Meta"s "selling computing power" crashes AI hardware? Wall Street: Don"t panic, this does not equal overcapacity, this is not an industry turning point

- Core Viewpoint: Meta"s plan to lease out excess computing power is not a signal of industry overcapacity, but a pragmatic balance between AI investment and financial returns for the tech giant; this directly impacts new cloud companies like CoreWeave, but provides an EPS buffer for Meta"s shareholders. The trend in AI hardware demand needs confirmation from the earnings season.

- Key Elements:

- Meta is considering offering hosting models/API access or leasing out "raw computing power," leading to a 13% drop in CoreWeave shares and a 15% drop in Nebius, reflecting market concerns over competition and potential downward revisions in capital expenditure.

- Morgan Stanley"s model shows that Meta"s 2027 capital expenditure ($175 billion) will not be revised down due to temporary computing power leasing; if the cloud business is scaled up, it could instead push spending higher.

- Meta"s computing power "surplus" is not equivalent to industry-wide overcapacity; Bernstein points out that news of Google restricting Meta"s computing usage due to capacity constraints suggests the computing power is a matter of "reallocation," not "excess supply."

- UBS believes leasing out computing power can provide near-term revenue for Meta, alleviating the expectation of flat EPS in 2027; each 250MW of computing power leased could generate approximately 8% upside in EPS.

- CoreWeave faces the greatest risk: Meta is a client that accounts for over a third of its contracts. When contracts come up for renewal, Meta could shift from being a demand side to a direct competitor, putting long-term bargaining power under pressure.

- The hardware sector"s decline is primarily due to crowded trades and deleveraging. The inflection point for AI demand will depend on whether cloud vendors" capital expenditures and AI application ARR accelerate during the July-August earnings season.

- Three investment banks maintain a Buy rating on Meta (price targets $775-$865), none have adjusted their valuations based on the computing power leasing, with the core focus remaining on advertising and AI product innovation.

Original author: Long Yue

Original source: Wall Street News

A piece of news about Meta selling off its surplus computing power has simultaneously brought several of the most sensitive issues in the AI trade to the forefront: Is there actually a shortage of computing power? Will Meta revise down its capital expenditure? Can Neocloud continue to be profitable?

As mentioned by Wall Street News, Meta is formulating a cloud business plan that may offer two types of services: one is managed model/API access, similar to AWS Bedrock; the other is leasing "raw computing power," similar to Neocloud.

Upon the release of this news, CoreWeave, a prominent next-generation GPU cloud service provider, saw its stock price plummet by 13%, while Nebius dropped by 15%. Consequently, the AI hardware sector, including chips, suffered a heavy blow. If Meta starts selling computing power, investors will naturally ask three questions:

First, has Meta bought too much computing power?

Second, is Meta reducing its heavy investment in models and AI products?

Third, is the demand curve for AI hardware and Neocloud about to change?

According to information from ZhuiFeng Trading Desk, on July 1st, Wall Street investment banks including UBS, Morgan Stanley, and Bernstein quickly analyzed this event. This might not be a collapse of the AI fundamentals, but rather a pragmatic move by the tech giant to balance computing power constraints with financial returns. This event cannot simply be equated to "Meta no longer needing computing power." However, its implications vary for different assets.

For Meta, leasing computing power could be a transitional bridge for revenue and EPS. UBS judges: "Selling cloud computing power or model access rights could theoretically generate near-term revenue faster than waiting for Meta Business Agents and Meta AI chatbots to scale, and alleviate concerns about flat or contracting EPS in 2027."

For Neocloud companies like CoreWeave, this represents potential competitive pressure.

For the chip and server supply chain, the market is more concerned about the future pace of capital expenditure.

"Having Surplus Capacity to Lease" Does Not Equal "Industry-Wide Oversupply"

The market's shortest chain of reasoning is: Leasing computing power = Oversupply of computing power = Reduction in capital expenditure.

Meta may have temporary computing power available for lease, but this does not automatically mean there is an industry-wide oversupply. Different institutions use different capacity metrics, which cannot be directly summed.

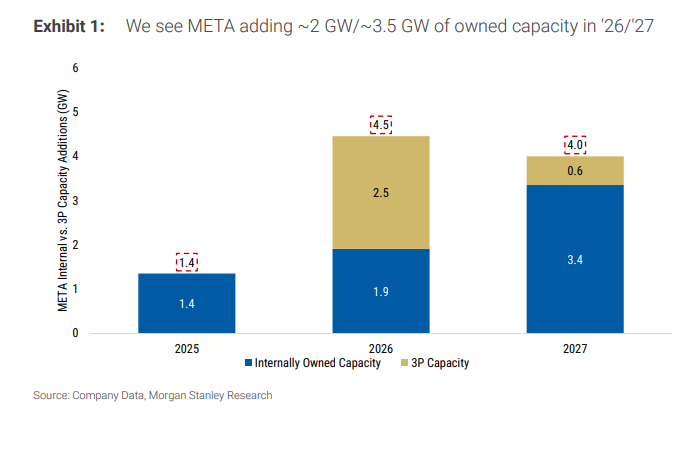

In Morgan Stanley's model, Meta is expected to add approximately 2GW and 3.5GW of owned IT capacity in 2026 and 2027, respectively, with a baseline of about 3GW by the end of 2025. For comparison, hyperscale cloud providers like Amazon and Google are expected to add 5GW and 9GW of new IT capacity in 2027, respectively. In other words, even if Meta allocates a portion of its owned capacity for external leasing, it is difficult for this alone to change the overall landscape of cloud provider construction over the next three years.

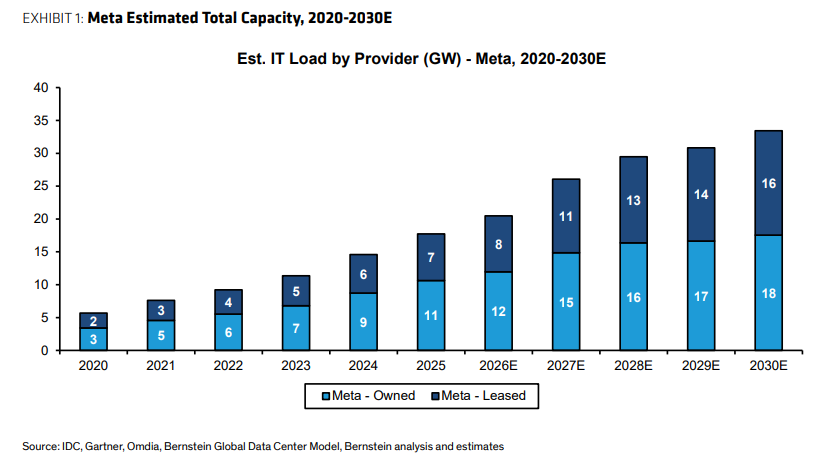

Bernstein uses a broader metric of total data center footprint: Meta currently has an estimated global capacity of about 20GW, and plans to bring approximately 14GW more online in the coming years, comprising a mix of owned and leased capacity. While this number appears large, it is not "all rentable AI computing power," nor does it represent the same generation of GPUs, the same type of workload, or the same pricing curve.

Market calculations also include a more aggressive extrapolation: using contracts and capacity plans like Google with Anthropic, AWS with Anthropic/OpenAI, and Microsoft with OpenAI as anchors, the total AI computing power of several cloud providers in the future could be around 20GW or even higher. OpenAI's own Stargate, as well as the 10GW-level arrangements related to Nvidia and Broadcom, are also factored into the demand side. The purpose of this metric is not precise prediction but to illustrate one point: Meta's localized leasing does not prove that global AI construction has entered a phase of oversupply.

More counter-intuitively, Bernstein also mentioned that over the weekend, there was news that Google limited Meta's computational usage due to its own capacity constraints. If this claim holds, Meta is simultaneously trying to secure external computing power while preparing to sell a portion of its own in the future. This looks more like a reallocation based on "different generations, different use cases, different time windows" rather than simply "having too much."

This Is Not the First Time Meta Has Put "Selling Computing Power" on the Table

On May 27, 2026, a shareholder asked Meta whether it would build a cloud business to compete with AWS, Azure, etc. Zuckerberg replied:

"Of course, that's certainly something we think about... We haven't done it because we think we can use this computing power ourselves. But obviously, if we get to a point where we feel we've overbuilt, it's an option we have. And that's part of the reason we're confident to keep investing."

Earlier, on October 29, 2025, Zuckerberg discussed a similar logic:

"For any computing power we don't need, we're pretty confident we can absorb a very large portion of it... Of course, we might overbuild. If that happens... we see a lot of new demand, both internally and externally. Almost every week, people from outside the company approach us, asking if we can build an API service, or they ask if they can get different types of computing power from us. We haven't done that yet. But obviously, if you get to a stage of overbuilding, it can become an option."

This explains why UBS calls it "not new news."

For Meta Shareholders, Selling Computing Power is More Like an "EPS Bridge," Not a New Core Business

For Meta, the most straightforward benefit of leasing computing power is converting long-term AI investments into near-term revenue.

In UBS's table, Meta's diluted EPS for 2026 and 2027 is approximately $32.6 and $33.0, respectively. The market is concerned that 2027 EPS might be flat or even compressed compared to 2026. Leasing computing power or selling model access rights could provide a revenue and profit buffer before Meta Business Agents and Meta AI chatbots truly scale.

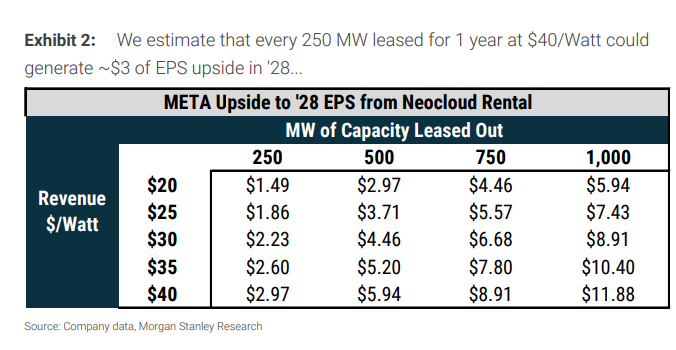

Morgan Stanley's sensitivity analysis is more intuitive: leasing 250MW of computing power for one year at a price of $40/Watt could potentially add about $2.97 to Meta's 2028 EPS, roughly an 8% upside. If capacity expands to 500MW, 750MW, or 1000MW, or if the price differs, the EPS elasticity would scale up or down accordingly.

This is why the market hasn't interpreted it solely as bad news. From a Meta shareholder's perspective, Zuckerberg has essentially added another plan B: if internal AI products can't consume all the computing power in the short term, he can sell it to external AI labs first and recoup some of the investment.

The market also draws an analogy to xAI leasing computing power to Anthropic: 500MW corresponds to $1.25 billion per month, or approximately $30 billion/GW/year. If this pricing holds, the implied return is very high, suggesting that high-quality computing power is still tight in some scenarios. It's not evidence that "no one wants computing power," but evidence that "idle windows can be snapped up at high prices."

However, this can only be called a bridge, not the main story. Morgan Stanley still places the key to Meta's valuation on front-line product innovation: whether Meta AI, business agents, messaging, diffusion offerings, subscriptions, etc., can drive more sustained engagement and revenue growth. Selling computing power can supplement EPS but won't automatically lift the valuation multiple.

Capital Expenditure May Not Be Revised Down; Building a Full Cloud Could Actually Be More Costly

The market's biggest fear is that Meta will revise down its 2027 capital expenditure, causing the entire AI hardware chain to lower expectations.

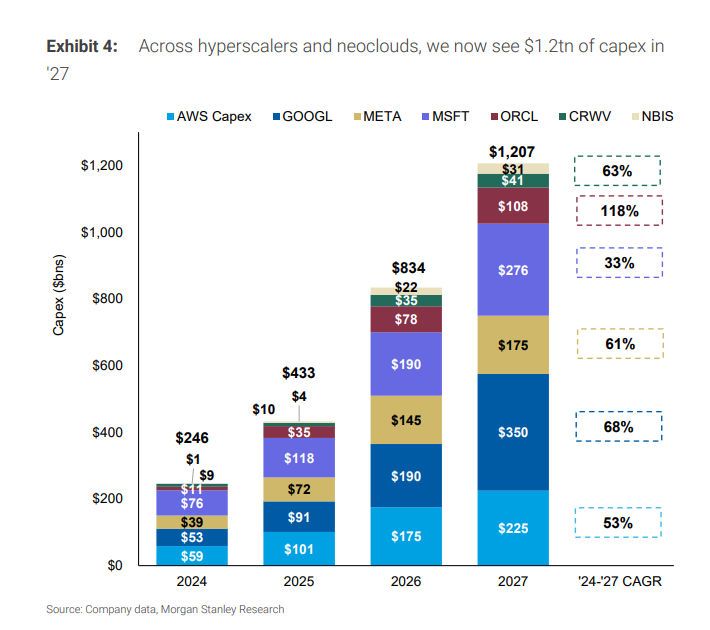

However, Morgan Stanley's current model assumes Meta's capital expenditure will rise from $145 billion in 2026 to $175 billion in 2027 and $205 billion in 2028. The premise of this model is that Meta is primarily building capacity for its own front-line products rather than creating a complete hyperscale cloud service provider.

If Meta actually scales up its external cloud services, especially by building a model/API platform rather than just temporarily leasing raw computing power, capital expenditure could face upward pressure. A full-fledged cloud business requires longer-term data center capacity, more complex software platforms, and the ability to deliver to enterprise clients.

Bernstein also frames this issue in the context of post-2027. Meta is one of the most important "checkbooks" in the AI market, and any change in its construction pace will affect the supply chain. However, "temporary leasing" has different implications for capital expenditure than "permanent expansion of the cloud business," and the two should not be conflated.

A larger demand driver remains inference and agent applications. A market review by HY Computing & AI Power cited OpenAI's recent article on Codex/agentic AI as a demand signal: the number of non-developer individual users grew 137 times, organizational users grew 189 times, and internal OpenAI users grew 12 times. This perspective emphasizes that the expansion of new use cases may continue to drive demand for inference computing power.

So the crux of this divergence isn't "whether Meta will sell computing power," but whether the AI demand curve is still steepening. If overseas ARR accelerates, inference applications grow, and cloud provider capex continues to be revised upwards, Meta's leasing looks more like periodic asset monetization. If the next earnings season brings widespread downward revisions in capex, then this event will become a signal of an industry inflection point.

Selling Raw Computing Power is Easy; Building a Full AI Cloud is Very Hard

Meta's potential business has two paths, with vastly different difficulty levels.

The first path is selling "raw computing power" or bare chip capacity, similar to a neocloud. Customers buy GPU/computing resources, and Meta doesn't immediately need to provide a complete suite of enterprise software, developer tools, model platforms, and sales systems.

The second path is offering managed model/API access, similar to AWS Bedrock or Google Vertex AI. This is not a business you can run just by having "data centers and chips." It requires robust model capabilities, a software stack, a developer experience, enterprise customer sales, and service support.

Morgan Stanley's model is more cautious about the second path. It notes that Meta's Muse model family hasn't performed exceptionally well on TerminalBench and SWE Bench Verified, benchmarks which relate to coding abilities and third-party usage scenarios. If Meta wants to compete with frontier models like Gemini, subsequent models need significant improvement.

This is also why the deduction "Meta selling computing power = Meta exiting the model game" is unstable. Potential plans already include model/API access. Front-line products like Meta AI, business agents, messengers, diffusion offerings, and subscription revenue remain the core of long-term valuation. The issue isn't whether Meta will do models, but whether it can build model capabilities into a cloud service that external customers are willing to pay for.

Some market discussions also point to Muse Spark, the closed-source strategy, and management adjustments as evidence that Meta is still a player in the model game. However, these are better suited as follow-up items. At least based on the three frameworks, a more certain conclusion for now is: the execution barrier for selling raw computing power is low, but the barrier for building a full-stack AI cloud is high.

Is CoreWeave the Biggest "Victim"? Clients Turn into Potential Competitors

The immediate impact fell most directly on new cloud/GPUaaS companies like CoreWeave.

Bernstein gives CoreWeave an Underperform rating with a price target of $67, while rating Meta as Outperform with a target of $850. Its logic is straightforward: If Meta offers cloud infrastructure externally, it could directly compete with CoreWeave.

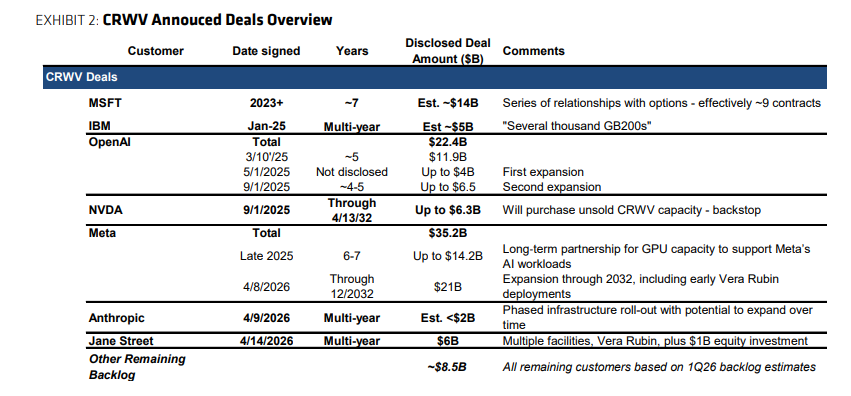

Compounding the problem, Meta itself is a major customer of CoreWeave. According to Bernstein, Meta currently has $35.2 billion in contracts with CoreWeave, accounting for over a third of CoreWeave's order backlog. Combined with Microsoft's approximately $14 billion in contracts, nearly half of CoreWeave's orders come from clients who might become competitors upon future contract renewals.

Short-term risk is less direct. Existing contracts have strong commitments, making it difficult for clients to exit immediately. Therefore, CoreWeave's short-term revenue and debt pressures may not worsen instantly.

The long-term problem is more difficult to handle. If clients build their own clouds and sell their own computing power, the bargaining power of new cloud companies will decline. Especially during renewals, CoreWeave will face not just a demand side, but a potential supply side with money, technology, and data center experience.

JPMorgan's trading desk noted that the market's reaction to CRWV falling 13% and NBIS falling 15% is relatively easy to understand: Meta transformed overnight from a client into a potential competitor. For chip hardware, the impact is more indirect; for GPUaaS, the impact feels more like a business model stress test.

Why Hardware Fell First: Fundamentals Aside, There's Crowded Positioning

From a short-term trading perspective, the market isn't just trading on fundamentals.

JPMorgan's trading desk debate splits into two sides: one side asks whether the Meta news represents a shift in the narrative about CSP capital expenditure and AI computing demand; the other side points to overly crowded positioning, with deleveraging and profit-taking amplifying the decline. They lean towards the latter being more important, and that the real judgment on whether fundamentals have shifted will come from the upcoming earnings season language.

The positioning backdrop is not light. With major index rebalancing just passed, total flow and leverage are starting from a high base. Over the past four weeks, increases in both long and short positions have been at +2 standard deviations. Historically, hedge fund deleveraging has often occurred in July over the past five years, with changes typically ranging from -1 to -3 standard deviations. Semiconductor and memory positioning is near the 100th percentile.

This explains why a single piece of Meta news could hit the entire AI hardware chain. When a crowded trade meets a narrative like "computing power might not be scarce," it's easy to sell first and ask questions later. On that day, the rise of software, crowded shorts, and Chinese ADRs by over 1.4 standard deviations also fits the pattern of short covering during a deleveraging process.

Signals for a potential reversal include several key factors the market is watching: Whether Meta clarifies the news; whether overseas AI application ARR accelerates; whether cloud provider capex continues to be revised upwards; and whether Q2 results beat expectations. The timeline is concentrated from July to August. For now, it