Copilot is also shifting towards more usage-based and value-based pricing. The company has also introduced fair use terms for high-usage scenarios, attempting to more tightly bind higher inference costs with the payment mechanism.

The market wants to see not just an increase in seat count, but also user engagement, renewal willingness, and actual paid expansion on the enterprise side. If Copilot's user experience and commercialization pace do not improve synchronously, the realization of high-margin AI software will be delayed.

Chips and supply chain represent another track. Microsoft's self-developed AI chip, Maia, is still in a catch-up phase, with maturity lagging behind some peers. Improvements in Maia 300, production progress with AMD as a second source, and memory procurement costs will all affect Microsoft's ability to reduce dependence on the external GPU supply chain.

The company has previously mentioned that new supply needs to be balanced across Azure, first-party applications, R&D, and server replacements. If new supply comes online smoothly, Microsoft can deliver more computing power to external Azure customers while continuing internal AI R&D. If release is uneven, growth in Azure, internal model training, and Copilot inference demand will remain in conflict.

Xbox Restructuring is Peripheral to Valuation

Beyond the main AI theme, Goldman Sachs' report also uses a SOTP method to estimate Microsoft's gaming business value at roughly $30 billion.

On July 6, Microsoft announced a restructuring of its Xbox business. Multiple media reports indicated that Microsoft is laying off approximately 4,800 employees, with about 1,600 from Xbox being cut immediately and another roughly 3,200 within FY27. Four studios—Compulsion, Double Fine, Ninja Theory, and Undead Labs—are leaving the Xbox management structure, and the company has reportedly streamlined some management layers.

This is more of a business structure adjustment than a core earnings trading theme. Microsoft's gaming business still has value, and the restructuring shows the company is cleaning up inefficient assets and shrinking some non-core investments. However, in the short term, it cannot replace Azure, Copilot, and AI capital expenditure returns as the primary factor explaining stock price direction.

According to Goldman Sachs' SOTP valuation, Intelligent Cloud remains the largest contributor to Microsoft's enterprise value. M365 Commercial and Consumer businesses imply an enterprise value of approximately $492 billion, corresponding to about 4x EV/Sales or 6x GAAP EBIT for 2027, which already incorporates some disintermediation risk assumptions.

Realizing the $610 Target Depends on Three Things

The outlook from this earnings preview remains cautiously optimistic: Microsoft is well-positioned in AI computing power, Copilot, and the agent orchestration layer, with opportunities to continue benefiting from the AI product cycle. However, whether the $610 price target materializes depends on whether the earnings report and conference call can provide more verifiable progress.

Azure needs to continue delivering high growth and demonstrate that new capacity deployment can support external customer demand. If growth merely meets already high market expectations, higher capital expenditure could become a point of contention.

Maia 300 and the AMD second source need to show clearer progress. Supply chain tightness, rising memory costs, and insufficient chip maturity will all impact the unit economics of Microsoft's AI investments.

Copilot needs to prove its genuine monetization capability. Over 20 million paid seats are just the starting point. Enterprise-side paid expansion, usage-based billing, and user feedback will determine whether it can evolve from an AI gateway into a profit source.

The key takeaway from Microsoft's earnings is not whether AI investment will continue, but whether higher spending can translate faster into Azure growth, AI software revenue, and sustainable profit margins. If these proofs remain insufficient, the debate over capital expenditure returns will continue to weigh on the stock price.