Opinion: The AI stock market bubble is already here. Why am I turning to bet on Bitcoin instead?

- Core Thesis: The current AI-driven stock market frenzy exhibits classic characteristics of a "bubble top." Based on Howard Marks' cycle theory, the author believes market risks far outweigh opportunities and has thus liquidated tech stock positions to pivot towards bottom-fishing Bitcoin, which offers a wider margin of safety.

- Key Elements:

- Clear Signs of AI Bubble: The market displays a "price is irrelevant" sentiment, with massive capital flooding into a single narrative. The Shiller CAPE Ratio for the stock market has breached 40 for the first time, nearing the peak of the dot-com bubble era.

- Significant Market Disconnect: Under the Fed's tightening cycle, the stock market continued to rally due to AI capital expenditure, fiscal stimuli, and passive fund inflows. However, market breadth is extremely narrow, with AI-related stocks contributing approximately 80% of the gains.

- Risk vs. Opportunity Comparison: The author argues that AI stocks are overvalued, with downside risks greater than upside potential. Conversely, Bitcoin exhibits many characteristics of a "market bottom" (such as negative sentiment and forced selling), offering a safer investment prospect.

- Personal Investment Strategy: The author employs a "three-bucket" allocation, with 70% designated as long-term accumulation capital. Currently holding over 80% cash, they have begun buying spot Bitcoin in batches at an average price of approximately $59,000.

- Other Market Signals: South Korea's KOSPI index triggered two trading halts due to plunging AI stocks. Dalio's bubble indicators are near historical highs, and Buffett holds a record $381 billion in cash, indicating selective risk appetite.

Original Author: Investing Beanstock

Original Translation: TechFlow

Introduction: AI stocks are surging, but this trader is actually liquidating tech stocks and bottom-fishing Bitcoin instead—using Howard Marks' cycle theory to check the current market point by point, he finds that AI already meets almost all characteristics of a "bubble top." For investors, this article provides a冷静 cycle positioning framework to help you decide whether now is the time for greed or fear.

The stock market is experiencing an AI-driven狂野 bull run, which should come as no surprise to anyone.

If you're not holding any positions, you feel like a fool—because capital expenditures (CAPEX) will only continue to rise, and the forward valuations of all these stocks will only become more insane.

I don't intend to comment on specific stocks or indices; banks and financial media worldwide are already covering them extensively. I'm more interested in figuring out—or at least trying to decipher—which stage of the market we are in. Not just crypto, but the entire financial market.

To that end, I've drawn a lot of inspiration from one of my favorite books: Howard Marks' *The Most Important Thing*.

Most people understand a cycle as a sequence of events. Most also understand that these events usually follow each other in a conventional order: a rise is followed by a fall, and then eventually a new rise. But to fully understand a cycle, this is not enough. The events in a cycle should not only be seen as one following another, but more importantly, each is causing the next to happen.

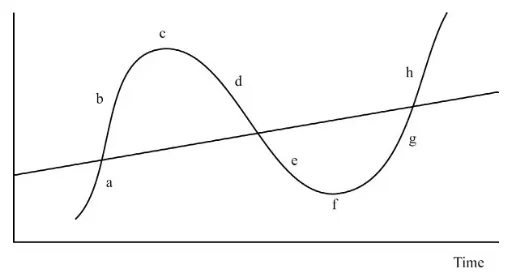

The straight line = the midpoint, and the market's pendulum isthe wave line oscillating around this midpoint. Together, they form the market cycle, driven by various market forces that cause it to deviate from the midpoint from time to time.

The movement of cyclical phenomena can be easily identified in several stages:

a: Recovery from the excessively depressed lower extreme or "low point" towards the midpoint

b: Continuing past the midpoint to swing towards the upper extreme or "high point"

c: Reaching the high point

d: Correcting downwards from the high point back to the midpoint or mean

e: Continuing downward past the midpoint towards a new low

f: Reaching the low point

g: Recovering from the low point back to the midpoint

h: The cycle repeats

So where are we now?

Is this a bubble? I think it's quite obvious by now that AI is indeed a bubble. According to Marks, when the sentiment of "price doesn't matter" is strong, that's a hallmark of a bubble.

In a bubble, investors often conclude that you can make money by borrowing (leverage) to buy the mania asset. Regardless of your loan rate or funding fee, the asset is sure to appreciate faster than that.

"No price is too high" is the ultimate ingredient of a bubble, a rather clear signal that the market has gone too far.

There are actually conflicting schools of thought, believing that the market can trade far above its intrinsic value and still continue to yield multiples due to mania.

What should we do?

Since we are unsure when the bubble will burst, in my view, we have two clear methods for portfolio allocation.

Dollar-cost averaging (I mean real DCA, no timing, you just buy a little bit in a boring, mechanical way. The more batches you split into, the smoother your eventual cost basis becomes. That's the whole point of doing this.)

Heavy cash position, but still allowing yourself to participate in the market through tactical/satellite positions, like active trading.

I personally prefer the second method. But that's because I actively monitor the market day in and day out, relying on my market experience and intuition to navigate it.

DCA is not a bad method either. But it does require an individual to truly extend their time horizon. Not 1 or 3 years, but at least 5 years to truly see some results. Most people DCA for a few weeks, or try to time while DCAing, which ends up counterproductive. If you plan to DCA a specific investment, make sure you fully understand the business/sector, then just stick with it in a super boring, repetitive way and continue with your life.

In my 2025 review and reflection post, I mentioned allocating 25% of my portfolio to passive ETFs, including QQQ, SOXQ, XAR, URA, and UFO. I think a large part of that gain came from QQQ and SOXQ, but I sold all of them in May because I thought the market had gone well past the midpoint.

I also said I was generally bearish on crypto until early 2026 (turned out to be right). I managed to keep a lot of cash and am now patiently deploying a portion of it into BTC. My target accumulation range is $50k-$60k, so I've started allocating at the time of writing.

"Crypto is dead, move to AI"

Honestly, my only regret is not allocating more to the speculative private market exposure in Anthropic and xAI. I believe frontier models still offer the purest AI exposure compared to the public market's "picks and shovels" types, like the GPU/semiconductor/storage narrative. Since those are already the consensus, I don't think chasing them now offers asymmetric upside. That ship has long sailed. Stocks like MU almost 10x'd in a year, while stocks like SNDK basically oscillated like a memecoin. Upside might still be there, but the downside risk looks much worse.

But CAPEX! Yes, this could translate into real value add in the future, but it's still speculative. Excessive speculation, too much money flowing into the same thing. I've seen this movie before.

Is it disappointing tomiss out on a big chunk of the AI bull run? Sure, it stings a bit. But I still have exposure, and it's doubling. I really don't think it's responsible to tell people at today's valuations that AI stocks are actually worth buying, unless they really know what they're doing and are in it for the long term (most aren't; they're here for the quick money).

Market Sanity Checklist

Now, let's get back to how Marks determines if we are approaching/are at the market top:

The economy is growing, economic reports are positive

Corporate earnings are rising and beating expectations

The media only reports good news

The securities market is strong

Investors are becoming increasingly confident and optimistic

Risk is considered scarce and mild

Investors believe taking risk is the path to profit

Greed drives behavior

Demand for investment opportunities exceeds supply

Asset prices exceed intrinsic value

Capital markets are wide open; raising capital or rolling over debt is easy

Defaults are rare

Skepticism is low, confidence is high, meaning risky deals can be done

No one can imagine things going wrong. No positive development seems impossible

Everyone assumes things will get better forever

Investors ignore the possibility of loss, only worrying about missing out

No one can think of a reason to sell, and no one is forced to sell

Buyers outnumber sellers

If the market falls, investors will be happy to buy

Prices reach new highs

The media celebrates this exciting event

Investors become euphoric and carefree

Shareholders marvel at their own smartness: maybe they'll buy more

Those who were on the sidelines feel regret; therefore, they capitulate and buy

^ This means:

Future returns are low (or negative)

Risk is high

Investors should forget about missed opportunities and only worry about losing money

This is the time for caution!

So, how many of these do you think the current stock market is exhibiting?

On the flip side of the "market top" checklist, the opposite scenario can also emerge:

The economy is slowing: reports are negative

Corporate earnings are flat or declining, missing expectations

The media only reports bad news

The market is weak

Investors become worried and沮丧

Risk is seen as being everywhere

Investors believe taking risk is just a way to lose money

Fear dominates investor psychology

Demand for securities is lower than supply

Asset prices are below intrinsic value

Capital markets are closed tight; it's difficult to issue securities or refinance debt

Defaults skyrocket

Skepticism is high, confidence is low, meaning only safe trades can be made, or none at all

No one thinks improvement is possible. No outcome seems too negative to happen

Everyone assumes things will get worse forever

Investors ignore the possibility of missing out, only worrying about losing money

No one can think of a reason to buy

Sellers outnumber buyers

"Don't try to catch a falling knife" replaces "buy the dip"

Prices reach new lows

The media focuses on this depressing trend

Investors become沮丧 and panicked

Shareholders feel stupid and disillusioned. They realize they didn't really understand the reasons behind the investments they made

Those who didn't buy (or sold) feel vindicated and are praised for their smartness

Those who are holding on give up and sell at depressed prices, further fueling the downward spiral

^ This means:

Implied future returns are sky-high

Risk is very low

Investors should forget about the risk of losing money and only worry about missing out

This is the time for aggression!

Based on the checklist above, I do think BTC is exhibiting many of these points (especially the Saylor/MSTR case). So I genuinely feel BTC presents a more attractive investment prospect compared to today's high-flying AI stocks.

However, please note that the above developments are simplifications; they may not even occur in the same order, nor necessarily in every market cycle, but these behaviors are real, and they are indeed the rhyming elements in the market for decades.

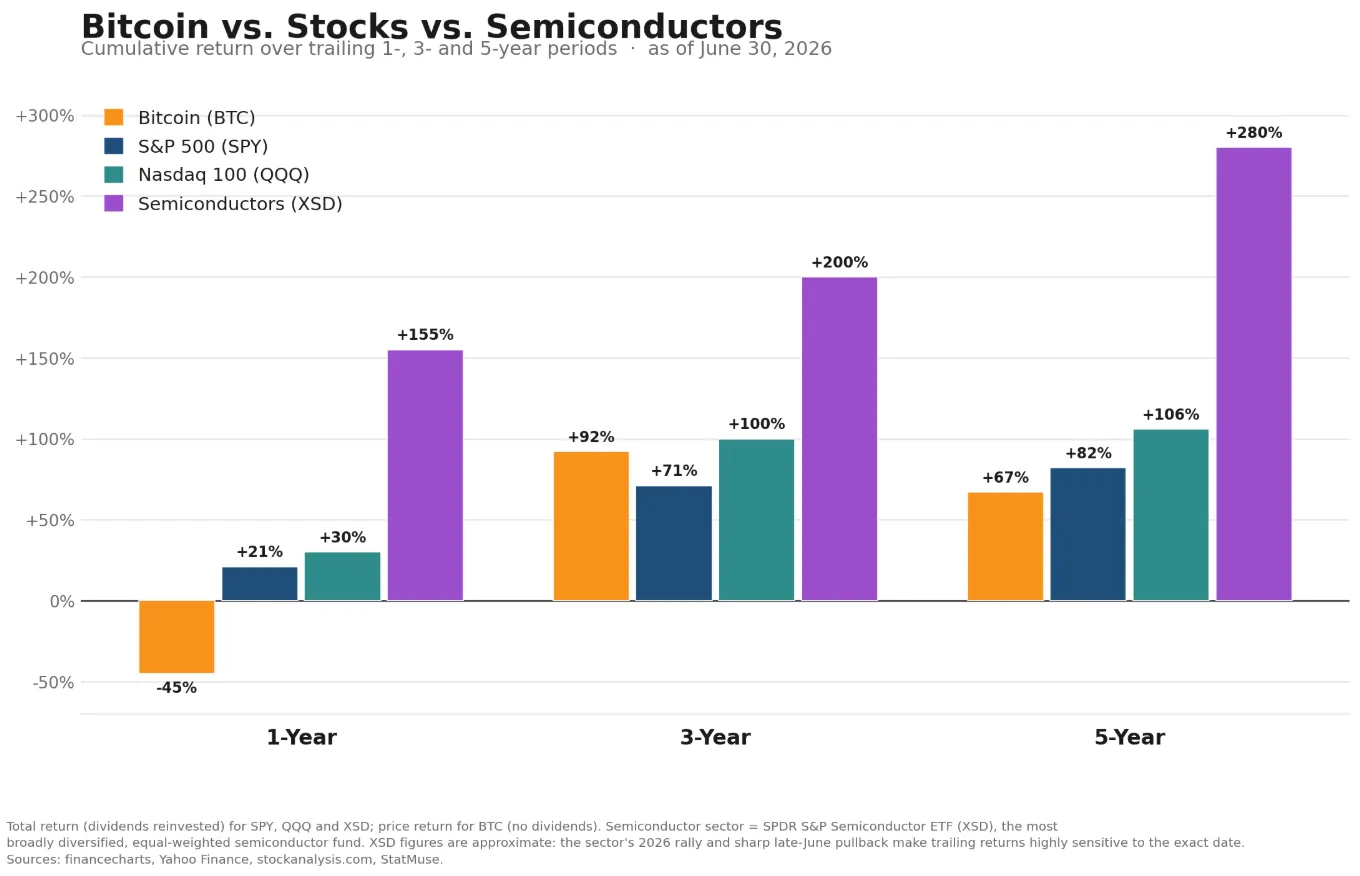

The AI revolution has clearly benefited tech stocks, especially semiconductors, over the 1/3/5 year periods.

But investing is never about looking in the rearview mirror (unfortunately, most people do and draw references from the past); the advantage lies where people overlook/dismiss it. We need to look at "what will happen 1 to 10 years from now," not what the environment is today.

Looking at the chart above, it seems foolish to say you are a crypto investor and should have invested in stocks.

According to the chart above, if you chose stocks, the probability of future underperformance from a statistical standpoint is quite high.

Also, reading this in 2026 might sound like a joke, but based on past cycle experience and understanding of forward returns/valuation fundamentals, I genuinely believe BTC will outperform stocks in the coming years.

The Most Disconnected Macro Environment in History

We are also in one of the most disconnected and irrational market environments ever.

Under the leadership of new Fed Chair Warsh, interest rates are currently maintained at 3.5-3.75%, and he has publicly taken a hawkish stance. But rates haven't compressed, and the stock market continues to rise, simply because AI will cure cancer, and everyone will make infinite amounts of money forever, right?

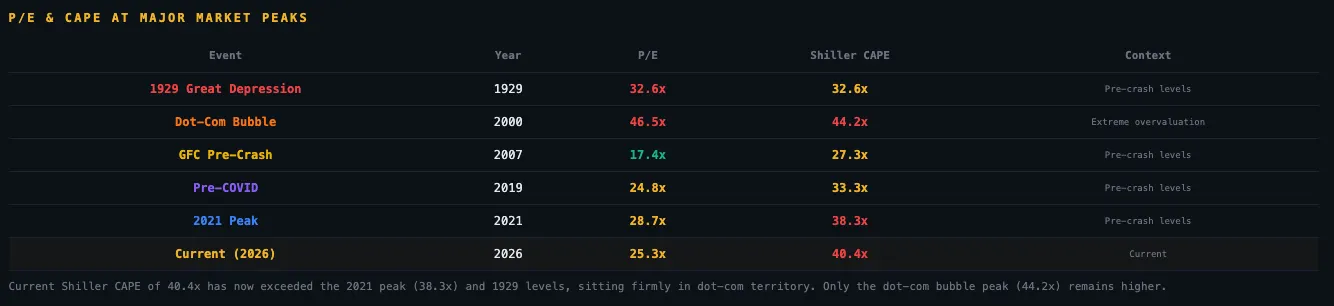

The stock market's cyclically adjusted price-to-earnings ratio (CAPE) has broken above 40 for the first time since the peak of the dot-com bubble era. The U.S. stock market cap is now close to 2 times its GDP, with valuations higher than during the 2000 bubble.

Valuation multiples expanding during a tightening cycle—this is the textbook definition of disconnection.

This disconnect is primarily driven by a three-engine narrative/liquidity machine:

AI CAPEX Super Cycle: Large hyperscalers are spending up to $725 billion in 2026, nearing $1 trillion, now accounting for over 30% of the entire S&P 500.

Late-Cycle Fiscal Stimulus: Lower corporate and personal taxes/tariff rebates are boosting nominal earnings, even as the Fed tightens policy.

Passive Index Fund Flows: Index funds mechanically pour every dollar of 401(k) pension money into the largest market cap companies, regardless of price. Baby boomers are now forced to buy these hyperscaler stocks at all-time highs, and it continues.

Selective Risk Appetite

Today, capital is flooding into the AI/semiconductor sector, while everything else, including Bitcoin (the darling of the last cycle), shows little growth or is bleeding. This is not a market of universal greed, but a market funneling all funds into a single narrative (AI and its related verticals).

In 2025, AI-related stocks accounted for approximately 80% of the entire U.S. stock market's gains. Behind these historic highs, market breadth is extremely narrow;